Inheritance Tax 2026: 6 States + Pay $0 Guide

Only 6 U.S. states charge inheritance tax in 2026: Iowa, Kentucky, Maryland, Nebraska, New Jersey, Pennsylvania. Discover rates, exemptions, and 7 proven strategies to pay $0 legally.

In This Article

Only 6 U.S. states charge inheritance tax in 2026: Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. If you live in the other 44 states, your heirs pay zero state inheritance tax when they inherit from you. The federal government also imposes no inheritance tax—though estates over $13.99 million face federal estate tax.

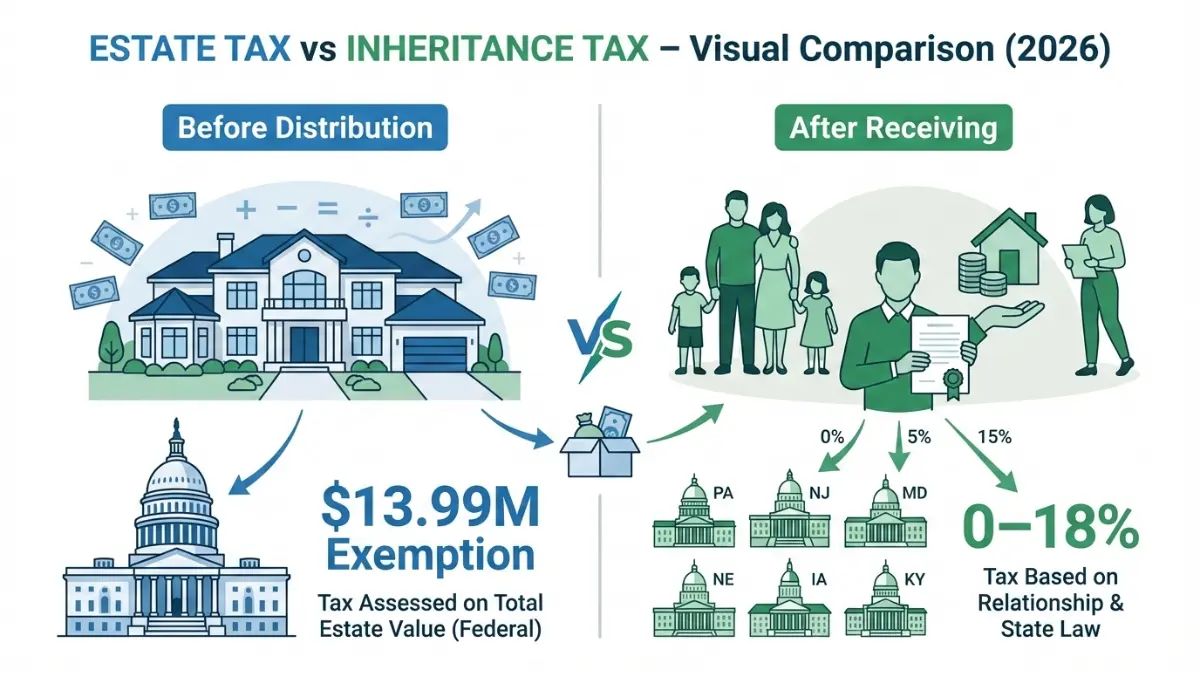

Here’s the critical distinction: inheritance tax is paid by the beneficiary who receives assets, while estate tax is paid by the deceased person’s estate before distribution. This guide shows you exactly how to navigate both and, in many cases, pay $0.

What You’ll Learn:

- Complete breakdown of all 6 inheritance tax states and their rates

- Estate tax vs inheritance tax: why the difference matters for your planning

- 2026 federal exemption updates ($13.99M) and state threshold changes

- 7 proven strategies to legally reduce or eliminate inheritance tax

- Real calculations showing exactly what you’d pay in each state

Who This Affects:

You need this information if you’re inheriting assets from someone in Iowa, Kentucky, Maryland, Nebraska, New Jersey, or Pennsylvania—or if you live in these states and want to protect your heirs from unnecessary tax burdens.

Whether you’re planning your estate or recently received an inheritance, understanding these 2026 tax brackets will help you make informed decisions that could save your family tens of thousands of dollars.

