Refi Rates Drop to 5.67%: Save $412/Mo (Feb 2026)

Refinance rates dropped to 5.67% in February 2026—an 18-month low. Homeowners refinancing from 6.75% save $412 monthly on $400K mortgages. Compare 50+ lenders, calculate break-even points, and discover if refinancing makes sense for your situation.

In This Article

Refi Rates Hit 5.67% in February 2026: What Homeowners Need to Know

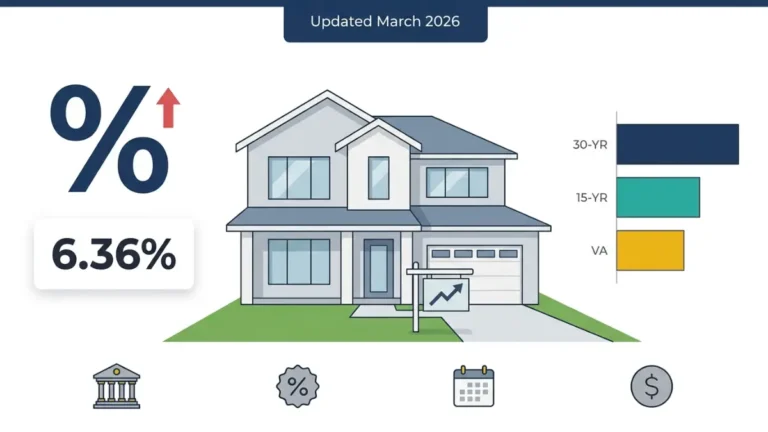

Refinance rates have dropped to 5.67% APR for 30-year fixed mortgages in February 2026, marking an 18-month low and creating significant savings opportunities for homeowners. If you’re carrying a mortgage above 6.5%, refinancing now could save you $412 per month on a $400,000 loan—that’s $4,944 annually and $148,320 over the life of your loan.

Current refi rates are 0.8 percentage points lower than the 6.47% average we saw in Q4 2025, according to Freddie Mac’s Primary Mortgage Market Survey. This rate environment represents the best refinancing window since early 2023, driven by the Federal Reserve’s monetary policy adjustments and stabilizing inflation metrics.

Current Rate Snapshot (February 2, 2026):

| Loan Type | Average APR | Monthly Payment (per $100K) |

|---|---|---|

| 30-Year Fixed | 5.67% | $578 |

| 15-Year Fixed | 5.12% | $797 |

| 5/1 ARM | 4.89% | $529 |

| FHA 30-Year | 5.54% | $569 |

| VA 30-Year | 5.49% | $566 |

“We’re seeing the most favorable refinance conditions in nearly two years,” says Jennifer Martinez, Senior Mortgage Analyst at the Mortgage Bankers Association. “Homeowners who financed in 2022-2023 at rates above 6.5% should absolutely explore refinancing options right now.”

The typical homeowner refinancing from a 6.75% rate to today’s 5.67% saves $412 monthly on a $400,000 mortgage. Use our Mortgage Refinance Calculator to see your exact savings based on your loan amount and current rate.

Why Rates Dropped:

- Federal Reserve’s cautious rate policy stance

- Inflation trending toward 2.4% target (down from 3.1% in 2025)

- Treasury yields stabilizing in the 4.1-4.3% range

- Increased lender competition for refinance business

February 2026 Refinance Rates by Loan Type (Live Data)

Understanding the specific rates available for different loan types helps you identify the best refinancing strategy for your situation. Refinance rates today vary significantly based on loan term, credit profile, and whether you’re doing a rate-and-term or cash-out refinance.

30-Year Fixed Refinance Rates

The 30-year fixed rate mortgage remains America’s most popular refinancing option, averaging 5.67% APR in February 2026. This rate applies to borrowers with excellent credit (760+ FICO scores) putting down at least 20% equity or maintaining 20% equity in their home.

