Down Payment 2026: $18K Free Help Most Buyers Miss

Most buyers waste years saving 20% down they never needed. The 2026 reality: first-timers put down 10%, and 2,624 programs offer $18K average assistance. Here’s how to access it.

In This Article

Most homebuyers waste years saving for a 20% down payment they never needed. The median first-time buyer in 2026 puts down just 10%—and more than 2,600 assistance programs offer an average of $18,000 in free or forgivable help. Here’s everything you need to know about down payments, from minimum requirements to hidden programs that could save you thousands.

Down Payment 2026: The $18K Free Money Most Buyers Don’t Know Exists

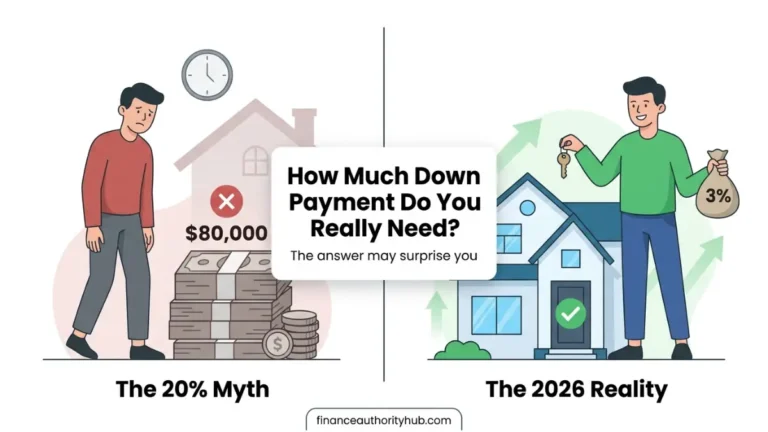

The 20% down payment “rule” is bankrupting the American Dream. While buyers spend 5-7 years scraping together $80,000, they miss out on years of equity building and price appreciation—all because of a myth.

The 2026 reality is drastically different. According to the National Association of Realtors’ 2025 Profile, first-time buyers now put down a median of just 10%, while repeat buyers contribute 19%. These figures represent the highest down payment levels since 1989 for first-timers—but they’re still far below the mythical 20% threshold most people believe is mandatory.

Here’s the breakdown that changes everything:

