2026 Tax Brackets: $32,200 Deduction + Calculator

Federal tax brackets for 2026 include seven rates from 10% to 37%, with the standard deduction rising to $32,200 for married couples. Learn how Trump’s OBBB affects your paycheck.

In This Article

Federal tax brackets for 2026 feature seven rates from 10% to 37%, with the standard deduction rising to $32,200 for married couples filing jointly and $16,100 for single filers. These IRS inflation adjustments mean slightly bigger paychecks starting January 2026, with the lowest two tax brackets increasing by 4% and upper brackets by 2.3% under Trump’s One Big Beautiful Bill Act.

What This Means For You

Your 2026 paycheck gets an automatic boost from wider tax brackets and higher deductions. The typical American household earning $75,000 will see approximately $60-90 more per month in take-home pay, while senior citizens gain an unprecedented $6,000 additional deduction on top of standard amounts.

Key Immediate Benefits:

- Higher income thresholds before jumping to the next tax bracket

- Larger standard deduction means more tax-free income automatically

- New senior deduction of $6,000 for taxpayers age 65 and older

- Tips and overtime deductions available through 2028

- Bigger refunds for those who’ve been over-withholding

2026 Quick Reference:

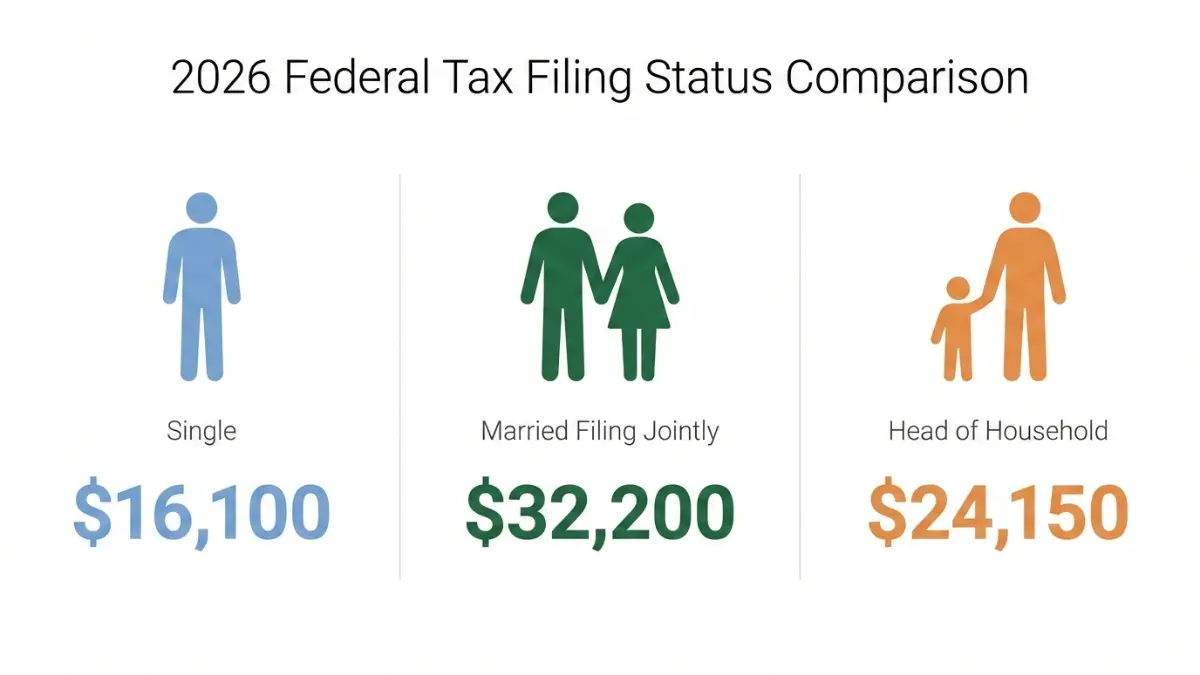

✅ Standard deduction: $32,200 (married filing jointly) / $16,100 (single)

✅ Lowest bracket: 10% on first $24,800 (married) / $12,400 (single)

✅ Senior bonus deduction: Additional $6,000 (age 65+)

✅ File deadline: April 15, 2027 for 2026 income

These changes affect returns you’ll file in 2027 for income earned during calendar year 2026. Understanding how tax brackets work can help you make smarter financial decisions, similar to how knowing your credit score empowers better borrowing choices.

