Care Health Insurance: Real Cost & Truth in 2026

Care Health Insurance offers 24,800+ cashless hospitals & 96.74% CSR — but high complaint rates hide a truth most buyers miss. Get the full expert breakdown for 2026.

In This Article

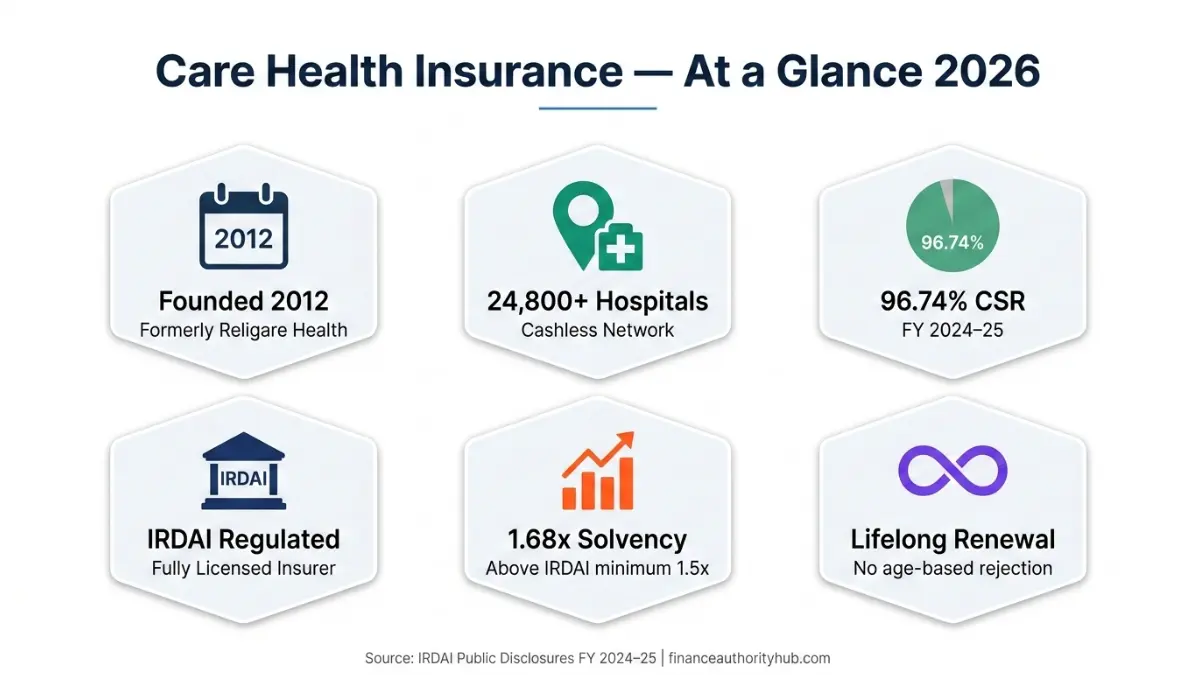

Care Health Insurance is India’s leading standalone health insurer — formerly known as Religare Health Insurance — offering individual, family, and senior citizen plans with a network of 24,800+ cashless hospitals across India. In 2026, with medical inflation running at 14% annually, choosing the right care health insurance plan has never mattered more. This article gives you every number, every gap, and every truth that competitors hide.

What Is Care Health Insurance? (The Truth Most Sites Skip)

From Religare to Care Health: The Rebrand That Confuses Millions

Many buyers still search for “Religare Health Insurance” without knowing it was rebranded as Care Health Insurance in 2012. The brand pivot aligned with a customer-first promise — but the confusion costs buyers time when comparing policies.

