FHA Loan vs Conventional Loan: Which Is Better for You in 2026?

FHA or conventional loan in 2026? Wrong choice costs $30,000+. Compare credit score requirements, MIP vs PMI, down payments, and loan limits to find your best mortgage.

In This Article

If your credit score is below 680 or you have limited savings, an FHA loan is likely your best path to homeownership. If your score is 720 or higher and you can put down 10%+, a conventional loan will almost certainly save you more money over time. The wrong choice can cost you $30,000+ over the life of your mortgage.

Before diving deeper, use our Home Affordability Calculator to understand exactly how much home you can afford under each loan type.

FHA Loan vs Conventional Loan — 2026 Fast Facts

The FHA loan vs conventional loan debate is the most important mortgage decision most homebuyers will ever make. Yet most buyers choose based on gut instinct rather than data.

Here is what the numbers actually say in 2026:

- FHA average rate (Feb 2026): 6.16%

- Conventional average rate (Feb 2026): 6.09%

- FHA loan limits 2026: $541,287 (standard) — $1,249,125 (high-cost areas)

- Conventional conforming limits 2026: $832,750 — $1,249,125

The rate gap looks tiny. But the total cost gap — driven by mortgage insurance — can be $20,000–$40,000 over 10 years depending on your credit score.

That is the number no competitor talks about loudly enough.

