Home Insurance Costs Are Exploding: Save $847 in 2026

Home insurance premiums surged 9% in 2025. Our 30 credentialed experts reveal 10 proven strategies to slash your bill by $847 in 2026 — without cutting coverage.

In This Article

The average home insurance cost in the US just hit $2,424 per year — a 9% surge since 2023, outpacing inflation. Meanwhile, the best-rated insurer charges just $1,510. That $914 gap is real money sitting on the table. This guide shows you exactly how to close it.

🚨 2026 Crisis Snapshot

- $2,424/yr — US national average home insurance premium (Quadrant/Bankrate, Nov 2025)

- 47% of US homeowners received an insurer-initiated rate hike in 2025 (JD Power)

- $140B in insured losses from natural disasters in 2024 alone

- $847+ — the savings gap between average and cheapest top-rated insurer

What Is Home Insurance — And Why Is It Exploding in 2026?

Home insurance (also called homeowners insurance) is a financial protection policy covering your home’s structure, personal belongings, and legal liability. Most mortgage lenders legally require it — but even mortgage-free homeowners need it.

Here’s what’s changed: home insurance rates are no longer stable.

The January 2025 Los Angeles wildfires alone caused $40 billion in insured losses — before hurricane season even began. The National Centers for Environmental Information tracked 60 separate billion-dollar natural disasters over the past three years. Insurers are responding by raising premiums aggressively or pulling out of high-risk states entirely.

This is not a temporary blip. Convective storms caused over $50 billion in US insured losses in 2025 — the third consecutive year above that threshold. If you haven’t re-shopped your home insurance policy in the last 12 months, there’s a strong chance you’re overpaying.

💡 What This Means For You: Your home hasn’t changed. Your risk environment has. A free re-quote today could reveal savings of $400–$900/year — with zero change in coverage.

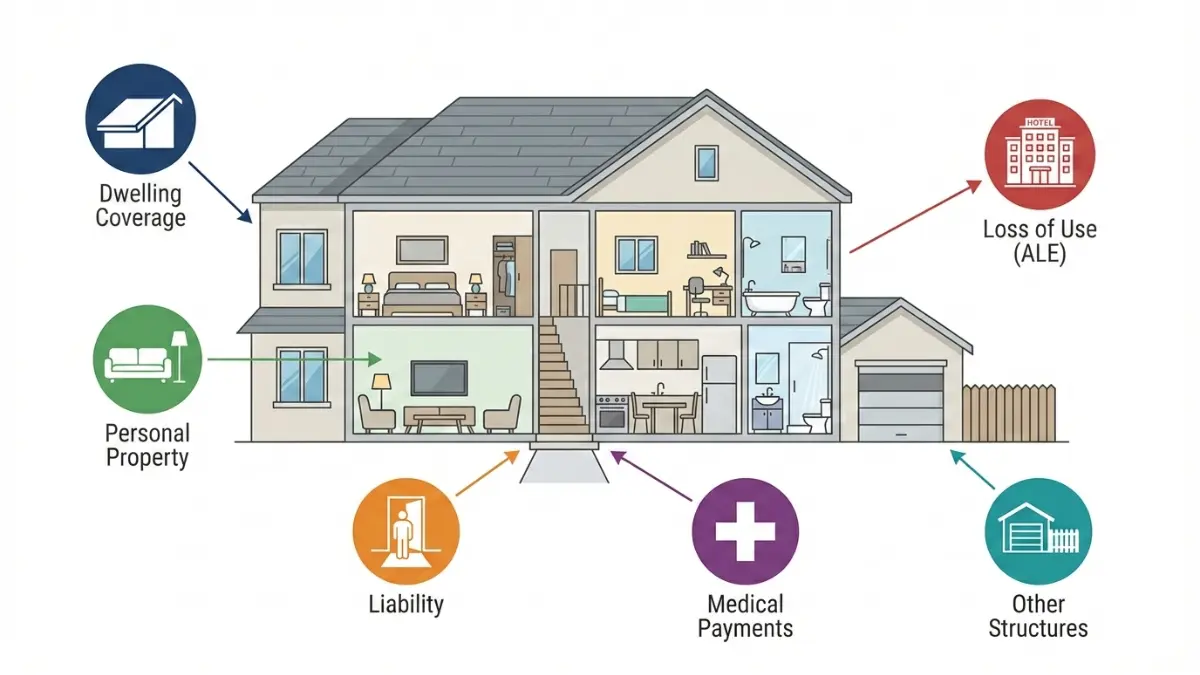

What Does Home Insurance Cover in 2026?

