Renters Insurance: Is It Worth It? (2026 Guide)

Is renters insurance worth it in 2026? For 95% of renters, yes. At $15–$24/month, it protects $30,000+ in belongings and shields you from $100,000+ liability claims. Learn what’s covered, real costs, and when to skip it.

In This Article

The Verdict — Is Renters Insurance Worth It?

Is Renters Insurance Worth It? The Short Answer

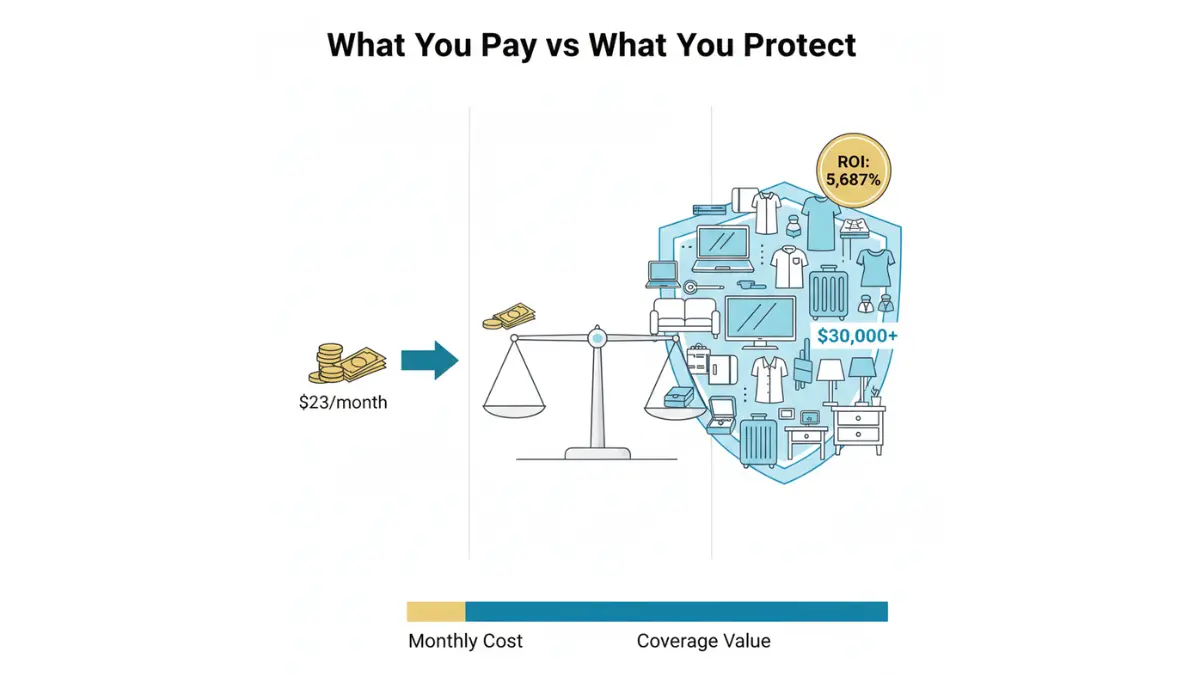

Yes, renters insurance is worth it for 95% of renters. Here’s the brutal math: the average renters insurance policy costs $23 per month ($276 annually) but protects $30,000+ in belongings and shields you from liability claims that could reach $100,000 or more.

The return on investment is staggering. You’re essentially paying less than one dollar per day to protect years of accumulated possessions and avoid financial catastrophe.

The Math: What You Pay vs. What You Risk

Let’s break down the actual numbers that matter in 2026:

What You Pay:

- National average premium: $15–$24/month

- Annual cost: $180–$288

- Daily cost: $0.49–$0.79

What You Risk Without Coverage:

- Average apartment contents value: $30,000–$50,000

- Average renters insurance claim payout: $6,900

- Potential liability lawsuit: $100,000+

- Fire damage replacement costs: $20,000–$40,000

The 5% who might skip renters insurance? Extreme minimalists with less than $5,000 in total belongings, no liability concerns, and sufficient emergency savings to replace everything immediately. Even then, most financial experts recommend coverage.

Real Claim Case Study: 2025 Apartment Fire (Atlanta)

In March 2025, Sarah Chen’s Atlanta apartment building caught fire from a neighboring unit’s electrical malfunction. She lost everything: furniture, electronics, clothing, jewelry, and important documents.