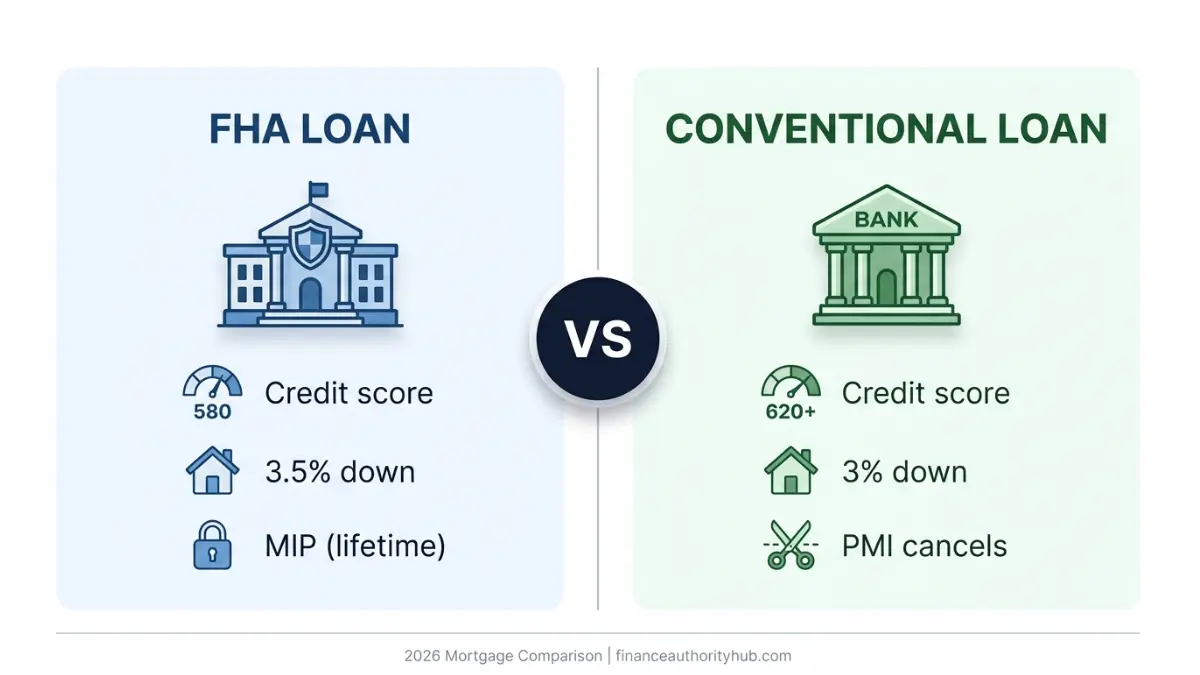

FHA Loan vs Conventional Loan — Full 2026 Side-by-Side Comparison

| Factor | FHA Loan | Conventional Loan |

|---|---|---|

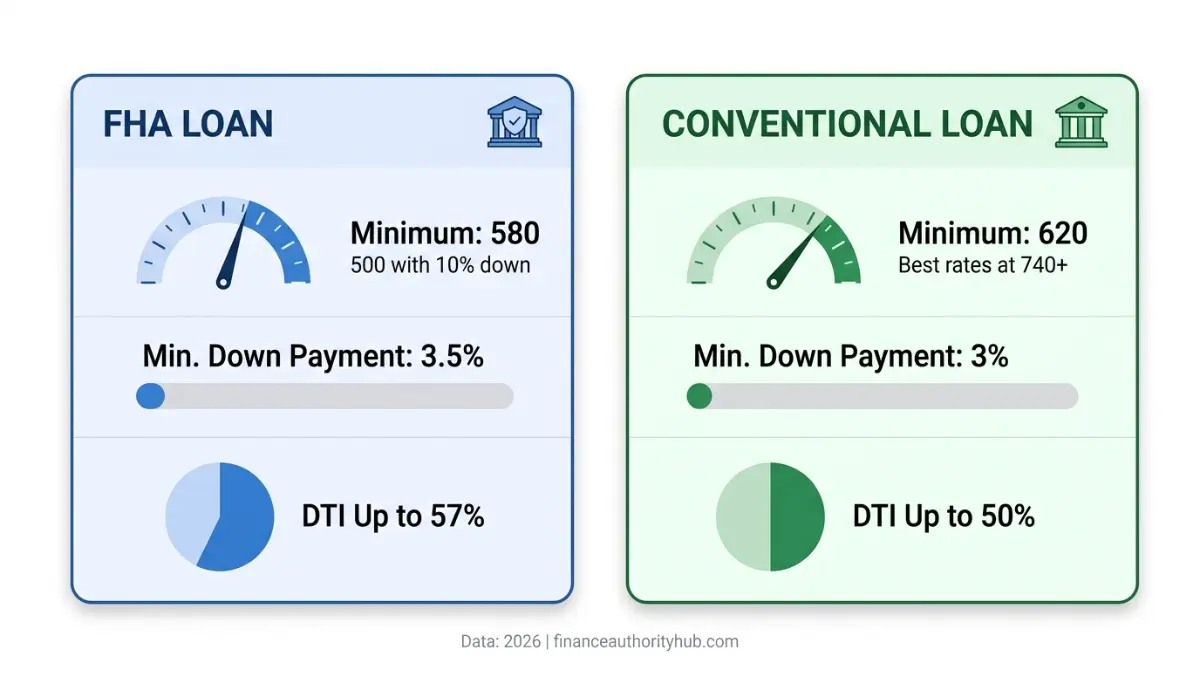

| Minimum credit score | 580 (3.5% down) / 500 (10% down) | 620 minimum; best rates at 740+ |

| Minimum down payment | 3.5% | 3% (HomeReady/Home Possible) |

| Mortgage insurance | MIP for life of loan (if <10% down) | PMI cancels at 20% equity |

| Upfront insurance fee | 1.75% of loan amount | None |

| Annual insurance rate | 0.55% of loan amount | 0.2%–1.5% (varies by credit) |

| Loan limit (standard, 2026) | $541,287 | $832,750 |

| Loan limit (high-cost, 2026) | $1,249,125 | $1,249,125 |

| Property use | Primary residence only | Primary, second home, investment |

| DTI ratio limit | Up to 57% (with compensating factors) | Typically 43–50% |

| Backed by | Federal government (HUD/FHA) | Private lenders (Fannie/Freddie) |

Source: HUD 2026 Loan Limits Announcement

Credit Score Requirements: FHA vs Conventional

FHA loans allow credit scores as low as 580 for the 3.5% down payment option. Scores between 500–579 still qualify but require a 10% down payment.

