Tax Refund 2026: Who Gets $1,000 More & How Fast

The 2026 tax season brings historic refund increases averaging $4,000-$4,200—up $1,000 from 2025. Learn who qualifies for bigger refunds, exact timelines, and expert maximization strategies.

In This Article

The 2026 tax season brings the biggest refund increase in U.S. history, with average refunds jumping to $4,000-$4,200 (up $1,000 from 2025’s $3,167). This surge stems from President Trump’s One Big Beautiful Bill Act (OBBBA), which slashed taxes in 2025 but left paycheck withholdings unchanged. Tip workers, overtime earners, families with children, and seniors 65+ see the largest gains. Track your federal tax refund status starting 24 hours after e-filing, with most payments arriving in 8-21 days via direct deposit—though IRS staffing cuts may delay some refunds beyond this window.

What Makes 2026 the “Biggest Tax Refund Season Ever”?

The 2026 tax filing season marks a historic shift in American tax policy. Bank of America Global Research projects tax refunds will surge by $65-$100 billion compared to 2025, representing an 18% year-over-year increase. This windfall isn’t accidental—it’s the result of deliberate tax cuts that took effect for 2025 income without corresponding adjustments to paycheck withholdings.

Trump’s One Big Beautiful Bill Act (OBBBA) Explained

The OBBBA, passed in summer 2025, fundamentally restructured federal income taxation. Here’s what changed for tax year 2025 (filed in 2026):

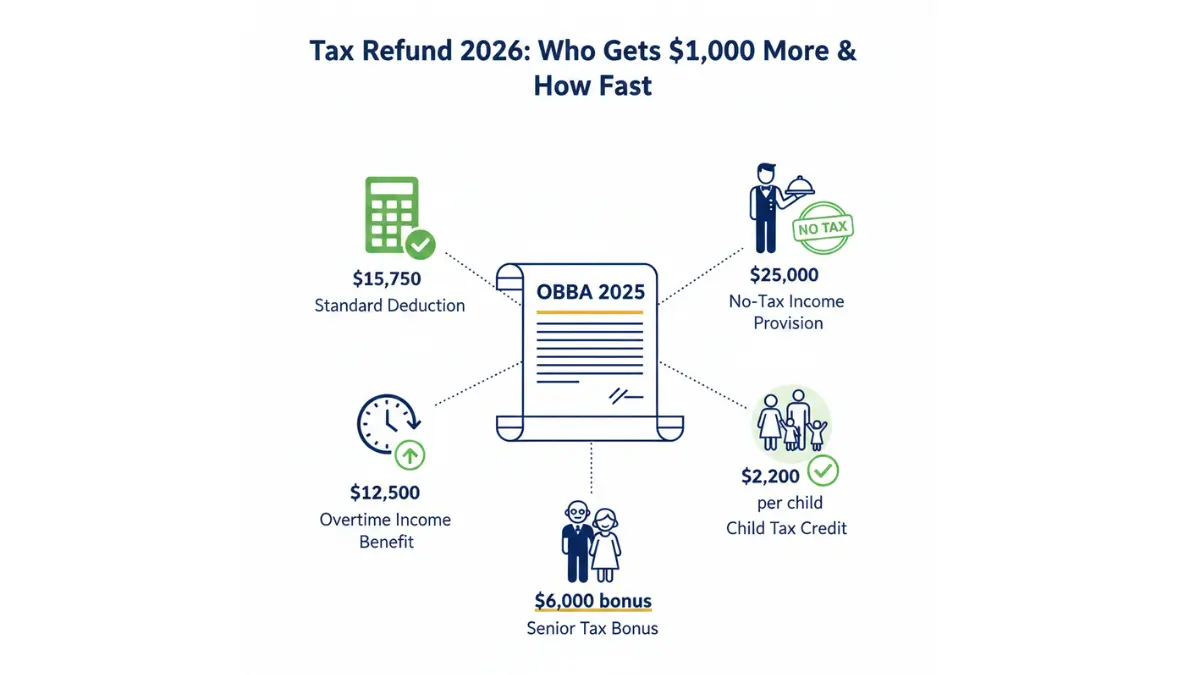

Standard Deduction Increases:

- Single filers: $15,750 (up from $15,000)

- Married filing jointly: $31,500 (up from $30,000)

- Head of household: $22,500 (up from $22,200)

New Income Exclusions:

- Up to $25,000 in tip income: completely tax-free

- Up to $12,500 in overtime pay: exempt from federal taxation

- Social Security benefits: expanded exclusions for middle-income earners

Enhanced Tax Credits:

- Child Tax Credit: $2,200 per qualifying child (up from $2,000), indexed to inflation

- Seniors 65+: Additional $6,000 deduction based on modified adjusted gross income (MAGI)

- State and Local Tax (SALT) deduction cap: expanded for high-tax states

Understanding the 2026 tax brackets helps contextualize how these changes reduce your overall tax burden and increase your potential refund.