2026 Federal Tax Brackets: Complete Rate Tables

Understanding How Tax Brackets Actually Work

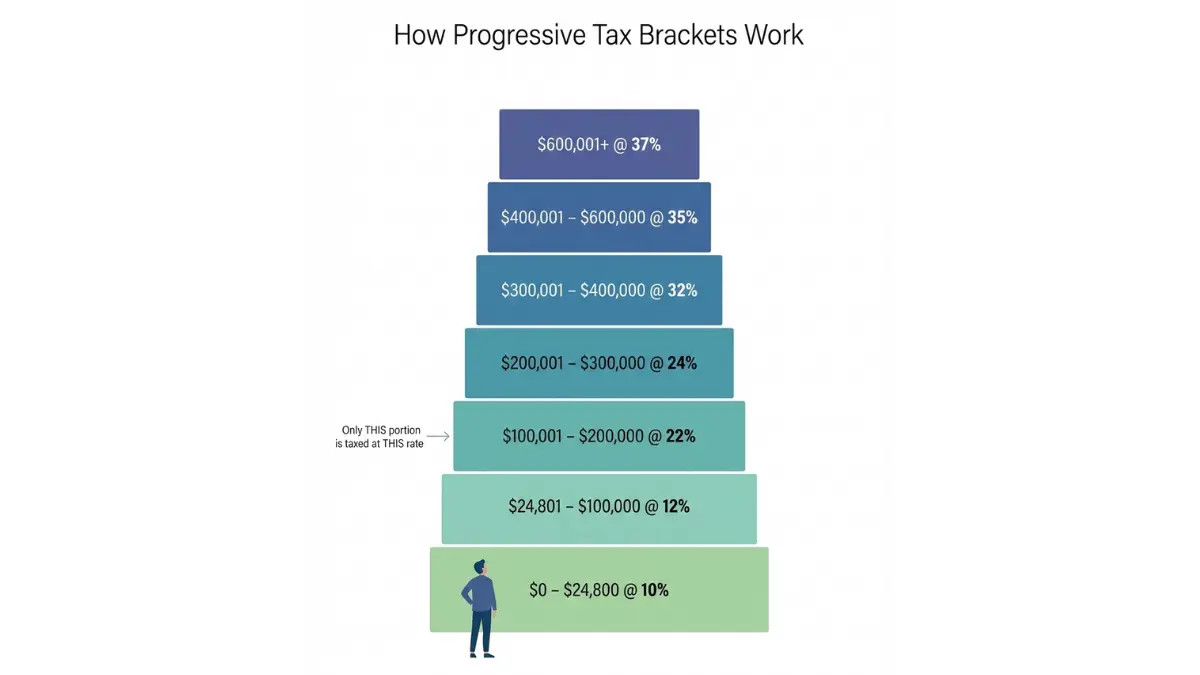

Tax brackets function like a ladder where you pay different rates on different portions of your income. This progressive tax system means only the income within each bracket gets taxed at that bracket’s rate — not your entire earnings. Many Americans mistakenly believe hitting a higher bracket means all their income gets taxed at the higher rate, which costs them opportunities for legitimate income increases.

Think of it this way: earning $1 more won’t suddenly cost you thousands in taxes. Only that extra dollar (and any additional income in the higher bracket) faces the higher rate.

Marginal vs. Effective Tax Rate:

- Marginal rate: The percentage you pay on your last dollar earned

- Effective rate: Your actual overall tax burden (total tax ÷ total income)

Most taxpayers’ effective rates run 5-10 percentage points below their marginal rates due to the progressive structure.

