Types of Home Loans: Which Mortgage Is Right for You? (2026 Guide)

Not sure which mortgage fits your budget? Compare every type of home loan in 2026 — FHA, VA, USDA, conventional & more — with real costs and a decision guide.

In This Article

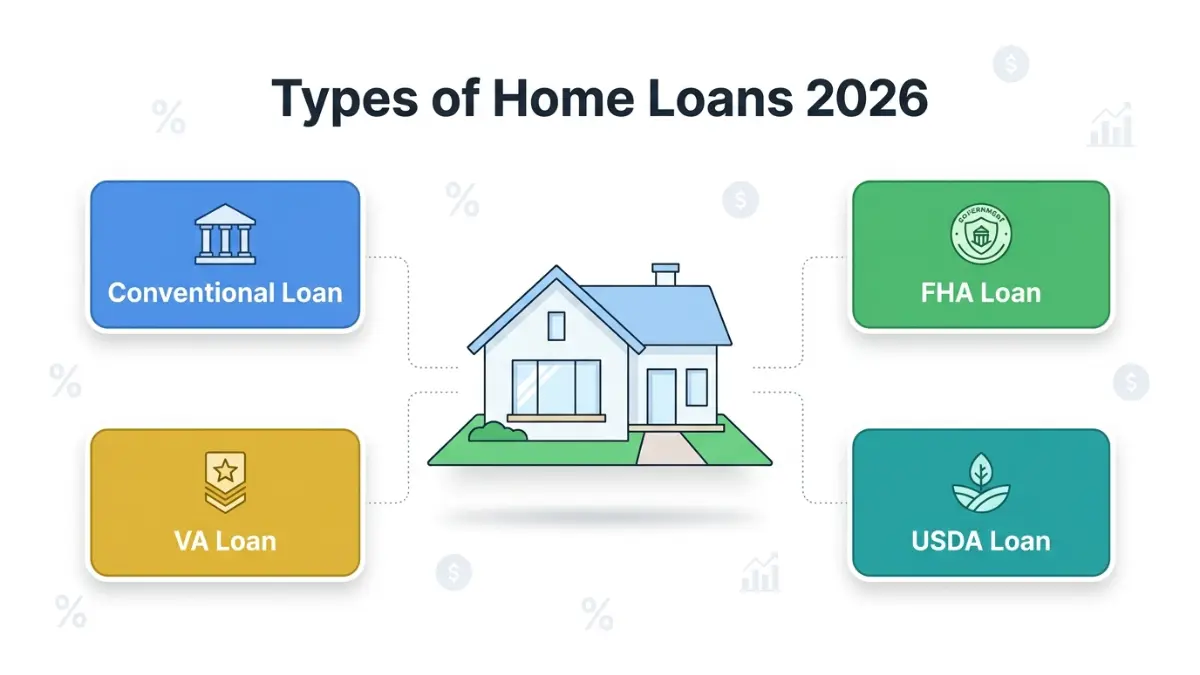

There are 4 main types of home loans — conventional, FHA, VA, and USDA — each built for different buyers, credit scores, and budgets. Choosing the wrong mortgage type in 2026 can cost you tens of thousands of dollars over the life of your loan. This guide breaks down every type of home loan, compares real costs on a $400,000 purchase, and gives you a decision matrix to find your best fit in under 5 minutes.

The 4 Core Types of Home Loans (2026)

Understanding the types of home loans starts with knowing what separates government-backed loans from conventional ones. As the Consumer Financial Protection Bureau (CFPB) notes, each loan type is designed for a different situation — and choosing the right one can mean the difference between owning a home now or waiting years.

Here are the four major mortgage types every American homebuyer should know.