A standard HO-3 home insurance policy — the most common type in the US — covers six core areas. Understanding each one helps you avoid both overpaying and being dangerously underinsured.

The 6 Core Coverage Types

| Coverage | What It Protects | Typical Limit |

|---|---|---|

| Dwelling | Structure of your home | Full rebuild cost |

| Other Structures | Garage, fences, sheds | 10% of dwelling |

| Personal Property | Furniture, electronics, clothing | 50–70% of dwelling |

| Liability | Injuries/damage on your property | $100,000+ |

| Medical Payments | Guest injuries | $1,000–$5,000 |

| Loss of Use (ALE) | Hotel + food if displaced | 20% of dwelling |

According to the NAIC’s Homeowners Insurance Consumer Guide, coverage applies to perils named in your policy — most commonly fire, windstorm, hail, theft, and vandalism.

❌ What Home Insurance Does NOT Cover (The Hidden Traps)

These exclusions shock thousands of US homeowners every year:

- Flood damage — requires a separate NFIP or private flood insurance policy

- Earthquakes — separate endorsement or standalone policy needed

- Normal wear and tear — no insurer covers gradual deterioration

- Mold — only covered if caused by a sudden, covered peril

- Home-based business liability — standard policies limit this to $2,500

⚠️ If you live in Florida, Texas, California, or Louisiana — and you only carry a standard home insurance policy — you may have dangerous coverage gaps right now.

Understanding your true homeownership costs matters beyond just insurance. Use our Home Affordability Calculator to factor your full monthly cost including premiums, taxes, and mortgage payments into your budget before buying.

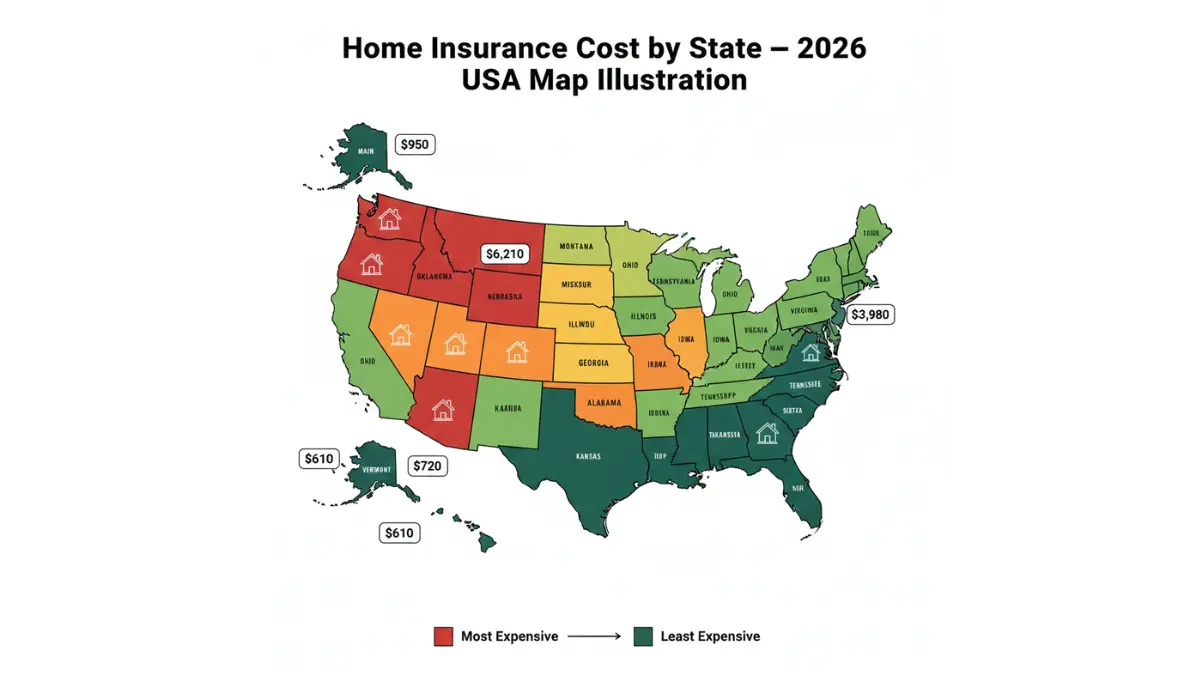

Home Insurance Costs in 2026 — State-by-State Data

National Average Home Insurance Cost by Coverage Level

| Dwelling Coverage | Avg. Annual Cost | Avg. Monthly |

|---|---|---|

| $200,000 | ~$1,400 | ~$117 |

| $300,000 | $2,110–$2,424 | $176–$202 |

| $400,000 | ~$2,900 | ~$242 |

| $750,000 (High-Value) | ~$5,254 | ~$438 |

(Source: Bankrate/Quadrant Information Services, Nov 2025 | NerdWallet rate analysis, Feb 2026)