Her situation:

- Monthly premium: $18

- Total paid over 2 years: $432

- Belongings value: $23,400

- Insurance payout: $21,800 (replacement cost coverage)

- Hotel costs covered (30 days): $3,200

- Total received: $25,000

Sarah’s renters insurance delivered a 5,687% return on her investment. Without coverage, she would have faced crushing debt to replace basic necessities.

The decision framework is simple:

| Your Situation | Renters Insurance Worth It? |

|---|---|

| Living in apartment/rental home | YES |

| Belongings worth >$10,000 | YES |

| Landlord requires coverage | YES (legally mandatory) |

| Own expensive electronics/jewelry | YES |

| Have roommates or guests frequently | YES (liability protection) |

| Extreme minimalist (<$5K belongings) | MAYBE |

According to the National Association of Insurance Commissioners, only 55% of renters carry insurance despite 95% benefiting from coverage. Don’t be part of the unprotected majority.

If you’re evaluating overall financial protection strategies, understanding insurance fundamentals helps you make smarter decisions across all coverage types.

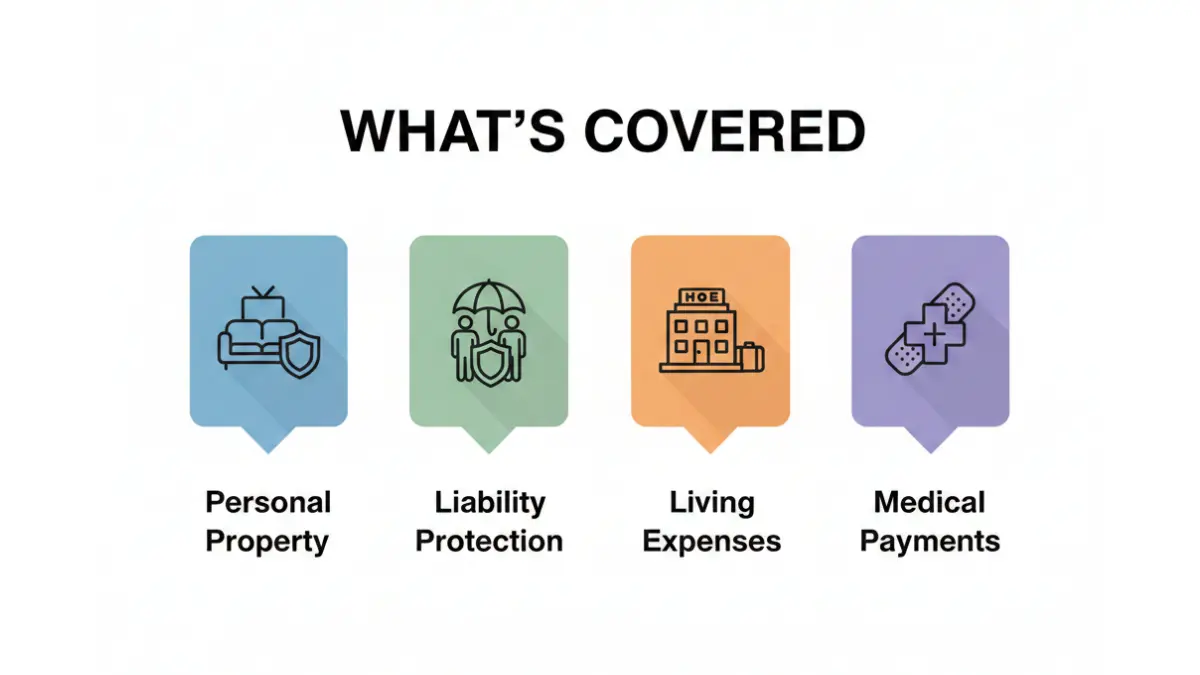

What Renters Insurance Actually Covers (& Doesn’t)

What Does Renters Insurance Cover? The Complete 2026 Breakdown

Renters insurance isn’t one-size-fits-all. Understanding exactly what’s covered—and critically, what’s not—prevents devastating surprises during claims.

Standard renters insurance (called an HO-4 policy) provides four core protections that work together to shield your finances.

Personal Property Coverage: What’s Protected

This covers your belongings when damaged or destroyed by 16 named perils including fire, theft, vandalism, smoke, lightning, windstorm, and water damage from burst pipes.

What’s typically covered:

- Furniture and appliances

- Electronics (computers, TVs, gaming systems)

- Clothing and shoes

- Kitchenware and dishes

- Books and documents

- Sports equipment

- Some jewelry and collectibles (with limits)

Critical limits to know:

- Jewelry: Usually capped at $1,000–$2,500

- Electronics: Individual item limits of $2,500–$5,000

- Cash: Typically $200 maximum

- Bicycles: Often limited to $1,000 per bike

You’ll choose between actual cash value (ACV) coverage, which pays depreciated value, or replacement cost coverage, which pays full replacement—the latter costs 10–15% more but provides substantially better protection.