Care Health Insurance At a Glance (2026)

| Factor | Detail |

|---|---|

| Founded | 2012 (formerly Religare Health Insurance) |

| Regulator | IRDAI (Insurance Regulatory and Development Authority of India) |

| Network Hospitals | 24,800+ cashless hospitals |

| Claim Settlement Ratio | 96.74% (FY 2024–25) |

| Solvency Ratio | 1.68x (industry minimum: 1.5x) |

| Plans Available | 12+ individual, family, senior, and critical illness plans |

| Minimum Entry Age | 91 days (family floater basis) |

| Renewability | Lifelong |

Care Health Insurance is a standalone health insurer — meaning 100% of its business is health insurance, unlike general insurers who sell motor, property, and travel alongside health. This focus translates to deeper claims expertise.

Who Is Care Health Insurance Best For?

Care health insurance plans are strongest for:

- Young families who want unlimited restoration of sum insured

- Individuals in metro cities seeking cashless access at premium hospitals

- Buyers wanting add-ons like OPD cover, no room rent capping, and international coverage

- People with pre-existing conditions who can afford a 2–3 year waiting period trade-off for lower premiums

If you’re comparing care health insurance versus other coverage types, also review our guide to health insurance plans for a broader framework.

Care Health Insurance Plans — Full 2026 Breakdown

Which Care Health Insurance Plan Matches Your Needs?

Care offers 12+ health insurance plans in 2026. Here are the most searched and purchased:

Master Plan Comparison Table — Care Health Insurance 2026

| Plan Name | Sum Insured | Key Unique Feature | Best For | PED Waiting Period | Room Rent Cap |

|---|---|---|---|---|---|

| Care Supreme | ₹5L – ₹6Cr | 500% Cumulative Bonus | Young families, long-term buyers | 3 years (reducible to 1 yr) | No cap (top variants) |

| Care Classic | ₹3L – ₹10L | Unlimited Recharge | First-time buyers | 4 years | Room-rent sub-limits apply |

| Care Plus | ₹3L – ₹75L | Global Emergency Cover | Frequent travellers | 3 years | No cap |

| Care Freedom | ₹3L – ₹10L | Zero waiting for PED (with co-pay) | Diabetics, BP patients | Zero (20-30% co-pay) | Sub-limits |

| Care Heart | ₹3L – ₹10L | Covers pre-existing cardiac conditions | Cardiac patients | Zero (20-30% co-pay) | Sub-limits |

| Care Senior | ₹3L – ₹10L | Designed for 61–75 age group | Retired individuals | 4 years | Sub-limits |

| Care Critical Mediclaim | ₹5L – ₹40L | Lump-sum for 32 critical illnesses | High-income earners | 90 days | N/A (lump-sum payout) |

What This Means For You: If you’re a first-time buyer under 35, Care Supreme is the 2026 market leader. Its cumulative bonus grows your sum insured up to 500% over time — the best compound health protection in the segment.

The Hidden Features Most Buyers Miss

- Unlimited Automatic Recharge: If your sum insured is exhausted, it refills automatically — unlimited times per policy year. Standard policies don’t offer this.

- Cashless Anywhere: Care’s 2026 feature allows cashless claims even at non-network hospitals in emergencies.

- AYUSH Coverage: Covers Ayurveda, Yoga, Unani, Siddha, and Homeopathy treatments — as mandated by IRDAI health insurance regulations.

- Inflation Protection: Sum insured increases automatically with medical inflation. No extra premium required in select plans.

For a deeper dive into how care health insurance plans compare to private medical options globally, read our private medical insurance guide.

The Real Cost — Care Health Insurance Premiums in 2026

What You’ll Actually Pay for Care Health Insurance in 2026

Medical inflation is rising at 14% annually in India in 2026. A single hospital stay can now cost ₹2–5 lakh for a standard procedure in a metro city. The question isn’t whether you need care health insurance — it’s whether your sum insured is enough.