The 6 States with Inheritance Tax (Deep Dive)

Which States Have Inheritance Tax in 2026?

Unlike income tax or property tax, inheritance tax exists in only a handful of states—and that number continues shrinking. Here’s the complete 2026 list with current status:

The 6 States:

- Iowa (phase-out scheduled—fully eliminated by 2025, verify current status)

- Kentucky (0% to 16% depending on relationship)

- Maryland (0% to 10%, only state with both inheritance AND estate tax)

- Nebraska (1% to 18% based on beneficiary class)

- New Jersey (0% to 16% for distant relatives)

- Pennsylvania (0% to 15%, among the highest rates)

State-by-State Breakdown Table

| State | Tax Rate Range | Spouse Exempt? | Children Exempt? | Siblings Rate | 2026 Change |

|---|---|---|---|---|---|

| Iowa | 0-15% | ✅ Yes | ✅ Yes | 5-10% | Phase-out continuing |

| Kentucky | 0-16% | ✅ Yes | ✅ Yes | 4-16% | Rates unchanged |

| Maryland | 0-10% | ✅ Yes | ✅ Yes* | 10% | *$50K child exemption new |

| Nebraska | 1-18% | ✅ Yes | ✅ Yes | 13-18% | Inflation-adjusted |

| New Jersey | 0-16% | ✅ Yes | ✅ Yes | 11-16% | Thresholds updated |

| Pennsylvania | 0-15% | ✅ Yes | ❌ No (4.5%) | 12% | No changes |

Who Pays vs. Who’s Exempt

Inheritance tax operates on a relationship-based system. The closer your relationship to the deceased, the lower your tax—or complete exemption.

Always Exempt (All 6 States):

- Surviving spouses pay zero inheritance tax

- Charitable organizations receive 100% tax exemption

- Government entities are fully exempt

Usually Exempt:

- Direct descendants (children, grandchildren) in most states

- Parents inheriting from children in several states

Highest Tax Brackets:

- Siblings typically face 10-18% rates

- Nieces, nephews, cousins pay top rates (11-18%)

- Unrelated beneficiaries hit maximum brackets

Real Example: $500K Inheritance Calculation

Let’s examine a concrete scenario in Nebraska, which has among the highest rates:

Scenario: Your uncle in Nebraska passes away and leaves you (his nephew) $500,000.

Calculation:

- Relationship class: Distant relative

- Nebraska rate for nephews: 13% (first $15,000) to 18% (over $15,000)

- Exemption: $15,000

- Taxable amount: $485,000

- Tax owed: $87,300

With Proper Planning: If your uncle had used estate planning strategies like an irrevocable trust or annual gifting (discussed in Section 5), that $87,300 could have been reduced to zero.

Compare this to the federal estate tax regulations from the IRS, which only applies to estates exceeding $13.99 million—far above what most families face.

Estate Tax vs Inheritance Tax

Estate Tax vs Inheritance Tax: Critical Differences

The most common confusion in estate planning? Thinking estate tax and inheritance tax are the same thing. They’re not—and understanding the difference could save your family hundreds of thousands of dollars.

Side-by-Side Comparison

| Factor | Estate Tax | Inheritance Tax |

|---|---|---|

| Who Pays? | The deceased’s estate (before distribution) | Individual beneficiaries (after receiving assets) |

| Federal or State? | Both federal ($13.99M threshold) + 12 states | State only (6 states) |

| Tax Rate | 18-40% federal; varies by state | 0-18% depending on relationship |

| Exemption | $13.99M per person (2026) | Varies by state and relationship |

| Filing Deadline | 9 months after death | Typically 9-12 months (state-specific) |

| When Calculated | Before assets distributed | After assets received |

Can You Owe Both Taxes?

Yes—but only in Maryland, the sole state imposing both estate and inheritance taxes simultaneously.

Example Scenario: A Maryland resident dies with a $5 million estate, leaving assets to a sibling.

Dual Taxation:

- Estate tax applied first at state level (Maryland estate tax threshold is $5 million)

- Inheritance tax calculated on sibling’s share after estate tax paid

- Combined effective rate can exceed 20%

For estates facing both taxes, advanced planning using strategies like qualified personal residence trusts or family limited partnerships becomes essential. Understanding these distinctions is as critical as knowing your income tax bracket for retirement planning.

