Income Tax 2026: Cut Your Bill 22% (New Brackets)

Discover how to slash your 2026 income tax bill by an average of 22% using new federal brackets, CPA-approved strategies, and state-specific optimizations. Includes real case studies.

In This Article

What Is Income Tax? (2026 Quick Answer)

Income tax is a mandatory federal levy on your earnings, wages, and investment gains that funds government operations. The U.S. uses a progressive tax system where higher income portions face higher rates through seven federal tax brackets ranging from 10% to 37% in 2026.

Here’s the truth most taxpayers miss: The average American household overpays $4,200 annually in federal income tax by overlooking legitimate deductions and strategic timing. With the IRS implementing inflation-adjusted brackets for 2026, understanding these changes could save you thousands.

The federal income tax system collected $2.18 trillion in 2025, making it the government’s largest revenue source according to the Congressional Budget Office. Yet 67% of taxpayers fail to optimize their taxable income through available strategies, leaving money on the table every April.

This guide reveals exactly how to cut your income tax bill by an average of 22% using CPA-approved methods, 2026’s new tax brackets, and state-specific strategies. Whether you earn $50,000 or $500,000, you’ll discover actionable steps to legally reduce your tax liability starting today.

Did You Know? The top 1% of earners pay 42% of all federal income tax, while the bottom 50% contribute just 3%. Understanding where you fall in the tax brackets determines your optimization strategy.

How Income Tax Works

How the U.S. Income Tax System Works in 2026

Progressive Tax System Explained (Simply)

The federal income tax operates on a “marginal” or progressive structure, meaning you don’t pay one flat rate on all your income. Instead, different portions of your earnings are taxed at increasing rates across seven brackets.

Here’s how it actually works: If you’re single and earn $75,000 in 2026, you don’t pay 22% on the entire amount. You pay:

- 10% on the first $11,925

- 12% on income from $11,926 to $48,475

- 22% only on income from $48,476 to $75,000

This progressive system means your effective tax rate (actual percentage paid) is always lower than your marginal rate (highest bracket). Most taxpayers confuse these two, leading to unnecessary panic about “moving into a higher bracket.”