Conventional loans require a minimum of 620, but borrowers below 740 face meaningfully higher rates and PMI costs. A 640-score borrower on a conventional loan can pay 2–3x more for PMI than a 760-score borrower.

Before applying, check where you stand using our Credit Score Calculator — your score is the single biggest factor in this decision.

Down Payment: 3.5% vs 3% — What’s the Real Difference?

The gap sounds small. On a $400,000 home:

- FHA requires $14,000 (3.5%)

- Conventional HomeReady requires $12,000 (3%)

That $2,000 difference is minor. The bigger issue is who qualifies for the 3% conventional option — it requires a minimum 660 credit score and meets income restrictions. FHA’s 3.5% is far more accessible.

Use our Down Payment Calculator to see exactly how much you need to save for your target home price.

Debt-to-Income Ratio (DTI) — Which Is More Forgiving?

FHA loans allow DTI ratios up to 57% with compensating factors (larger down payment, cash reserves). Conventional loans typically cap at 43–50%.

If you carry student loans, car payments, or credit card debt, FHA’s higher DTI flexibility is a major advantage. Calculate your current DTI with our Debt-to-Income Ratio Calculator before applying for either loan type.

For a full breakdown of DTI and how lenders evaluate it, see our guide on Debt-to-Income Ratio for Home Loans.

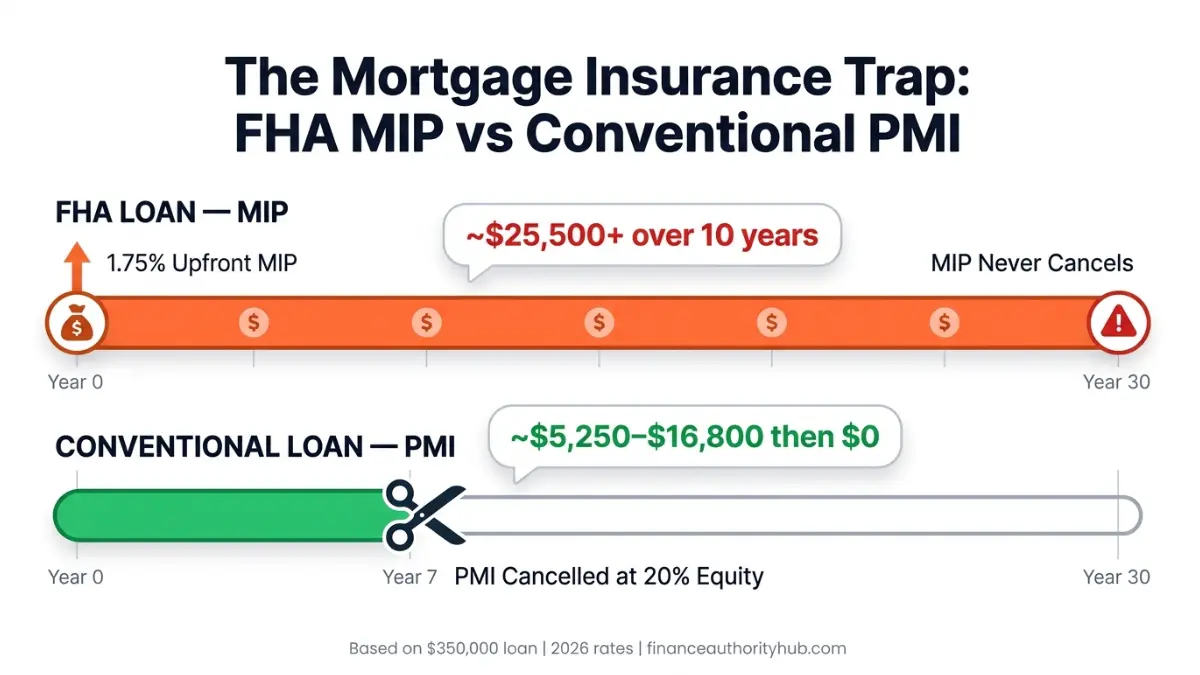

The Hidden Cost Trap — MIP vs PMI (What Competitors Bury)

This is the most important section in the entire FHA loan vs conventional loan comparison — and the detail most buyers miss until it’s too late.