Why Refunds Are Bigger (The Withholding Gap)

The refund surge has a simple explanation: the IRS didn’t adjust employer withholding tables to reflect the OBBBA’s tax cuts. Throughout 2025, employers withheld taxes based on 2024 rates—higher than what you actually owe under the new law. When you file your 2025 tax return in 2026, the IRS calculates what you truly owe using the reduced rates, finds you overpaid significantly, and issues a larger refund to correct the difference.

Think of it as an unintentional forced savings account. You paid 2024-level taxes all year but only owe 2025-level taxes when filing. The gap? That’s your bigger refund.

The U.S. Treasury Department confirmed this mechanism in January 2026 statements, noting that while refunds will be larger this year, Americans should adjust their W-4 withholding to avoid repeating this overpayment in 2026.

Who Qualifies for the $1,000+ Refund Boost?

Not all taxpayers benefit equally from the OBBBA’s provisions. Your refund increase depends heavily on which tax breaks you qualify for and how much you overpaid during 2025.

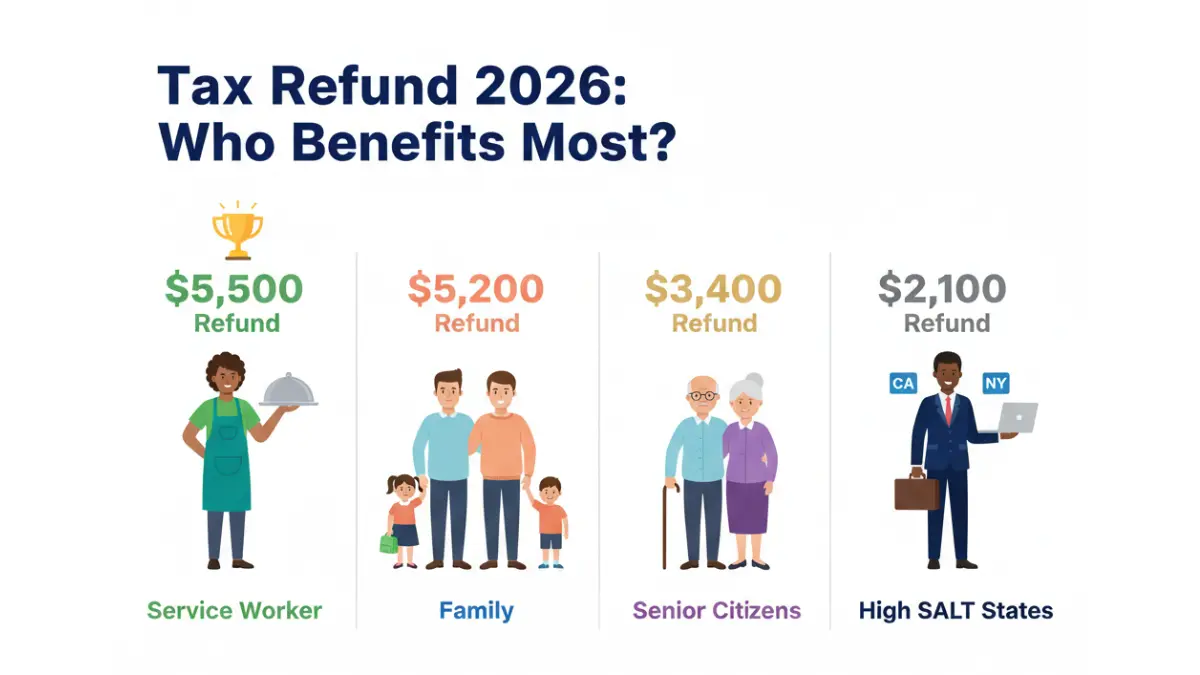

Winner Group #1: Tip & Overtime Workers

Service industry workers are the OBBBA’s biggest winners. Servers, bartenders, hospitality staff, hair stylists, delivery drivers, and anyone receiving regular tips can exclude up to $25,000 in tip income from federal taxation. Similarly, hourly workers who logged substantial overtime can deduct up to $12,500 in overtime wages.