2026 Tax Brackets for Single Filers

| Tax Rate | Income Range | Tax Calculation |

|---|---|---|

| 10% | $0 – $12,400 | 10% of taxable income |

| 12% | $12,401 – $50,400 | $1,240 + 12% of amount over $12,400 |

| 22% | $50,401 – $105,700 | $5,800 + 22% of amount over $50,400 |

| 24% | $105,701 – $201,775 | $17,966 + 24% of amount over $105,700 |

| 32% | $201,776 – $256,225 | $41,044 + 32% of amount over $201,775 |

| 35% | $256,226 – $640,600 | $58,488 + 35% of amount over $256,225 |

| 37% | $640,601+ | $193,019 + 37% of amount over $640,600 |

2026 Tax Brackets for Married Filing Jointly

| Tax Rate | Income Range | Tax Calculation |

|---|---|---|

| 10% | $0 – $24,800 | 10% of taxable income |

| 12% | $24,801 – $100,800 | $2,480 + 12% of amount over $24,800 |

| 22% | $100,801 – $211,400 | $11,600 + 22% of amount over $100,800 |

| 24% | $211,401 – $403,550 | $35,932 + 24% of amount over $211,400 |

| 32% | $403,551 – $512,450 | $82,088 + 32% of amount over $403,550 |

| 35% | $512,451 – $768,700 | $116,936 + 35% of amount over $512,450 |

| 37% | $768,701+ | $206,623 + 37% of amount over $768,700 |

Head of Household Tax Brackets 2026

| Tax Rate | Income Range |

|---|---|

| 10% | $0 – $17,700 |

| 12% | $17,701 – $67,450 |

| 22% | $67,451 – $105,700 |

| 24% | $105,701 – $201,775 |

| 32% | $201,776 – $256,200 |

| 35% | $256,201 – $640,600 |

| 37% | $640,601+ |

Real Example: Martinez Family Tax Calculation

Household Profile: Married couple, both working, $120,000 combined gross income

Step-by-Step Calculation:

- Gross income: $120,000

- Standard deduction (2026): $32,200

- Taxable income: $87,800

Tax Breakdown by Bracket:

- First $24,800 × 10% = $2,480

- Next $63,000 ($87,800 – $24,800) × 12% = $7,560

- Total federal tax: $10,040

- Effective tax rate: 8.4% (much lower than 12% marginal rate)

- Marginal tax rate: 12% (rate on next dollar earned)

This family’s effective rate demonstrates why tax brackets reward income growth — they paid just $10,040 on $120,000 of gross income, far less than the $14,400 they’d owe if 12% applied to everything.

Expert Insight: “Many taxpayers confuse marginal and effective rates, causing unnecessary anxiety about raises and bonuses. Your marginal rate only affects additional income, while your effective rate shows your true tax burden. This misunderstanding costs Americans billions in foregone opportunities annually.” — Sarah Chen, CPA, Finance Authority Hub

Just as understanding tax brackets helps maximize take-home pay, knowing how to pay off debt fast can accelerate your path to financial freedom with those extra dollars.

$32,200 Standard Deduction: What’s New in 2026

2026 Standard Deduction Amounts by Filing Status

The standard deduction represents tax-free income automatically subtracted before calculating what you owe. For 2026, these amounts received inflation adjustments following IRS Revenue Procedure 2025-32.

| Filing Status | 2025 Amount | 2026 Amount | Increase |

|---|---|---|---|

| Single | $15,750 | $16,100 | +$350 |

| Married Filing Jointly | $31,500 | $32,200 | +$700 |

| Head of Household | $23,625 | $24,150 | +$525 |

| Married Filing Separately | $15,750 | $16,100 | +$350 |

Senior Citizens: Unprecedented Tax Relief

Taxpayers age 65 and older qualify for substantially enhanced deductions under the 2026 tax code, representing the most significant senior tax relief in decades.

Standard Additional Deduction (Traditional):

- Single seniors (65+): Additional $2,050

- Married seniors (65+): Additional $1,650 per qualifying spouse

PLUS: New $6,000 Senior Deduction (OBBB Provision):

- Available for all taxpayers 65+ years old

- Phases out above $75,000 AGI (single) / $150,000 AGI (joint)