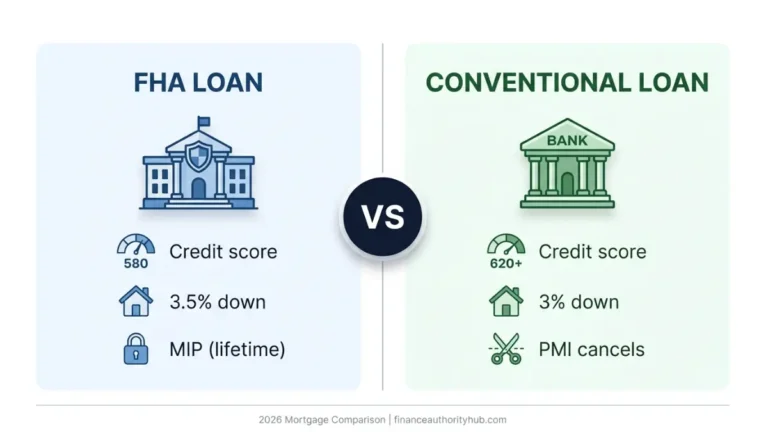

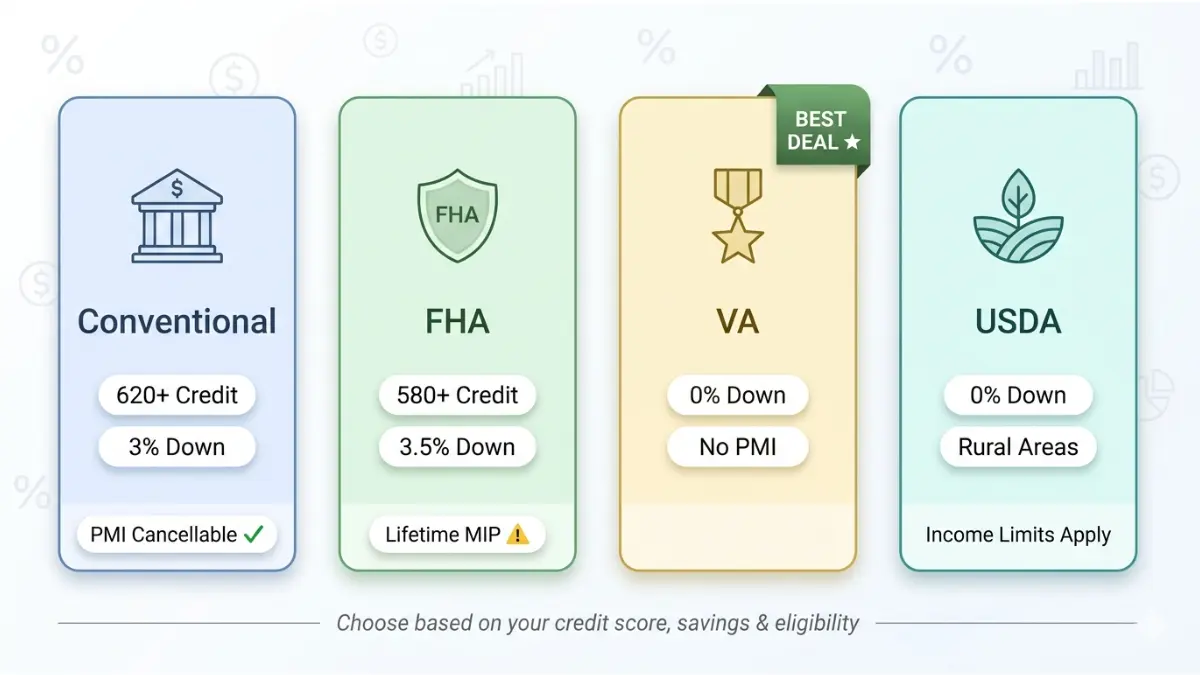

Conventional Loans

A conventional mortgage is any home loan not insured or guaranteed by a federal agency. It’s the most popular mortgage type in the U.S., accounting for over 70% of all originations.