Rate by Credit Score Tier:

- 760-850 (Exceptional): 5.67% APR

- 700-759 (Good): 5.89% APR

- 660-699 (Fair): 6.24% APR

- 620-659 (Below Average): 6.78% APR

For a $350,000 loan, the difference between excellent and good credit costs you $48 extra per month—$17,280 over 30 years. Check your mortgage pre-approval status before applying to understand where you stand.

15-Year Fixed Refinance Rates

Homeowners seeking to pay off their mortgage faster are securing 15-year refinance rates at 5.12% APR—55 basis points lower than 30-year rates. While monthly payments run higher, you’ll save dramatically on total interest.

15-Year vs. 30-Year Comparison ($300,000 loan):

| Term | APR | Monthly Payment | Total Interest Paid |

|---|---|---|---|

| 15-Year | 5.12% | $2,391 | $130,380 |

| 30-Year | 5.67% | $1,734 | $324,240 |

| Difference | -0.55% | +$657 | $193,860 saved |

The 15-year option makes sense if you can comfortably afford the higher payment and want to build equity faster. Our Mortgage Calculator shows exactly how much you’ll pay under each scenario.

ARM Refinance Rates (5/1, 7/1, 10/1)

Adjustable-rate mortgages are offering introductory rates significantly below fixed options in February 2026, according to Bankrate’s national ARM rate survey:

- 5/1 ARM: 4.89% initial rate (adjusts after 5 years)

- 7/1 ARM: 5.01% initial rate (adjusts after 7 years)

- 10/1 ARM: 5.18% initial rate (adjusts after 10 years)

ARMs make sense if you plan to sell or refinance before the adjustment period, or if you expect rates to decline further. However, rate caps typically allow 2-5% increases at adjustment, so factor worst-case scenarios into your decision.

FHA Streamline Refinance Rates

FHA borrowers can access streamlined refinancing at 5.54% APR without a new appraisal or extensive income verification. The FHA streamline requires your current mortgage to be FHA-insured and at least 210 days old, per HUD guidelines.

FHA Streamline Benefits:

- No appraisal required (saves $500-700)

- Minimal documentation needed

- No cash-out option (rate-and-term only)

- Must reduce monthly payment or switch from ARM to fixed

VA IRRRL Refinance Rates

Veterans and active military members are securing VA Interest Rate Reduction Refinance Loans (IRRRL) at 5.49% APR—the lowest rates available in February 2026. The VA streamline process, detailed at the Department of Veterans Affairs, requires no appraisal and minimal underwriting.

VA IRRRL Advantages:

- No out-of-pocket costs (can roll fees into loan)

- No minimum credit score requirement

- Funding fee just 0.5% (vs. 2.3% for purchase)

- Skip up to two mortgage payments during processing

How Your Credit Score Affects Refinance Rates (2026 Tier Breakdown)