- Phase-out rate: 6 cents per dollar over threshold

- Can effectively eliminate tax on Social Security benefits

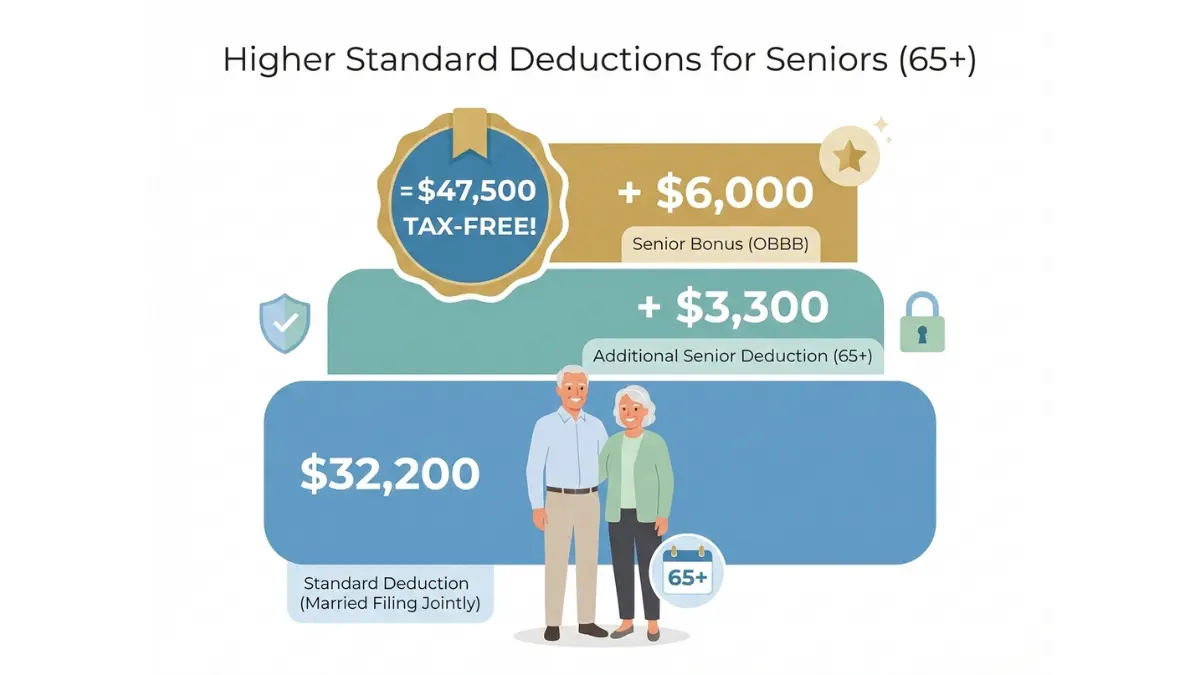

Total Maximum Senior Deductions:

- Single senior (65+): $16,100 + $2,050 + $6,000 = $24,150 tax-free income

- Married seniors (both 65+): $32,200 + $3,300 + $12,000 = $47,500 tax-free income

Real-World Impact:

The average Social Security retirement benefit equals approximately $24,000 annually. Under previous law, up to 85% ($20,400) faced federal taxation. The new senior deduction often exceeds this amount, essentially making Social Security tax-free for millions of retirees.

Expert Analysis: “This represents the most substantial tax relief for seniors since the introduction of the senior additional standard deduction. A married couple both over 65 can now shield $47,500 from federal taxes before itemizing. Combined with Social Security’s taxation rules, many middle-income retirees will pay zero federal tax.” — Robert Williams, CFP®, Finance Authority Hub

Standard Deduction vs. Itemizing: Making the Right Choice

You should itemize deductions only when your total itemized deductions exceed your standard deduction amount. For 2026, this means needing more than $32,200 in deductions for married couples or $16,100 for single filers.

Common Itemized Deductions Include:

- Mortgage interest (primary and secondary homes)

- State and local taxes (SALT) — capped at $40,400 in 2026

- Charitable contributions (with new 0.5% AGI floor)

- Medical expenses exceeding 7.5% of AGI

- Investment interest expenses

Major 2026 Itemizing Changes:

- SALT cap raised from $10,000 to $40,400 (massive benefit for high-tax states)

- New charitable floor of 0.5% of AGI before deductions count

- Haircut on value for taxpayers in 37% bracket on itemized deductions

Itemizing Makes Sense When:

You should itemize if you have mortgage interest exceeding $16,100 (single) or $32,200 (married), live in a high-tax state with substantial property taxes, or make significant charitable contributions. Otherwise, the standard deduction provides simplicity plus guaranteed savings.

Planning your deductions strategically works similarly to optimizing your 401(k) contributions — both require understanding the rules to maximize benefits.