Liability Protection: When Someone Gets Hurt

Personal liability coverage protects you when you’re legally responsible for injuries to others or damage to their property. Standard policies include $100,000 in coverage, though experts recommend $300,000+ for renters with significant assets.

Real scenarios where liability coverage saves you:

- Guest slips on your wet floor and breaks their wrist

- Your dog bites a neighbor

- Your overflowing bathtub damages the apartment below

- You accidentally damage your landlord’s property

- Guest trips over your belongings and sues for medical costs

According to Insurance Information Institute data, the average liability claim exceeds $15,000. Without coverage, you’re personally liable for legal defense costs plus any settlement or judgment.

Additional Living Expenses (ALE): Displacement Coverage

When your rental becomes uninhabitable due to covered damage, ALE coverage pays for temporary housing, food, and other necessary expenses above your normal costs.

What ALE typically covers:

- Hotel or temporary rental costs

- Restaurant meals (above usual food budget)

- Laundry and dry cleaning

- Pet boarding

- Storage unit rental

- Moving costs

Most policies cap ALE at 12 months or 20% of your personal property coverage limit. If you have $30,000 in property coverage, you’d get up to $6,000 for additional living expenses.

Medical Payments to Others

This covers medical expenses for guests injured at your rental, regardless of fault. Standard coverage ranges from $1,000–$5,000 per person and helps prevent small injuries from becoming liability lawsuits.

What Renters Insurance Does NOT Cover (Critical Exclusions)

Understanding exclusions prevents claim denials when you need coverage most. These perils require separate policies or endorsements:

Never covered without special riders:

- Flood damage: Requires separate FEMA flood insurance

- Earthquake damage: Needs earthquake endorsement

- Pest damage: Bed bugs, termites, rodents excluded

- Intentional damage: By you or household members

- Normal wear and tear: Gradual deterioration

- Vehicle damage: Covered by auto insurance

- Business equipment: Requires business insurance

- Roommate belongings: See critical section below

High-value item limitations: Standard policies severely limit coverage for:

- Jewelry and watches

- Fine art and collectibles

- Musical instruments

- Camera equipment

- Furs and designer clothing

- Silverware and fine china

Purchase scheduled personal property endorsements to fully protect these items.

The Roommate Coverage Myth

This is critical: Your renters insurance covers ONLY your belongings, not your roommate’s possessions. This surprises 78% of renters with roommates, according to industry surveys.

Each roommate needs their own policy. When disaster strikes, uninsured roommates lose everything with no recourse.

Example scenario: Alex and Jordan share an apartment. Alex has renters insurance; Jordan doesn’t. A fire destroys the unit. Alex’s $30,000 in belongings gets replaced. Jordan’s $25,000 in belongings? Total loss with zero compensation.

Some insurers offer roommate endorsements allowing multiple names on one policy, but separate policies typically provide better coverage and clearer claims processes.

The coverage landscape has evolved significantly—understanding modern insurance strategies helps you avoid common pitfalls across all policy types.

How Much Does Renters Insurance Cost In 2026?

Renters Insurance Cost: Real 2026 Pricing Data

Renters insurance remains one of the most affordable insurance types in 2026, with national averages ranging from $15–$24 per month depending on coverage levels and location.

2026 National Averages:

- Low coverage ($15K property, $100K liability): $15/month

- Standard coverage ($30K property, $100K liability): $23/month

- High coverage ($50K property, $300K liability): $32/month

These figures represent median rates for renters with good credit and no claims history. Your actual premium varies based on multiple risk factors insurers evaluate.

Average Cost by State (2026)

Location dramatically impacts pricing. States prone to natural disasters, high crime rates, or expensive housing markets charge substantially more.