2026 Down Payment Reality:

- Median down payment (all buyers): 19% or $78,888 on a $415,200 home

- First-time buyers median: 10% or $41,520

- Repeat buyers median: 23% or $95,496

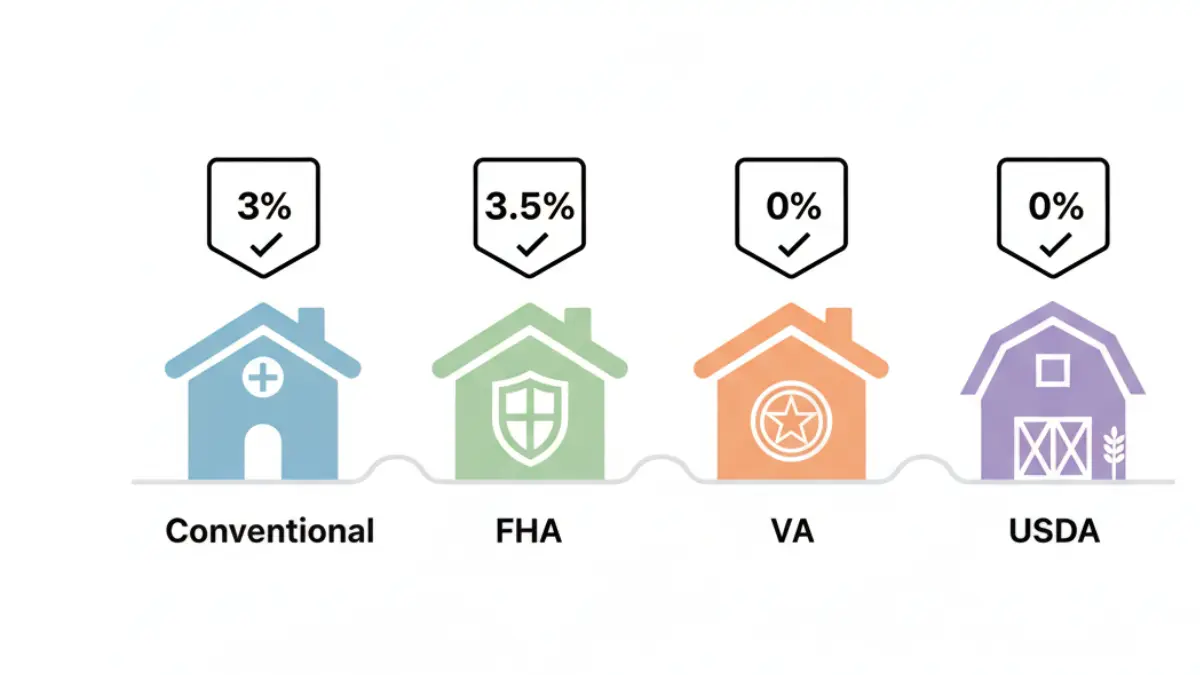

- Minimum down payment: As low as 0% with VA/USDA loans or 3% conventional

The bigger shock? Over 2,600 down payment assistance programs exist across the United States, with the average recipient receiving $10,000-$18,000 in grants, forgivable loans, or deferred payment help. Yet 76% of eligible buyers never apply because they don’t know these programs exist.

Consider Sarah and Michael, a dual-income couple from Phoenix earning $92,000 combined. They spent three years saving $60,000 for a 20% down payment on a $300,000 home. During those three years, Phoenix home prices rose 18%, pushing their target home to $354,000. Their savings actually lost ground against appreciation.

What they didn’t know: Arizona offers multiple down payment assistance programs, including the Arizona Housing Finance Authority HOME Plus program providing up to $15,000 in forgivable second mortgages. Combined with a 3% down conventional loan ($9,000), they could have purchased at $300,000 with just $9,000 of their own money—keeping $51,000 in reserves and avoiding three years of price increases.

The cost of waiting is staggering. That same Phoenix home purchased in 2023 for $300,000 is now worth $354,000—a $54,000 equity gain. The couple’s “responsible” approach to saving 20% cost them more than their entire down payment in lost appreciation.

Use our Home Affordability Calculator to see how different down payment amounts affect your monthly payment and total purchase power. The results might surprise you—especially when you factor in appreciation and rental costs avoided.

Why this matters now: First-time buyers represented just 21% of all purchases in 2025, down from 32% in 2023 and 45% in 2009. The median age of first-time buyers hit a record 40 years old, up from the late 20s in the 1980s. This delay costs buyers an estimated $150,000 in lost equity on a typical starter home, according to NAR analysis.

The crisis is clear: buyers who could afford monthly mortgage payments are locked out by upfront costs they believe are larger than reality. Let’s fix that misconception with facts.

How Much Down Payment Do You Really Need in 2026?

Down payment requirements vary dramatically by loan type, and understanding these options is critical to making an informed decision. Here’s the complete breakdown for 2026:

Conventional Loans: 3-20% Range Explained

Conventional loans—mortgages not backed by government agencies—offer the most flexibility in down payment options. Contrary to popular belief, you don’t need 20% down for a conventional loan.

Conventional Loan Down Payment Tiers:

| Down Payment % | Home Price: $400K | Your Cost | PMI Required? | Rate Impact |

|---|---|---|---|---|

| 3% | $400,000 | $12,000 | Yes | Standard |

| 5% | $400,000 | $20,000 | Yes | -0.125% |

| 10% | $400,000 | $40,000 | Yes | -0.25% |

| 15% | $400,000 | $60,000 | Yes | -0.375% |

| 20% | $400,000 | $80,000 | No | -0.50% |

Private Mortgage Insurance (PMI) kicks in on conventional loans with less than 20% down, typically costing 0.5-1.5% of the original loan amount annually ($167-$500/month on a $400K home). However, PMI automatically cancels once you reach 20% equity through payments and appreciation.

Programs like Fannie Mae’s HomeReady and Freddie Mac’s Home Possible offer 3% down for qualifying buyers with income limits up to 80% of area median income. These programs are designed specifically for first-time and moderate-income buyers.

FHA Loans: 3.5% Minimum for First-Time Buyers

Federal Housing Administration loans require just 3.5% down for borrowers with credit scores of 580 or higher. With scores between 500-579, the minimum jumps to 10%.

FHA Loan Example (3.5% down):

- Home price: $350,000

- Down payment: $12,250

- Loan amount: $337,750

- Monthly PMI (MIP): ~$235/month

The catch with FHA loans? Mortgage insurance premiums (MIP) last for the life of the loan if you put down less than 10%, though you can refinance to a conventional loan once you reach 20% equity. Despite this, FHA remains popular—28% of all home purchases in 2025 used FHA financing, according to NAR data.