Estimated Annual Premium Table — Care Supreme (2026)

| Profile | Sum Insured | Approx. Annual Premium |

|---|---|---|

| Single adult, age 28 | ₹10 lakh | ₹8,500 – ₹11,000 |

| Single adult, age 45 | ₹10 lakh | ₹18,000 – ₹24,000 |

| Family of 3 (floater), age 35 | ₹10 lakh | ₹16,000 – ₹22,000 |

| Family of 3 (floater), age 45 | ₹20 lakh | ₹28,000 – ₹36,000 |

| Senior couple, age 60–65 | ₹5 lakh | ₹42,000 – ₹58,000 |

Premiums are indicative and vary by city tier, add-ons selected, and underwriting. Always get a personalised quote from careinsurance.com.

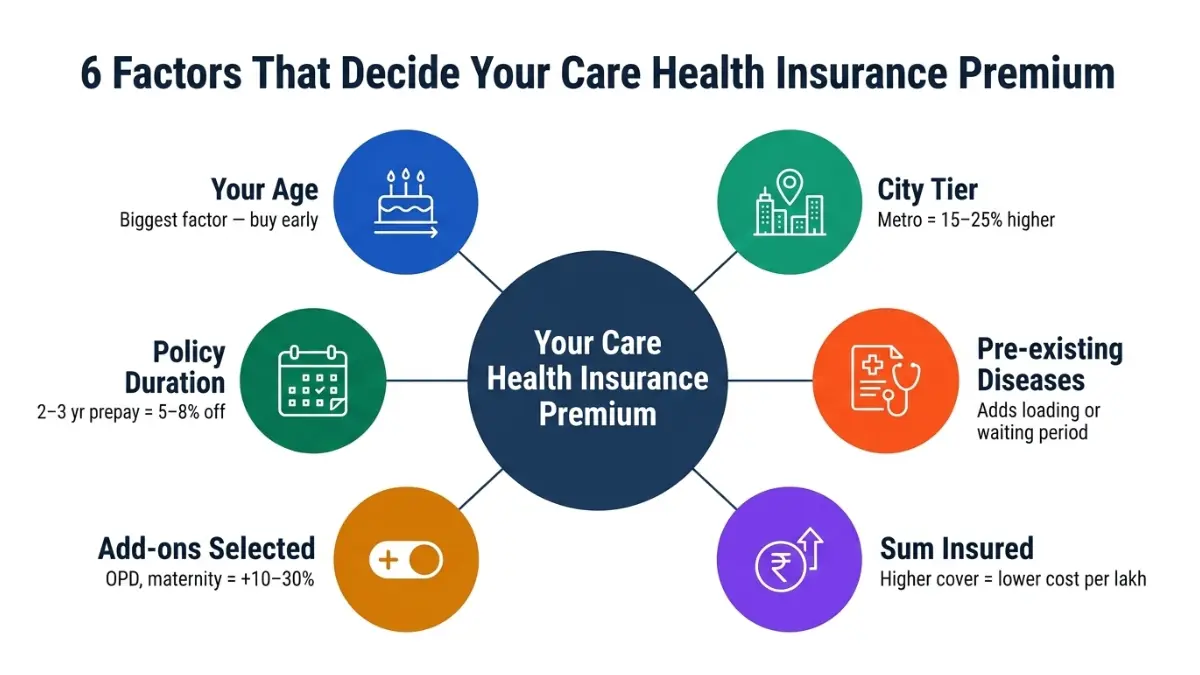

What Drives Your Care Health Insurance Premium Up

- Age — biggest single factor; premiums rise sharply post-45

- City tier — metro premiums 15–25% higher than Tier 2 cities

- Pre-existing diseases — disclosed PEDs trigger loading or waiting periods

- Add-ons selected — OPD cover, international cover, and maternity riders add 10–30% to base premium

- Sum insured chosen — higher coverage = proportionally lower cost per lakh

5 Legal Ways to Reduce Your Care Health Insurance Premium

- Buy early — A 28-year-old pays nearly 60% less than a 45-year-old for identical coverage

- Pay multi-year premiums — Care offers 5–8% discount for 2–3 year policies

- Go for higher deductibles on super top-up plans to lower base cost

- Use no-claim bonus — up to 50% sum insured increase for each claim-free year

- Choose Tier 2 city address if you primarily live outside metros

What This Means For You: Every year you delay buying care health insurance costs you more in premiums and risks gaps in coverage during a claim period. A 30-year-old buying today pays roughly ₹9,000/year for ₹10L cover. At 45, that same cover costs ₹21,000+.

