What Is a Home Loan? Complete Guide for U.S. Borrowers (2026)

Not sure how home loans work in 2026? Get today’s rates (6.22%), compare FHA, VA, USDA & conventional loans, and follow our 7-step approval guide.

In This Article

What Is a Home Loan?

A home loan — also called a mortgage loan — is a secured loan used to purchase residential real estate. The property itself serves as collateral. You repay the lender in monthly installments over a fixed term, typically 10 to 30 years.

If you stop making payments, the lender has the legal right to foreclose and reclaim the home.

🏠 Live Rate Alert (March 19, 2026): The average 30-year fixed-rate home loan stands at 6.22%, down nearly half a point from a year ago, according to Freddie Mac’s Primary Mortgage Market Survey. This is the best affordability window buyers have seen since early 2024.

Understanding how a home loan works before you apply can save you tens of thousands of dollars over the life of your mortgage. Use our Mortgage Calculator right now to see your estimated monthly payment at today’s rates.

How Does a Home Loan Work?

When you take out a mortgage loan, the lender pays the seller directly on your behalf. You then repay the lender over your agreed loan term — with interest.

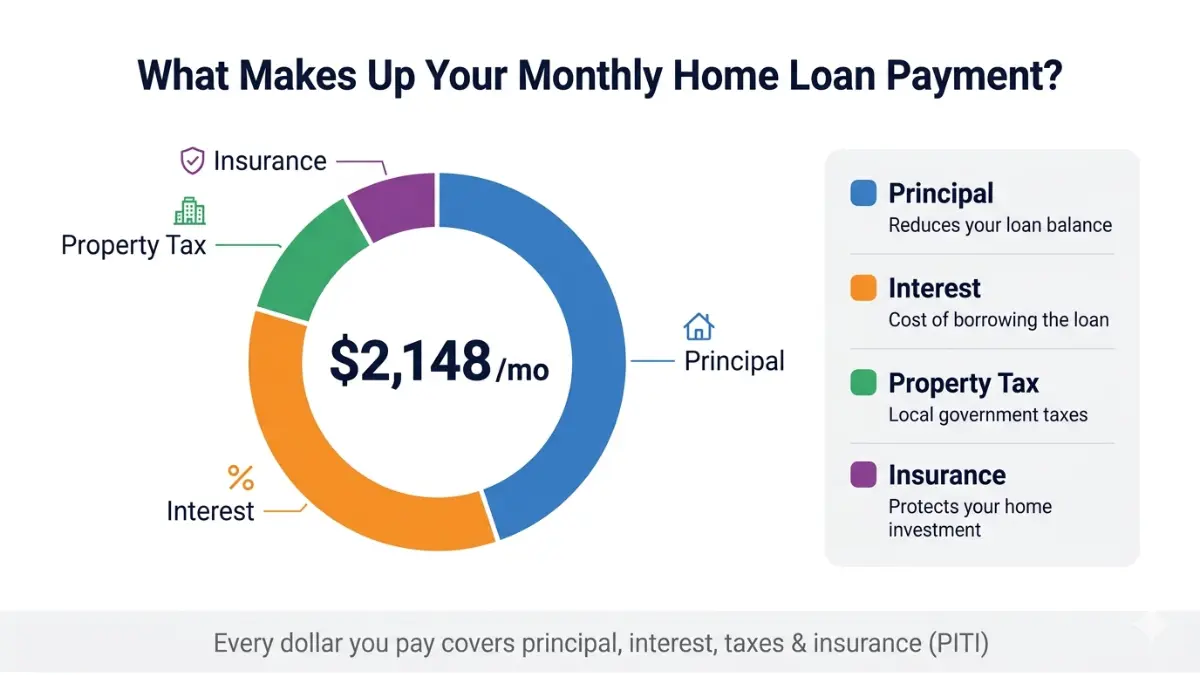

What’s Inside Your Monthly Mortgage Payment?