How FHA Mortgage Insurance Works

FHA loans carry a two-part mortgage insurance premium (MIP) structure:

- Upfront MIP: 1.75% of your loan amount at closing (can be rolled into the loan)

- Annual MIP: 0.55% of the loan amount, divided into monthly payments

The critical trap: If you put down less than 10%, FHA MIP lasts for the entire life of the loan. The only way to remove it is to refinance into a conventional loan or sell the home.

The CFPB’s mortgage insurance explainer at consumerfinance.gov confirms this: FHA MIP applies regardless of credit score and remains mandatory unless you exit the FHA program entirely.

How Conventional PMI Works

Private mortgage insurance (PMI) on a conventional loan works differently in three key ways:

- No upfront fee — only a monthly premium

- Cost varies by credit score (0.2%–1.5% annually)

- Automatically cancels when you reach 78% LTV; you can request cancellation at 80% equity

A 760-score borrower might pay just 0.3% PMI annually. That same borrower on an FHA loan pays the flat 0.55% rate — plus the 1.75% upfront MIP.

Real Dollar Comparison — $350,000 Home, 3.5% vs 3.5% Down

| Scenario | Loan Type | Credit Score | Upfront MIP/PMI | Annual Insurance Cost | Insurance Cost Over 7 Years |

|---|---|---|---|---|---|

| Buyer A | FHA | 640 | $6,038 (MIP) | $1,925/yr | $19,513 (never cancels) |

| Buyer B | Conventional | 640 | $0 | $4,200/yr (1.2% PMI) | $16,800 (cancels at ~yr 7) |

| Buyer C | Conventional | 760 | $0 | $1,050/yr (0.3% PMI) | $5,250 (cancels at ~yr 7) |

Key takeaway: For a 640-score buyer, FHA and conventional MIP/PMI costs are surprisingly comparable — but FHA’s never goes away. For a 760-score buyer, conventional PMI costs less than one-third of FHA insurance over the same period.

Use our Mortgage Calculator to run your own side-by-side payment estimates.