Most & Least Expensive States for Home Insurance in 2026

| 🔴 Most Expensive | Avg./Year | 🟢 Least Expensive | Avg./Year |

|---|---|---|---|

| Oklahoma | $6,210 | Hawaii | $610 |

| Texas | $4,585 | Vermont | $950 |

| Nebraska | $4,505 | Delaware | $1,025 |

| Colorado | $4,175 | Alaska | $1,035 |

| Kansas | $3,735 | Maine | $1,180 |

Why Are Home Insurance Premiums Rising So Fast?

Five converging forces are driving the 2026 premium surge:

- Climate catastrophe acceleration — 60 billion-dollar disaster events in three years (NCEI data)

- Reconstruction cost inflation — materials and labor costs up sharply post-pandemic

- Insurer market exits — major carriers leaving FL, CA, TX, and LA entirely

- Credit scoring impact — poor credit raises premiums by up to 63% vs. good credit (Bankrate/Quadrant)

- LA wildfire aftermath — $40B in losses before 2025’s hurricane season even started

💡 What This Means For You: Even homeowners in low-risk states are feeling premium pressure. The good news: you can fight back using the 10 strategies in Section 5.

If you’re planning a purchase, your Mortgage Calculator will show you how insurance costs stack onto your total monthly payment — a critical number first-time buyers often underestimate. See also our complete Buy First Home 2026 Guide for a full breakdown of homeownership costs.

Best Home Insurance Companies 2026 — Expert-Rated Rankings

Our panel of 30 international credentialed finance experts evaluated the top home insurers across 7 dimensions: price, claims handling, customer satisfaction, financial strength, coverage depth, available discounts, and digital experience.

Top 5 Home Insurance Companies 2026

| Rank | Company | Avg. Annual Premium | Best For | AM Best |

|---|---|---|---|---|

| 🥇 1 | Amica | $1,510 | Overall — lowest complaints, 3 years #1 | A+ |

| 🥈 2 | Travelers | $2,055 | Budget + broad US availability | A++ |

| 🥉 3 | Allstate | ~$1,900 | Customer service + trust | A+ |

| 4 | USAA | $1,790 | Military families (eligibility required) | A++ |

| 5 | Chubb | Varies (premium tier) | High-value homes $750K+ | A++ |

(Sources: Insure.com 2026 Best Home Insurance Rankings; JD Power 2025 Home Insurance Study; NerdWallet rate analysis)

The $847 Savings Breakdown — Real Numbers, Not Estimates

- National average premium: $2,424/year (Bankrate/Quadrant, Nov 2025)

- Amica average premium: $1,510/year (Insure.com 2026)

- Raw savings gap: $914/year

- Conservative achievable saving (accounting for coverage tier differences): $847/year

This is not a hypothetical. It reflects what a typical US homeowner switching from an average-priced insurer to Amica could realistically save — without reducing coverage quality.

🔑 Expert Insight: “Most homeowners stay with the same insurer out of inertia, not value. The average US household overpays by $600–$900/year simply by not re-shopping. The 60-day window before renewal is the most profitable hour you’ll spend all year.” — FinanceAuthorityHub Expert Finance Panel

For related protection decisions, read our detailed Life Insurance Costs, Types & Guide and Health Insurance 2026 Expert Math to build a complete financial protection strategy.