Claim Settlement Ratio — The Number That Can Save or Cost You Lakhs

Care Health Insurance Claim Settlement Ratio 2026: Honest Numbers

Most buyers fixate on premiums and ignore the single most critical metric: how reliably does the insurer pay when you need it most?

CSR vs ICR — What’s the Real Difference?

| Metric | What It Measures | Care’s 2026 Figure |

|---|---|---|

| Claim Settlement Ratio (CSR) | % of claims settled (count-based) | 96.74% (FY 2024–25) |

| Incurred Claim Ratio (ICR) | Total claims paid ÷ total premium collected (amount-based) | 57.69% (FY 2023) |

| Complaint Rate | Claims complaints per 10,000 policies | 42 per 10,000 (high vs. industry) |

Reading the numbers honestly:

- A 96.74% CSR means roughly 97 out of every 100 claims get settled — above the industry average of ~94%

- The 57.69% ICR is healthy for insurers (means they have reserves to pay future claims)

- The high complaint volume (42/10,000) is a red flag — it means claim processes can be delayed or disputed even when eventually settled

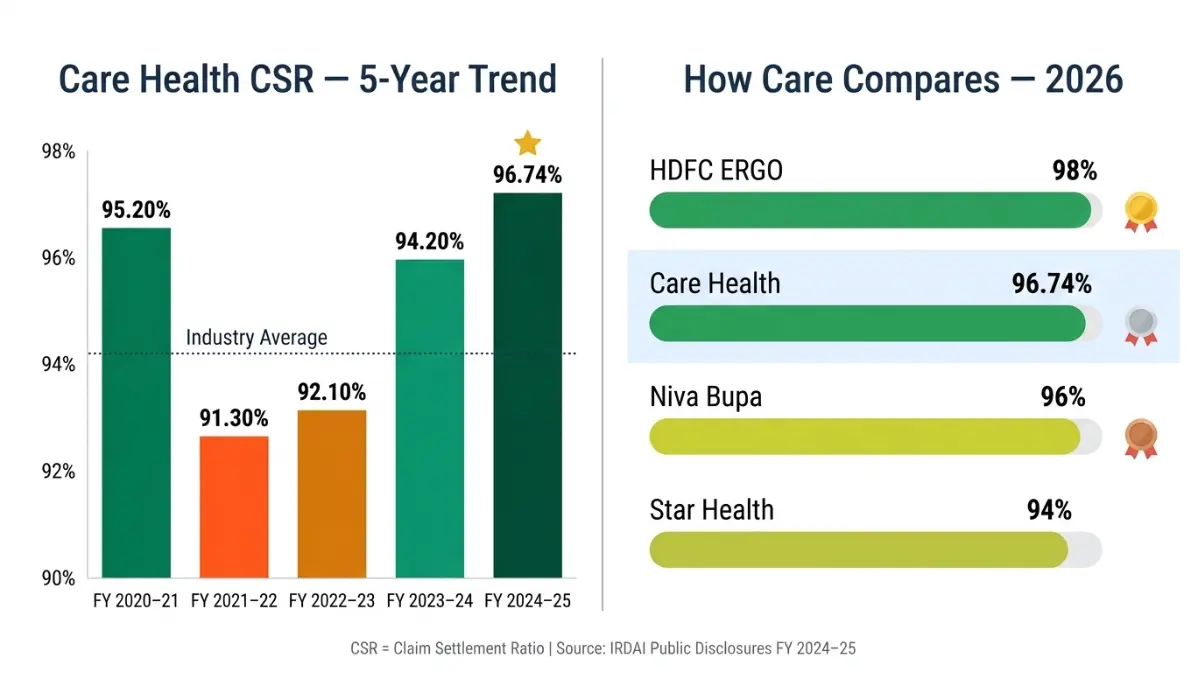

Care Health Insurance’s CSR for FY 2024-25 stands at 96.74%, and its 3-year average from FY 2022–25 is 93.13% — solid but not flawless. According to IRDAI’s health insurance guidelines, insurers must settle or reject cashless claims within 1 hour of authorisation, and reimbursement claims within 30 days.