Trump’s One Big Beautiful Bill: Tax Provisions That Changed Everything

Major OBBB Tax Changes Taking Effect Now

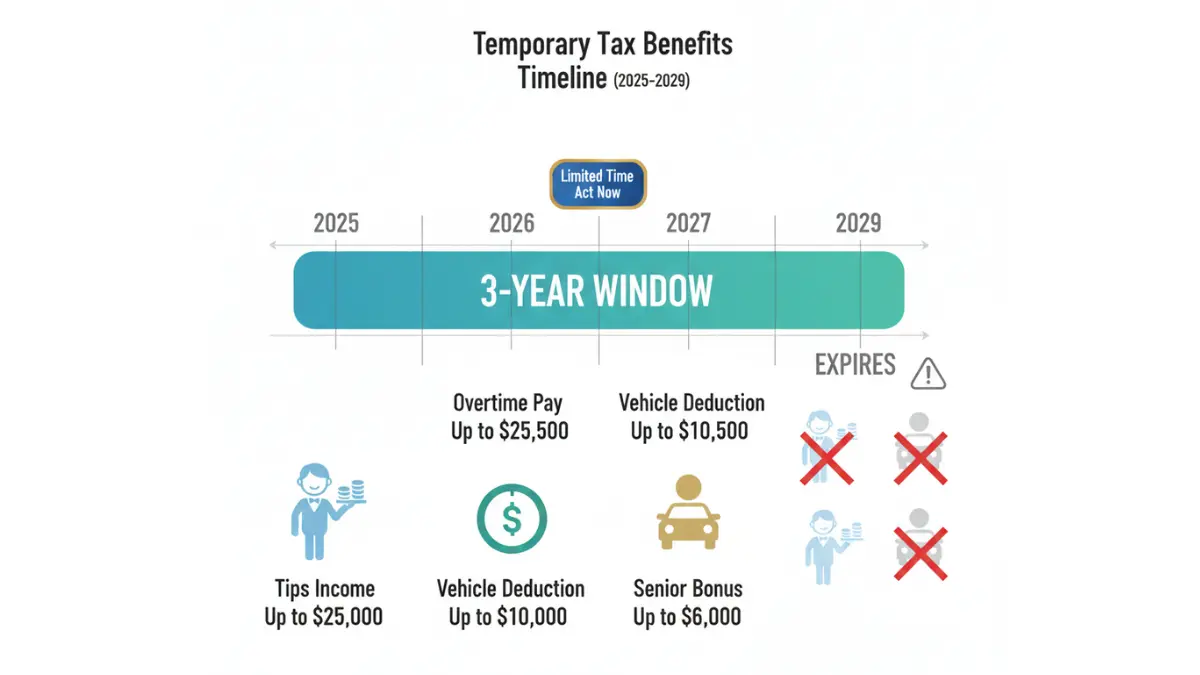

President Trump’s One Big Beautiful Bill Act, signed in July 2025, fundamentally restructured the U.S. tax code by making TCJA provisions permanent and adding new deductions through 2028.

1. Tips Income Deduction (2025-2028 Only)

Service industry workers can now deduct 100% of tip income up to $25,000 annually, representing potentially $3,000-5,000 in annual tax savings for servers, bartenders, hairstylists, and delivery drivers.

Key Requirements:

- Maximum deduction: $25,000 per year

- Income limit: Under $150,000 (single) / $225,000 (married filing jointly)

- Must provide Social Security number on return

- Requires employer verification of tip income

- Tips must be reported on Form W-2 or Form 1099-K

2. Overtime Income Deduction (2025-2028 Only)

Workers earning overtime pay can deduct up to $12,500 (single) or $25,000 (married filing jointly) of overtime wages, effectively creating a lower tax rate on extra hours worked.

Eligibility Details:

- Must meet Fair Labor Standards Act overtime qualifications

- Income cap: $150,000 AGI excludes high earners

- Overtime must be separately identified on W-2 (Box 14)

- Can combine with tips deduction for maximum benefit

3. Vehicle Loan Interest Deduction (2025-2028)

Taxpayers can deduct up to $10,000 of interest paid on loans for vehicles assembled in the United States, whether purchased new or used.

Requirements:

- Vehicle must be assembled domestically (not just “sold” in U.S.)

