Tractor Trailer Insurance: Real Costs & Savings (2026)

Tractor trailer insurance costs $900–$2,500/mo for own-authority operators in 2026. Get real cost tables, FMCSA requirements, coverage types & 7 savings strategies.

In This Article

Quick Answer: Tractor trailer insurance is a bundled package of commercial trucking coverages — not a single policy. In 2026, own-authority owner-operators pay $900–$2,500+/month, while leased operators pay $250–$500/month. Costs are rising faster than ever due to a 52% surge in nuclear verdicts and tightening underwriting standards.

What Is Tractor Trailer Insurance — And Why It Costs More in 2026

Tractor trailer insurance is the mandatory coverage package that protects owner-operators, motor carriers, and small fleets from the financial risks of operating a commercial semi-truck. It is not a single policy — it is a bundle of coverages tailored to how you operate, what you haul, and whether you run under your own authority or lease onto a carrier.

Every for-hire tractor trailer traveling on U.S. public roads is legally required to carry insurance under FMCSA regulations (49 CFR Part 387). Failure to maintain active filings can result in immediate authority revocation.

Why 2026 is different from any prior year:

- Nuclear verdicts — jury awards exceeding $10 million — surged 52% in 2024, directly driving up liability premiums across every trucking class

- Cargo theft remains an active pricing lever, especially on high-value freight lanes through Texas, Florida, and Georgia

- Telematics-based underwriting is now the industry standard; carriers without ELD data face higher premiums or fewer quote options

- The FMCSA is rolling out its new Motus filing system in 2026, replacing the legacy Licensing & Insurance portal — new operators must be aware of this transition

Whether you are an independent owner-operator budgeting for your first truck or a small fleet owner trying to control costs, understanding tractor trailer insurance is one of the most important financial decisions in trucking. For a broader look at how commercial vehicle costs fit into your total operating expenses, explore our commercial truck insurance cost breakdown.

How Much Does Tractor Trailer Insurance Cost in 2026?

This is the question every trucker has — and the one every competitor answers poorly. Here are the real 2026 numbers, broken down by operator type, state, and coverage scenario.