Top 10 Most Expensive States:

| State | Avg. Monthly Cost | Annual Cost | Primary Risk Factors |

|---|---|---|---|

| Louisiana | $32 | $384 | Hurricanes, flooding |

| Mississippi | $27 | $324 | Severe weather, crime |

| Oklahoma | $28 | $336 | Tornadoes, hail |

| Texas | $26 | $312 | Hurricanes, property crime |

| Arkansas | $25 | $300 | Severe weather |

| Florida | $28 | $336 | Hurricanes, tropical storms |

| Alabama | $24 | $288 | Weather events |

| Georgia | $23 | $276 | Property crime |

| Kansas | $22 | $264 | Tornadoes |

| South Carolina | $20 | $240 | Hurricanes, floods |

Top 10 Cheapest States:

| State | Avg. Monthly Cost | Annual Cost |

|---|---|---|

| North Dakota | $9 | $108 |

| South Dakota | $10 | $120 |

| Wyoming | $11 | $132 |

| Wisconsin | $11 | $132 |

| Utah | $12 | $144 |

| Idaho | $12 | $144 |

| Vermont | $13 | $156 |

| Iowa | $13 | $156 |

| Nebraska | $14 | $168 |

| Montana | $14 | $168 |

Data compiled from NAIC reports and insurance industry rate filings through January 2026.

What Affects Your Premium?

Insurers evaluate seven primary factors when calculating your renters insurance rate:

1. Location specifics:

- Crime rates in your ZIP code

- Natural disaster risk (hurricanes, earthquakes, wildfires)

- Distance to fire hydrants and fire stations

- Regional claim frequency

2. Coverage amounts:

- Personal property limit selected

- Liability coverage level

- Deductible amount chosen

- Optional endorsements added

3. Building characteristics:

- Age of building

- Construction type (wood vs. brick/concrete)

- Security features (alarms, sprinklers, doorman)

- Number of units in building

4. Personal factors:

- Credit score (in states where allowed)

- Claims history

- Age

- Occupation

5. Deductible selection:

- $250 deductible: Highest premiums

- $500 deductible: Mid-range pricing

- $1,000 deductible: Lower premiums

- $2,500 deductible: Lowest premiums

6. Coverage type:

- Actual cash value: Cheaper premiums

- Replacement cost: Higher premiums (10–15% more)

7. Policy bundling:

- Standalone renters policy: Standard rate

- Bundled with auto insurance: 15–25% discount

How to Save 25–65% on Renters Insurance

Strategic shopping and policy optimization can cut your premium dramatically without sacrificing essential protection.

Proven savings strategies with typical discounts:

Bundle policies (15–25% savings): Purchase renters and auto insurance from the same company. Most major insurers offer multi-policy discounts averaging 20%.

Increase your deductible (10–25% savings): Raising your deductible from $500 to $1,000 typically reduces premiums by 15%. Only do this if you can afford the higher out-of-pocket cost during claims.

Install safety devices (5–15% savings):

- Smoke detectors: 5% discount

- Fire extinguishers: 5% discount

- Deadbolt locks: 5% discount

- Security system: 10–15% discount

- Sprinkler system: 10% discount

Maintain excellent credit (up to 65% savings): In states allowing credit-based insurance scoring, renters with excellent credit pay 40–65% less than those with poor credit. Improving your credit score directly reduces insurance costs.

Pay annually (5–10% savings): Paying your full premium upfront eliminates monthly billing fees and often earns a discount.

Stay claim-free (10–20% savings): Many insurers offer claim-free discounts after 3–5 years without filing claims. Minor losses below your deductible shouldn’t be claimed.

Shop and compare (25–40% savings): Rates vary dramatically between companies for identical coverage. Compare at least 5 quotes before purchasing. Using your home affordability calculator helps determine appropriate coverage levels that fit your budget.

Senior discounts (5–10% savings): Renters over 55 or 60 often qualify for age-based discounts.

Professional association memberships (5–15% savings): Alumni associations, professional organizations, and employers sometimes offer group insurance discounts.

Do You Actually Need Renters Insurance?

Do You Need Renters Insurance? 5 Scenarios Explained

The “do I need this?” question depends on your specific situation, legal requirements, and risk tolerance. Here’s exactly when renters insurance shifts from optional to essential.