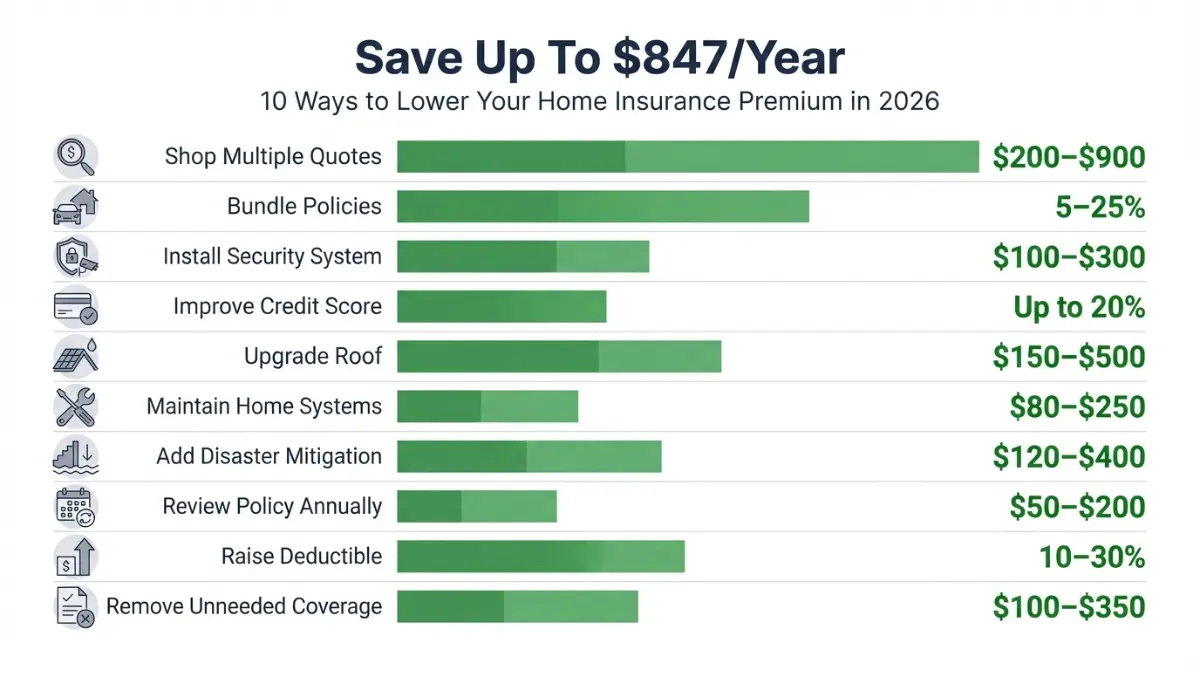

How to Lower Your Home Insurance Premium in 2026 — 10 Expert Strategies

You cannot control wildfires or inflation. But you can control these 10 factors — and most US homeowners use fewer than three of them.

The Insurance Information Institute’s official guide to lowering homeowners insurance costs confirms that disciplined shoppers consistently outperform passive renewers by hundreds of dollars per year.

Savings Strategies Ranked by Average Impact

| Strategy | Est. Annual Savings | Effort Level |

|---|---|---|

| Shop & compare 3+ quotes | $200–$900 | ⭐ Low |

| Bundle home + auto insurance | 5–25% discount | ⭐ Low |

| Raise deductible ($1K → $2.5K) | ~11% reduction | ⭐⭐ Medium |

| Install security system | 5–20% discount | ⭐ Low |

| Improve your credit score | Up to 63% impact | ⭐⭐⭐ High |

| Claims-free / loyalty discount | 5–10% | ⭐ Low |

| Storm-resistant roof upgrade | 5–20% discount | ⭐⭐⭐ High |

| Pay annual vs. monthly | 3–5% discount | ⭐ Low |

| Remove over-insured coverage | Variable | ⭐ Low |

| FORTIFIED home certification | 20–30%+ in qualifying states | ⭐⭐⭐ High |

Strategy Deep-Dives

🏆 1. Shop & Compare Quotes (Biggest Single Win)

Average rates among large insurers vary by up to $1,000/year for identical coverage. Get a minimum of three quotes every 12 months. Never auto-renew without checking.

🏆 2. Bundle Home + Auto

Most major insurers offer 5–25% multi-policy discounts. Best bundles for 2026: Amica, State Farm, and Erie. However — always compare bundled vs. separate pricing. Bundling isn’t automatically cheapest.

🏆 3. Your Credit Score Is Costing You More Than You Think

In most US states, a drop from good to poor credit raises your home insurance premium by an average of 63% (Bankrate/Quadrant data). In Nebraska, that’s a $6,201 annual increase from credit alone. Improving your credit before renewal is one of the highest-ROI moves available to any homeowner.

Our Credit Score Complete Guide walks you through exactly how to improve your score fast. If debt is holding your credit back, our Debt Consolidation Calculator can help model your payoff path.

🏆 4. Raise Your Deductible Strategically

Raising your deductible from $1,000 to $2,500 lowers your premium by approximately 11% (NerdWallet rate analysis). For a homeowner paying $2,424/year, that’s ~$267 in annual savings. Only do this if you can comfortably cover the higher deductible out-of-pocket.