Real Example: Maria, a restaurant server in Dallas, earned $38,000 in base wages plus $22,000 in tips during 2025. Her employer withheld taxes on all $60,000. When filing her 2025 return in February 2026, she excludes the full $22,000 in tips, dropping her taxable income to $38,000. Result: a $5,500 refund instead of the $1,200 she received in 2025.

The National Restaurant Association estimates 2.4 million service workers will save an average of $4,800 annually from this provision alone.

Winner Group #2: Families with Children

The expanded Child Tax Credit delivers $200 more per child compared to 2025. For a family with three children, that’s an extra $600—but the real benefit compounds when combined with the higher standard deduction.

Refund Calculation Example:

- Family of four (married, two children under 17)

- Combined income: $73,000

- Standard deduction: $31,500

- Taxable income: $41,500

- Child Tax Credit: $4,400 (2 children × $2,200)

- Federal income tax liability: $0

This family paid federal taxes throughout 2025 via paycheck withholding but owes nothing when filing. Every dollar withheld becomes a refund. In this scenario, assuming standard withholding rates, the family receives approximately $5,200 back.

Families managing multiple financial priorities should explore our debt consolidation calculator to strategically deploy larger refunds toward high-interest debt elimination.

Winner Group #3: Seniors 65 and Older

Americans 65 and older qualify for a bonus $6,000 standard deduction if their MAGI falls below specific thresholds. This provision particularly benefits retirees with modest pension or Social Security income who still work part-time.

Eligibility Thresholds (2025 tax year):

- Single/Head of Household: MAGI below $100,000

- Married Filing Jointly: MAGI below $200,000

Example: Robert, 67, receives $32,000 in Social Security benefits and earns $28,000 from part-time consulting. Under previous law, his taxable income was higher. With the senior deduction, his tax burden drops by approximately $1,200, converting previous payments into refund dollars.

Winner Group #4: High SALT Deduction States

Residents of California, New York, New Jersey, Connecticut, Illinois, and Massachusetts see expanded SALT deduction caps. While the exact cap varies by filing status, the increase allows upper-middle-income families in high-tax states to deduct more state and local taxes from federal taxable income.

Impact Example: A married couple in Bergen County, NJ, paid $18,000 in property taxes and $12,000 in state income taxes (total $30,000). Under the expanded SALT cap, they deduct significantly more than the previous $10,000 limit, reducing federal taxable income and triggering larger refunds.

Who Gets Less (Or Owes Money)

Three groups see minimal benefit or potentially owe taxes:

- Lower-income filers with no tax liability: If you already paid zero federal income tax, there’s nothing to refund

- Very high earners: Income phase-outs limit or eliminate benefits above certain thresholds

- Insufficient withholding: If you claimed excessive allowances on your 2025 W-4, you may have underpaid despite the tax cuts

| Income Bracket | Family Type | Average Refund Increase |

|---|---|---|

| $30K-$50K | Single, no children | +$350 |

| $50K-$75K | Married, 2 children | +$1,200 |

| $75K-$100K | Single with tips/overtime | +$3,800 |

| $100K-$150K | Married, 2 children, high SALT | +$2,100 |

| $150K+ | Varies widely | +$500 to $2,000+ |

When Will You Get Your 2026 Tax Refund?

Timing your refund requires understanding both standard IRS processing schedules and 2026-specific challenges.