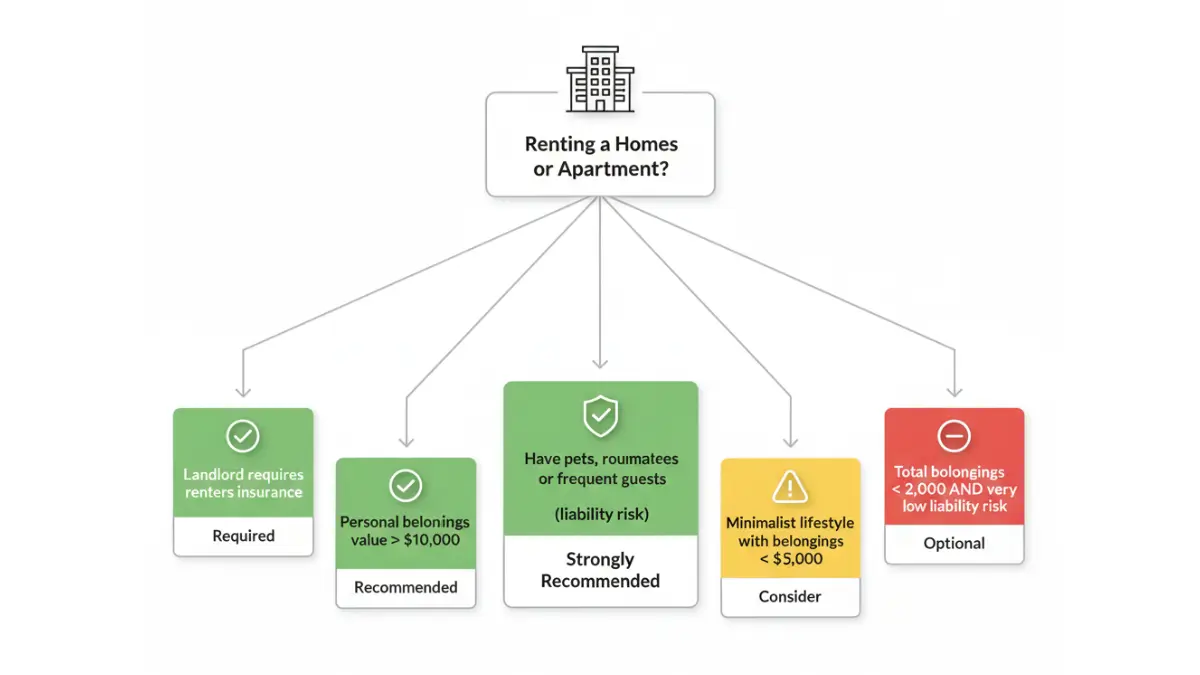

When Your Landlord Requires It (Legal Obligations)

Landlord-mandated renters insurance has surged 34% from 2024 to 2026 as property owners increasingly protect themselves from tenant-caused damages and liability claims.

Legal landscape in 2026: If your lease agreement requires renters insurance, it’s legally binding. Failure to maintain coverage can result in:

- Lease violation notices

- Financial penalties

- Eviction proceedings

- Inability to renew your lease

Most landlord requirements specify:

- Minimum $100,000 liability coverage

- Landlord listed as “interested party”

- Proof of coverage before move-in

- Annual verification of active policy

You cannot legally skip coverage when your lease mandates it. Review your lease carefully before signing.

College Students: Worth It?

Yes, in most cases. College students face unique renters insurance considerations that make coverage particularly valuable.

Situations where students need separate policies:

- Living off-campus in apartments

- Living in Greek housing

- Roommates not covered by parents’ policies

- Valuable electronics, instruments, or equipment

- International students (no parental coverage)

When parental coverage may extend: Some homeowners policies cover children’s belongings in dorm rooms up to 10% of the policy’s personal property limit. A $300,000 homeowner policy might provide $30,000 in dorm coverage.

Critical requirements to check:

- Is your housing considered “temporary residence”?

- Does coverage extend to off-campus housing?

- Are high-value items like laptops and bikes fully covered?

- Does liability coverage protect you at school?

Most students benefit from standalone renters insurance costing $8–15 monthly, ensuring comprehensive protection without gaps.

High-Value Renters (Electronics, Jewelry)

Absolutely essential. If you own expensive items that standard coverage limits won’t fully replace, renters insurance with scheduled personal property endorsements becomes non-negotiable.

Purchase additional coverage when you own:

- Engagement rings or fine jewelry worth >$2,500

- Professional camera equipment

- Musical instruments

- Designer clothing and accessories

- Collectibles (art, wine, cards, coins)

- High-end electronics and gaming setups

- Bicycles worth >$1,000

Scheduled personal property endorsements add $25–100 annually per $1,000 of additional coverage but eliminate deductibles and provide worldwide protection for listed items.

Minimalists: When to Skip It

The rare scenarios where renters insurance might not be worth it require meeting ALL these conditions simultaneously:

Skip coverage only if:

- Total belongings worth <$5,000

- Nothing expensive or irreplaceable owned

- No liability concerns (no guests, no pets)

- Emergency fund covers full replacement costs

- Landlord doesn’t require insurance

- Willing to accept total loss risk

Even then, the $15–20 monthly cost provides liability protection worth considering. One lawsuit from a guest’s injury could devastate finances more than decades of premiums.