VA Loans: $0 Down for Veterans

Veterans, active-duty service members, and qualifying surviving spouses can access VA loans with zero down payment and no monthly mortgage insurance. This is arguably the most powerful homebuying benefit available.

VA Loan Advantages:

- $0 down payment on any home price (up to county limits)

- No monthly mortgage insurance

- Competitive interest rates (typically 0.25-0.50% lower than conventional)

- Funding fee: 2.15% for first-time use, can be financed into loan

On a $400,000 home, a VA loan eliminates $80,000 in upfront costs compared to a 20% conventional down payment. Check eligibility at the Department of Veterans Affairs.

USDA Loans: $0 Down in Eligible Rural Areas

USDA loans serve rural and suburban homebuyers with zero down payment requirements for properties in eligible areas. Despite the “rural” label, many suburban communities qualify.

USDA Loan Requirements:

- 0% down payment

- Property must be in USDA-eligible area (check the USDA map)

- Household income limits apply (typically 115% of area median)

- 1% guarantee fee (can be financed)

Our Mortgage Calculator shows how these different loan types impact your monthly payment. A $300,000 home with 3% down ($9,000) versus 20% down ($60,000) changes monthly principal and interest by roughly $350—but preserves $51,000 in cash reserves.

Expert insight: “I see buyers delay homeownership for years trying to hit 20% down,” says Marcus Thompson, senior loan officer at Pacific Mortgage Group. “Meanwhile, they’re paying $2,000/month in rent that builds zero equity. A 5% down payment with PMI at $150/month makes far more financial sense than continuing to rent while saving.”

Understanding the mortgage pre-approval process helps you determine which loan type fits your situation best. Getting pre-approved early reveals your options and buying power—often showing you need far less cash than expected.

Down Payment Assistance Programs: $18K Average Help in 2026

Down payment assistance (DPA) is the housing market’s best-kept secret. As of Q3 2025, a record 2,624 programs operate nationwide, yet three-quarters of eligible buyers never apply.

4 Types of Down Payment Assistance Explained

1. Grants (Free Money—Never Repaid)

Grants are the gold standard of down payment assistance. You receive funds at closing that never need to be repaid, regardless of how long you live in the home.

Example Grant Programs:

- Bank of America’s Down Payment Grant: Up to 3% of purchase price ($10,000 max) in select markets

- Chenoa Fund: Up to 3.5% for FHA buyers nationwide

- State Housing Finance Agency grants: Typically $2,500-$7,500

2. Forgivable Loans (Forgiven After 5-15 Years)

Forgivable loans function as second mortgages with no monthly payment. After living in the home for a specified period (usually 5-15 years), the loan is completely forgiven.

Example: California’s Dream For All program offers up to $150,000 in shared appreciation loans. While not technically “forgivable,” they require no monthly payment and are only repaid when you sell or refinance.

3. Deferred Payment Loans (No Payment Until You Sell)

These second mortgages carry 0% interest and require no monthly payment. You repay them only when you sell, refinance, or no longer occupy the home as your primary residence.

Common Structure:

- Loan amount: $5,000-$25,000

- Interest rate: 0%

- Monthly payment: $0

- Repayment trigger: Sale, refinance, or move

4. Low-Interest Second Mortgages

Some DPA programs provide below-market second mortgages requiring monthly payments but at rates significantly lower than market rates.

State-by-State Program Breakdown (Top 10 States)

| State | Max Assistance | Program Type | Income Limit (% AMI) | First-Time Buyer Only? |

|---|---|---|---|---|

| California | $150,000 | Shared appreciation | 150% | Yes |

| Texas | $30,000 | Forgivable/deferred | 140% | No (some programs) |

| Florida | $15,000 | Deferred payment | 140% | Varies |

| New York | $100,000 | Various | 130% | Varies |

| Pennsylvania | $15,000 | Forgivable loan | 120% | Yes (most) |

| Illinois | $10,000 | Grant | 120% | No |

| Ohio | $7,500 | Forgivable loan | 120% | Yes |

| Michigan | $7,500 | Deferred payment | 120% | Yes |

| Georgia | $7,500 | Grant + loan | 140% | Yes |

| North Carolina | $8,000 | Forgivable loan | 115% | Yes |

How to Find Programs in Your Area

Finding DPA programs requires knowing where to look:

1. DownPaymentResource.com – The most comprehensive national database connecting buyers with local programs

2. State Housing Finance Agencies – Every state operates a housing finance authority administering DPA. Examples:

- California Housing Finance Agency (CalHFA)

- Texas Department of Housing

- Pennsylvania Housing Finance Agency

3. HUD-Approved Housing Counselors – Free counseling connecting you to local programs (find counselors here)

4. Local City/County Programs – Many municipalities offer additional assistance beyond state programs

Eligibility Requirements Most Buyers Meet

DPA eligibility is more accessible than most people realize:

Common Requirements:

- First-time homebuyer status: Defined as not owning a home in the past 3 years (you don’t have to be a true first-timer)

- Income limits: Typically 80-140% of Area Median Income ($70,000-$140,000 for many metros)

- Credit score: Usually 620-640 minimum

- Homebuyer education: 6-8 hour course (often available online for $50-$100)

- Owner occupancy: Must live in the home as primary residence

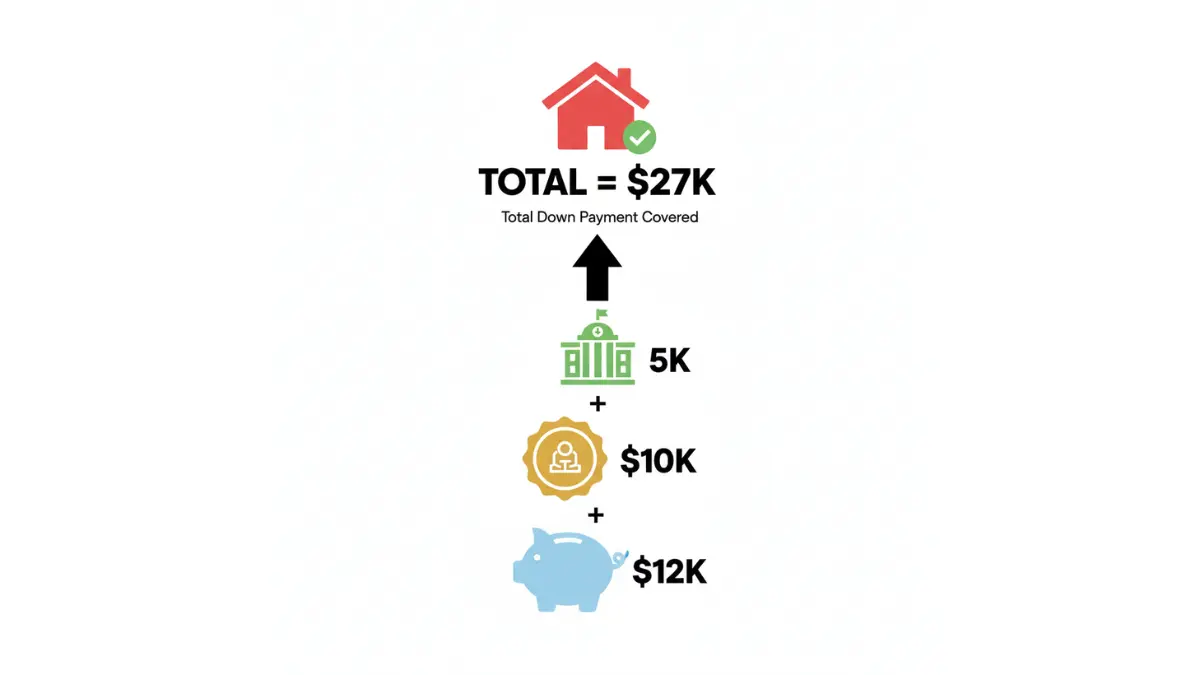

Real success story: Jennifer Martinez, a single teacher in Denver earning $68,000, thought homeownership was impossible. Denver’s median home price of $575,000 would require $115,000 for a 20% down payment—nearly two years of her gross income.

Instead, Jennifer worked with a HUD-certified housing counselor who identified three programs she qualified for. She combined:

- Colorado Housing Finance Authority’s down payment assistance: $8,000 grant

- Denver METRO Hardest Hit Fund: $10,000 forgivable loan

- 3% conventional loan: $17,250 from savings

Total out-of-pocket: $17,250 for a $575,000 home (3% instead of 20%). Her monthly payment with PMI is $3,850—only $350 more than she was paying in rent. Within two years, Denver’s 6% annual appreciation gave her $68,700 in equity while PMI dropped to $245/month as her loan-to-value improved.