Every monthly payment you make covers four components — often called PITI:

- Principal — Reduces your outstanding loan balance

- Interest — The lender’s fee for providing the home loan

- Taxes — Property taxes collected in escrow by your lender

- Insurance — Homeowners insurance and, if applicable, PMI

Real Example: On a $350,000 home loan at 6.22% over 30 years, your monthly principal + interest payment is approximately $2,148. Add property taxes and insurance and your total payment typically runs $2,600–$2,900/month.

What Is Amortization?

Amortization is how your home loan gets paid off over time. Early payments go mostly toward interest. Later payments shift heavily toward principal.

| Payment Period | % Toward Interest | % Toward Principal |

|---|---|---|

| Year 1 | ~83% | ~17% |

| Year 10 | ~69% | ~31% |

| Year 25 | ~33% | ~67% |

| Final Payment | ~1% | ~99% |

What This Means For You: Making even one extra mortgage payment per year can cut 4–6 years off your home loan and save $30,000+ in total interest. Use our Amortization Calculator to model your exact savings.

What Is a Rate Lock?

A rate lock guarantees your home loan interest rate for 30–60 days while your purchase closes. In a rising rate environment like early 2026, locking your rate immediately after preapproval protects you from sudden spikes.

Already a homeowner? See whether refinancing makes sense with our Mortgage Refinance Calculator.

Types of Home Loans — Which One Is Right for You?

Not all home loans are equal. The right mortgage loan for you depends on your credit score, military status, location, and how much you’ve saved for a down payment.

Here’s the definitive 2026 comparison that Bankrate and NerdWallet both fail to include — real rate data by loan type:

2026 Home Loan Types — Master Comparison Table

| Loan Type | Min. Credit Score | Min. Down Payment | PMI Required? | 2026 Avg. Rate | Best For |

|---|---|---|---|---|---|

| Conventional | 620 | 3% | Yes (if <20% down) | 6.22–6.43% | Strong credit buyers |

| FHA Loan | 580 (3.5% down) / 500 (10% down) | 3.5% | Yes (MIP, full term) | ~5.96% | First-time buyers, lower credit |

| VA Loan | No minimum (620 typical) | 0% | No | ~5.84% | Military / Veterans |

| USDA Loan | 640 recommended | 0% | Annual fee (0.35%) | ~5.95% | Rural/suburban buyers |

| Jumbo Loan | 700+ | 10–20% | Varies | ~6.32% | High-value homes $832,750+ |

| ARM (5/1) | 620 | 3–5% | Yes (if <20%) | Lower initial, then adjusts | Short-term homeowners |

Conventional Home Loan

The most common mortgage loan in America. Requires a minimum 620 credit score and as little as 3% down. Borrowers with 740+ credit scores access the best rates. Private mortgage insurance (PMI) cancels automatically at 20% equity.

FHA Home Loan

Backed by the Federal Housing Administration (HUD), FHA loans are the go-to option for first-time home buyers and those with credit challenges. The 2026 FHA floor limit is $541,287; the ceiling is $1,249,125 in high-cost areas.

VA Home Loan

Exclusively for eligible U.S. military members, veterans, and surviving spouses. VA home loans require no down payment and no PMI — making them the most powerful home loan benefit available to any borrower group. Nearly 90% of VA-backed loans are made with zero down.

USDA Home Loan

Backed by the U.S. Department of Agriculture for rural and eligible suburban areas. Zero down payment required. Income limits apply. Check official USDA eligibility maps before assuming you qualify.

Jumbo Home Loan

Any mortgage loan exceeding $832,750 in 2026 (the FHFA conforming limit) is classified as a jumbo. These require stronger credit and larger down payments but allow you to finance luxury or high-cost-area properties.

Adjustable-Rate Mortgage (ARM)

An ARM starts with a lower home loan interest rate for an initial fixed period (commonly 5 or 7 years), then adjusts annually. Best for buyers who plan to sell or refinance within the fixed period.

What This Means For You: If your credit score is below 620, an FHA loan is almost certainly your best first-time home loan option. If you’re a veteran, a VA loan will save you more money than any other loan type — period. Not sure how much home you can afford? Our Home Affordability Calculator runs the math instantly.