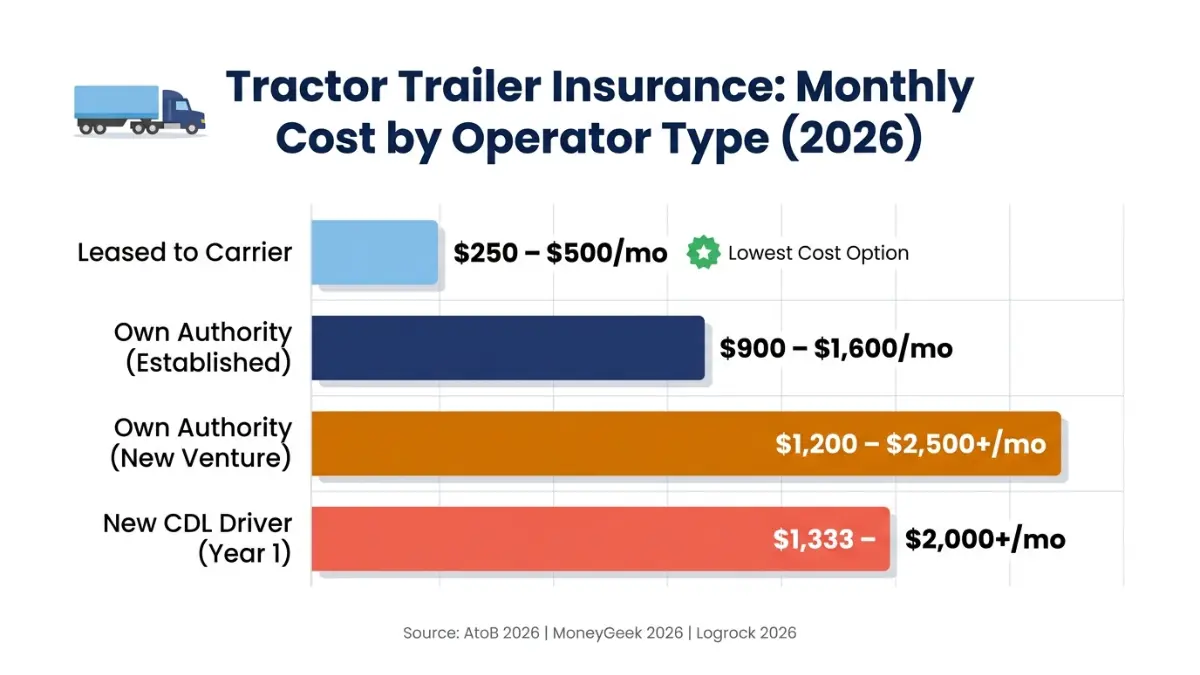

2026 Cost by Operator Type

| Operator Type | Monthly Cost | Annual Cost |

|---|---|---|

| Own Authority — Established (3+ years) | $900 – $1,600 | $10,800 – $19,200 |

| Own Authority — New Venture (Year 1) | $1,200 – $2,500+ | $14,400 – $30,000+ |

| Leased to Motor Carrier | $250 – $500 | $3,000 – $6,000 |

| New CDL Driver (First Year, Own Authority) | $1,333 – $2,000+ | $16,000 – $24,000+ |

Sources: AtoB 2026 owner-operator cost statistics; MoneyGeek 2026 commercial truck insurance analysis; Logrock 2026 benchmarks.

Key insight: New authority operators typically pay 40–100% more than established carriers. After 3 years of clean operation, rates drop significantly — making your first three years the most critical for cost management.

2026 Cost by State — Cheapest vs. Most Expensive

Geographic location can swing your premium by over $400/month for identical coverage.

| State | Monthly Premium (Est.) | Notes |

|---|---|---|

| Vermont | $284 | Consistently cheapest |

| Maine | $275 | Low claim frequency |

| Pennsylvania | $293 | Among lowest for state minimum |

| Michigan | $382 | Above average |

| Florida | $281–$320+ | High accident frequency |

| New York | $666 | Highest litigation environment |

| Texas / Georgia | Above average | High-claim corridors |

What this means for you: An owner-operator moving their garaging ZIP from New York to Vermont saves approximately $391/month — or $4,692/year — on identical coverage. State selection is an underutilized savings lever.

What Is Driving Costs Higher in 2026?

Three systemic forces are pushing tractor trailer insurance premiums upward:

- Nuclear verdict litigation pressure — large carriers and owner-operators alike are priced for catastrophic loss scenarios, especially in high-lawsuit states like Florida and California

- Cargo theft surge — commodity type, parking practices, and operating lanes directly affect your premium; unsecured overnight parking in metro areas is a major red flag for underwriters

- Telematics requirements — carriers that cannot demonstrate safe driving data through ELD or dashcam integration are viewed as higher-risk accounts

To model how insurance costs fit into your monthly cash flow alongside truck payments and operating expenses, use our Business Loan Calculator to stress-test your numbers before committing to a policy.