Key facts for 2026:

- Minimum credit score: 620

- Minimum down payment: 3% (first-time buyers via Conventional 97)

- 2026 conforming loan limit: $806,500 (most areas); up to $1,209,750 in high-cost markets

- Private Mortgage Insurance (PMI) required if down payment is under 20%

- PMI can be canceled once you reach 20% equity — unlike FHA

Best for: Buyers with good credit (620+) and at least 3–5% down.

💡 What This Means For You: If your credit score is 680 or above and you have a few thousand saved, a conventional loan will likely give you the lowest long-term cost. Use our Mortgage Calculator to estimate your monthly payment instantly.

FHA Loans

FHA loans are backed by the Federal Housing Administration (HUD) and were created specifically to help lower-income and first-time buyers enter homeownership.

Key facts for 2026:

- Minimum credit score: 580 (3.5% down) or 500 (10% down)

- Minimum down payment: 3.5%

- Mortgage Insurance Premium (MIP): Paid at closing + monthly — for the life of the loan in most cases

- Loan limit: Follows conforming limits by county

Best for: First-time buyers, buyers with credit scores between 580–619, or limited savings.

💡 What This Means For You: FHA loans are easier to qualify for but cost more long-term due to MIP that never cancels. If you can get your score above 620, compare both options carefully before committing.

VA Loans

VA loans are backed by the U.S. Department of Veterans Affairs and remain one of the most powerful home loan benefits ever created for American military families.

Key facts for 2026:

- $0 down payment required

- No PMI — ever

- No minimum credit score set by the VA (most lenders require 620)

- VA funding fee: 2.15% (first use, no down payment) — can be financed into the loan

- VA guarantees up to 25% of loans up to $806,500 with no down payment

Best for: Active-duty military, veterans, and eligible surviving spouses.

💡 What This Means For You: On a $400,000 home, a VA loan saves you $20,000 in down payment plus ~$200/month in PMI vs. a 5%-down conventional loan. Over 5 years, that’s over $32,000 in savings.

USDA Loans

USDA loans are offered through the U.S. Department of Agriculture for buyers in eligible rural and suburban areas. Like VA loans, they require zero down payment.

Key facts for 2026:

- $0 down payment

- Household income must be ≤115% of local median income

- Minimum credit score: 640 (most lenders)

- Lower mortgage insurance than FHA

- Property must be in a USDA-eligible area

Best for: Low-to-moderate income buyers purchasing in rural or outer-suburban areas.

💡 What This Means For You: If you qualify by location and income, USDA loans beat FHA on monthly cost and beat conventional on the down payment. Always check USDA eligibility before defaulting to FHA.

Quick Comparison Table: 4 Core Mortgage Types (2026)

| Loan Type | Min. Credit Score | Min. Down Payment | Mortgage Insurance | Who Qualifies |