Which Tax Affects You? Quick Assessment

Check Estate Tax Risk If:

- Total estate value exceeds $13.99 million (federal)

- You live in one of 12 states with state estate tax

- You own substantial real estate, business interests, or investment portfolios

Check Inheritance Tax Risk If:

- You’re inheriting from someone in the 6 inheritance tax states

- Your relationship to deceased is sibling or more distant

- You’re receiving over $15,000-$40,000 (varies by state)

Both Apply If:

- Inheriting in Maryland from a large estate

- Estate exceeds federal exemption AND you’re in an inheritance tax state

The IRS provides comprehensive guidance on federal estate and gift tax regulations to help you determine your exposure.

2026 Exemptions & Thresholds

2026 Inheritance Tax Exemptions & Federal Updates

Tax thresholds change annually with inflation—and 2026 brings significant updates you need to know.

Federal Estate Tax Exemption 2026

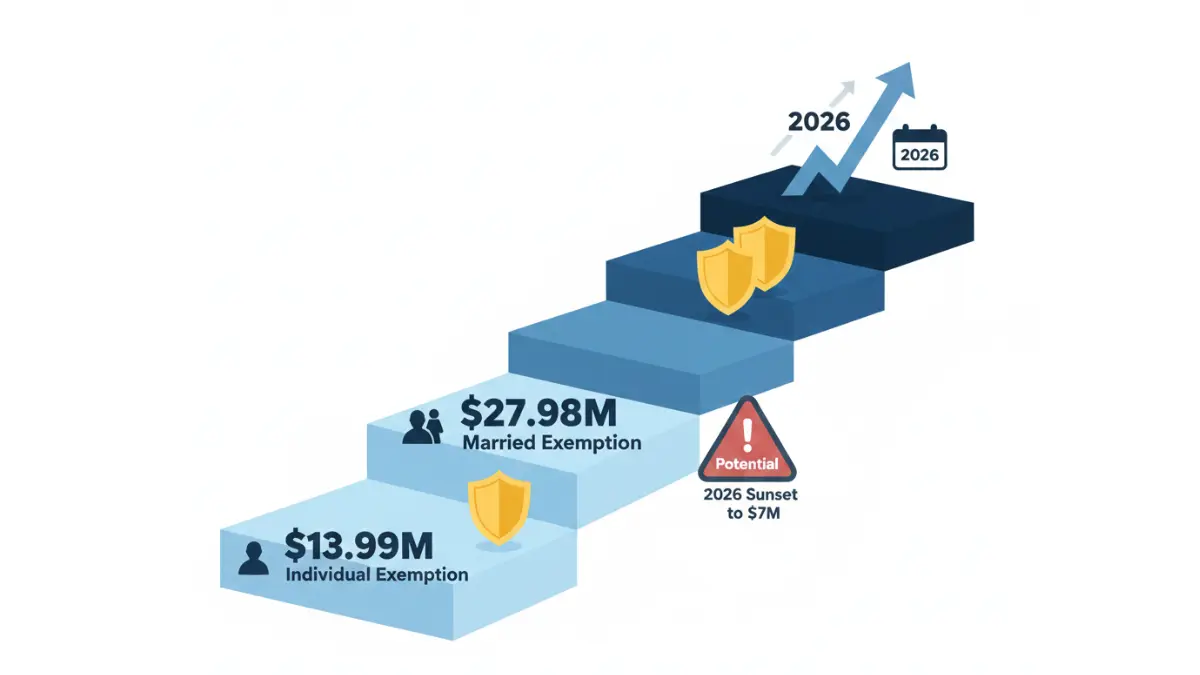

The federal estate tax exemption rose to $13.99 million per individual for 2026, up from $13.61 million in 2025. Married couples can combine exemptions for a total $27.98 million shield through portability.

Critical 2026 Sunset Warning: Current exemptions expire December 31, 2025, under the Tax Cuts and Jobs Act. Without congressional action, the exemption could drop to approximately $7 million (inflation-adjusted from the pre-2018 $5 million level) starting January 1, 2026.