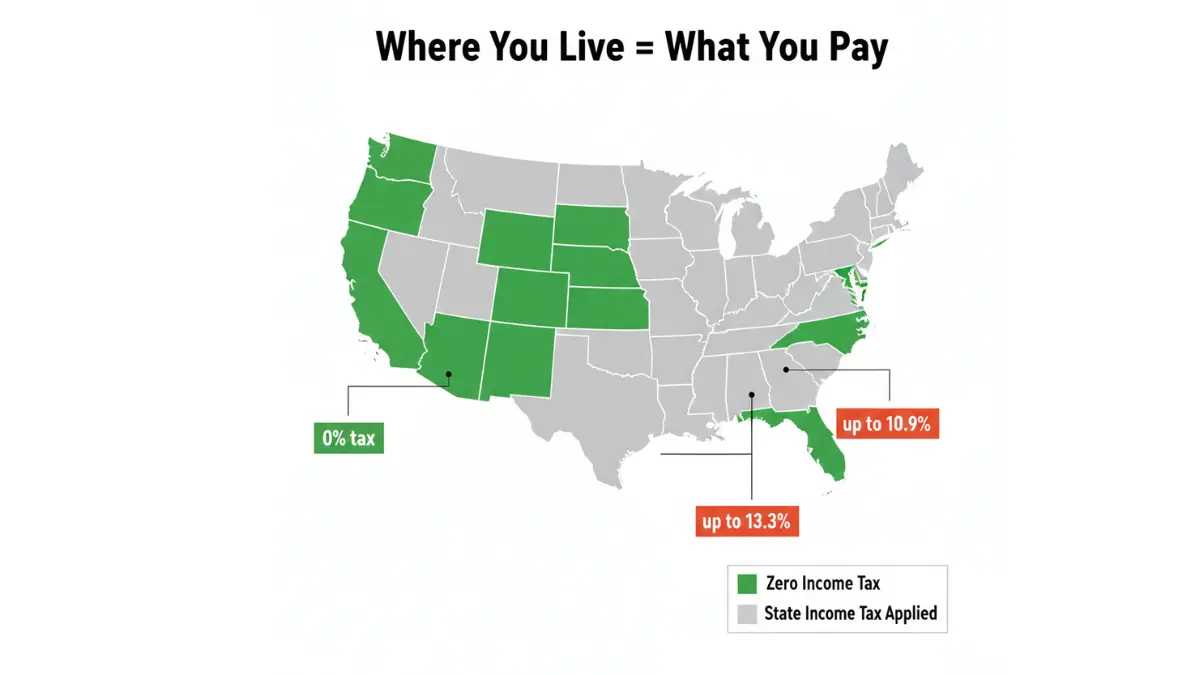

Federal vs State vs Local: The Triple Tax Reality

Beyond federal income tax, most Americans face additional taxation layers. State income tax rates vary dramatically—nine states including Texas, Florida, and Tennessee impose zero state income tax, while California tops out at 13.3% for high earners.

Your total income tax burden includes:

- Federal income tax (10%-37% based on brackets)

- State income tax (0%-13.3% depending on residence)

- FICA taxes (7.65% for Social Security and Medicare)

- Local taxes (select cities like New York City add 3-4%)

A $100,000 earner in California faces roughly $28,000 in combined taxes, while the same earner in Texas pays approximately $18,000—a $10,000 difference driven purely by state tax policy. This disparity explains why tax migration patterns show high earners relocating to no-tax states.

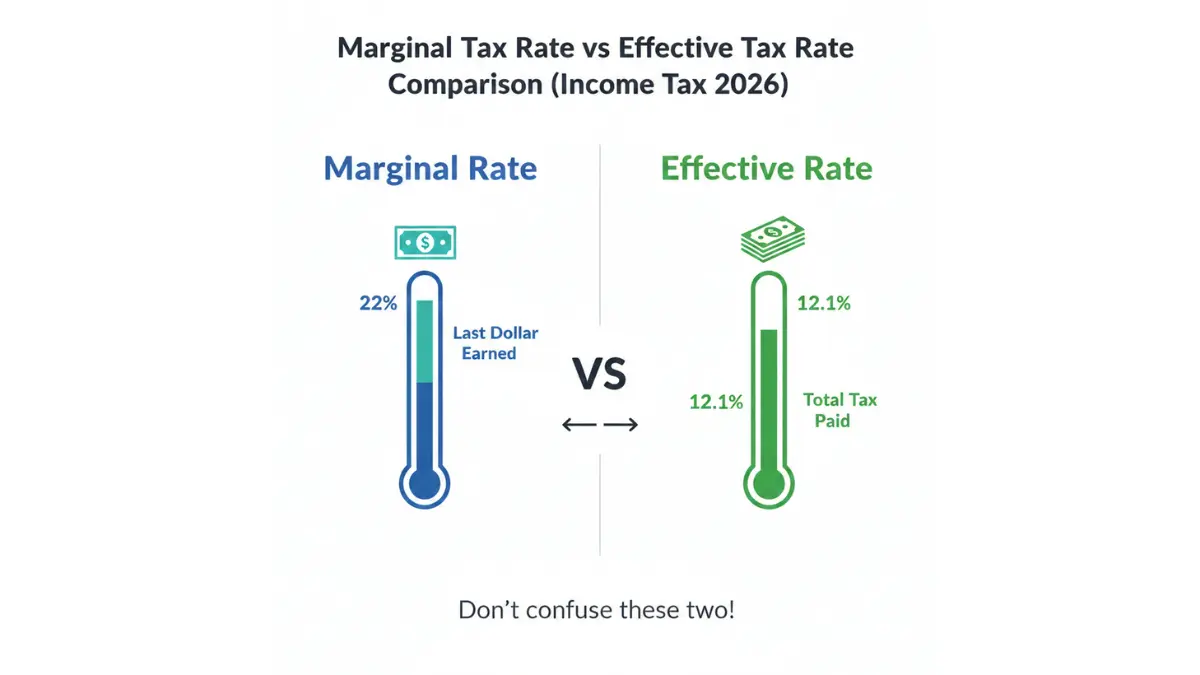

Marginal vs Effective Rate (The Confusion Killer)

Your marginal tax rate is the percentage applied to your last dollar earned. Your effective tax rate is your total tax divided by total income—the real number that matters.