Standard Refund Timelines

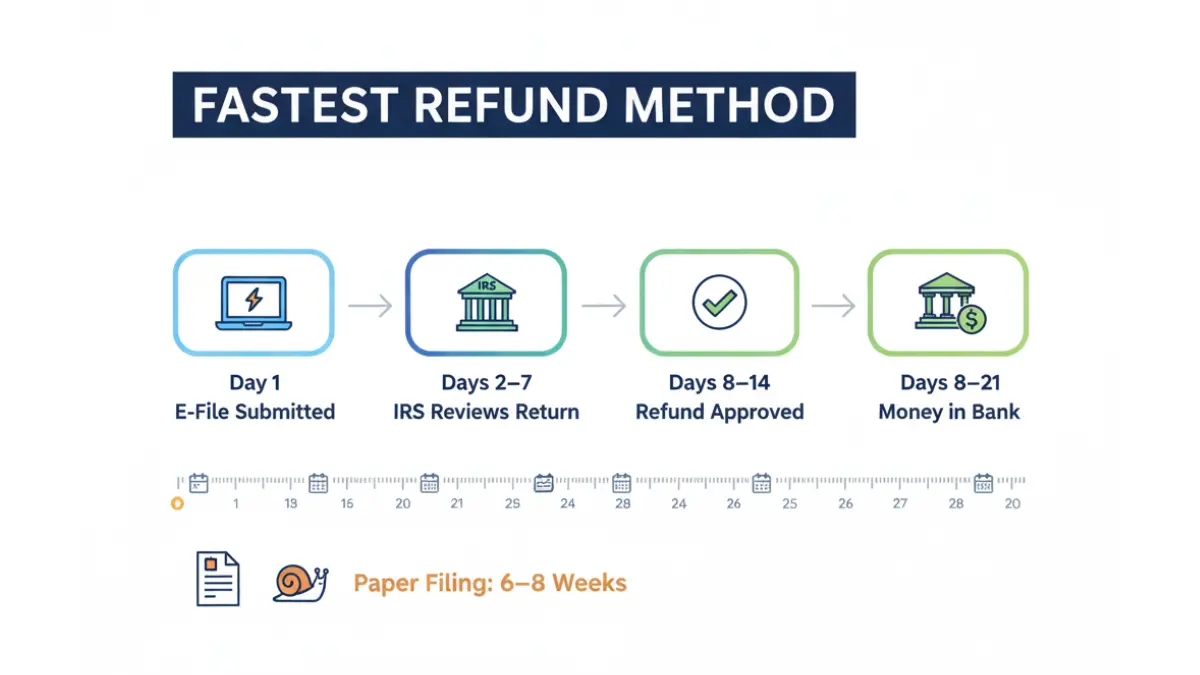

The IRS officially opened the 2026 filing season on January 27, 2026, with an April 15 deadline. E-filing your return dramatically accelerates processing compared to paper filing.

Typical Processing Times:

- E-file + Direct Deposit: 8-21 days (fastest method)

- E-file + Paper Check: 3-4 weeks

- Paper Filing + Direct Deposit: 4-6 weeks

- Paper Filing + Paper Check: 6-8 weeks (slowest)

The IRS recommends checking Where’s My Refund starting 24 hours after e-filing or four weeks after mailing a paper return.

2026 IRS Staffing Crisis Warning

Budget constraints have left the IRS significantly understaffed entering the 2026 filing season. According to reporting from Axios and government watchdog groups, the agency faces its lowest staffing levels in decades while processing what may be the largest refund season in history.

What This Means for You:

- Complex returns requiring manual review may take 30-45 days instead of the standard 21

- Phone wait times for IRS assistance exceed 45 minutes on average

- Amended returns take 20-24 weeks instead of the typical 16

Filing early—ideally by mid-February—minimizes your exposure to processing backlogs. The IRS processes returns in the order received, so February filers typically receive refunds before late March or April filers.

How to Track Your Tax Refund Status

The IRS provides multiple tracking methods, all updated daily:

1. Where’s My Refund? Online Tool

Visit the official IRS tracking portal with your Social Security number, filing status, and exact refund amount. The tool displays three stages:

- Return Received: IRS has your return and began processing

- Refund Approved: IRS approved your refund and scheduled a payment date

- Refund Sent: Money transferred to your bank or check mailed

2. IRS2Go Mobile App

Available for iOS and Android, IRS2Go provides the same information as the web tool with push notifications when your refund status changes. Download from your device’s app store.

3. Automated Phone Hotline

Call 800-829-1954 for refund status 24/7. Have your SSN, filing status, and refund amount ready. Note: this is an automated system; speaking with an agent requires calling 800-829-1040 during business hours (expect long wait times).

What Each Status Update Means

Understanding IRS status updates helps set realistic expectations:

- “Return Received” appears 24-48 hours after e-filing. Your return is in the processing queue. This status typically lasts 7-14 days for straightforward returns.

- “Refund Approved” means IRS completed all reviews, verified your information, and scheduled your payment. The tool displays your expected deposit or check mail date. Count on 5 business days for direct deposits to appear in your account, 2-3 weeks for paper checks.