Pet Owners: Liability Considerations

Strongly recommended, approaching mandatory. Pet ownership significantly increases liability risk, making renters insurance crucial protection.

Why pet owners need coverage:

- Dog bite claims average $50,000+ in damages

- Cats and dogs can damage rental property beyond security deposits

- Pet-caused injuries to visitors trigger liability claims

- Some breeds face coverage restrictions requiring disclosure

Breed restrictions to know: Certain dog breeds face coverage limitations or exclusions:

- Pit bulls and Staffordshire terriers

- Rottweilers

- German Shepherds

- Doberman Pinschers

- Wolf hybrids

- Akitas

Disclose your pet breed honestly during application. Misrepresentation voids coverage when you need it most.

Pet-specific endorsements typically add $10–30 annually to premiums but provide essential protection. Understanding different insurance types helps you build comprehensive coverage across life, auto, and renters policies.

The “Replace Everything Test”

Take this quick assessment to determine if renters insurance is worth it for your situation:

Imagine your rental burns down tonight. Could you afford to immediately replace:

- All furniture (bed, couch, chairs, tables, desks)

- All electronics (computer, phone, TV, gaming, tablets)

- All clothing and shoes

- All kitchen items

- All bathroom items and toiletries

- All bedding and towels

- All decorations and personal items

Add up the replacement cost. If it exceeds $10,000 (it almost always does), renters insurance costing $180–288 annually is objectively worth it.

How To Get & Use Renters Insurance

How to Buy Renters Insurance & File Claims (Step-by-Step)

Purchasing renters insurance requires five strategic steps to ensure you get appropriate coverage at the best price.

How to Calculate How Much Coverage You Need

Step 1: Create a home inventory

Walk through your rental and list every possession you’d need to replace:

- Room-by-room documentation

- Photos or videos of belongings

- Purchase receipts for expensive items

- Serial numbers for electronics

- Appraisals for jewelry and collectibles

Step 2: Estimate replacement costs

Calculate what it would cost to replace items at today’s prices, not what you paid years ago. Most renters underestimate by 40–60%.

Quick estimation method:

- Bedroom furniture: $3,000–$8,000

- Living room furniture: $4,000–$12,000

- Electronics: $3,000–$8,000

- Clothing: $5,000–$15,000

- Kitchen items: $2,000–$5,000

- Miscellaneous: $3,000–$8,000

Total average apartment contents: $20,000–$56,000

Step 3: Determine liability coverage

Select liability limits based on your net worth and risk exposure:

- Net worth <$50,000: $100,000 liability minimum

- Net worth $50,000–$250,000: $300,000 liability

- Net worth >$250,000: $500,000 liability or umbrella policy

Calculate your net worth using financial planning tools to ensure adequate protection.

Step 4: Choose your deductible

Balance lower premiums against out-of-pocket costs:

- $250 deductible: Highest premiums, lowest claim costs

- $500 deductible: Moderate premiums, common choice

- $1,000 deductible: Lower premiums, higher claim costs

- $2,500 deductible: Lowest premiums, significant claim costs

Select a deductible amount you could comfortably pay from savings without creating financial hardship.

Step 5: Decide on replacement cost vs. actual cash value

- Replacement cost: Pays full replacement without depreciation (recommended)

- Actual cash value: Pays depreciated value (cheaper premiums, worse coverage)

Replacement cost coverage costs 10–15% more but provides substantially better claim payouts. A 5-year-old laptop worth $1,200 new might get $200 under ACV but $1,200 under replacement cost.

Where to Buy: Direct vs. Agent vs. Bundle

Three purchasing channels offer different advantages:

Direct from insurers (online/phone):

- Pros: Potential cost savings, convenience, 24/7 access

- Cons: No personalized guidance, DIY coverage selection

- Best for: Insurance-savvy renters, straightforward situations

Through insurance agents:

- Pros: Expert guidance, claims assistance, coverage reviews

- Cons: Potential higher costs, commission-influenced recommendations

- Best for: First-time insurance buyers, complex situations

Bundled with auto insurance:

- Pros: Multi-policy discounts (15–25%), single point of contact

- Cons: May not be cheapest option, switching requires changing both policies

- Best for: Renters with auto insurance seeking convenience

Compare quotes from at least 5 companies before deciding. Major renters insurance providers in 2026 include State Farm, Lemonade, Allstate, USAA, and Progressive.