Understanding how to pay off debt fast before applying improves your debt-to-income ratio and approval odds. Many DPA programs require DTI below 43-50%.

Down Payment Costs by Region: 2026 Market Reality

Down payment requirements hit different depending on where you buy. A 10% down payment ranges from $20,000 in affordable markets to $125,000 in coastal cities—making regional strategy essential.

High-Cost Markets: Where You Need More

Most Expensive Down Payment Markets (10% down):

| Metro Area | Median Home Price | 10% Down | 3% Down (Minimum) |

|---|---|---|---|

| San Jose, CA | $1,400,000 | $140,000 | $42,000 |

| San Francisco, CA | $1,350,000 | $135,000 | $40,500 |

| Honolulu, HI | $985,000 | $98,500 | $29,550 |

| Los Angeles, CA | $925,000 | $92,500 | $27,750 |

| San Diego, CA | $875,000 | $87,500 | $26,250 |

| Seattle, WA | $745,000 | $74,500 | $22,350 |

| Boston, MA | $685,000 | $68,500 | $20,550 |

| New York, NY | $650,000 | $65,000 | $19,500 |

| Denver, CO | $575,000 | $57,500 | $17,250 |

| Miami, FL | $535,000 | $53,500 | $16,050 |

High-cost markets create the biggest barrier to entry, but they also offer the most robust down payment assistance programs. California alone has over 300 DPA programs, with some offering up to $150,000 in help.

Affordable Markets: Under $200K Homes Still Exist

Despite national headlines, dozens of markets still offer median home prices under $300,000—making 10% down payment requirements achievable at under $30,000.

Most Affordable Markets (10% down under $25,000):