- “Refund Sent” confirms the IRS transmitted payment. If using direct deposit and funds haven’t appeared after 5 business days, contact your bank. If expecting a paper check and it doesn’t arrive within 4 weeks of this status, call the IRS to request a trace.

Early Access Options & Refund Advance Loans

Some tax preparation services advertise “get your refund up to 5 days early” or offer Refund Advance loans of $250-$4,000 before the IRS even accepts your return.

Pros:

- Immediate access to funds (within 24-48 hours of filing)

- 0% APR on most Refund Advance products

Cons:

- Requires opening a specific bank account (usually)

- Refund amount typically limited to 50% of expected refund

- Ties you to a particular tax software/preparer

- If IRS delays or reduces your refund, you’re responsible for repaying the advance

For most taxpayers, standard direct deposit sufficiently meets timing needs without the complications of early access products. However, those facing financial emergencies might consider these options alongside traditional personal finance strategies like building an emergency fund.

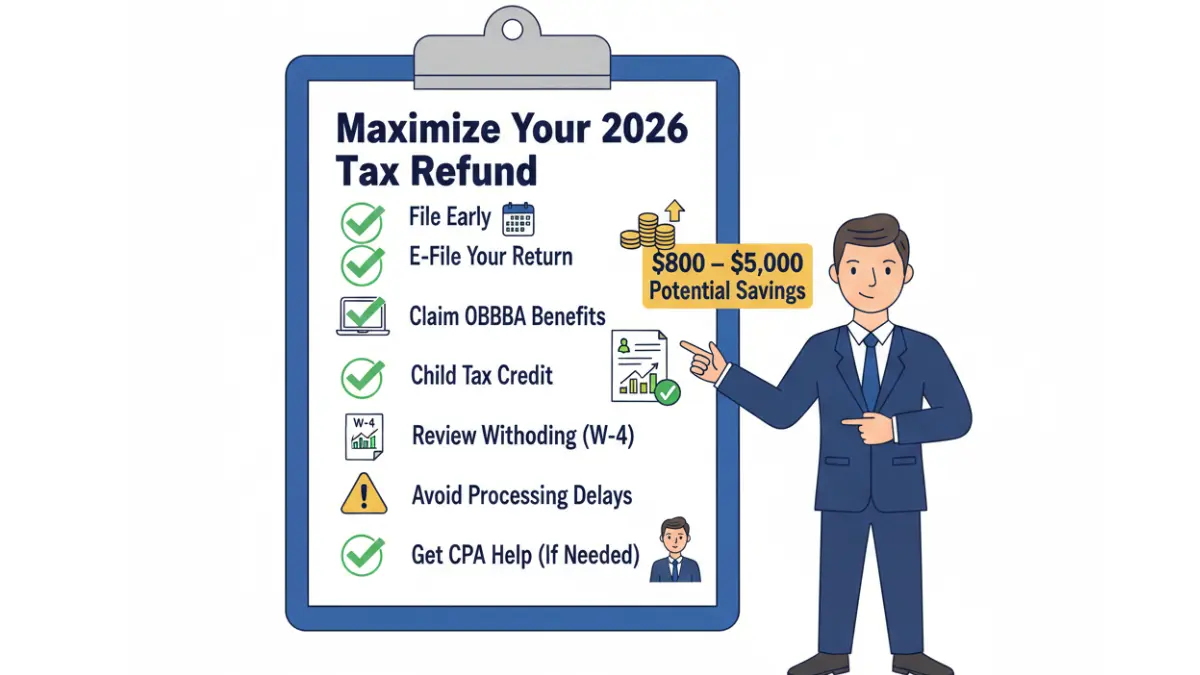

7 Expert Strategies to Maximize Your 2026 Tax Refund

Maximizing your refund requires more than just claiming standard deductions—it demands strategic planning and attention to OBBBA provisions many filers overlook.

Strategy #1: File Early to Beat Delays

The IRS began accepting returns January 27, 2026. Filing within the first four weeks of tax season (before February 24) positions you ahead of the bulk of filers who wait until March or April. Early filers typically receive refunds 3-7 days faster than late filers due to reduced system load.

Additional Benefit: Filing early protects against identity theft. Fraudsters filing fake returns using your SSN get rejected if you’ve already filed a legitimate return.

Strategy #2: Choose E-File + Direct Deposit

Paper filing extends processing by 4-6 weeks compared to electronic filing. The IRS must manually enter paper returns into computer systems—a process prone to errors and delays.