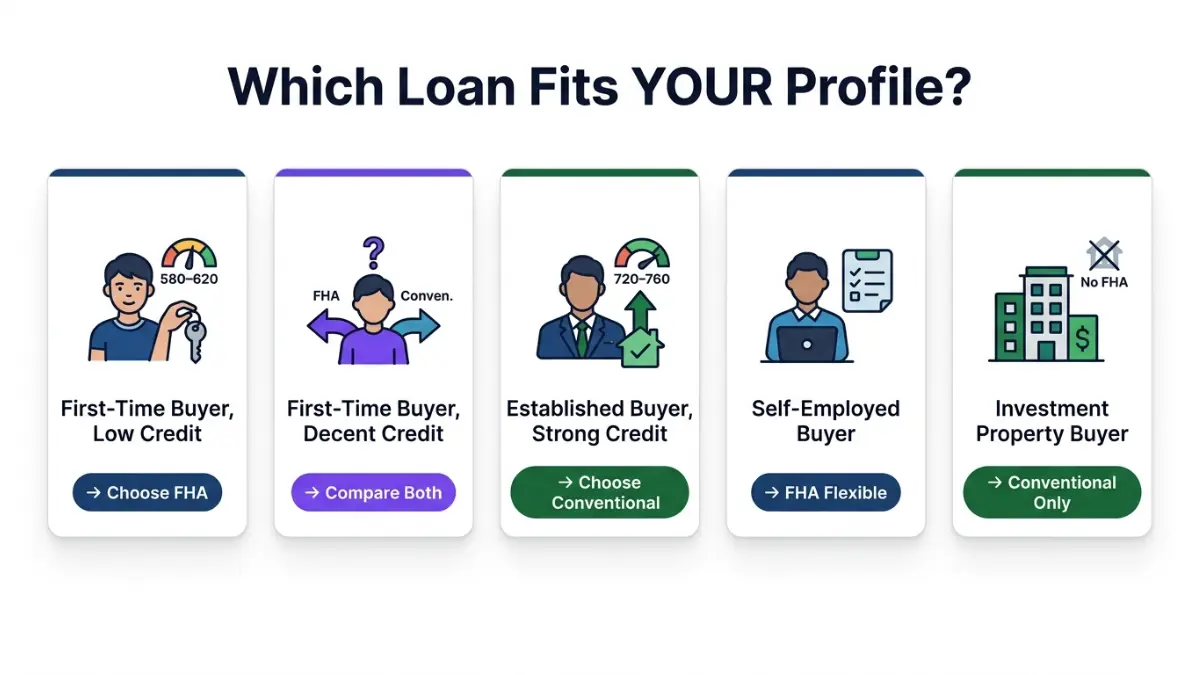

Which Loan Is Right for You? — The 2026 Buyer Profile Matrix

Stop guessing. Match your profile to the loan.

| Your Profile | Credit Score | Down Payment | Best Choice | Why |

|---|---|---|---|---|

| First-time buyer, building credit | 580–620 | 3.5% | FHA | Lower barrier to qualify |

| First-time buyer, decent credit | 640–680 | 5–10% | Run both scenarios | Numbers are close; get quotes for both |

| Established buyer, strong credit | 720–760 | 10–20% | Conventional | PMI cancels, lower long-term cost |

| Self-employed / irregular income | 620+ | 5%+ | FHA | More flexible underwriting |

| Investment property buyer | Any | 15%+ | Conventional only | FHA requires primary residence |

| Buying in a high-cost market | Any | Varies | Compare limits | FHA caps at $541,287 in most areas |

Should First-Time Buyers Always Choose FHA?

No — this is one of the most persistent myths in mortgage lending.

If your credit score is 660+, a conventional loan with HomeReady (Fannie Mae) or Home Possible (Freddie Mac) at 3% down may cost you significantly less over 5–7 years, because PMI cancels and there is no upfront MIP fee.

FHA is the right choice when:

- Your credit score is below 640

- Your DTI is above 45%

- You went through a bankruptcy or foreclosure within the last 3 years

- You have limited cash reserves beyond the down payment

Read our complete guide on Credit Score to Buy a House to understand exactly how your credit score affects both loan types.

The FHA-to-Conventional Refinance Strategy

Many smart buyers use this deliberate two-step approach:

- Buy with FHA when credit is under 660 or savings are limited

- Refinance to conventional after 2–3 years once credit improves and equity reaches 20%

This strategy eliminates lifetime MIP while still getting into the market now. Use our Mortgage Refinance Calculator to calculate your potential savings from refinancing out of FHA.

“The FHA-to-conventional refinance is one of the most underused wealth-building strategies in residential real estate. Buyers who plan this from day one save tens of thousands.” — Laura M. Bennett, CFP, Finance Authority Hub Expert Panel

How to Apply — Step-by-Step Guide for 2026

Whether you choose an FHA loan or conventional loan, the application process follows the same core steps. Here is what to do — and where FHA and conventional differ.

Step 1: Check your credit score Pull your free report from AnnualCreditReport.com. Scores below 620: target FHA. Scores 660+: compare both. See our Home Loan Requirements guide for a full checklist.

Step 2: Calculate your DTI ratio Add all monthly debt payments ÷ gross monthly income. FHA allows up to 57%; conventional typically caps at 50%.

Step 3: Determine your down payment FHA minimum: 3.5% (credit 580+). Conventional minimum: 3% (credit 660+, income limits apply). Check our Down Payment Help Guide for 2026 assistance programs.

Step 4: Get pre-approved For FHA, use only HUD-approved lenders. For conventional loans, compare at least 3 lenders — rates vary significantly.

Step 5: Lock your rate Rates change daily. In February 2026, FHA averaged 6.16% vs conventional 6.09% — but your personal rate depends on your credit tier, LTV, and lender. See our guide on APR vs Interest Rate to understand why the APR matters more than the rate alone.

Step 6: Close and move in FHA appraisals are stricter — properties must meet HUD’s Minimum Property Standards. Conventional appraisals focus primarily on value. Factor in 30–60 days for closing on either loan type. Use our Closing Cost Calculator to budget accurately.