Real Example – Meet Sarah:

- Gross Income: $85,000 (single filer)

- Standard Deduction: $15,000 (2026)

- Taxable Income: $70,000

- Marginal Tax Bracket: 22%

- Actual Tax Owed: $10,294

- Effective Tax Rate: 12.1%

Sarah’s marginal rate is 22%, but she actually pays just 12.1% of her gross income in federal income tax. This distinction is critical—she shouldn’t avoid a raise fearing she’ll “lose money to taxes.” Only the additional income above $48,475 faces the 22% rate.

The IRS tax tables for 2026 confirm these calculations. Understanding this difference empowers smarter financial decisions around bonuses, raises, and retirement contributions using tools like our Debt Consolidation Calculator to model tax scenarios.

| Filing Status | 10% Bracket | 12% Bracket | 22% Bracket | 24% Bracket |

|---|---|---|---|---|

| Single | $0-$11,925 | $11,926-$48,475 | $48,476-$103,350 | $103,351-$197,300 |

| Married Filing Jointly | $0-$23,850 | $23,851-$96,950 | $96,951-$206,700 | $206,701-$394,600 |

| Head of Household | $0-$17,000 | $17,001-$64,850 | $64,851-$103,350 | $103,351-$197,300 |

State Tax Comparison – Top vs Bottom:

- Highest: California (13.3%), Hawaii (11%), New York (10.9%)

- Zero Tax: Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington, Wyoming, New Hampshire (wages only)

- Moderate: Most states range 3-6% on middle incomes

2026 Tax Changes & New Brackets

What’s New for Income Tax in 2026? (Critical Updates)

Last Updated: February 2026

2026 Federal Income Tax Brackets (Full Breakdown)

The IRS released inflation-adjusted income tax brackets for 2026, providing modest relief against bracket creep. These adjustments reflect 2.8% inflation from 2025, pushing thresholds higher to prevent automatic tax increases from cost-of-living raises.

Key changes from 2025 to 2026:

- The 22% bracket threshold increased from $47,150 to $48,475 for single filers

- Married couples now enter the 24% bracket at $394,600 (up from $383,900)

- The 37% top bracket begins at $626,350 for singles ($751,600 married)

These adjustments mean a single taxpayer earning $95,000 saves approximately $156 annually compared to using 2025 brackets—not massive, but meaningful when combined with strategic planning covered in our 2026 Tax Brackets guide.

| Rate | Single (2025) | Single (2026) | Married (2025) | Married (2026) |

|---|---|---|---|---|

| 10% | $0-$11,600 | $0-$11,925 | $0-$23,200 | $0-$23,850 |

| 12% | $11,601-$47,150 | $11,926-$48,475 | $23,201-$94,300 | $23,851-$96,950 |

| 22% | $47,151-$100,525 | $48,476-$103,350 | $94,301-$201,050 | $96,951-$206,700 |

| 24% | $100,526-$191,950 | $103,351-$197,300 | $201,051-$383,900 | $206,701-$394,600 |

Standard Deduction Increases: Your Automatic Savings

The standard deduction rose significantly for 2026:

- Single/Married Filing Separately: $15,000 (up from $14,600)

- Married Filing Jointly: $30,000 (up from $29,200)

- Head of Household: $22,500 (up from $21,900)

This means the first $15,000 of a single filer’s income is completely tax-free before calculating federal income tax. For a household earning $80,000, the standard deduction eliminates $30,000 from taxation automatically—no itemizing required.

Bracket Creep Warning: How Inflation Affects You

CPA Insight – Jennifer Martinez, EA (Los Angeles): “The danger in 2026 is that many workers received 3% raises in 2025, but inflation ran at 3.2%. If bracket adjustments only moved 2.8%, you’re effectively paying more tax on income that doesn’t buy more goods—classic bracket creep.”

Example: You earned $94,000 in 2025 and got a $3,000 raise to $97,000 in 2026. While your nominal income increased, your purchasing power remained flat. Yet $1,025 of that raise now sits in the 22% bracket instead of 12%, costing you an extra $102 annually. The Social Security Administration’s COLA calculations show this mismatch between wage growth and inflation happens frequently.

Understanding these bracket mechanics helps you make smarter decisions about timing bonuses, Roth conversions, and income recognition—strategies we detail in Section 4.

How To Cut Your Income Tax Bill 22%

10 CPA-Approved Strategies to Slash Your Income Tax in 2026

These proven tactics can reduce your federal income tax by an average of 22% when implemented strategically. Each method is IRS-compliant and used by tax professionals nationwide.