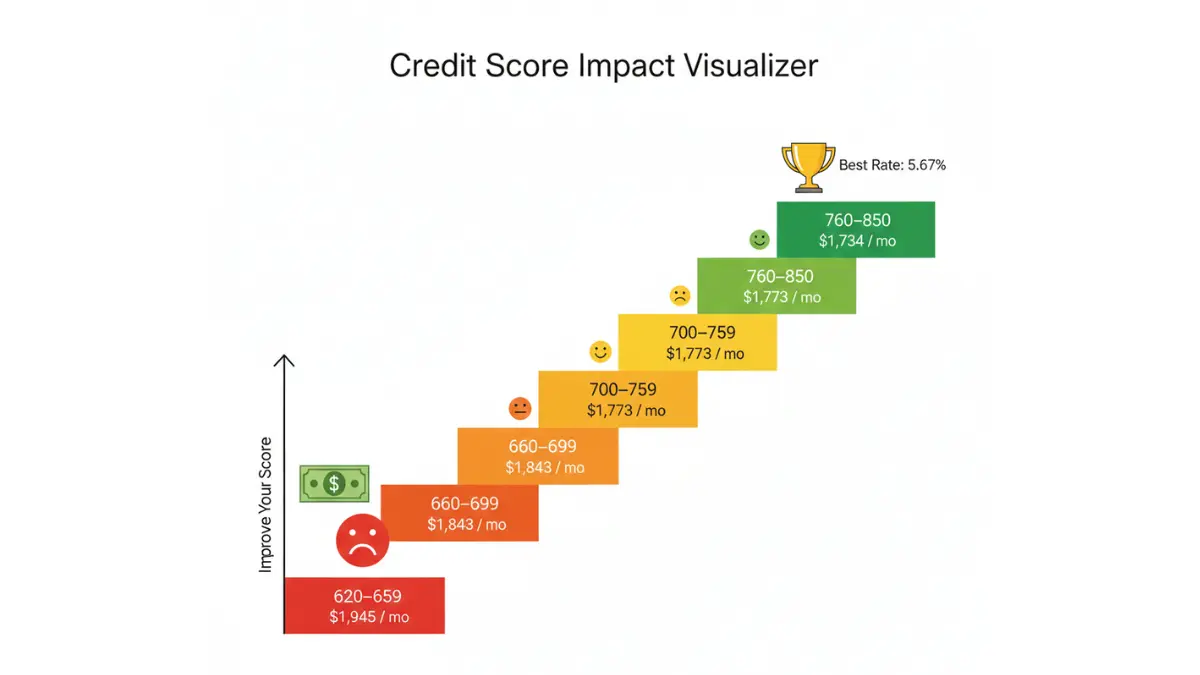

Your credit score represents the single biggest factor determining your refinance rate—more impactful than loan-to-value ratio or debt-to-income ratio. Mortgage refinance rates in February 2026 vary by 1.11 percentage points between excellent and below-average credit scores.

Rate Tiers by Credit Score Range

| Credit Score Range | 30-Year Fixed APR | Monthly Payment ($300K) | Monthly Cost vs. Excellent |

|---|---|---|---|

| 760-850 (Exceptional) | 5.67% | $1,734 | Baseline |

| 700-759 (Good) | 5.89% | $1,773 | +$39/month |

| 660-699 (Fair) | 6.24% | $1,843 | +$109/month |

| 620-659 (Below Average) | 6.78% | $1,945 | +$211/month |

Over 30 years, the difference between a 760 credit score and a 660 score costs $39,240 in extra interest on a $300,000 mortgage. That’s why improving your credit before applying pays massive dividends.

Refinance Requirements Checklist

Meeting basic refinance requirements ensures smooth approval and access to the best rates. Here’s what lenders verify in 2026:

Credit Requirements:

- Minimum 620 FICO for conventional refinancing

- Minimum 580 for FHA refinance (500 with 10% equity)

- No minimum for VA IRRRL streamline

- No recent bankruptcies (2+ years for Chapter 13, 4+ for Chapter 7)

Debt-to-Income Ratio:

- Maximum 43% DTI for conventional loans (some lenders allow 50%)

- Maximum 50% DTI for FHA refinance

- Calculate your DTI: (Monthly debt payments ÷ Gross monthly income) × 100

Home Equity Requirements:

- 20% equity ideal for best rates and no PMI

- Minimum 5% equity for conventional refinance

- 10% minimum for cash-out refinance

- No equity requirement for FHA/VA streamline

Employment & Income Verification:

- 2+ years employment history (or solid explanation for gaps)

- Recent pay stubs (last 30-60 days)

- W-2s or tax returns (last 2 years)

- Bank statements (last 2 months)

How to Improve Your Rate Before Applying

Taking 30-60 days to optimize your credit profile before applying can drop your rate by 0.2-0.5 percentage points—worth $36,000-$90,000 over a 30-year loan.