2026 Market Context — Does It Favor FHA or Conventional?

Rising home prices have pushed the median U.S. home value above $400,000 in many markets, stretching FHA’s $541,287 standard limit. In high-cost metros like San Francisco, Seattle, and New York, FHA and conventional limits converge at $1,249,125 — making loan type selection entirely about cost, not limit.

With rates above 6%, the MIP trap on FHA loans is even more painful because you are financing the 1.75% upfront MIP at 6%+ interest for 30 years if you do not refinance. For a $350,000 loan, that upfront MIP rolled into the loan costs approximately $11,000 in interest over 30 years on top of the premium itself.

FAQs — FHA Loan vs Conventional Loan

1. What credit score do I need for an FHA loan vs conventional loan?

FHA requires a minimum 580 for 3.5% down; 500 with 10% down. Conventional loans require at least 620, with best rates starting at 740+.

2. Is FHA easier to get than a conventional loan?

Yes. FHA has lower credit score minimums, higher DTI allowances, and more flexible underwriting — especially for buyers who experienced past financial hardship.

3. Can I switch from an FHA loan to a conventional loan?

Yes — through refinancing. Once you have 20% equity and a qualifying credit score (typically 620+), you can refinance to a conventional loan and eliminate FHA MIP permanently.

4. Which loan has lower monthly payments — FHA or conventional?

It depends on your credit score. Buyers with scores above 720 will typically have lower monthly payments on a conventional loan. Below 660, FHA often wins on the base rate — but the MIP adds back to the payment.

5. Does FHA mortgage insurance ever go away?

Only if you put down 10% or more — in which case MIP ends after 11 years. If you put down less than 10%, MIP lasts for the life of the loan. This is the single most important reason to consider refinancing to conventional once you build equity.

6. What is the FHA loan limit in 2026?

The standard FHA limit for a single-family home in 2026 is $541,287 in most U.S. counties and $1,249,125 in high-cost areas, per HUD’s official 2026 announcement.

7. Can I use an FHA loan to buy an investment property?

No. FHA loans are restricted to primary residences only. For second homes or investment properties, a conventional loan is your only option.

8. Which is better for first-time buyers — FHA or conventional?

FHA is better if your credit is below 660 or your DTI is above 45%. Conventional (HomeReady/Home Possible) is better if you have a 660+ score and want to avoid lifetime MIP. Always compare total 5-year and 10-year costs, not just the monthly payment.

9. What is PMI on a conventional loan?

PMI (Private Mortgage Insurance) is required when your down payment is less than 20%. Unlike FHA MIP, PMI can be cancelled once you reach 20% equity. Rates vary from 0.2%–1.5% annually based on your credit score and LTV.

10. How long does FHA loan approval take vs conventional?

Both typically take 30–60 days. FHA can take slightly longer due to the stricter property appraisal requirements under HUD’s Minimum Property Standards.

11. Is a conventional loan always better if I have good credit?

Generally yes — if your score is 740+ and you can put down 10–20%. But for scores between 660–720, run the numbers on both. The break-even analysis sometimes surprises borrowers.

Expert Verdict

“The FHA vs conventional decision is financial, not emotional. Run the 10-year total cost comparison before you choose — not just the monthly payment.” — Laura M. Bennett, CFP, Finance Authority Hub Expert Panel

The right mortgage is the one that matches your current financial profile and your 5-year plan. If you are building credit now, FHA is your bridge. If you are credit-ready today, conventional saves you more. Either way, get pre-approved for both and compare the full Loan Estimate documents side by side.

Explore your full home-buying toolkit: Mortgage Calculator | Amortization Calculator | Home Loan Requirements Guide

📋 Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, or lending advice. Mortgage rates, guidelines, and loan limits are subject to change. FHA loan limits cited reflect HUD’s official 2026 announcement. Individual rates and qualification depend on your credit profile, income, and lender. Please consult a licensed mortgage professional or HUD-approved housing counselor for advice specific to your situation.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.