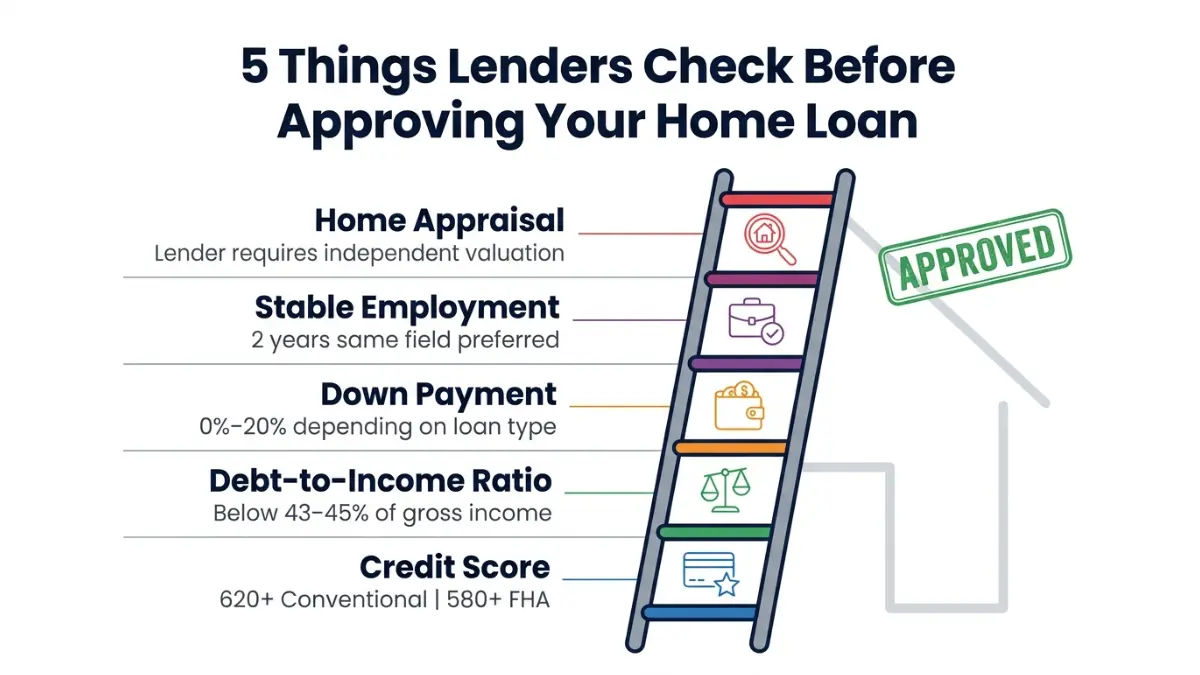

Home Loan Requirements — Do You Qualify in 2026?

Qualifying for a home loan in 2026 isn’t about being perfect. It’s about meeting specific benchmarks. Here’s exactly what every mortgage lender evaluates.

1. Credit Score

Your credit score is the single most powerful factor in your home loan rate.

| Credit Score | Loan Type Available | Rate Impact |

|---|---|---|

| 760+ | Conventional, all types | Best available rates |

| 700–759 | Conventional, all types | Competitive rates |

| 660–699 | Conventional, FHA | Slightly higher rates |

| 620–659 | Conventional (minimum), FHA | Higher rates apply |

| 580–619 | FHA only (3.5% down) | Limited options |

| 500–579 | FHA only (10% down) | Very limited options |

| Below 500 | No standard home loan | Must rebuild credit first |

Key Insight: Improving your credit score by just 40 points before applying can cut your home loan interest rate by 0.5% — saving over $35,000 on a $350,000 loan over 30 years.

Check and monitor your credit score with our free Credit Score Calculator.

2. Debt-to-Income Ratio (DTI)

DTI = your total monthly debt payments ÷ gross monthly income.

Most lenders cap DTI at 43–45% for conventional home loans. FHA loans allow up to 57% with strong compensating factors.