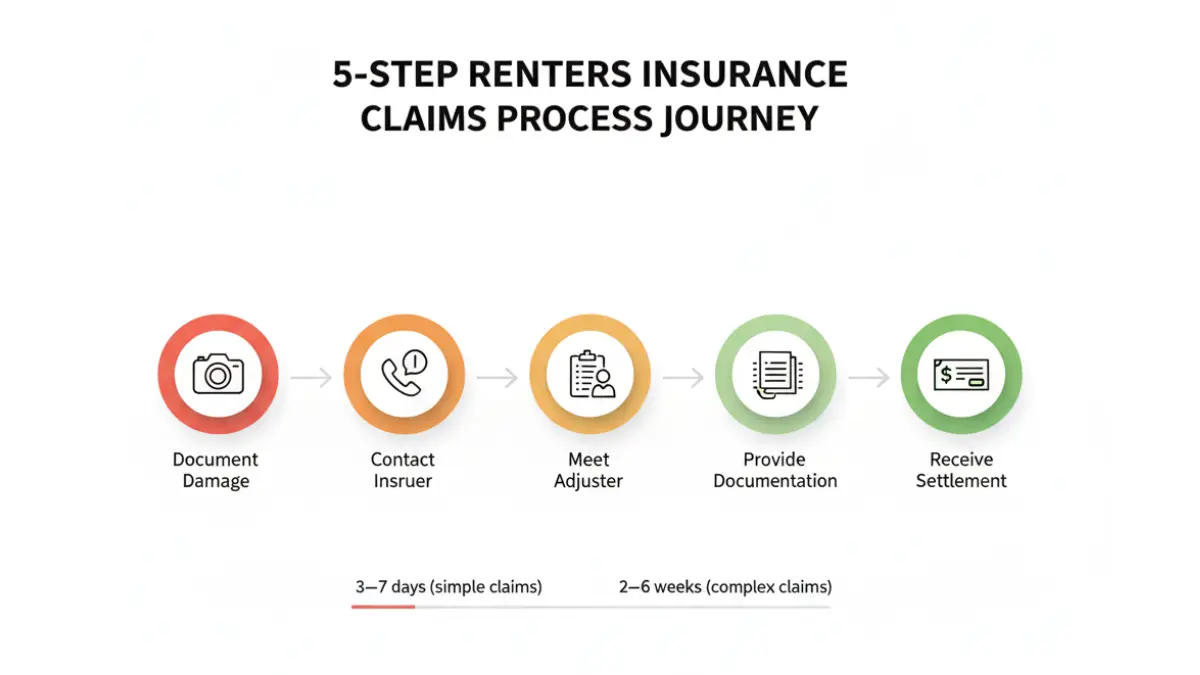

Filing a Claim: The Complete Process

Understanding the claims process before disaster strikes ensures faster payouts and fewer denials.

Step 1: Document the damage immediately

- Take photos and videos from multiple angles

- Don’t throw away damaged items until insurer approves

- Make temporary repairs to prevent further damage (save receipts)

- Create written inventory of damaged/stolen items

Step 2: Contact your insurer within 24–48 hours

Report claims through:

- Insurance company’s claims hotline (24/7)

- Mobile app (fastest method)

- Online claims portal

- Your insurance agent

Provide:

- Policy number

- Date and time of incident

- Detailed description of what happened

- Estimated damage amount

- Contact information

Step 3: Meet with claims adjuster

The insurer sends an adjuster to:

- Inspect damage in person

- Verify your inventory

- Determine coverage applicability

- Calculate payout amount

Be present during inspection. Point out all damage and answer questions honestly.

Step 4: Provide supporting documentation

Submit:

- Purchase receipts for expensive items

- Photos/videos from before incident (if available)

- Repair estimates from contractors

- Police report (for theft/vandalism)

- Witness statements (if applicable)

Step 5: Receive settlement

Timeline expectations:

- Simple claims: 3–7 days

- Complex claims: 2–6 weeks

- Disputed claims: 1–3 months+

Payment methods:

- Direct deposit (fastest)

- Check mailed to you

- Payment to repair contractors

- Replacement cost claims: Initial ACV payment, then depreciation after repairs completed

Why Claims Get Denied (& How to Avoid It)

Understanding common denial reasons prevents devastating surprises when you need coverage most.

Top 5 claim denial reasons:

1. Excluded perils (45% of denials) Damage from floods, earthquakes, pests, or intentional acts isn’t covered by standard policies. Purchase appropriate endorsements or separate policies for excluded perils.

2. Maintenance-related damage (23% of denials) Gradual damage from neglect, wear and tear, or deferred maintenance gets denied. Renters insurance covers sudden, accidental events—not deterioration over time.