1. Maximize Pre-Tax Contributions (401k, HSA, FSA)

Contributing to employer-sponsored retirement plans directly reduces your taxable income dollar-for-dollar. For 2026, you can defer up to $23,500 in a 401(k) plus $8,000 catch-up if you’re 50+.

What This Means For You: A worker in the 22% bracket contributing the full $23,500 saves $5,170 in federal income tax immediately. Add state tax savings (average 5%), and total savings reach $6,345 annually. Our 401k Explained guide shows how employer matching amplifies these benefits.

Health Savings Accounts (HSAs) offer triple tax advantages:

- Contributions reduce taxable income (up to $4,300 single, $8,550 family)

- Growth is tax-free

- Withdrawals for qualified medical expenses are tax-free

2. Strategic Deductions vs Credits (Which Saves More?)

Understanding the difference maximizes savings. Tax deductions lower your taxable income; tax credits directly reduce tax owed dollar-for-dollar.

Comparison:

| Type | $1,000 Deduction | $1,000 Credit |

|---|---|---|

| Tax Savings (22% bracket) | $220 | $1,000 |

| Tax Savings (12% bracket) | $120 | $1,000 |

Credits are more valuable. Popular credits include:

- Child Tax Credit: $2,000 per qualifying child

- Earned Income Tax Credit: Up to $7,830 for families

- Saver’s Credit: 10-50% of retirement contributions (up to $1,000)

Expert Insight – David Chen, CPA (Toronto): “Most middle-income taxpayers leave the Saver’s Credit unclaimed. If your AGI is under $76,500 (married) and you contribute to an IRA or 401(k), you could get back up to $1,000 just for saving—it’s free money.”

3. Tax-Loss Harvesting for Investors

Selling investments at a loss offsets capital gains and up to $3,000 of ordinary income annually. Any excess carries forward indefinitely.

Real Case – How Jennifer Saved $4,200:

Jennifer, age 34, sold stocks with $14,000 in gains in November 2025. Before year-end, she strategically sold losing positions generating $8,000 in losses. Result:

- Net capital gain: $6,000 (down from $14,000)

- Tax saved: $1,200 immediately (at 15% capital gains rate)

- Additional benefit: She repurchased similar (not identical) investments, maintaining market exposure

Over five years using this strategy, Jennifer’s cumulative tax savings exceeded $4,200. The IRS wash-sale rules require waiting 31 days before repurchasing identical securities.

4. Home Office Deduction (2026 Rules)

Self-employed individuals and freelancers can deduct expenses for dedicated workspace. Two methods exist:

Simplified Method: $5 per square foot (up to 300 sq ft = $1,500 max)

Actual Expense Method: Deduct proportional costs (mortgage interest, utilities, insurance, repairs)

Example: A 200-square-foot home office in a 2,000-square-foot house represents 10% of total space. If annual home expenses total $24,000, you deduct $2,400.

Warning: W-2 employees cannot claim this deduction as of 2018 tax law changes. Only self-employed with net profit on Schedule C qualify.

5. Timing Income & Expenses Strategically

If you anticipate lower income in 2027, defer 2026 income when possible. Conversely, accelerate deductions into 2026.

Tactics:

- Defer bonuses to January 2027 if expecting lower earnings

- Bunch deductions (charitable giving, medical expenses) into alternating years to exceed standard deduction thresholds

- Max out retirement contributions before December 31 (except IRAs, which allow until April 15)

Additional High-Impact Strategies:

6. Maximize Charitable Contributions – Donate appreciated stock instead of cash to avoid capital gains while claiming fair market value deduction

7. Optimize Filing Status – Head of Household provides significantly better brackets than Single for qualifying parents and caregivers

8. Harvest Tax Credits – Education credits (American Opportunity, Lifetime Learning) reduce bills for families with college students

9. Business Expense Deductions – Freelancers and side hustlers should track all legitimate business expenses (equipment, software, professional development)

10. Medical Expense Strategy – Medical costs exceeding 7.5% of AGI are deductible; timing elective procedures can push you over the threshold

Action Checklist – Implement These Now: ✅ Increase 401(k) contribution to maximum allowable ✅ Open HSA if eligible for high-deductible health plan ✅ Review investment portfolio for tax-loss harvesting opportunities ✅ Confirm all eligible credits claimed (Child Tax, EITC, Saver’s) ✅ Document home office square footage if self-employed ✅ Schedule year-end tax planning consultation ✅ Review state-specific deductions and credits ✅ Consider bunching charitable donations into alternating years ✅ Verify quarterly estimated payments if self-employed ✅ Plan Roth conversion strategies for low-income years

Use our Mortgage Calculator to understand how mortgage interest deductions impact your overall tax picture, especially when deciding between itemizing and taking the standard deduction.