| Metro Area | Median Price | 10% Down | 3% Down |

|---|---|---|---|

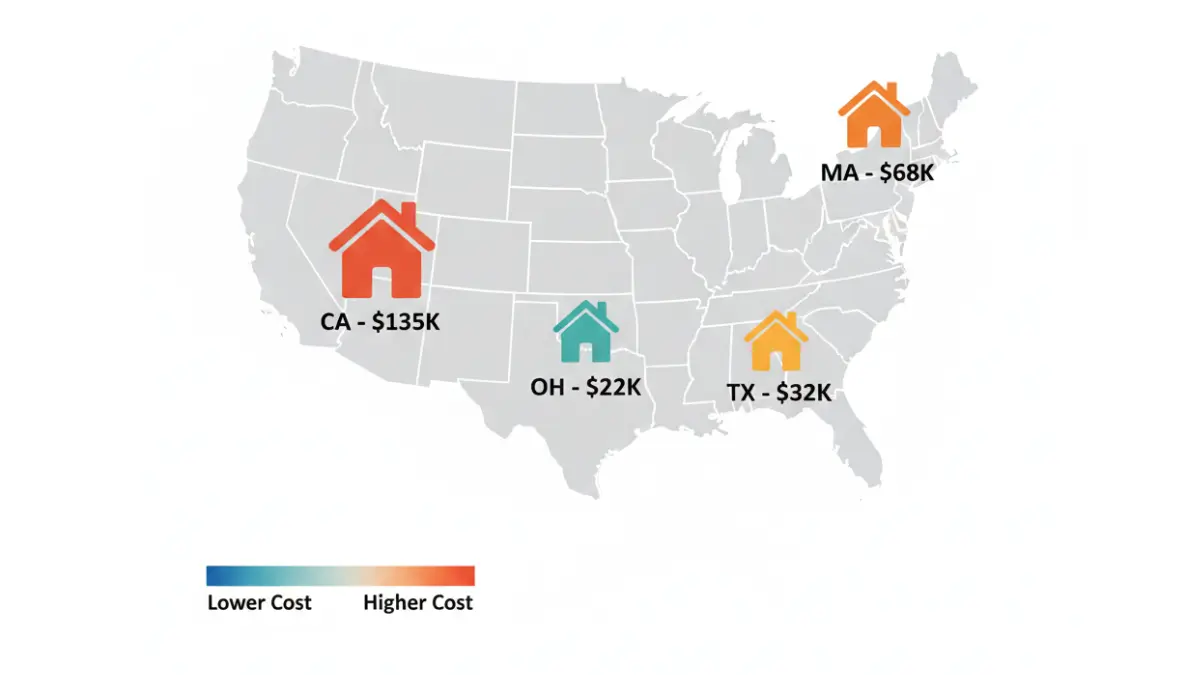

| Detroit, MI | $225,000 | $22,500 | $6,750 |

| Cleveland, OH | $240,000 | $24,000 | $7,200 |

| St. Louis, MO | $245,000 | $24,500 | $7,350 |

| Pittsburgh, PA | $250,000 | $25,000 | $7,500 |

| Memphis, TN | $265,000 | $26,500 | $7,950 |

| Oklahoma City, OK | $275,000 | $27,500 | $8,250 |

| Buffalo, NY | $280,000 | $28,000 | $8,400 |

| Indianapolis, IN | $290,000 | $29,000 | $8,700 |

These markets offer realistic entry points for median-income earners. A household earning $75,000 can save $22,500 (10% down on Detroit’s median) in roughly 18-24 months with disciplined saving.

First-Time Buyer Hotspots for 2026

According to realtor.com’s 2026 analysis, the best markets for first-time buyers balance affordability, job growth, and inventory availability:

Top 10 First-Time Buyer Markets:

- Pittsburgh, PA – Median $250K, strong job market

- Indianapolis, IN – Median $290K, growing tech sector

- Memphis, TN – Median $265K, low cost of living

- Cincinnati, OH – Median $295K, diverse economy

- Kansas City, MO – Median $315K, steady growth

- Columbus, OH – Median $320K, university hub

- Louisville, KY – Median $285K, manufacturing strong

- Birmingham, AL – Median $270K, healthcare growing

- Buffalo, NY – Median $280K, renaissance underway

- Des Moines, IA – Median $300K, insurance jobs

National context matters: The median age of first-time buyers reached 40 in 2025, reflecting affordability challenges. Households need a median income of $97,000 to afford the typical home at current rates and prices, according to NAR analysis—up from $76,000 just three years ago.

Regional planning using our Home Affordability Calculator helps you target realistic markets. If San Francisco requires $135,000 for 10% down but Sacramento needs just $45,000, relocating 90 miles could reduce your savings requirement by $90,000.

Expert perspective: “Geography is destiny in real estate,” notes Dr. Lisa Chen, housing economist at Stanford University. “A nurse earning $85,000 in San Francisco is priced out completely, but that same nurse in Pittsburgh qualifies for a $350,000 home with 3% down and assistance programs covering half their down payment.”

For buyers exploring different markets, understanding lowest mortgage rates by state reveals how rate variations impact affordability—sometimes as much as down payment differences.

How to Save for a Down Payment Fast (2026 Action Plan)

Saving for a down payment feels impossible until you reverse-engineer the math and leverage assistance programs. Here’s how to accelerate your timeline.

6-Month, 12-Month, and 24-Month Savings Plans

Timeline Planning by Down Payment Goal:

| Home Price | 3% Down | 5% Down | 10% Down | 20% Down |

|---|---|---|---|---|

| $250,000 | $7,500 | $12,500 | $25,000 | $50,000 |

| Monthly (6 mo) | $1,250 | $2,083 | $4,167 | $8,333 |

| Monthly (12 mo) | $625 | $1,042 | $2,083 | $4,167 |

| Monthly (24 mo) | $313 | $521 | $1,042 | $2,083 |

$350,000 target:

- 3% down: $10,500

- Monthly (6 mo): $1,750

- Monthly (12 mo): $875

- Monthly (24 mo): $438

These calculations assume zero interest, but high-yield savings significantly boost results.

High-Yield Savings Accounts for Down Payment Funds

Traditional savings accounts pay 0.01% APY—effectively $0. High-yield savings accounts now offer 4.0-5.0% APY through online banks.

Impact of High-Yield Savings:

Saving $800/month for 24 months to reach $19,200:

- Traditional savings (0.01%): $19,202

- High-yield savings (4.5%): $20,064

- Bonus earned: $862

The best high-yield savings accounts currently offering 5% APY include American Express, Marcus, and Ally Bank. Every dollar saved earns interest daily, compounding your progress.

Combining Personal Savings with DPA Programs

The most powerful strategy: save enough for minimum down payment, then stack DPA programs to reduce your cash requirement.