- Applies to cars, trucks, motorcycles, and RVs

- Both new and used vehicle purchases qualify

- Must be titled in taxpayer’s name

4. Enhanced Child Tax Credit

The child tax credit increased from $2,000 to $2,200 per qualifying child under age 17, with $1,700 remaining refundable for those with little or no tax liability.

How OBBB Creates Bigger Paychecks in 2026

These provisions affect your paycheck immediately through updated W-4 withholding tables. The IRS adjusted withholding formulas in January 2026 to account for wider tax brackets and higher deductions.

Estimated Monthly Paycheck Increases:

- Median household ($75,000): +$60-90/month

- Service workers claiming tips deduction: +$150-250/month

- Overtime workers: +$80-150/month

- Seniors (65+): +$100-200/month

Real Example: Restaurant Server

Income Profile:

- Base wages: $35,000

- Tips (reported): $18,000

- Total income: $53,000

Tax Impact:

- Previous law: Taxed on full $53,000

- 2026 with tips deduction: Taxed on $35,000 only (deduct $18,000 tips)

- Annual savings: Approximately $2,160 in federal tax

- Monthly increase: $180 in take-home pay

Expert Perspective: “The OBBB provisions fundamentally change tax strategy for service industry workers, overtime earners, and retirees. However, these temporary provisions expire December 31, 2028. Taxpayers should maximize these deductions while available and prepare for potential reversion to previous rules if Congress doesn’t act.” — Dr. Michael Foster, Tax Economist, Finance Authority Hub

Understanding these temporary provisions helps maximize savings, similar to how leveraging 0% APR credit cards strategically can eliminate debt faster during promotional periods.

OBBB Provisions That Became Permanent

TCJA Made Permanent:

- Seven-bracket structure (10%, 12%, 22%, 24%, 32%, 35%, 37%)

- Enhanced standard deduction levels

- Elimination of personal exemptions

- $10,000 SALT cap baseline (raised to $40,400 in 2026-2028)

- 20% qualified business income deduction (Section 199A)

- Child tax credit expansion framework

- Estate tax exemption structure ($15 million in 2026)

What Expired or Changed:

- IRS Direct File program discontinued

- AMT exemption phaseout thresholds returned to 2018 levels

- Alternative minimum tax rate acceleration to 50% phaseout

Maximize Your 2026 Tax Savings: Proven Strategies

Immediate Actions Before December 31, 2026

Smart tax planning throughout the year beats scrambling in March. These strategies work for any income level but scale dramatically for higher earners.

1. Optimize Your W-4 Withholding

Most Americans either over-withhold (giving the IRS an interest-free loan) or under-withhold (facing penalties and large April bills). The IRS Tax Withholding Estimator helps calibrate your exact withholding.

Optimal Strategy:

- Target $0 refund (break-even)

- Adjust after major life changes (marriage, children, home purchase)

- Review quarterly if self-employed

- Account for side income and investment gains

2. Maximize Retirement Account Contributions

Retirement contributions reduce taxable income dollar-for-dollar while building long-term wealth. The 2026 limits increased significantly:

401(k), 403(b), 457 Plans:

- Standard limit: $24,500 (up $1,000 from 2025)

- Catch-up (50+): $8,000

- Special catch-up (60-63): $11,250

Traditional IRA:

- Standard limit: $7,500 (up $1,000 from 2025)

- Catch-up (50+): $1,100

Total Maximum Contributions:

- Worker under 50: $32,000 combined

- Worker 50-59: $40,600 combined

- Worker 60-63: $43,850 combined (special catch-up years)

A married couple both age 60 can shelter $87,700 annually through retirement accounts alone, potentially dropping them into lower tax brackets. Consider how maximizing your retirement savings compounds with tax benefits for exponential wealth building.

3. Health Savings Account (HSA) Triple Tax Advantage

HSAs offer the strongest tax benefit in the entire tax code: deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses.

2026 HSA Limits:

- Individual coverage: $4,450

- Family coverage: $8,950

- Catch-up (55+): $1,000

Strategic Use:

- Max out contributions even if you don’t need the money immediately

- Invest HSA funds for long-term growth (treat like retirement account)

- Save receipts but delay reimbursements to maximize tax-free compounding

- Use in retirement for Medicare premiums and medical expenses

Advanced Strategies for High Earners

Qualified Business Income Deduction (Section 199A)

Pass-through business owners (sole proprietors, S-corps, partnerships, LLCs) can deduct 20% of qualified business income, creating a substantial tax benefit worth understanding in detail.