Care’s 5-Year CSR Trend

| Financial Year | CSR % | Verdict |

|---|---|---|

| FY 2020–21 | 95.20% | Strong |

| FY 2021–22 | 91.30% | Dip (COVID-era claims surge) |

| FY 2022–23 | 92.10% | Recovery |

| FY 2023–24 | 94.20% | Improving |

| FY 2024–25 | 96.74% | Best in 5 years |

Your 7-Step Claims Survival Guide (Exclusive — No Competitor Offers This)

The complaint data is real. Here’s how to protect yourself:

- Disclose all pre-existing diseases honestly at policy inception — non-disclosure is the #1 reason for claim rejection

- Always use network hospitals for planned procedures to access cashless facility

- Intimate your insurer within 24 hours of emergency hospitalisation

- Collect all original bills and discharge summaries — digital scans accepted but originals needed for disputes

- Submit reimbursement claims within 30 days of discharge — delays trigger automatic review

- File a complaint with the IRDAI Grievance Portal if your claim is wrongly rejected

- Request a second opinion on rejection letters — many rejections are overturned with additional documentation

Care Health Insurance vs Competitors — 2026 Verdict

Care vs Niva Bupa vs Star Health vs HDFC ERGO (The Definitive 2026 Comparison)

The 4-Way Master Comparison Table

| Factor | Care Health | Niva Bupa | Star Health | HDFC ERGO |

|---|---|---|---|---|

| CSR (FY 2024–25) | 96.74% | ~96% | ~94% | ~98% |

| Network Hospitals | 24,800+ | 10,000+ | 14,000+ | 13,000+ |

| Best Flagship Plan | Care Supreme | ReAssure 2.0 | Family Health Optima | Optima Secure |

| Room Rent Cap | None (top plans) | None | Sub-limits on base plans | None |

| Unique Differentiator | 500% Cumulative Bonus | Lifetime ReAssure Benefit | In-house claims (no TPA) | 2X Coverage from Day 1 |

| Complaint Rate | High (42/10K) | Moderate | Low | Low |

| Premiums (₹10L, age 35) | ₹16–22K | ₹18–25K | ₹14–20K | ₹19–28K |

| IRDAI Status | ✅ Registered | ✅ Registered | ✅ Registered | ✅ Registered |

When to Choose Care Health Insurance

✅ You want the largest cashless network (24,800+ hospitals — largest in segment) ✅ You’re a young buyer who wants 500% bonus growth over time ✅ You need OPD + international cover in one plan ✅ You have pre-existing cardiac/diabetic conditions (Care Freedom/Heart plans)

When NOT to Choose Care Health Insurance

❌ You need zero complaints in claims processing — HDFC ERGO or Star Health perform better ❌ You’re price-sensitive and want the lowest base premium — Star Health is cheaper on base plans ❌ You want a TPA-free, in-house settlement experience — Star Health has this advantage

Expert Panel Verdict (financeauthorityhub.com): Care Health Insurance is a strong choice for comprehensive, long-term family coverage — especially with the Care Supreme plan. However, buyers who anticipate frequent claims or have complex medical histories should weigh HDFC ERGO Optima Secure for its superior complaint track record.

Johns Hopkins Bloomberg School of Public Health researchers confirm that health insurance affordability has worsened significantly in 2026, making it essential to evaluate insurers not just on premiums but on reliability of claim payout. This is exactly why CSR and complaint rate analysis matters.