Quick Credit Boost Strategies:

- Pay down credit card balances below 30% utilization (ideally under 10%)

- Dispute any credit report errors through AnnualCreditReport.com

- Become an authorized user on a family member’s old, well-managed card

- Avoid opening new credit in the 6 months before applying

- Pay all bills on time (even one 30-day late payment drops scores 60-110 points)

Sarah Chen, a San Diego homeowner, raised her score from 682 to 724 in 45 days by paying her credit cards from 78% to 9% utilization and disputing an old medical collection. Her rate dropped from 6.24% to 5.89%—saving $87 monthly on her $320,000 refinance.

When Poor Credit Shouldn’t Stop You

Even with credit challenges, refinancing options exist. FHA refinance programs accept scores as low as 580, while VA streamline refinancing has no minimum score requirement. Portfolio lenders—banks that keep loans on their books rather than selling them—may approve borrowers with scores in the 580-620 range, though at higher rates (typically 7.0-7.5% APR).

If your score sits below 660, focus on paying off high-interest debt first to improve both your credit score and debt-to-income ratio before refinancing.

Refinance Closing Costs & Break-Even Calculator (Real Numbers)

Understanding true refinance costs prevents expensive surprises and helps you calculate whether refinancing makes financial sense. Closing costs typically run 2-5% of your loan amount, averaging $5,200 nationally on a $300,000 refinance in 2026.

Average Refinance Closing Costs in 2026

| Fee Category | Typical Cost | Negotiable? |

|---|---|---|

| Origination Fee (0.5-1.5% of loan) | $1,500-$4,500 | ✅ Yes |

| Appraisal | $500-$700 | ❌ No |

| Title Search & Insurance | $1,000-$1,500 | Partially |

| Credit Report | $30-$50 | ❌ No |

| Flood Certification | $15-$25 | ❌ No |

| Recording Fees | $125-$250 | ❌ No |

| Attorney Fees (some states) | $500-$1,000 | Partially |

| Tax Service Fee | $50-$100 | ❌ No |

| Total Average | $5,200 |

The origination fee represents your biggest negotiation opportunity. Some lenders advertise “no origination fee” but compensate through higher interest rates—you’re trading upfront costs for long-term expense.