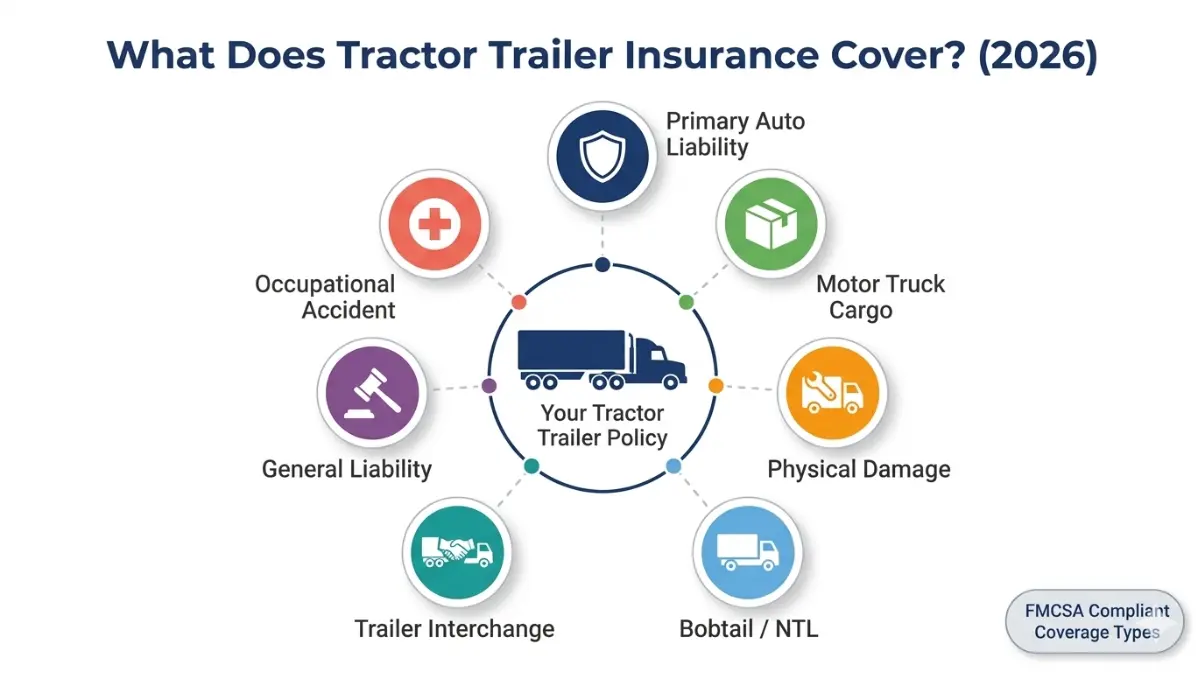

What Does Tractor Trailer Insurance Cover?

Most truckers are confused about what they actually need — because competitors present coverage types without connecting them to real operator scenarios. Here is every coverage explained, with who needs it and why.

Core Coverages — Required for Most Operations

Primary Auto Liability Covers bodily injury and property damage you cause to third parties. The FMCSA minimum is $750,000 for non-hazardous property carriers, but most freight brokers and shippers require $1,000,000. Always quote to $1M — not the federal floor.

Motor Truck Cargo Insurance Covers freight you are hauling against loss, damage, or theft. Limits are driven by commodity type and contract requirements. High-theft cargo (electronics, pharmaceuticals, alcohol) faces exclusions on many policies — confirm your exclusion language before signing.

Physical Damage Coverage Covers your tractor for collision, theft, fire, and weather damage. Required by lenders on financed trucks. Choose a deductible you can actually pay on short notice — a $5,000 deductible that leaves you unable to make your truck payment is not a savings strategy.

Additional Coverages — Situational

| Coverage | What It Does | Who Needs It |

|---|---|---|

| Bobtail / Non-Trucking Liability (NTL) | Covers you when off-dispatch, not hauling | Leased owner-operators |

| Trailer Interchange | Physical damage for non-owned trailers under written agreement | Operators pulling others’ trailers |

| Motor Truck General Liability | Covers incidents not involving road crashes (dock accidents, yard damage) | Operators with shipper contracts requiring it |

| Occupational Accident | Work-injury protection replacing workers’ comp for owner-operators | 1-truck operations |

| Rental Reimbursement / Downtime | Offsets lost income during repairs after a covered claim | Anyone whose cash flow depends on daily miles |

⚠️ The Coverage Gap Warning (Exclusive — Not in Any Top Competitor)

The most dangerous moment in trucking is the transition between dispatch and off-dispatch. Bobtail and non-trucking liability policies vary widely by carrier. Some cover you only when the trailer is detached; others cover personal use regardless of trailer status. Always confirm your policy’s exact definition of “off-dispatch” before signing — gaps here have destroyed owner-operators financially.

Quick decision tool — what do you actually need?

- Leased to a carrier? → Minimum: Physical damage + bobtail/NTL

- Own authority, for-hire? → Required: Primary liability ($1M) + motor truck cargo + physical damage + FMCSA BMC-91 filing

- Small fleet (2–5 trucks)? → Add: General liability + umbrella policy + occupational accident per driver

For context on how tractor trailer insurance compares to other commercial auto products, see our truck insurance 2026 rates guide.