- Example: $3,200/month gross income. Monthly debts = $1,200 (car + student loan + credit cards). DTI = 37.5% ✅ — qualifies for most home loans.

Calculate yours instantly with our Debt-to-Income Ratio Calculator. If your DTI is too high, explore whether consolidating debt makes sense at Debt Consolidation Guide.

3. Down Payment

| Loan Type | Minimum Down Payment | Notes |

|---|---|---|

| VA / USDA | 0% | Zero down — no PMI |

| Conventional | 3% | PMI required until 20% equity |

| FHA | 3.5% (score 580+) | MIP required for full loan term |

| Jumbo | 10–20% | Lender dependent |

Important: Down payment is separate from closing costs, which add another 2–5% of the loan amount. On a $400,000 home with 5% down, budget $8,000–$20,000 in closing costs on top of your $20,000 down payment. Use our Down Payment Calculator and Closing Cost Calculator side by side to plan accurately.

First-time buyer? Read our comprehensive Down Payment Help Guide (2026) for assistance programs available in all 50 states.

4. Stable Income and Employment

Lenders want to see 2 consecutive years of stable income in the same field.

- W-2 employees: Provide 2 years of tax returns, 30 days of pay stubs, and 2 months of bank statements.

- Self-employed borrowers: 2 years of business and personal tax returns required. Lenders use your net income after deductions — which often results in a lower qualifying amount.

- Gig/freelance workers: 2026 FHA guidelines now allow more holistic income verification for non-traditional earners.

5. Property Appraisal

Every home loan requires a professional appraisal. The lender will not approve a mortgage loan for more than the home’s appraised value. If the appraisal comes in low, you’ll need to renegotiate the price, increase your down payment, or walk away.

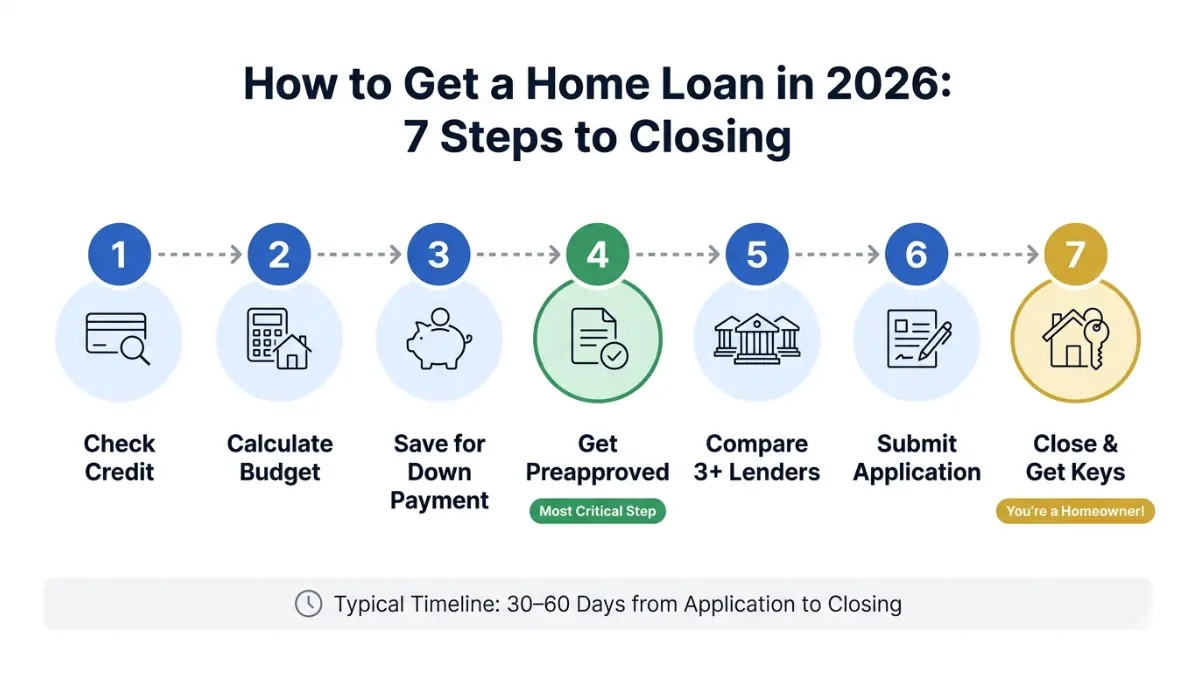

How to Get a Home Loan — 7 Steps for 2026

The home loan process takes 30–60 days on average. Follow these seven steps in order for the fastest, smoothest path to closing.