Planning Window: If you have an estate approaching $7-14 million, the next 10 months represent a crucial planning window. Strategies like spousal lifetime access trusts (SLATs) or accelerated gifting can lock in the current higher exemption before potential reduction.

State Exemption Changes for 2026

| State | 2025 Exemption (Children) | 2026 Exemption | Change |

|---|---|---|---|

| Maryland | $0 | $50,000 | +$50K NEW |

| Nebraska | $40,000 | $40,000 | Unchanged |

| Iowa | Varies | Phase-out | Elimination path |

| Kentucky | $0 (exempt) | $0 (exempt) | Exempt |

| New Jersey | $25,000 | $25,000 | Unchanged |

| Pennsylvania | $0 (4.5% tax) | $0 (4.5% tax) | Unchanged |

Maryland’s New $50,000 Child Exemption: Maryland became more generous in 2026, now exempting the first $50,000 inherited by direct descendants. For a child receiving $200,000, this saves approximately $5,000 in tax.

Annual Gift Tax Exclusion

The IRS gift tax annual exclusion remains $18,000 per recipient for 2024-2026.

Strategic Application:

- Gift $18,000 annually to unlimited recipients

- Reduces your taxable estate by $18,000 per gift

- No gift tax return required for amounts under $18,000

Example: Gift $18,000 to each of 5 children annually = $90,000 estate reduction per year. Over 10 years: $900,000 removed from taxable estate with zero tax consequences.

Unlimited Exceptions:

- Medical expenses paid directly to healthcare providers

- Educational tuition paid directly to institutions

- Both avoid gift tax regardless of amount

Similar to maximizing tax refund strategies, proper gift timing can substantially reduce your family’s tax burden.

Step-Up in Basis Advantage

Inherited assets receive a “step-up” to fair market value at the date of death, eliminating capital gains tax on appreciation during the deceased’s lifetime.

Example:

- Stock purchased 1990: $100,000

- Value at death 2026: $500,000

- Heir sells immediately: $0 capital gains tax on $400,000 appreciation

This benefit, combined with inheritance tax planning, creates powerful wealth transfer opportunities for families—similar to how Roth IRA accounts provide tax-free growth for retirement savings.