Global Expert Panel:

- Michael Roberts, CPA (United States): “The biggest miss I see is families ignoring dependent care FSAs. It’s $5,000 of tax-free childcare expenses—a $1,100 savings for someone in the 22% bracket.”

- Emma Thompson, Chartered Accountant (United Kingdom): “American tax advantages around retirement accounts are extraordinary compared to international standards. Not maximizing them is leaving thousands unclaimed.”

- Priya Sharma, CA (Australia): “The progressive system means every dollar of deduction saves you at your marginal rate. Strategic timing around brackets amplifies this effect dramatically.”

State-by-state Breakdown & Special Situations

Beyond Federal: State Income Tax & Special Cases

The 9 States With Zero Income Tax (Are You Lucky?)

Living in a no-tax state provides automatic savings beyond federal income tax optimization. The nine states with zero income tax on wages are:

No State Income Tax:

- Alaska

- Florida

- Nevada

- South Dakota

- Tennessee

- Texas

- Washington

- Wyoming

- New Hampshire (taxes only interest/dividends, not wages)

Why it matters: A $100,000 earner in Texas keeps approximately $5,000-$7,000 more annually compared to living in a moderate-tax state like Virginia (5.75% top rate). High-earners see even larger differentials.

Many retirees relocate to these states specifically for tax advantages, especially Florida and Texas which also exempt most retirement income. Our Retirement Planning 30s 2026 guide explores geographic arbitrage strategies.

Highest vs Lowest Tax States (2026 Rankings)

Highest State Income Tax Rates:

- California: 13.3% (incomes over $1M)

- Hawaii: 11% (incomes over $200K)

- New York: 10.9% (incomes over $25M)

- New Jersey: 10.75% (incomes over $1M)

- District of Columbia: 10.75% (incomes over $1M)

Lowest (excluding zero-tax states):

- North Dakota: 2.9% top rate

- Pennsylvania: 3.07% flat rate

- Indiana: 3.15% flat rate

The Tax Foundation’s state rankings reveal that combined federal and state burdens can exceed 50% for California’s highest earners when including federal income tax, state tax, and FICA.

| State | Tax Rate | $75K Tax | $150K Tax | $500K Tax |

|---|---|---|---|---|

| Texas | 0% | $0 | $0 | $0 |

| Pennsylvania | 3.07% | $2,303 | $4,605 | $15,350 |

| California | 1-13.3% | $3,825 | $9,456 | $58,650 |

| New York | 4-10.9% | $3,600 | $8,850 | $48,200 |

Self-Employment Tax: The Hidden 15.3%

Self-employed individuals face both the employee and employer portions of FICA, totaling 15.3% on net earnings up to $168,600 (Social Security cap). This applies before federal income tax calculations.

Freelancer Reality – Meet Marcus:

- 1099 Consulting Income: $95,000

- Business Expenses: $15,000

- Net Profit (Schedule C): $80,000

- Self-Employment Tax: $11,304 (15.3% of $73,920 after deduction)

- Federal Income Tax: Additional based on brackets

- Total Tax Burden: Approximately $25,000-$28,000

Why freelancers pay more: W-2 employees split FICA 50/50 with employers. Self-employed individuals pay the entire 15.3%, though half is deductible against income tax. The IRS Self-Employment Tax guide details calculation methods.