|---|---|---|---|---|

| Conventional | 620 | 3% | PMI (cancellable) | Most buyers |

| FHA | 500–580 | 3.5%–10% | MIP (lifetime) | Low credit / first-time |

| VA | None (620 typical) | 0% | None | Military / veterans |

| USDA | 640 | 0% | Low annual fee | Rural / low income |

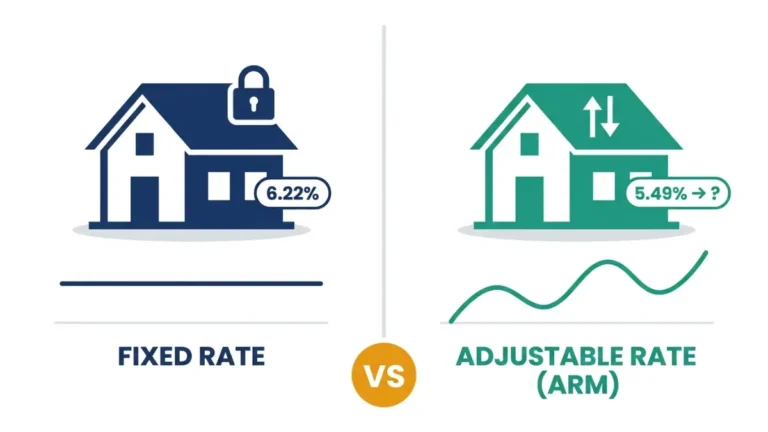

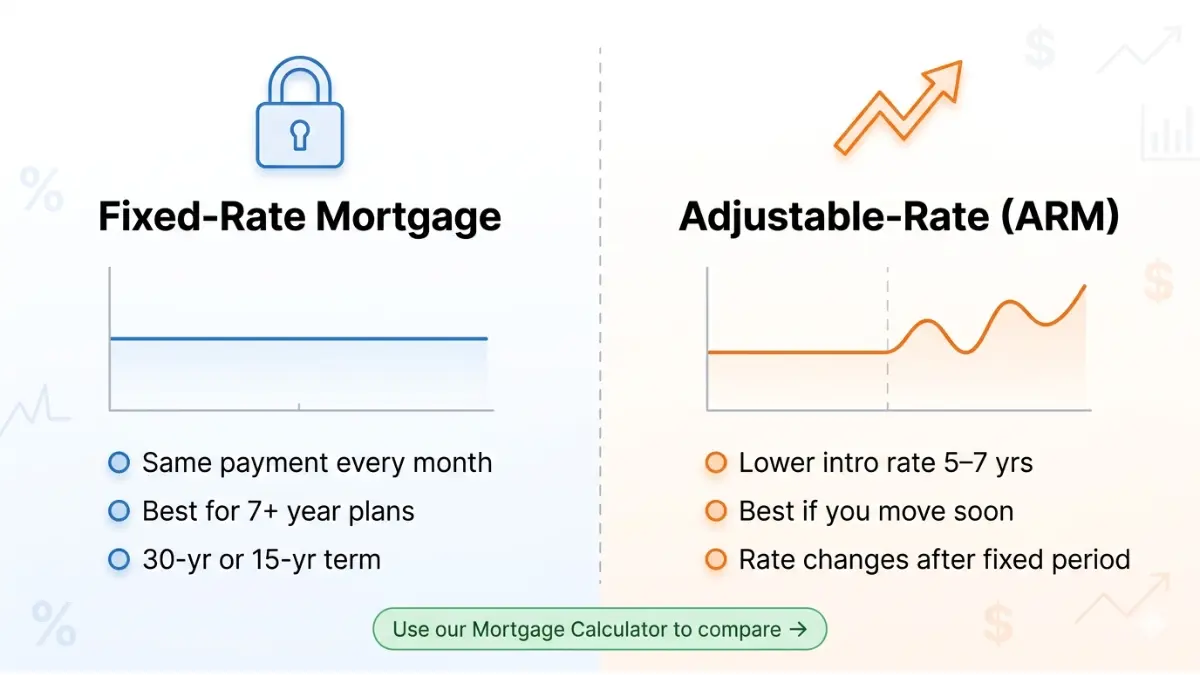

Fixed-Rate vs. Adjustable-Rate Mortgages

Once you choose your loan type, your second biggest decision is the interest rate structure. This choice affects your monthly payment for the next 15–30 years.

Fixed-Rate Mortgages (FRM)

With a fixed-rate mortgage, your interest rate never changes. Your principal + interest payment stays identical from month 1 to your final payment.

- 30-year fixed: Lower monthly payment, higher total interest paid

- 15-year fixed: Higher monthly payment, dramatically lower total interest paid

- Most popular: 30-year fixed-rate remains America’s #1 choice in 2026

Read more: Our 15 vs. 30-Year Mortgage Comparison breaks down the full cost difference with real numbers.

Adjustable-Rate Mortgages (ARM)

An ARM starts with a fixed rate for an introductory period, then adjusts periodically based on a market index.