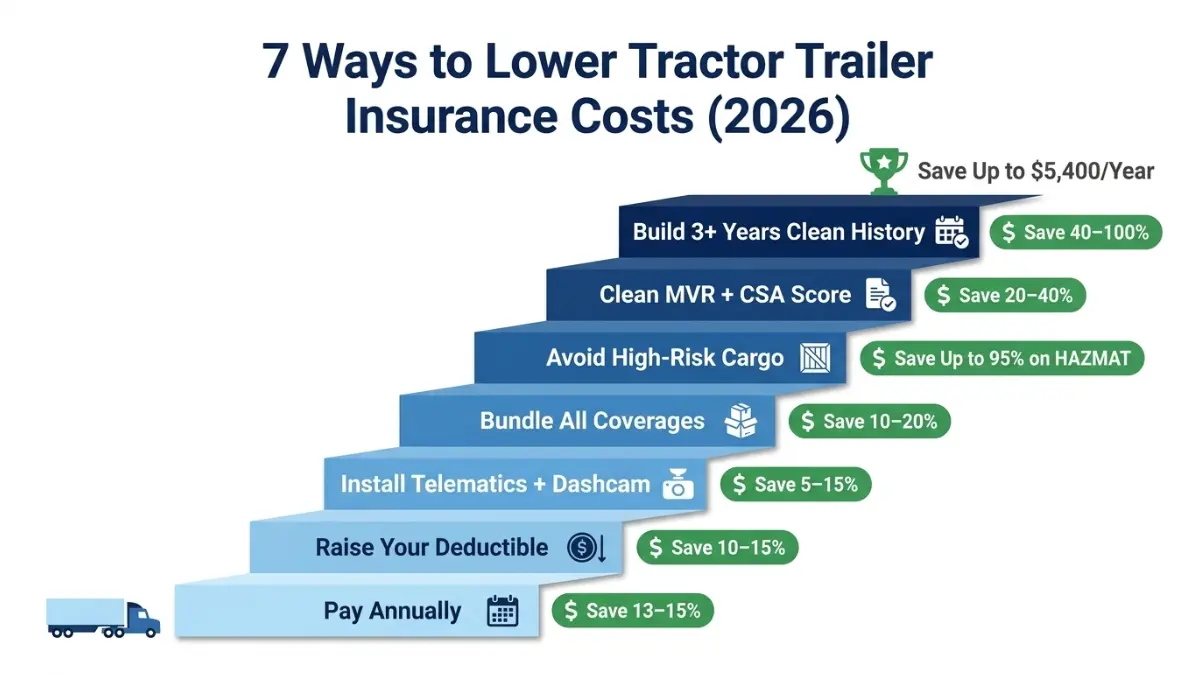

7 Proven Ways to Lower Your Tractor Trailer Insurance Premium

This is the section no competitor gives you. Not a generic “shop around” tip — a ranked, dollar-specific savings playbook built from 2026 underwriting data.

1. Install Telematics + Dashcams

Carriers that share ELD data with their insurer save 5–15% on premiums. Progressive’s SmartHaul program alone saves enrolled operators an average of $1,106/year. Dashcam footage also eliminates fraudulent claims — one saved claim can offset years of premium savings.

2. Maintain a Clean MVR and CSA Score

A spotless Motor Vehicle Record and strong CSA (Compliance, Safety, Accountability) score saves 20–40% versus drivers with violations. Speeding tickets, following-too-close violations, and at-fault accidents are the three fastest ways to destroy your rate.

3. Pay Annually — Not Monthly

Paying your annual premium upfront saves 13–15%. A $12,000 annual policy paid monthly costs approximately $13,800 with financing charges. Paying upfront saves you roughly $1,800/year for zero additional risk.

4. Raise Your Deductible Strategically

Increasing your physical damage deductible from $1,000 to $2,500 cuts that coverage cost by 10–15%. Only do this if you have cash reserves to cover the deductible immediately after a loss — otherwise it becomes a trap.

5. Bundle All Coverages With One Carrier

Placing liability, cargo, and physical damage with a single insurer saves 10–20% versus buying each separately. Ask about a Commercial Package Policy (CPP) that combines everything on one bill.

6. Build 3+ Years of Claims-Free History

This is the single biggest long-term lever. New ventures pay 40–100% more than established carriers. A clean record held for 36 months is worth thousands per year in premium reduction at renewal. Protect it aggressively — file only claims that exceed your financial break-even point.

7. Avoid High-Risk Cargo When Your Routes Allow

HAZMAT endorsements add 95–107% to your premium. Reefer loads and high-theft commodities (electronics, pharma) attract exclusions and higher rates. When you have freight choice, general dry-van cargo is consistently the cheapest to insure.

What this means for you: A trucker currently paying $1,500/month who installs telematics, raises deductibles, pays annually, and bundles coverage could realistically reduce costs to $1,050–$1,150/month — saving $4,200–$5,400/year.

Planning your trucking business finances? Our ROI Calculator can help you model the real return on safety investments like telematics and driver training programs.