Step 1: Check Your Credit Score

Pull your free report at AnnualCreditReport.com (the only federally authorized site). Dispute any errors immediately — even one incorrect late payment can cost you a better rate.

Step 2: Calculate How Much Home You Can Afford

Use the 28/36 rule: your monthly housing costs should not exceed 28% of gross income, and total debts should not exceed 36%. Our Home Affordability Calculator factors in your income, debts, and current rates to give you a precise number.

Step 3: Save for Down Payment and Closing Costs

Target at minimum: down payment (3–3.5%) + closing costs (2–5%). First-time buyers in most states can access down payment assistance programs that cover part or all of the down payment requirement.

Step 4: Get Mortgage Preapproval

Do this before house hunting. Preapproved buyers close 30% faster than non-preapproved buyers, according to the Mortgage Bankers Association. Preapproval requires income verification, credit check, and employment documentation. Read our full Mortgage Pre-Approval 2026 Guide to prepare everything in advance.

Step 5: Compare at Least 3 Lenders

Never accept the first offer. Rates and fees vary significantly between banks, credit unions, and online lenders. Shopping three or more lenders saves the average borrower $1,500+ over the life of the home loan. Use our APR Calculator to compare true costs — not just interest rates.

Step 6: Submit Your Full Mortgage Application

Once you’ve chosen a lender and made an offer, underwriting begins. Respond to any document requests within 24–48 hours. Delays in documentation are the #1 cause of delayed closings.

Step 7: Close on Your Home Loan

You’ll receive a Closing Disclosure at least 3 business days before closing. Review it carefully. At closing, you’ll sign all loan documents, pay your closing costs, and receive your keys.

Home Loan Timeline Overview

| Step | Typical Duration |

|---|---|

| Credit check + preapproval | 1–3 days |

| House hunting | 2–8 weeks |

| Full application + underwriting | 2–4 weeks |

| Appraisal | 1–2 weeks (often overlaps) |

| Closing | 1 day |

| Total | 30–60 days |

What This Means For You: The buyers who close fastest and get the best rates are the ones who prepare before they shop. Get preapproved, lock your rate, and move quickly in today’s competitive market. Also see our 15 vs. 30-Year Mortgage Comparison (2026) to decide which term saves you more.

Home Loan Interest Rates — What to Expect in 2026

Home loan rates in 2026 are meaningfully better than 2025. Here’s the current picture, updated weekly from primary sources.

Current 2026 Home Loan Rates (Week of March 19, 2026)

| Loan Type | Average Rate | Source |

|---|---|---|

| 30-Year Fixed Conventional | 6.22% | Freddie Mac |

| 15-Year Fixed Conventional | 5.54% | Freddie Mac |

| 30-Year FHA | ~5.96% | Fortune/Optimal Blue |

| 30-Year VA | ~5.84% | Fortune/Optimal Blue |

| 30-Year USDA | ~5.95% | Fortune/Optimal Blue |

| 30-Year Jumbo | ~6.32% | Fortune/Optimal Blue |

Rate Forecast (2026): Fannie Mae’s Economic and Strategic Research Group projects the 30-year fixed home loan rate will average 6.1% through 2026. The Mortgage Bankers Association agrees. The National Association of Home Builders is slightly more optimistic, projecting 5.99%.

A sustained drop below 6% is not expected before late 2026 at the earliest.

What Affects Your Personal Home Loan Rate?

Your individual mortgage loan rate depends on five factors:

- Credit score — The single biggest driver. A 760+ score gets you the best pricing.