Case Study Strategy:

Goal: Purchase $400,000 home Traditional approach (20%): $80,000 needed

Optimized approach:

- Target 3% down payment: $12,000 personal savings (achievable in 12-15 months saving $850/month)

- Apply for state DPA: $10,000 grant

- Apply for city DPA: $5,000 forgivable loan

- Total out-of-pocket: $12,000 vs $80,000

- Time saved: 9-10 years of additional saving avoided

This approach frees up $68,000 to keep as emergency reserves, pay off high-interest debt, or invest elsewhere. Our Debt Consolidation Calculator shows how eliminating credit card debt before buying improves approval odds and monthly cash flow.

Gift Funds from Family: Rules & Documentation

Gift funds can cover part or all of your down payment, but lenders require specific documentation to distinguish gifts from loans.

Gift Fund Requirements:

- Donor must be family member (parent, sibling, grandparent, spouse-to-be)

- Gift letter stating funds are a gift, not a loan, with no repayment expected

- Paper trail showing transfer from donor’s account to yours

- Funds must “season” in your account (usually 60 days) or come directly to closing

Conventional loans: Gifts can cover entire down payment if donor qualifies

FHA loans: Gifts can cover 100% of down payment

VA/USDA loans: Not applicable (0% down), but gifts can cover closing costs

Understanding how the 52-week savings challenge works provides a structured approach—participants save increasing amounts weekly, accumulating $1,378 in 52 weeks without feeling the impact.

Realistic timeline: A couple earning $110,000 combined saving $1,200/month in a 4.5% high-yield account reaches:

- $15,000 in 12 months

- $30,000 in 24 months

- $45,000 in 36 months

Combined with $15,000 in down payment assistance, they need just 18-24 months to access homeownership at 3-5% down rather than 5-7 years for 20%.

Down Payment Myths That Cost Buyers Thousands

Misconceptions about down payments delay homeownership by an average of 4.3 years for first-time buyers. Let’s demolish the most expensive myths with data.

Myth #1: You Must Put 20% Down

Reality: Only 8% of first-time buyers put 20% or more down in 2025.

The 20% threshold originated from private mortgage insurance (PMI) requirements on conventional loans—not as a mandatory minimum. With median first-time buyers putting down just 10%, and minimums as low as 3%, the 20% “requirement” is pure fiction.

Financial impact of this myth:

Waiting to save 20% on a $400,000 home while renting $2,000/month:

- Down payment target: $80,000

- Time to save at $1,000/month: 80 months (6.7 years)

- Total rent paid while saving: $160,000

- Equity in rent: $0

- Home appreciation missed (5%/year): $138,000

Buying with 5% down ($20,000) after 20 months:

- Rent paid: $40,000

- Equity built: $42,000 (appreciation + principal paydown)

- Net advantage: $138,000

Myth #2: PMI Is Always a Bad Deal

Reality: PMI often costs less than rent increases and becomes irrelevant as equity grows.

Private mortgage insurance on a $380,000 loan (5% down on $400K) costs approximately $200/month at 0.63% annually. That’s often less than annual rent increases in competitive markets where rents rise 3-5% yearly.

PMI Math Example:

$400,000 home, 5% down ($20,000):

- Loan amount: $380,000

- PMI: ~$200/month ($2,400/year)

- After 5 years appreciation (5%/year): Home worth $510,000

- Equity from appreciation: $110,000

- PMI automatically cancels at 20% equity (reached in ~5 years with appreciation + paydown)

- Total PMI paid: ~$12,000

- Equity gained: $110,000+ from appreciation alone

Paying $12,000 in PMI to access $110,000 in equity is a 917% return on “investment.” Waiting to avoid PMI means missing that entire appreciation cycle.

Myth #3: You Can’t Buy with Student Loan Debt

Reality: 45% of first-time buyers carry student loan debt, with median balances of $30,000.

Lenders calculate debt-to-income ratio using minimum monthly payments, not total debt. A $50,000 student loan at 5% on a 20-year term costs $330/month—manageable within 43-50% DTI limits for most buyers.

Student Debt Impact Example:

Household income: $95,000

Monthly gross: $7,917

Student loan payment: $330

Car payment: $400

Credit cards (minimum): $150

Total debt: $880/month

DTI: 11.1%

Remaining DTI capacity for housing (at 43% max): $2,524/month

This supports a ~$450,000 home purchase with minimal impact from student loans.

The real strategy? Understanding how to pay off debt fast to reduce high-interest obligations before applying, freeing up more DTI for housing. Paying off credit cards ($150/month minimum) allows $150 more monthly housing payment—roughly $30,000 more buying power.