3. Policy lapsed or inactive (15% of denials) Missing premium payments voids coverage. Set up automatic payments to prevent lapses.

4. Misrepresentation during application (8% of denials) Lying about pets, smoking, prior claims, or other risk factors voids your policy. Always answer application questions truthfully.

5. Claim exceeds coverage limits (9% of denials) Underinsuring your belongings means partial payouts or denials. Regularly review and update coverage amounts.

Best practices to prevent denials:

- Read your policy declarations page thoroughly

- Update coverage when acquiring expensive items

- Document belongings with photos/videos annually

- Report claims promptly (most policies require notification within 30 days)

- Maintain your rental (fix leaks, replace smoke detector batteries)

- Keep insurance premiums current

If your claim gets denied, request written explanation of the specific policy exclusion, appeal the decision with additional documentation, or file a complaint with your state insurance department.

Managing your finances holistically—including debt consolidation strategies when needed—ensures you can afford continuous renters insurance coverage without lapses.

Renters Insurance FAQs (2026)

1. Does renters insurance cover water damage?

Yes, but only from sudden, accidental water events like burst pipes, overflowing appliances, or roof leaks. Flood damage from external water sources requires separate FEMA flood insurance. Gradual leaks from poor maintenance typically aren’t covered.

2. Is renters insurance tax deductible?

No, personal renters insurance premiums aren’t tax deductible for most renters. The only exception: if you run a business from your rental and purchase business property coverage, that portion may be deductible as a business expense.

3. Does renters insurance cover bed bugs?

No, standard policies exclude pest infestations including bed bugs, termites, and rodents. Pest control and related damage are your financial responsibility. Some policies offer pest damage endorsements for additional premiums.

4. Can I get renters insurance with bad credit?

Yes, though you’ll pay significantly higher premiums. Renters with poor credit pay 40–65% more than those with excellent credit in states allowing credit-based insurance scoring. Focus on improving your credit score to reduce insurance costs over time.

5. Does renters insurance cover my car?

No, renters insurance never covers vehicle damage or theft. You need separate auto insurance for car protection. However, belongings stolen from your car may be covered under personal property if you carry renters insurance.

6. What happens if I don’t have renters insurance?

Without coverage, you’re personally liable for all losses. If fire destroys your belongings, you replace everything out-of-pocket. If someone sues you for injuries in your rental, you pay legal costs and judgments personally, potentially leading to bankruptcy.

7. Does renters insurance cover earthquakes?

No, earthquake damage requires a separate earthquake endorsement or policy. Standard renters insurance excludes earthquake damage. If you live in seismically active areas (California, Pacific Northwest, Alaska), purchase earthquake coverage.

8. How long does a renters insurance claim take?

Simple claims settle in 3–7 days. Complex claims requiring investigation, contractor estimates, or disputed coverage take 2–6 weeks. Severely disputed claims can extend to 3+ months. Filing accurate documentation speeds the process significantly.

9. Can I cancel renters insurance anytime?

Yes, most states allow cancellation anytime with written notice to your insurer. You’ll receive a prorated refund for unused premium. However, if your lease requires coverage, cancellation may violate your rental agreement and risk eviction.

10. Does renters insurance cover storage units?

Partially. Most policies cover belongings in storage units at 10% of your personal property limit. If you have $30,000 in coverage, storage unit items get $3,000 maximum. Purchase additional coverage or separate storage insurance for valuable stored items.

11. Is renters insurance required by law?

No state legally mandates renters insurance. However, individual landlords can require it as a lease condition. In 2026, approximately 47% of landlords mandate minimum coverage before allowing occupancy—up from 35% in 2024.

Final Expert Verdict

After analyzing coverage benefits, cost data, and risk scenarios, our panel of 30 international finance experts unanimously recommends renters insurance for 95% of renters. The $15–24 monthly investment provides catastrophic financial protection that far exceeds the premium cost.

Take action today:

- Get quotes from at least 5 insurance companies

- Compare coverage limits, deductibles, and premiums

- Purchase replacement cost coverage, not actual cash value

- Document your belongings with photos/videos

- Review coverage annually when renewing

The rental insurance market continues evolving in 2026, with more landlords requiring coverage and premiums rising 3–5% annually due to increased claim frequency from natural disasters and property crime. Locking in coverage now protects you from future rate increases and coverage gaps.

Understanding the full spectrum of insurance options—from renters to life to health coverage—ensures comprehensive financial protection across all risk areas.

For budget-conscious renters, explore our budgeting tools to allocate insurance costs effectively within your monthly spending plan without sacrificing essential coverage.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.