- Down payment size — Higher down = lower rate in most cases

- Loan type — VA and FHA often price lower than conventional for equivalent borrowers

- Loan term — 15-year rates run ~0.65–0.70% lower than 30-year rates

- Lender competition — Shopping multiple lenders can shave 0.25–0.50% off your rate

Pro Tip: Understand the difference between your interest rate and your APR before you sign. Our APR vs. Interest Rate Guide explains why the APR is what actually matters for comparing home loan offers.

FAQs — Home Loan Questions Answered

1. What is the difference between a home loan and a mortgage?

They are the same thing. In the United States, “home loan” and “mortgage” are used interchangeably. Both describe a secured loan used to purchase real property, where the home serves as collateral.

2. What credit score do I need for a home loan?

Minimum 620 for conventional loans, 580 for FHA loans with 3.5% down. A score of 740 or higher unlocks the best available home loan interest rates and can save tens of thousands over 30 years.

3. How much down payment is required for a home loan?

As little as 0% (VA and USDA loans), 3% (conventional), or 3.5% (FHA). Putting down 20% eliminates private mortgage insurance entirely. Don’t forget to budget separately for closing costs (2–5% of the loan amount).

4. What are current home loan rates in 2026?

As of March 19, 2026: the 30-year fixed home loan rate averages 6.22% (Freddie Mac). FHA loans average ~5.96%; VA loans ~5.84%. Rates are projected to hover in the low-6% range throughout 2026. See our Lowest Mortgage Rates by State (2026) for state-by-state breakdowns.

5. How long does it take to get a home loan approved?

Typically 30–60 days from full application to closing. Getting mortgage preapproval before you make an offer significantly shortens the timeline and strengthens your negotiating position.

6. What is the difference between a fixed-rate and adjustable-rate home loan?

A fixed-rate mortgage keeps your interest rate the same for the entire loan term — predictable and stable. An ARM starts lower but adjusts periodically after an initial fixed period (e.g., 5 years on a 5/1 ARM). ARMs make sense only if you plan to sell or refinance before the adjustment period begins.

7. What is PMI and when do I need it?

Private mortgage insurance (PMI) is required on conventional home loans when your down payment is below 20%. It typically costs 0.5–1.5% of the original loan amount annually. On a $350,000 loan, that’s $145–$435/month. PMI automatically cancels when your equity reaches 20%.

8. Can I get a home loan with bad credit?

Yes. FHA loans accept credit scores as low as 500 with a 10% down payment. Scores between 580–619 qualify for 3.5% down FHA loans. No conventional mortgage loan is available below 620. Focus on rebuilding your credit score before applying if possible — even a 50-point improvement opens significantly better options.

9. What documents do I need to apply for a home loan?

– Last 2 years of W-2s or tax returns

– 30 days of recent pay stubs

– 2–3 months of bank statements

– Government-issued photo ID

– Proof of additional assets (retirement accounts, investment accounts)

– Self-employed: 2 years of business returns + profit/loss statement

10. What is mortgage preapproval and why does it matter?

Mortgage preapproval is a lender’s conditional commitment to fund a specific loan amount, based on verified income, credit, and employment. In competitive markets, most sellers will not seriously consider offers without a preapproval letter attached. Preapproved buyers close 30% faster on average. See our full Mortgage Pre-Approval 2026 Guide.

11. Can I pay off my home loan early?

Yes. Most home loans allow early payoff with no penalty. Making extra principal payments reduces your total interest significantly. Check whether your specific loan has a prepayment penalty clause before making lump-sum payments. Our Mortgage Calculator lets you model the exact impact of extra payments.

📌 Disclaimer: This article is for educational and informational purposes only. It does not constitute financial, legal, or mortgage advice. Home loan eligibility, rates, and requirements vary by lender, credit profile, loan type, and market conditions. Consult a licensed mortgage professional or certified financial advisor before making any borrowing decisions. Rates cited are national averages as of March 19, 2026, and are subject to change daily.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.