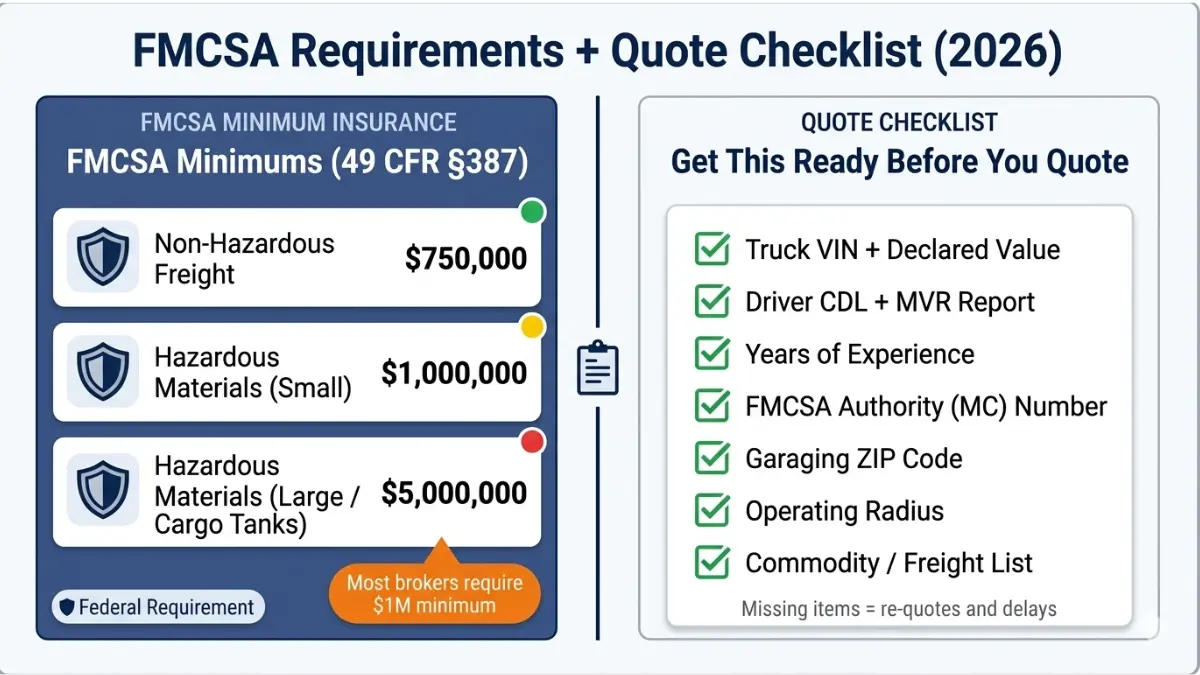

FMCSA Requirements + How to Get the Right Quote

Federal Minimum Insurance Requirements (2026)

The FMCSA sets the legal floor for tractor trailer insurance under 49 CFR Part 387. Here is what you are required to carry:

| Operation Type | FMCSA Minimum Liability |

|---|---|

| Non-hazardous freight (interstate) | $750,000 |

| Hazardous materials (small quantities) | $1,000,000 |

| Hazardous materials (large quantities / cargo tanks 3,500+ gallons) | $5,000,000 |

| Oil (non-hazardous, less than 3,500 gallons) | $1,000,000 |

Critical 2026 note: Most freight brokers and shippers require $1,000,000 in liability as a condition of tendering loads — regardless of what FMCSA requires. Quote to $1M from day one. Quoting to the $750K minimum will not get you dispatched.

FMCSA Filing — How It Works

- Interstate for-hire carriers file proof of insurance using Form BMC-91 or BMC-91X

- Your insurer files directly with FMCSA — you do not file yourself

- Filing timeline: 24–48 hours after binding, assuming clean paperwork

- Most common delay: Entity name or address mismatch between your authority application and your insurance policy. Confirm these match exactly before submitting.

- 2026 Update: FMCSA is migrating all filings to the new Motus system, replacing the legacy Licensing & Insurance portal. New operators registering in 2026 should verify filing procedures directly at the FMCSA Insurance Filing Requirements page.

Quote Checklist — Have This Ready Before You Call

Gather these before contacting any insurer or broker. Missing items cause re-quotes, delays, and higher pricing:

- ✅ Truck VIN, year, make, model, declared value

- ✅ Driver CDL number and MVR report (Motor Vehicle Record)

- ✅ Years of CDL experience and claims history

- ✅ FMCSA authority number (MC number) if applicable

- ✅ Garaging ZIP code (not your home address — where the truck sleeps)

- ✅ Operating radius: local / regional / long-haul

- ✅ Commodity list (exact freight types you haul)

- ✅ Prior insurance carrier and history (any lapses will be flagged)

Pro tip: Get quotes from at least 3 carriers. Rates for identical coverage vary 30–50% between insurers. Use a one-page spec sheet — same limits, deductibles, and cargo — so every quote is directly comparable.