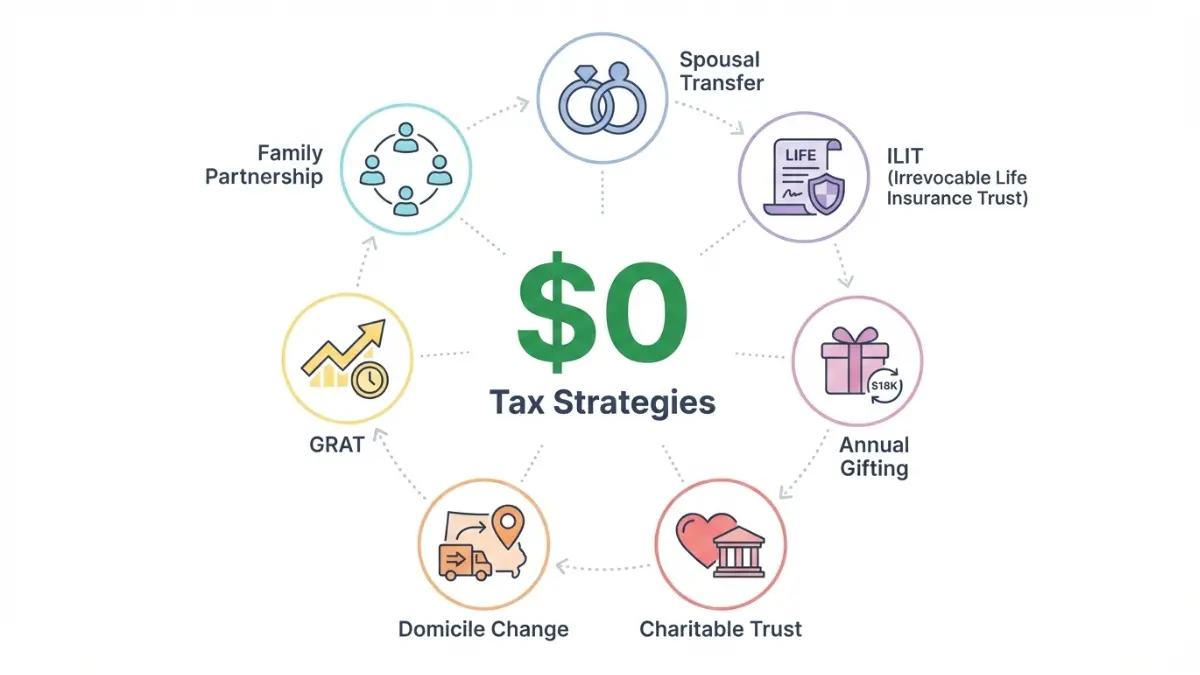

Pay $0 Inheritance Tax Strategy Guide

How to Pay $0 in Inheritance Tax: 7 Proven Strategies

Legal tax minimization isn’t just possible—it’s expected by tax law. Here are seven strategies estate attorneys use to eliminate or drastically reduce inheritance tax burdens.

Strategy 1: Spousal Transfer (Unlimited Marital Deduction)

How It Works: All 6 inheritance tax states fully exempt spouse-to-spouse transfers. Federal law provides unlimited marital deduction for estate tax as well.

Action Steps:

- Ensure beneficiary designations name spouse as primary

- Update retirement accounts, life insurance policies

- Review trust documents for marital deduction language

Limitation: This strategy defers tax to the second death. When the surviving spouse dies, their estate includes previously inherited assets.

Best For: Married couples with combined estates under $27.98 million seeking maximum flexibility.

Strategy 2: Irrevocable Life Insurance Trust (ILIT)

How It Works: Life insurance proceeds typically bypass inheritance tax when paid directly to beneficiaries, but they can inflate the estate for estate tax purposes. An ILIT removes the policy from your taxable estate entirely.

Real Example: $2 million life insurance policy owned by ILIT = $2 million removed from estate. At 40% federal estate tax rate, saves $800,000 in estate tax.

Requirements:

- Trust must be irrevocable (you cannot change it)

- Three-year look-back rule (transfer policies at least 3 years before death)

- Trustee manages distributions to beneficiaries

Setup Cost: $2,000-$5,000 attorney fees

Best For: High-net-worth individuals with substantial life insurance policies who want to maximize inheritance to heirs.

Strategy 3: Annual Gifting Strategy

How It Works: Use the $18,000 annual gift tax exclusion to systematically reduce your taxable estate over time.

Power of Compounding Gifts:

- 4 children × $18,000 = $72,000 annual estate reduction

- Both spouses can gift: $72,000 × 2 = $144,000 combined

- Over 10 years: $1.44 million removed from estate

- Tax saved at 18% inheritance tax rate: $259,200

Documentation: Keep detailed gift records. For gifts over $18,000, file IRS Form 709 even if no tax is owed.

Best For: Individuals with liquid assets who want to see their wealth benefit heirs during their lifetime, similar to building an emergency fund proactively.

Strategy 4: Charitable Remainder Trust (CRT)

How It Works: Transfer assets to an irrevocable trust that pays you income for life or a term of years, then distributes the remainder to charity. You receive immediate charitable deduction, reducing estate value.

Example:

- Transfer $1 million to CRT

- Receive 5% annual income ($50,000) for 20 years

- Total income: $1 million

- Remainder to charity: $1 million

- Estate reduction: $1 million

- Charitable deduction: Immediate tax benefit

Tax Benefits:

- Income tax deduction in year of contribution

- Estate tax reduction

- May avoid capital gains on appreciated assets transferred to trust

Best For: Charitably-inclined individuals seeking income plus estate tax reduction.

Strategy 5: Domicile Change to Non-Inheritance Tax State

How It Works: Inheritance tax is based on the deceased’s state of residence, not the beneficiary’s location. Relocating to one of 44 states without inheritance tax eliminates the liability entirely.