Your Next Steps to Homeownership in 2026

7-Step Action Checklist:

1. Calculate your real budget – Use our Home Affordability Calculator to determine realistic price range

2. Check your credit score – Obtain free reports from AnnualCreditReport.com and target 620+ for most programs

3. Research DPA programs – Start at DownPaymentResource.com and your state housing finance agency

4. Get pre-approved – Contact 3-5 lenders to compare rates and down payment requirements

5. Complete homebuyer education – Many DPA programs require this ($50-$100, 6-8 hours online)

6. Open high-yield savings – Start earning 4-5% on every dollar saved versus 0.01% at traditional banks

7. Connect with HUD counselor – Free expert guidance through the entire process (find counselors)

Pre-approval importance: Getting pre-approved reveals your actual buying power and down payment needs based on your specific financial situation—often showing you need 40-60% less than assumed. Our guide on mortgage pre-approval walks through documentation requirements and timeline.

Expert final word: “The biggest regret I hear from clients isn’t buying too early—it’s waiting too long,” says Jennifer Nguyen, senior housing counselor at NeighborWorks America. “First-time buyers spending three years saving 20% down miss out on equity building, price appreciation, and tax benefits. Meanwhile their rent increases annually with zero return. The ‘perfect’ down payment is the one that gets you into homeownership while maintaining financial stability.”

For comprehensive guidance on the entire first-time homebuyer process, including timeline, costs, and common mistakes, see our complete first-time home buyer guide.

Frequently Asked Questions

1. What is the minimum down payment for a house in 2026?

The minimum down payment is 0% for VA and USDA loans, 3% for conventional loans, and 3.5% for FHA loans with credit scores above 580.

2. Do I really need 20% down to buy a home?

No. Only 8% of first-time buyers put 20% down. The median first-time buyer puts down 10%, with many successful buyers using 3-5% down payment programs.

3. What is down payment assistance and who qualifies?

Down payment assistance provides grants, forgivable loans, or deferred payment help averaging $10,000-$18,000. Most programs serve households earning up to 120-140% of area median income who haven’t owned homes in 3 years.

4. How much down payment do first-time buyers actually put down?

The median down payment for first-time buyers in 2026 is 10% ($41,520 on the median $415,200 home), the highest level since 1989 but still half the mythical 20% threshold.

5. Can I use gift money for my down payment?

Yes. All major loan types allow gift funds from family members to cover part or all of your down payment with proper documentation through a gift letter and paper trail.

6. What is PMI and how do I avoid it?

Private Mortgage Insurance costs 0.5-1.5% of the loan amount annually on conventional loans below 20% down. It automatically cancels at 20% equity. Only way to avoid: 20% down, piggyback loans, or lender-paid PMI (higher rate trade-off).

7. How long does it take to save for a down payment?

Saving $20,000 (5% on $400K home) takes 20 months at $1,000/month, 40 months at $500/month. High-yield savings at 4.5% APY accelerates this by earning $800-$1,600 in interest depending on timeline.

8. Can I buy a house with bad credit?

Yes, but with limitations. FHA loans accept credit scores as low as 500 (with 10% down) or 580 (with 3.5% down). Conventional loans typically require 620+. VA loans have no minimum score requirement set by the VA, though individual lenders set their own thresholds (usually 580-620).

9. What’s the difference between down payment and closing costs?

Down payment goes toward the purchase price and builds immediate equity. Closing costs (2-5% of purchase price) cover loan origination, appraisal, title insurance, and other transaction fees—these don’t build equity.

10. Are there $0 down payment loans available in 2026?

Yes. VA loans (for veterans/military) and USDA loans (for eligible rural/suburban properties) require $0 down payment. Some state housing finance agencies also offer 0% down programs for first-time buyers.

11. How do I find down payment assistance programs near me?

Start with DownPaymentResource.com, your state housing finance agency, and HUD-approved housing counselors. Many city and county governments also offer local programs.

Disclaimer

This article is for educational purposes and does not constitute financial advice. Down payment requirements, assistance programs, mortgage rates, and lending terms vary by lender, location, program availability, and individual financial circumstances. Program eligibility, income limits, and assistance amounts are subject to change. Consult with a licensed mortgage professional, HUD-certified housing counselor, or financial advisor to evaluate your specific situation before making homebuying decisions. All statistics and figures cited reflect data available as of February 2026 and may change over time.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.