Direct deposit eliminates mail time (2-3 weeks for paper checks) and reduces lost check problems. Verify your bank account and routing numbers carefully; errors cause rejection and restart the refund process.

Use the IRS Free File program if your adjusted gross income is $79,000 or less. Commercial tax software typically costs $60-$200 but offers more features and support.

Strategy #3: Claim All OBBBA Deductions

Many taxpayers miss claiming tip income and overtime exclusions because W-2 forms still show these amounts as taxable. You must actively claim the exclusions when filing.

How to Claim:

- Tip exclusion: Report on Schedule 1, Line 8z (Additional Income)

- Overtime exclusion: Also Schedule 1, with clear notation

- Senior bonus deduction: Automatically applied if you’re 65+ and meet MAGI thresholds

If you’re uncertain about properly claiming these benefits, consider using professional tax software designed to automatically identify and apply all OBBBA provisions.

Strategy #4: Maximize Child Tax Credit

The $2,200-per-child credit phases out at higher incomes but remains fully available for most families. Key points:

- Child must be under 17 on December 31, 2025

- Child must have a valid Social Security number

- Income phase-outs begin at $200,000 (single) or $400,000 (married filing jointly)

If you had a baby in 2025, you qualify for the full credit even if born December 31. Don’t overlook qualifying children like stepchildren, foster children, siblings, or grandchildren if you provided more than half their support.

Strategy #5: Review Your W-4 for Future Years

A large refund means you overpaid taxes all year—essentially giving the government an interest-free loan. While the 2026 refund surge results from the withholding/law change mismatch, you can optimize future years.

Use the IRS Tax Withholding Estimator to calculate proper withholding for 2026. Submit an updated W-4 to your employer to increase your take-home pay rather than getting a large refund next year.

Strategic Choice: Some financial advisors recommend continuing to “overpay” via withholding as a forced savings mechanism. If you lack discipline saving from each paycheck, a refund provides a once-annual lump sum. However, earning interest on that money throughout the year (even at modest rates) beats a zero-return IRS hold.

Strategy #6: Avoid Common Delays

Certain filing errors trigger manual IRS reviews, extending processing from 21 days to 45+ days:

Common Delay Triggers:

- Math errors on forms

- Mismatched SSN for dependents

- Incorrect bank account or routing numbers

- Claiming Earned Income Tax Credit or Additional Child Tax Credit (automatically flags for fraud review)

- Missing or incomplete W-2/1099 forms

- Amended returns (always slower)

Double-check all numbers before e-filing. Many tax software programs flag common errors, but paper filers should verify calculations manually. Cross-reference your 1099 forms and deadlines to ensure you’ve reported all income sources.

Strategy #7: Work with a Financial Professional

Certified Public Accountants (CPAs) and Enrolled Agents (EAs) possess expertise that generic tax software lacks—particularly with complex situations like:

- Multiple income sources (W-2 + 1099 + rental income)

- Small business or self-employment income

- Stock trades, cryptocurrency, or investment income

- Multi-state taxation

- Divorce or alimony

- Foreign income or accounts

Financial Expert Insight:

“We’re seeing taxpayers leave an average $800 on the table by missing deductions they qualify for,” explains Jennifer Martinez, CFP®, a financial advisor on the FinanceAuthorityHub.com expert panel. “The OBBBA introduced provisions that aren’t intuitive—like the tip exclusion calculation rules or senior deduction MAGI limits. Professional preparation pays for itself through maximized refunds and audit protection.”

Many CPAs offer fixed-rate tax preparation (typically $200-$500 for individuals) and include free consultation throughout the year. For those with straightforward situations, paid tax software with expert review options provides a middle ground.

2026 Tax Refund FAQs

1. How much will my 2026 tax refund be?

Your refund depends on your specific income, deductions, credits, and withholding throughout 2025. The national average is projected at $4,000-$4,200, but individual refunds range from $0 to $10,000+. Use a tax refund calculator or your tax software’s estimator for personalized predictions.

2. When did the 2026 tax filing season start?

The IRS began accepting 2025 tax returns on January 27, 2026. The deadline to file without an extension is April 15, 2026 (or the next business day if April 15 falls on a weekend/holiday). Extensions grant until October 15, 2026, but you must still pay any taxes owed by April 15 to avoid penalties.