- 5/1 ARM: Fixed for 5 years, adjusts annually after

- 7/1 ARM: Fixed for 7 years, adjusts annually after

- Initial rates are typically 0.5–1.5% lower than 30-year fixed rates

- Rate caps limit how much the rate can change per adjustment and over the life of the loan

When an ARM makes sense:

- You plan to sell or refinance within 5–7 years

- You expect your income to increase significantly

- You want lower initial payments while building equity

Fixed vs. ARM Cost Comparison on a $400,000 Loan

| Loan Type | Est. Rate (2026) | Monthly Payment | 5-Year Total Interest |

|---|---|---|---|

| 30-Year Fixed | 6.9% | ~$2,640 | ~$131,000 |

| 15-Year Fixed | 6.3% | ~$3,440 | ~$91,000 |

| 5/1 ARM | 6.1% | ~$2,430 | ~$113,000 |

💡 ARM Break-Even: If you move within 5 years, a 5/1 ARM saves you roughly $210/month — that’s $12,600 over the fixed period. Use our Mortgage Refinance Calculator to run your exact numbers.

5 Specialized Home Loan Types Worth Knowing

Beyond the core four, several specialized mortgage options exist for unique situations. Most competitors ignore these — but they could be exactly right for your circumstances.

Jumbo Loans

Jumbo loans are mortgages that exceed conforming loan limits. In 2026, that means any loan above $806,500 (most areas) or $1,209,750 (high-cost markets like NYC, LA, and San Francisco).

- Minimum credit score: 680–700+

- Down payment: 10–20% typically required

- No PMI in many cases, but rates are slightly higher

- Used for luxury homes, high-cost markets, or large land purchases

FHA 203(k) Renovation Loans

The FHA 203(k) program lets you roll the cost of home repairs into your mortgage. Perfect for fixer-uppers.

- Standard 203(k): For major structural work ($5,000+ in repairs)

- Limited 203(k): For minor improvements under $75,000

- One loan = purchase price + renovation costs combined

Construction Loans

A construction loan finances the building of a new home from the ground up. Once construction is complete, it converts to a permanent mortgage.

- Short-term (typically 12 months during construction)

- Higher interest rates than standard mortgages

- Funds are disbursed in stages as work is completed

Reverse Mortgages

Available to homeowners 62 or older, a reverse mortgage lets you convert home equity into cash — with no monthly mortgage payments required while you live in the home.

- You retain ownership of your home

- Loan balance grows over time as interest accrues

- Repaid when you sell, move, or pass away

Deep dive: Our guide on Reverse Mortgages in 2026 covers eligibility, costs, and whether it’s right for your retirement.

Interest-Only Mortgages

With an interest-only mortgage, you pay only the interest for a set period (typically 5–10 years), then begin repaying principal.