Also compare your health insurance expert math before finalising any plan.

How to Buy or Renew Care Health Insurance in 2026 (Avoid These Mistakes)

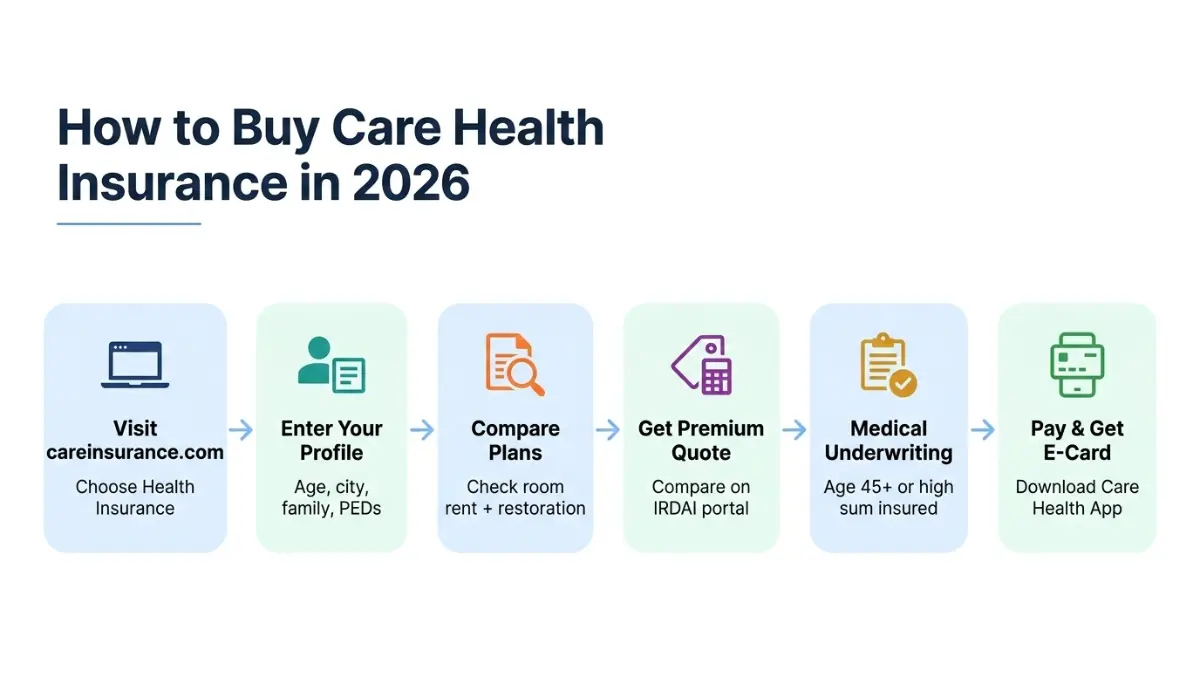

Step-by-Step: How to Buy Care Health Insurance Online

- Visit careinsurance.com → Choose ‘Health Insurance’ → Select your plan type

- Enter your profile — age, city, family members, pre-existing conditions

- Compare plans and add-ons — always check room rent cap and restoration benefit

- Get your premium quote — compare with alternatives on IRDAI’s policyholder portal

- Complete medical underwriting (if age 45+ or high sum insured)

- Pay and receive your e-card — download Care Health app immediately for hospital access

Renewing Your Care Health Insurance Policy

- Renew at least 30 days before expiry to avoid break in coverage

- A policy break resets the waiting period for pre-existing diseases — losing continuity benefits you’ve earned

- At renewal, review your sum insured — if you bought ₹5L cover 5 years ago, you likely need ₹15–20L in 2026 given medical inflation

5 Costly Mistakes to Avoid

- Choosing the cheapest plan without checking room rent limits — sub-limits mean you pay the difference for premium rooms out of pocket