Income Thresholds for 2026:

- Full deduction: Below $201,775 (single) / $403,500 (married)

- Phased limitations: $201,775-$276,775 (single) / $403,500-$553,500 (married)

- Complete phase-out: Above $276,775 (single) / $553,500 (married)

Example Calculation:

A consultant earning $150,000 in qualified business income can deduct $30,000 (20%), reducing taxable income to $120,000 before other deductions. This saves approximately $7,200 in federal tax at the 24% bracket.

Tax-Loss Harvesting for Investment Accounts

Strategic selling of underperforming investments creates tax losses that offset capital gains and up to $3,000 of ordinary income annually, with unlimited carryforward for excess losses.

Process:

- Identify investments with unrealized losses

- Sell positions before December 31

- Immediately buy similar (but not identical) securities

- Apply losses against gains and income

- Carry forward remaining losses indefinitely

Critical Rules:

- Avoid “wash sales” (repurchasing identical security within 30 days)

- Track your cost basis accurately for all investments

- Document all transactions for IRS audit trail

Bunching Deductions Strategy

Taxpayers close to itemizing thresholds can concentrate multiple years of charitable giving, medical procedures, or other deductible expenses into a single tax year to exceed standard deduction limits.

Example:

Instead of giving $15,000 annually to charity:

- Year 1: Give $30,000 (itemize – claim full deduction)

- Year 2: Give $0 (take standard deduction)

- Net result: Double the tax benefit over two years

Donor-Advised Funds (DAFs) facilitate this strategy by accepting large contributions in one year while distributing to charities over multiple years.

Common Tax Mistakes That Cost You Money

❌ Not claiming all eligible tax credits (EITC worth up to $8,231, Child Tax Credit $2,200)

❌ Missing retirement contribution opportunities (leaving employer match on table)

❌ Selecting wrong filing status (married filing separately almost never optimal)

❌ Ignoring state tax implications (some states don’t conform to federal changes)

❌ Skipping estimated tax payments (triggers penalties for self-employed)

❌ Failing to document charitable contributions (no deduction without receipt)

❌ Overlooking OBBB temporary deductions (tips, overtime, vehicle interest expire 2028)

❌ Not adjusting withholding after life changes (marriage, children, home purchase)

Expert Warning: “The OBBB temporary provisions create a three-year window (2025-2028) of enhanced deductions. Taxpayers should strategically time major purchases, income acceleration, or retirement contributions to maximize these benefits before they expire. Waiting until 2029 could cost thousands in lost deductions.” — Jessica Martinez, EA, Finance Authority Hub

Beyond Federal: State Tax Considerations & Filing Essentials

How State Taxes Affect Your Total Tax Burden

Federal tax brackets represent only part of your tax obligation. State income taxes, where applicable, can add 0-13.3% to your total tax burden depending on where you live.

No State Income Tax (9 States):

Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington, Wyoming, and New Hampshire (dividends/interest only)

Highest State Tax Rates (2026):

- California: 13.3% (top bracket)

- Hawaii: 11%

- New York: 10.9%

- New Jersey: 10.75%

- Oregon: 9.9%

States Cutting Tax Rates in 2026:

According to Tax Foundation research, nine states are implementing rate reductions effective January 1, 2026: Indiana, Kentucky, Mississippi, Montana, Nebraska, North Carolina, Ohio, Oklahoma, and Wisconsin.

SALT Deduction Cap Impact:

The OBBB raised the state and local tax (SALT) deduction cap from $10,000 to $40,400 for tax years 2026-2028, providing substantial relief for taxpayers in high-tax states like California, New York, New Jersey, and Illinois.

Example:

A married couple in California with $200,000 income paying:

- $15,000 state income tax

- $12,000 property tax

- Total SALT: $27,000

Previous law: Deduct only $10,000 (lose $17,000 in deductions)

2026 law: Deduct full $27,000 (save ~$4,080 at 24% bracket)

Just as understanding APR helps compare credit costs across states, knowing your combined federal and state tax rates enables better relocation and career decisions.