- Lower initial payments

- No equity built during interest-only period

- Risk: Large payment increase when principal repayment begins

Quick Reference: Specialized Loan Types

| Loan Type | Best For | Key Requirement |

|---|---|---|

| Jumbo | High-value homes | 680+ credit, 10–20% down |

| FHA 203(k) | Fixer-uppers | 580+ credit, eligible property |

| Construction | Building new home | Strong credit, detailed plans |

| Reverse Mortgage | Seniors 62+ | Significant home equity |

| Interest-Only | Short-term buyers | Strong income, clear exit plan |

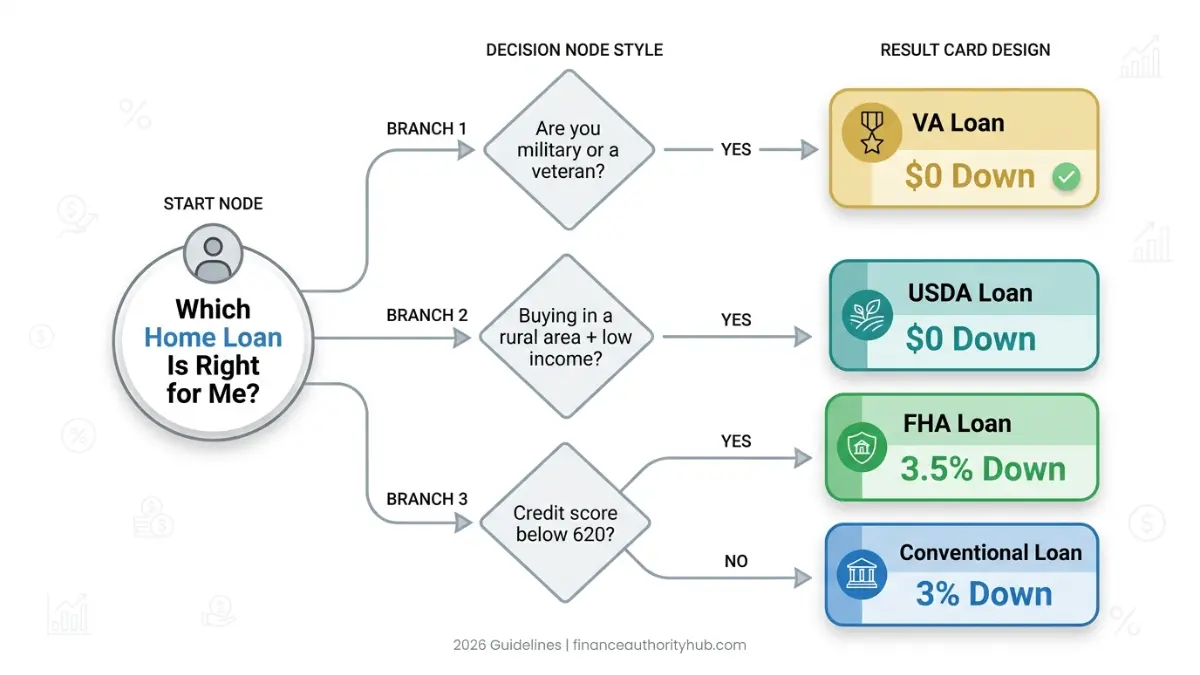

Which Type of Home Loan Is Right for You? (2026 Decision Guide)

Choosing among the types of home loans doesn’t have to be confusing. Your credit score, savings, and situation will almost always point to one clear winner. Here’s how to find it.

Decision Matrix: Best Loan By Buyer Profile

| Your Situation | Best Loan Type | Why |

|---|---|---|

| First-time buyer, 580–619 credit | FHA | Low score accepted, 3.5% down |

| First-time buyer, 620+ credit | Conventional | Lower long-term cost, cancellable PMI |

| Active military / veteran | VA | $0 down, no PMI, lowest rates |

| Buying in rural/suburban area, low-moderate income | USDA | $0 down, low insurance |

| Buying a $900K+ home | Jumbo | Exceeds conforming limits |

| Buying a fixer-upper | FHA 203(k) | Finances repairs in one loan |

| Short-term buyer (move in 5–7 yrs) | ARM | Lower initial rate |

| Homeowner 62+ needing income | Reverse Mortgage | Converts equity to cash |

Choosing by Credit Score

- 500–579: FHA only (10% down required)

- 580–619: FHA (3.5% down), or VA/USDA if eligible

- 620–679: Conventional or FHA — compare costs

- 680+: Conventional, Jumbo, VA — best rates available

Check your score first. Our Credit Score Calculator gives you a starting estimate before you talk to any lender.

Choosing by Down Payment Available

- $0 saved: VA (if military) or USDA (if rural eligible)

- 3–3.5%: Conventional 97 or FHA

- 5–10%: Conventional (lower PMI cost)

- 20%+: Conventional — no PMI, best rate possible

Before you decide, run the numbers with our Home Affordability Calculator and Down Payment Calculator to see exactly what each scenario costs you monthly.