- Not disclosing pre-existing conditions — leads to claim rejection when you need it most

- Ignoring the restoration benefit — without it, a family member’s major claim could exhaust your entire sum insured

- Buying low sum insured — ₹3–5L is insufficient for a metro hospital stay in 2026; aim for ₹10L minimum

- Skipping the waiting period reduction rider — for ₹1,000–₹2,000 extra per year, you can cut PED waiting from 4 years to 1 year

Documents Required for Care Health Insurance

- Aadhaar card / PAN card (ID proof)

- Recent passport-size photographs

- Medical reports (if age 45+ or pre-existing conditions declared)

- Cancelled cheque (for cashless card setup)

To understand how your health insurance premiums impact your broader financial plan, explore our guide on term insurance real costs and life insurance rates, types, and savings. If you’re also managing dental care costs, our dental insurance plans guide covers what most health policies don’t include.

For those in the UK and Commonwealth markets also evaluating options, our private medical insurance guide provides a global framework comparison.

Frequently Asked Questions — Care Health Insurance 2026

Q1. Is Care Health Insurance good in 2026?

Yes — Care Health Insurance is a strong, IRDAI-regulated insurer with a 96.74% CSR, 24,800+ network hospitals, and comprehensive plans. However, its higher complaint rate makes it essential to document all claims carefully.

Q2. What is Care Health Insurance’s claim settlement ratio?

Care’s CSR for FY 2024–25 is 96.74%, with a 3-year average of 93.13% (FY 2022–25). Above industry average but below HDFC ERGO’s ~98%.

Q3. How many hospitals are in Care Health Insurance’s cashless network?

Care Health Insurance has 24,800+ cashless network hospitals across India, making it one of the widest networks among standalone health insurers.

Q4. What is the waiting period for pre-existing diseases in Care plans?

Standard waiting period is 3–4 years depending on the plan. Care Freedom and Care Heart plans cover pre-existing conditions from Day 1 with a 20–30% co-payment.

Q5. Is Care Health Insurance the same as Religare?

Yes. Care Health Insurance was formerly known as Religare Health Insurance and was rebranded in 2012. The company, management, and IRDAI registration are the same entity.

Q6. How do I renew my Care Health Insurance policy?

Log in to careinsurance.com, go to ‘Renewals’, enter your policy number, review the new premium, and pay online. Renew at least 30 days before expiry to protect continuity benefits.

Q7. Does Care Health Insurance cover OPD expenses?

Yes — select Care plans include OPD cover for consultations, medicines, and diagnostic tests. OPD coverage is not standard across all plans; check your plan’s schedule of benefits.

Q8. What is the Care Supreme plan and is it worth it?

Care Supreme is Care’s flagship plan, offering 500% cumulative bonus, unlimited restoration, and no room rent capping (on higher variants). It is worth the premium for long-term family coverage.

Q9. Can I port my existing health insurance policy to Care Health Insurance?

Yes. IRDAI allows portability between health insurers. You retain your waiting period credits from your previous insurer. Apply for porting at least 45 days before renewal.

Q10. What documents are needed to file a Care Health Insurance claim?

For cashless: hospital’s pre-authorisation form, e-health card, government ID. For reimbursement: original bills, discharge summary, prescriptions, filled claim form, and cancelled cheque.

Q11. How does Care Health Insurance compare to Niva Bupa?

Care has a larger hospital network (24,800+ vs 10,000+) and stronger cumulative bonus. Niva Bupa’s ReAssure Lifetime Benefit is unique. For complaint rates, Niva Bupa performs better. Best choice depends on your city’s hospital network coverage.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, insurance, or legal advice. Premium figures are estimates based on publicly available data and may vary based on individual profile, city tier, add-ons, and underwriting decisions by the insurer. Always verify current data directly with IRDAI’s official portal or Care Health Insurance’s official website before making any purchase decision. financeauthorityhub.com does not sell, endorse, or receive compensation from any insurance product or company.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.