Requirements for Valid Domicile Change:

- Physical presence in new state (typically 183+ days/year)

- Update driver’s license and vehicle registration

- Register to vote in new state

- File state tax returns in new state

- Change mailing address, bank accounts

- Purchase or lease residence

Savings Example: Pennsylvania resident with $3 million estate, heirs are siblings:

- Inheritance tax liability: $360,000 (12% rate)

- After moving to Florida: $0

IRS Scrutiny: Changes made shortly before death may face challenge. Establish new domicile at least 2-3 years before death for strongest position. This is similar to how mortgage pre-approval requirements demand documented financial history.

Best For: Retirees with flexibility to relocate to tax-friendly states like Florida, Texas, Nevada, or Tennessee.

Strategy 6: Grantor Retained Annuity Trust (GRAT)

How It Works: Transfer appreciating assets to an irrevocable trust, retain the right to receive annuity payments for a term of years, and pass remaining appreciation to heirs tax-free.

Example:

- Transfer $1 million stock portfolio to 5-year GRAT

- Stock appreciates 8% annually to $1.47 million

- You receive annuity payments totaling $1 million over 5 years

- Appreciation of $470,000 passes to heirs gift-tax-free

Risk: If you die during the GRAT term, assets return to your estate. For this reason, GRATs work best for younger individuals or those using short terms (2-3 years).

IRS Requirements: Must use IRS-prescribed interest rates (Section 7520 rate) for calculations. Current low interest rates make GRATs particularly effective in 2026.

Best For: Individuals under 70 with rapidly appreciating assets (stocks, business interests, real estate).

Strategy 7: Family Limited Partnership (FLP)

How It Works: Pool family assets (typically real estate or business interests) into a partnership structure, then gift limited partnership interests to heirs at discounted values.

Valuation Discounts:

- Lack of marketability: 20-35% discount

- Lack of control (limited partner): 10-25% discount

- Combined discounts: Often 30-40%

Example:

- FLP holds $2 million real estate

- Gift 50% limited partnership interest to children

- Interest valued at $700,000 after 30% discount (not $1 million)

- Tax savings: 30% reduction in taxable transfer = approximately $120,000 at 40% estate tax rate

IRS Requirements:

- Must have legitimate business purpose (not solely tax avoidance)

- Follow partnership formalities (meetings, separate bank accounts, distributions based on ownership)

- Avoid “family piggy bank” treatment

Recent Cases: IRS has successfully challenged FLPs lacking business purpose. Work with experienced estate attorney to ensure compliance.

Best For: Families with significant real estate holdings, operating businesses, or investment portfolios who want multi-generational control and tax efficiency—similar to how debt consolidation strategies require careful structuring for maximum benefit.

Additional Resources: The National Association of Estate Planners & Councils provides educational resources on advanced estate planning techniques, while state-specific guidance is available through your state’s Department of Revenue website.

Advanced Considerations & FAQs

Advanced Inheritance Tax Considerations

Generation-Skipping Transfer Tax (GSTT)

When you leave assets directly to grandchildren, “skipping” your children’s generation, you may trigger the generation-skipping transfer tax in addition to estate or inheritance tax.

2026 GSTT Exemption: $13.99 million (same as estate tax exemption)

Tax Rate: Flat 40% federal rate on transfers exceeding exemption

Strategy: Allocate GSTT exemption to trusts benefiting grandchildren early in life to maximize tax-free growth. A $1 million allocation growing at 7% for 30 years becomes $7.6 million passing tax-free to grandchildren.

Non-U.S. Citizen Beneficiaries

Special rules apply when inheritance involves non-citizens.

Non-Citizen Spouse:

- No unlimited marital deduction (limited to $175,000 for 2026)

- Solution: Qualified Domestic Trust (QDOT) allows deferral until distributions made

- QDOT requires U.S. trustee and meets IRS requirements

Foreign Beneficiaries:

- May face tax withholding requirements

- Treaty considerations may reduce or eliminate U.S. tax

- International estate planning required (consult cross-border specialist)

State Estate Tax Interaction

Beyond the 6 inheritance tax states, 12 states plus Washington D.C. impose separate state estate taxes with exemptions far below the federal $13.99 million threshold.

States with Estate Tax (2026): Connecticut, Hawaii, Illinois, Maine, Massachusetts, Minnesota, New York, Oregon, Rhode Island, Vermont, Washington, plus Washington D.C.