3. What is the One Big Beautiful Bill Act (OBBBA)?

The OBBBA is comprehensive tax legislation signed into law in 2025 that:

– Increased standard deductions

– Eliminated federal tax on tip and overtime income (up to limits)

– Expanded Child Tax Credit to $2,200 per child

– Created a senior bonus deduction ($6,000 for those 65+)

– Raised SALT deduction caps

Learn more about how tax law changes affect your income tax brackets and overall tax liability.

4. Is there a $1,000 stimulus check coming?

No. Media reports about “$1,000 more” refer to increased tax refunds, not a separate stimulus payment. There are no federal stimulus checks scheduled for 2026. The refund increase stems from tax law changes (OBBBA), not direct government payments like pandemic-era stimulus.

5. What happens if I enter the wrong bank account number?

Contact the IRS immediately at 800-829-1040 if you discover the error before the refund is sent. If the deposit already went to the wrong account, contact your bank and the receiving bank to attempt recovery. The IRS cannot reverse direct deposits once transmitted. If recovery fails, you’ll need to pursue the funds through your bank’s dispute process.

In extreme cases where funds cannot be recovered, you may need to request a payment trace from the IRS, which can take 6-8 weeks to investigate and potentially issue a replacement check.

6. Are tax refunds taxable income?

Federal income tax refunds are never taxable for federal purposes. However, if you itemized deductions on your prior year return and claimed state/local tax deductions, your state refund may be taxable income on your current year federal return. The IRS will send Form 1099-G if your state refund exceeds $10.

Most taxpayers taking the standard deduction don’t face this issue. Understanding the interaction between tax brackets and deductions helps optimize your long-term tax strategy.

Why is my refund taking longer than 21 days?

Several factors delay processing beyond the standard 21-day window:

- IRS staffing shortages: 2026’s budget constraints slowed processing agency-wide

- Return errors: Math mistakes, mismatched SSN, or incomplete forms trigger manual review

- Earned Income Tax Credit (EITC) or Child Tax Credit claims: These automatically undergo fraud verification, adding 2-4 weeks

- Amended returns: Always take 16-24 weeks

- Outstanding debts: If you owe back taxes, child support, or student loans, IRS offsets your refund to pay those debts before sending you the balance

Check your refund status for specific information about your return.

Can I still get a refund if I owe back taxes?

It depends. The IRS will offset (deduct from) your 2026 refund to pay:

- Unpaid federal taxes from previous years

- State tax debts

- Past-due child support

- Federal student loan defaults

- Other government debts

You’ll receive a notice explaining the offset amount. If your refund exceeds your debts, you’ll receive the difference. If your debts exceed your refund, you’ll receive nothing and still owe the balance.

How do I get my tax refund faster?

Three methods accelerate refund delivery:

- E-file instead of paper filing: Saves 4-6 weeks

- Choose direct deposit over paper check: Saves 2-3 weeks mail time

- File early: Beat the processing backlog (file by mid-February)

Combined, these strategies can reduce your refund wait from 8 weeks to just 8-10 days.

What if I didn’t work in 2025?

You may still need to file and could qualify for a refund if:

- You had taxes withheld from any income (unemployment, pension, Social Security)

- You qualify for refundable credits like EITC even with minimal income

- You want to start your three-year refund claim period

Check IRS filing requirements to determine if you must file based on your income level and filing status.

Can I split my refund into multiple accounts?

Yes. IRS Form 8888 allows you to split your refund into up to three different accounts—checking, savings, retirement accounts, or even U.S. Series I Savings Bonds. This strategy helps automate savings, with many financial advisors recommending:

- 50% to checking for immediate bills

- 30% to savings for emergency fund building

- 20% to retirement accounts like a Roth IRA

Disclaimer

This article provides educational information about tax refunds and related topics for the 2026 tax filing season. It is not tax advice, financial advice, or a substitute for consultation with a qualified tax professional or certified financial advisor.

Tax situations vary significantly based on individual circumstances, filing status, income sources, deductions, and credits. While we strive for accuracy, tax laws change frequently and interpretation can vary.

For personalized guidance about your specific tax situation, consult a Certified Public Accountant (CPA), Enrolled Agent (EA), or tax attorney. For official tax information, forms, and instructions, visit IRS.gov or call the IRS directly at 800-829-1040.

FinanceAuthorityHub.com provides financial education but does not provide tax preparation, filing services, or individualized financial advice. All information is current as of February 2026 and subject to change.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.