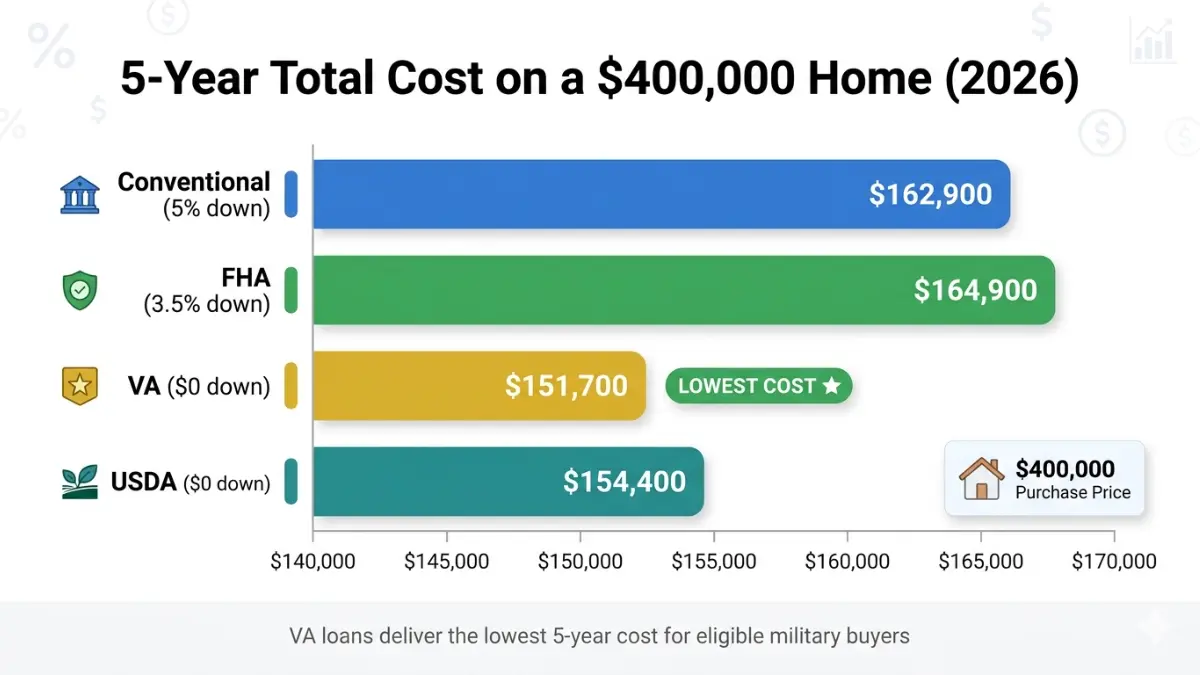

Real Cost Comparison — $400,000 Home Across Loan Types (2026)

Numbers never lie. Here’s what your actual monthly payment and 5-year total cost looks like across the four main mortgage types on a $400,000 home purchase in 2026.

Cost Breakdown Table

| Loan Type | Down Payment | Loan Amount | Est. Rate | Monthly P&I | Mortgage Insurance | 5-Year Total Cost |

|---|---|---|---|---|---|---|

| Conventional (5% down) | $20,000 | $380,000 | 6.9% | ~$2,505 | ~$190/mo PMI | ~$162,900 |

| FHA (3.5% down) | $14,000 | $386,000 | 6.7% | ~$2,488 | ~$260/mo MIP | ~$164,900 |

| VA ($0 down) | $0 | $400,000 | 6.5% | ~$2,528 | None | ~$151,700 |

| USDA ($0 down) | $0 | $400,000 | 6.6% | ~$2,540 | ~$67/mo | ~$154,400 |

Estimates based on March 2026 average rates. Actual rates vary by lender and borrower profile.