Dual Tax Risk: Maryland residents face both inheritance tax (on beneficiaries) and estate tax (on the estate)—potentially exceeding 25% combined effective rate on transfers to distant relatives.

For comparison of state-level tax burdens, the Tax Foundation maintains current rankings and analysis.

Frequently Asked Questions

Q1: Do I pay inheritance tax if I live in Florida but inherit from someone in Pennsylvania?

Yes. Inheritance tax is based on where the deceased person lived at death, not where you live as the beneficiary. Pennsylvania will assess inheritance tax on assets transferred to you based on your relationship to the deceased.

Q2: Is life insurance subject to inheritance tax?

Generally no, when life insurance is paid directly to a named beneficiary. However, if insurance is payable to the deceased’s estate, it becomes part of the estate and may be subject to inheritance tax. Always name specific beneficiaries.

Q3: Can I deduct funeral expenses from inheritance tax?

Yes. Most states allow deduction of funeral expenses, estate administration costs, and outstanding debts from the gross estate before calculating inheritance tax. Keep detailed receipts and documentation.

Q4: How long do I have to pay inheritance tax after someone dies?

Typically 9-12 months from the date of death, though exact deadlines vary by state. Pennsylvania requires payment within 9 months, while Nebraska allows up to 12 months. File extensions may be available but interest accrues on unpaid tax.

Q5: Is inheritance tax the same as income tax on inherited assets?

No. Inherited assets are not subject to federal income tax under current law. The step-up in basis at death eliminates capital gains tax on appreciation during the deceased’s lifetime. However, income generated by inherited assets after you receive them (interest, dividends, rent) is taxable as ordinary income, just like with compound interest growth on savings accounts.

Q6: Do I pay inheritance tax on my parents’ house if I inherit it?

Depends on the state and your relationship. Most states exempt direct descendants (children) from inheritance tax. However, Pennsylvania charges 4.5% even to children. Maryland now provides a $50,000 exemption for children as of 2026. Calculate your specific situation using your state’s rules.

Q7: Can inheritance tax be paid from the estate before distribution?

Yes. The executor can pay inheritance tax from estate assets before distributing to beneficiaries, though this must be authorized by the will or state law. Many executors prefer this method to avoid collecting tax from multiple beneficiaries.

Q8: What happens if I cannot afford to pay the inheritance tax?

Most states offer payment plans or installment options for inheritance tax. Contact your state’s Department of Revenue immediately to arrange payments. Some states charge interest on deferred payments. In cases involving illiquid assets (real estate, business interests), you may need to negotiate extended payment terms or sell assets to satisfy the tax.

Q9: Is there inheritance tax on retirement accounts like 401(k) or IRA?

Yes, if you’re in one of the 6 inheritance tax states and your relationship triggers tax. However, retirement accounts with named beneficiaries bypass probate and transfer directly to beneficiaries. The inheritance tax still applies based on the value received. Additionally, inherited retirement accounts have required distributions subject to income tax, separate from inheritance tax—a dual tax burden similar to managing both credit card debt strategies and student loans simultaneously.

Q10: How is inheritance tax different from probate fees?

Probate fees are court and administrative costs for processing the estate through probate court (typically 1-4% of estate value). Inheritance tax is a separate state tax on the right to receive inherited property (0-18% depending on state and relationship). Both can apply to the same estate.

Q11: Can I challenge an inheritance tax assessment if I believe it’s wrong?

Yes. File a formal protest or appeal with your state’s tax authority within the deadline (typically 60-90 days from assessment notice). Common grounds for appeal include incorrect asset valuation, misapplication of exemptions, or improper relationship classification. Consult a tax attorney for appeals involving significant amounts.

Disclaimer

This article is for educational purposes only and does not constitute financial, tax, or legal advice. Inheritance tax laws vary significantly by state and individual circumstances. Tax regulations change frequently, and what applies in 2026 may differ in future years.

Before making estate planning decisions or inheritance tax payments, consult with qualified professionals: a certified public accountant (CPA) for tax implications, an estate planning attorney for legal strategies, and a financial advisor for comprehensive planning. Every family’s situation is unique, and personalized guidance ensures you maximize available exemptions and minimize tax burdens legally.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.