If you are launching a new trucking business and managing startup costs, our Savings Calculator can help you plan your insurance reserve fund for the first 12 months of operation.

Frequently Asked Questions — Tractor Trailer Insurance (2026)

1. How much is tractor trailer insurance per month?

Own-authority operators pay $900–$2,500+/month; leased operators pay $250–$500/month. New ventures and first-year CDL drivers pay at the higher end of the own-authority range until they build clean operating history.

2. What is the minimum insurance required for a tractor trailer?

FMCSA requires a minimum of $750,000 in liability for non-hazardous interstate freight. However, most freight brokers require $1,000,000 — plan for this number from day one or risk being unable to book loads.

3. Is tractor trailer insurance the same as commercial truck insurance?

Tractor trailer insurance is a subset of commercial truck insurance. It specifically covers Class 8 semi-trucks (18-wheelers) and includes specialized coverages — such as motor truck cargo, trailer interchange, and FMCSA filings — not found in standard commercial auto policies. See our full commercial truck insurance guide for a detailed comparison.

4. What does tractor trailer insurance cover?

Core coverage includes primary auto liability, motor truck cargo, and physical damage. Additional coverages include bobtail/NTL, trailer interchange, general liability, occupational accident, and downtime reimbursement — depending on your operation type and contract requirements.

5. How much does new authority tractor trailer insurance cost?

New ventures typically pay $1,200–$2,500+/month in year one. Insurers view new authorities as high-risk due to no operating history. Rates drop significantly after 3 consecutive years of clean operation and claims-free history.

6. What is bobtail insurance?

Bobtail insurance covers your tractor when you are driving without a trailer and not under dispatch. It is often required by motor carriers for leased owner-operators to fill the liability gap between dispatch periods. Do not confuse it with non-trucking liability — the covered-use definitions differ by policy.

7. Does the motor carrier provide insurance for leased owner-operators?

Yes — partially. Motor carriers typically provide primary liability while you are under dispatch. You remain responsible for physical damage, bobtail/NTL coverage, and sometimes occupational accident insurance depending on your lease agreement. Always read your lease before assuming coverage.

8. What is trailer interchange coverage?

Trailer interchange covers physical damage to a non-owned trailer in your possession under a written interchange agreement. It is not the same as non-owned trailer physical damage — the written agreement is a required trigger. Virginia does not permit trailer interchange coverage.

9. Does my garaging state affect tractor trailer insurance costs?

Yes — dramatically. Rates can vary by over 240% between the cheapest and most expensive states. Vermont ($284/month) versus New York ($666/month) is the starkest example. Your garaging ZIP — not just your state — affects pricing based on local theft frequency, litigation trends, and claim severity.

10. What is a nuclear verdict and how does it affect my trucking insurance?

A nuclear verdict is a jury award exceeding $10 million. These surged 52% in 2024, according to AtoB’s 2026 trucking insurance cost statistics. Every operator — regardless of size or safety record — pays higher premiums because underwriters price for catastrophic loss scenarios driven by this litigation environment.

11. How do I get cheaper tractor trailer insurance without cutting coverage?

The fastest legitimate savings come from telematics installation (5–15%), paying annually (13–15%), bundling coverages (10–20%), and maintaining a clean MVR (20–40%). Combining all four strategies can realistically reduce annual premiums by $4,000–$6,000 without reducing your protection.

Expert Panel Review

This article was reviewed by Michael R. Thompson, CFA, Senior Finance & Risk Analyst at FinanceAuthorityHub.com, with expertise in commercial insurance cost analysis, risk-adjusted financial planning, and trucking industry economics.

📌 Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, or insurance advice. Tractor trailer insurance costs, coverage requirements, and FMCSA regulations vary by state, carrier, and individual circumstances. Premium estimates are market averages and your actual quote may differ. Always consult a licensed commercial insurance professional for guidance specific to your operation.

Related reading: Automobile Insurance Rates 2026 | Liability Insurance Guide | Workers’ Compensation 2026 | Gap Insurance Explained

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.