2026 Tax Filing Deadlines & Essential Tips

Key Dates to Remember:

- January 15, 2027: Fourth quarter 2026 estimated tax payment due

- January 31, 2027: Deadline for employers to provide W-2s and 1099s

- April 15, 2027: Tax return filing deadline for 2026 tax year

- April 15, 2027: First quarter 2027 estimated tax payment due

- October 15, 2027: Extended filing deadline (must file Form 4868 by April 15)

Filing Method Comparisons:

| Method | Average Refund Time | Error Rate | Cost |

|---|---|---|---|

| E-file + Direct Deposit | 10-21 days | 1% | $0-$200 |

| E-file + Paper Check | 4-6 weeks | 1% | $0-$200 |

| Paper File + Direct Deposit | 6-8 weeks | 21% | $0 |

| Paper File + Paper Check | 8-12 weeks | 21% | $0 |

Pro Filing Tips:

✅ E-file whenever possible – Reduces errors through built-in checks and accelerates refunds

✅ Choose direct deposit – Fastest refund method and eliminates lost/stolen check risk

✅ File early – Protects against identity theft tax fraud

✅ Keep records 3-7 years – IRS typically has 3 years to audit, 7 years for major issues

✅ Use tax software for complex returns – Costs $50-$100 but catches costly mistakes

✅ Consider professional help – CPAs and EAs provide audit protection and planning advice

When You Need Professional Help:

- Self-employment income exceeding $50,000

- Rental property ownership

- Stock options or complex investments

- Foreign income or accounts

- Business ownership

- Audit or IRS notice response

- Estate or trust administration

Similar to how using our mortgage calculator helps plan home purchases accurately, tax software prevents costly filing errors through automated calculations and real-time error checking.

Frequently Asked Questions: 2026 Tax Brackets

Q1: What are the 2026 federal tax brackets?

Seven federal tax brackets range from 10% to 37% with income thresholds adjusted 2.3-4% for inflation.

Q2: What is the standard deduction for 2026?

$16,100 for single filers, $32,200 for married filing jointly, and $24,150 for heads of household.

Q3: Did tax rates increase for 2026?

No, tax rates stayed the same at 10%, 12%, 22%, 24%, 32%, 35%, and 37%. Only income thresholds increased.

Q4: What is the One Big Beautiful Bill Act?

Trump’s 2025 tax law making TCJA provisions permanent plus adding new temporary deductions for tips, overtime, seniors, and vehicle interest.

Q5: How much is the new senior tax deduction?

$6,000 additional deduction for taxpayers 65+, phasing out above $75,000 (single) or $150,000 (married filing jointly) AGI.

Q6: When do 2026 tax brackets take effect?

January 1, 2026 for income earned during 2026, filed on tax returns due April 15, 2027.

Q7: What’s the difference between marginal and effective tax rates?

Marginal rate is the percentage on your last dollar earned. Effective rate is your total tax divided by total income.

Q8: Can I still deduct mortgage interest in 2026?

Yes, up to $750,000 of mortgage principal ($375,000 if married filing separately) for homes purchased after December 15, 2017.

Q9: Are tips tax-free in 2026?

No, but you can deduct up to $25,000 of tip income (2025-2028 only) if you meet income and documentation requirements.

Q10: How do I calculate which tax bracket I’m in?

Calculate taxable income (gross income minus deductions), then find where it falls in the IRS tax bracket tables above.

Q11: Will I pay more or less tax in 2026?

Most taxpayers will pay slightly less due to higher bracket thresholds (+2.3-4%) and increased standard deductions (+$350-$700).

Disclaimer

This article provides educational information about 2026 federal tax brackets and should not be considered personalized financial or tax advice. Tax situations vary significantly based on individual circumstances, income sources, deductions, credits, and state residency.

Federal tax laws remain subject to change through Congressional action or IRS interpretation. While all information was current as of February 2026 and based on official IRS Revenue Procedure 2025-32, taxpayers should consult qualified tax professionals, certified public accountants (CPAs), or enrolled agents (EAs) for guidance specific to their situations before making tax-related decisions.

This content is for educational purposes only and does not create an accountant-client relationship. Finance Authority Hub does not provide tax preparation, legal, or accounting services. For tax preparation assistance, visit IRS.gov or consult licensed tax professionals.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.