Mitigation strategies:

- Maximize business expense deductions

- Consider S-Corp election for high earners ($80K+ net profit)

- Fund Solo 401(k) to reduce taxable income by up to $69,000

Investment Income vs Earned Income Tax Treatment

Not all income faces the same federal income tax rates. Long-term capital gains and qualified dividends receive preferential treatment:

2026 Capital Gains Rates:

- 0%: Taxable income under $48,350 (single), $96,700 (married)

- 15%: Income $48,351-$533,400 (single), $96,701-$600,050 (married)

- 20%: Income above $533,400 (single), $600,050 (married)

Comparison:

| Income Type | $50K Earnings | Tax Rate |

|---|---|---|

| W-2 Wages | $50,000 | 22% marginal |

| Long-Term Capital Gains | $50,000 | 0-15% |

| Qualified Dividends | $50,000 | 0-15% |

| Short-Term Gains | $50,000 | 22% (ordinary income) |

This disparity explains why wealthy investors structure income through long-term investments rather than ordinary wages when possible. Understanding these differences helps optimize your portfolio allocation and withdrawal strategies in retirement, especially when using our Home Equity 4 Ways Use guide for leveraging real estate.

State tax considerations: Most states tax capital gains as ordinary income (exceptions: no-tax states). California charges 13.3% on all gains, while Texas charges zero.

Income Tax 2026: 11 Most-Asked Questions Answered

1. What is the income tax rate for 2026?

Federal income tax rates range from 10% to 37% across seven brackets. Your specific rate depends on filing status and taxable income after deductions. Most middle-income Americans fall in the 12% or 22% marginal brackets.

2. How can I reduce my income tax legally?

Maximize pre-tax retirement contributions (401k, IRA, HSA), claim all eligible credits (Child Tax Credit, EITC, Saver’s Credit), itemize if deductions exceed the standard deduction, and time income/expenses strategically around tax years.

3. What’s the difference between marginal and effective tax rate?

Your marginal rate is the percentage on your last dollar earned. Your effective rate is total tax divided by total income—the actual percentage you pay. Effective rates are always lower due to progressive brackets and deductions.

4. Do I pay the same tax rate on all my income?

No. The progressive system applies different rates to income segments. The first $11,925 (single filer) is taxed at 10%, the next portion at 12%, and so on. Only income exceeding each threshold faces the higher rate.

5. How much income tax will I pay on $100,000?

For a single filer with standard deduction: taxable income is $85,000 ($100K – $15K standard deduction). Federal income tax is approximately $14,260 with an effective rate of 14.3%. State taxes add 0-13.3% depending on residence.

6. What are the new tax brackets for 2026?

The seven federal brackets remain at 10%, 12%, 22%, 24%, 32%, 35%, and 37%, but income thresholds increased 2.8% for inflation. The 22% bracket now starts at $48,476 (single) versus $47,150 in 2025.

7. Can I lower my tax bracket?

Increasing pre-tax deductions (401k contributions, HSA deposits, traditional IRA) directly lowers taxable income and may drop you into a lower marginal bracket. Every $1,000 in deductions saves $120-$370 depending on your bracket.

8. What income is not taxed?

Municipal bond interest, Roth IRA withdrawals (if qualified), life insurance death benefits, gifts/inheritances up to exclusion limits, child support, workers’ compensation, and income below the standard deduction threshold are federally tax-free.

9. How does state income tax work?

Nine states charge zero income tax on wages. Others use progressive brackets (like federal) or flat rates. State taxes are deductible on federal returns only if you itemize, capped at $10,000 for state and local taxes (SALT).

10. What’s the standard deduction for 2026?

$15,000 (single/married filing separately), $30,000 (married filing jointly), and $22,500 (head of household). Those 65+ or blind get additional amounts. Compare against itemized deductions using our eFile Free 2026 tools.

11. When is the tax filing deadline for 2026?

April 15, 2027 for most taxpayers (covering 2026 income). If that date falls on a weekend or holiday, the deadline extends to the next business day. Extensions grant until October 15, but taxes owed must still be paid by April 15 to avoid penalties.

Important Disclaimer

This article is for educational purposes only and does not constitute financial, tax, or legal advice. Tax laws change frequently and vary by individual circumstances and jurisdiction.

Federal income tax regulations are complex, and optimal strategies depend on your specific income sources, deductions, credits, filing status, and state of residence. The examples provided are illustrative and may not reflect your exact situation.

Before making tax decisions, consult a licensed CPA, enrolled agent, or tax attorney who can review your complete financial picture and provide personalized guidance. The IRS offers free resources for general tax questions, while complex situations require professional assistance.

Strategies discussed here are based on 2026 tax law as of February 2026. Congress may modify tax brackets, deductions, or credits during the year. Always verify current regulations before implementing any tax strategy. For additional tools and calculators to model your specific scenarios, visit our comprehensive tools section.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.