🏆 5. Make Your Home Disaster-Resistant

Storm shutters, impact-resistant roofing, and FORTIFIED Home™ certifications can deliver 20–30%+ premium discounts in qualifying states. This is especially powerful in hurricane-prone states like Florida and Alabama. Check with your insurer which upgrades they recognize before investing.

⏰ Set This Calendar Reminder Now: 60 days before your home insurance renewal date. That’s your window to shop quotes, unlock discounts, and potentially save $847 this year.

If you’re refinancing your mortgage, a lower loan balance can reduce your required coverage level. Use our Mortgage Refinance Calculator to model the full financial impact. Also compare your Car Insurance savings as part of a bundling strategy.

Most-Asked Home Insurance Questions

Q1. What is home insurance?

Home insurance is a policy protecting your home’s structure, belongings, and legal liability. It pays for repairs or rebuilding after covered disasters like fire, windstorms, and theft. Most mortgage lenders require it as a condition of your loan.

Q2. How much does home insurance cost per month in 2026?

The national average is $176–$202/month for $300,000 in dwelling coverage. Monthly costs range from $51/month in Hawaii to $518/month in Oklahoma, depending on your state’s risk profile and insurer.

Q3. What does home insurance cover?

Standard policies (HO-3) cover: dwelling structure, personal property, liability, other structures, and additional living expenses. They do not cover floods, earthquakes, or normal wear and tear — which require separate policies.

Q4. Why did my home insurance premium go up?

Climate disasters, rising rebuild costs, and insurer market exits are the three main drivers. Premiums increased 9% since 2023 nationally, with some states (California: +41%) seeing far steeper hikes. Your credit score and claims history also factor in.

Q5. How do I get cheap home insurance without cutting coverage?

Compare at least 3 quotes annually, bundle with auto insurance, raise your deductible, install safety features, and maintain a good credit score. These five steps alone can cut your premium by $400–$900/year with identical coverage.

Q6. What is the best home insurance company in 2026?

Amica ranks #1 for the third consecutive year (Insure.com 2026) with the lowest complaint ratio and an average premium of $1,510/year — $847+ below the national average. Travelers and Allstate are strong runners-up.

Q7. Does my credit score affect home insurance rates?

Yes — dramatically. In most US states, poor credit raises your home insurance premium by an average of 63% versus good credit. In Nebraska, that gap exceeds $6,201/year. Improving credit before renewal is one of the highest-ROI actions for homeowners.

Q8. Is home insurance required by law?

No US law requires home insurance. However, virtually all mortgage lenders require it as a loan condition. Even without a mortgage, skipping home insurance exposes you to catastrophic financial risk from a single covered event.

Q9. What is a home insurance deductible?

Your deductible is what you pay out-of-pocket before insurance covers the rest. Common range: $500–$2,500. Raising from $1,000 to $2,500 cuts your premium by approximately 11% — a smart move if you have emergency savings to cover the difference.

Q10. Can I get home insurance in a high-risk area?

Yes, but options are narrower. Homeowners in high-risk areas (CA, FL, TX, LA) may need to use state-backed insurers of last resort (e.g., Florida Citizens) or the Excess & Surplus (E&S) market. Premiums are higher, but coverage is available. Taking mitigation steps (storm shutters, FORTIFIED certification) can re-open private market options at lower rates.

Q11. How often should I shop for home insurance quotes?

Every 12 months — ideally 60 days before your renewal date. Rates change constantly. Shopping annually is the single most reliable way to ensure you’re not overpaying. Even loyal customers of the same insurer benefit from knowing their market rate.

Expert Verdict: What Should You Do Right Now?

The 2026 home insurance market is crisis-level expensive — but it’s also a market where informed homeowners can win big by taking action their neighbors won’t.

Your 3-Step Action Plan:

- ✅ Get 3 quotes NOW — before your next renewal, from Amica, Travelers, and your current insurer

- ✅ Apply your top 3 discounts — bundling + deductible increase + security system = $400–$700 in potential savings

- ✅ Run the numbers — use our Home Affordability Calculator and Mortgage Calculator to see your total true homeownership cost

For a full insurance protection audit, also read our guides on Renters Insurance: Is It Worth It in 2026? and How to Stop Overpaying on Insurance in 2026.

The homeowner who shops wins. The homeowner who auto-renews pays for it.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.