Hidden Costs to Factor In

Many buyers focus only on the monthly payment and miss these critical upfront and ongoing costs:

- Closing costs: Typically 2–5% of the loan amount ($8,000–$20,000 on a $400K home)

- FHA upfront MIP: 1.75% of loan amount ($6,755 on $386K, usually financed)

- VA funding fee: 2.15% first use ($8,600 on $400K, can be financed)

- PMI (conventional): Approx. $50–$200/month, cancels at 20% equity

- Property taxes + homeowners insurance: Added to monthly escrow

Pro tip: Before finalizing any loan, check the official CFPB Loan Estimate guide to understand every line item your lender is required to disclose. Then run your exact scenario in our Closing Cost Calculator and Mortgage Calculator.

The VA Loan Advantage — Real Math

On the same $400,000 home, here’s how VA compares to conventional with 5% down over 5 years:

- Down payment saved: $20,000

- PMI avoided: $200/month × 60 months = $12,000

- VA funding fee paid: $8,600 (financed into loan)

- Net advantage of VA loan: ~$23,400 over 5 years

If you or your spouse has served, check your VA loan eligibility before considering any other mortgage type. It is almost always the best financial option for qualifying borrowers.

Frequently Asked Questions — Types of Home Loans

1. What are the 4 main types of home loans?

The four main types of home loans are conventional, FHA, VA, and USDA loans. Conventional loans are the most common. FHA suits buyers with lower credit. VA is exclusively for military. USDA targets rural and suburban areas with income limits.

2. Which home loan is easiest to get approved for?

FHA loans are generally the easiest to qualify for, accepting credit scores as low as 500 with 10% down or 580 with 3.5% down. They also allow higher debt-to-income ratios than conventional loans.

3. What credit score do I need for each loan type?

– FHA: 500–580 minimum

– Conventional: 620 minimum

– VA: No VA minimum (most lenders require 620)

– USDA: 640 minimum

– Jumbo: 680–700 minimum

4. Can I get a home loan with no down payment?

Yes. VA loans (for military/veterans) and USDA loans (for rural buyers) both offer 100% financing with zero down payment required.

5. What is the difference between FHA and conventional loans?

FHA loans are government-backed, accept lower credit scores, and require mortgage insurance for the life of the loan. Conventional loans are private, require better credit, but allow you to cancel PMI once you hit 20% equity — making them cheaper long-term for many buyers.

6. What is a jumbo loan in 2026?

A jumbo loan is any mortgage above $806,500 in most U.S. counties, or above $1,209,750 in high-cost areas. These loans are not backed by Fannie Mae or Freddie Mac and require stronger credit and larger down payments.

7. Are VA loans better than conventional loans?

For eligible veterans and military members, yes — VA loans offer $0 down, no PMI, and competitive interest rates. The only cost is a one-time VA funding fee, which can be financed into the loan.

8. What is a USDA loan and who qualifies?

A USDA loan is a zero-down mortgage backed by the U.S. Department of Agriculture for buyers in eligible rural and suburban areas. Your household income must be at or below 115% of the local median income. Credit scores of 640+ are typically required.

9. What is the best mortgage for first-time buyers?

It depends on your credit and savings. FHA is best for scores below 620. Conventional 97 is ideal for scores above 620. VA is best if you’re military. USDA wins if you qualify by location and income. Our First-Time Home Buyer Guide walks through every step.

10. Should I choose a fixed-rate or adjustable-rate mortgage?

Choose a fixed-rate if you plan to stay in your home 7+ years and want payment stability. Choose an ARM if you plan to sell or refinance within 5–7 years — the lower initial rate can save you thousands. Also read our comparison on APR vs. Interest Rate to understand what you’re actually paying.

11. What type of home loan has the lowest monthly payment?

On a $400,000 home, a VA loan typically offers the lowest monthly payment because it carries no PMI and often comes with below-market interest rates. A 30-year USDA loan is a close second for eligible buyers.

⚠️ Disclaimer: This article is for educational and informational purposes only and does not constitute financial, mortgage, or legal advice. Loan requirements, interest rates, limits, and eligibility criteria are subject to change. Always consult a licensed mortgage professional or HUD-approved housing counselor before making any home loan decision. For personalized guidance, contact a HUD-approved housing counselor at no cost.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.