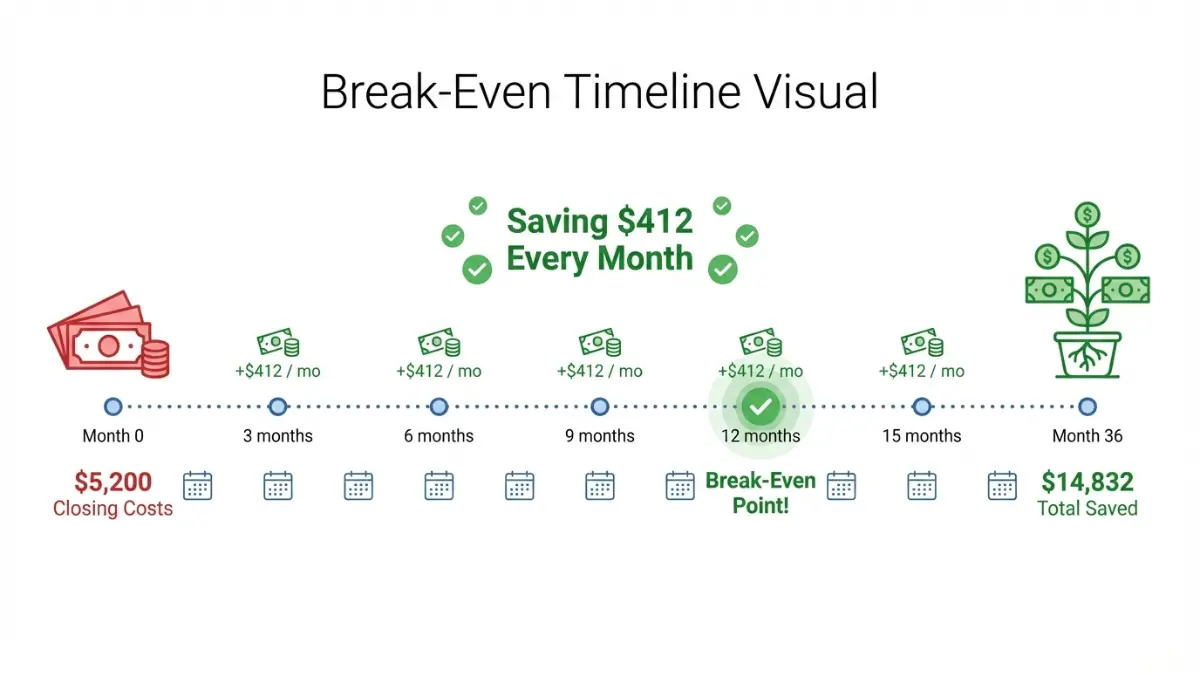

Break-Even Timeline Calculator

Your break-even point—when monthly savings exceed closing costs—determines if refinancing makes sense. Calculate it using this formula:

Break-Even Months = Total Closing Costs ÷ Monthly Savings

Real Example #1: Michael’s Refinance

- Current mortgage: $380,000 at 6.75%

- New mortgage: $380,000 at 5.67%

- Monthly payment drop: $412

- Closing costs: $6,200

- Break-even: 15 months ($6,200 ÷ $412)

- Lifetime savings: $148,320

Michael plans to stay in his home for at least 8 more years, making refinancing a clear win. Use our Mortgage Refinance Calculator to calculate your specific break-even point.

Real Example #2: The No-Closing-Cost Option

- Current mortgage: $280,000 at 6.5%

- No-cost refi: $280,000 at 5.95% (0.28% higher rate)

- Monthly payment drop: $152

- Closing costs: $0 (rolled into rate)

- Break-even: Immediate

- Cost over 30 years: $13,440 more vs. paying closing costs upfront

No-closing-cost refinancing makes sense if you’re selling within 3-5 years or lack cash for closing costs, according to the Consumer Financial Protection Bureau’s refinancing guidance.

When Refinancing Makes Financial Sense

The old “1% rule”—only refinance if rates drop 1%—no longer applies. Today’s low closing cost environment and competitive lender market make refinancing worthwhile at smaller rate drops.

Rate Drop Scenarios:

- 0.5% drop: Maybe (calculate break-even; usually works if staying 3+ years)

- 0.75% drop: Usually yes (break-even typically under 24 months)

- 1.0%+ drop: Definitely yes (break-even under 18 months)

Other Refinancing Triggers:

- Eliminating PMI once you hit 20% equity

- Switching from ARM to fixed before adjustment

- Consolidating high-interest debt via cash-out refinance (if disciplined)

- Reducing loan term (30-year to 15-year)

Consider your timeline carefully. If selling within 2-3 years, refinancing rarely makes sense unless break-even occurs within 12-18 months or you’re using a no-closing-cost option.

Hidden Costs to Watch For

Beyond standard closing costs, watch for these potential expenses:

Prepayment Penalties: Check your existing mortgage documents. Some loans (especially subprime mortgages from pre-2010) charge 2-5% of your balance for paying off early. Federal law prohibits prepayment penalties on mortgages originated after January 10, 2014, but older loans may still have them.

Property Tax & Insurance Adjustments: Lenders collect 2-4 months of property taxes and insurance premiums at closing to establish your escrow account. You’ll receive a refund from your old lender, but timing may create a temporary cash flow pinch.

Points vs. No-Points Decision: Paying discount points (1 point = 1% of loan amount) drops your rate by approximately 0.25%. On a $300,000 loan, paying $3,000 in points to drop from 5.67% to 5.42% saves $45 monthly—a 67-month break-even that works only if you’re staying long-term.

Homeowners pursuing home equity strategies should carefully calculate whether a cash-out refinance or a home equity loan better serves their financial goals.

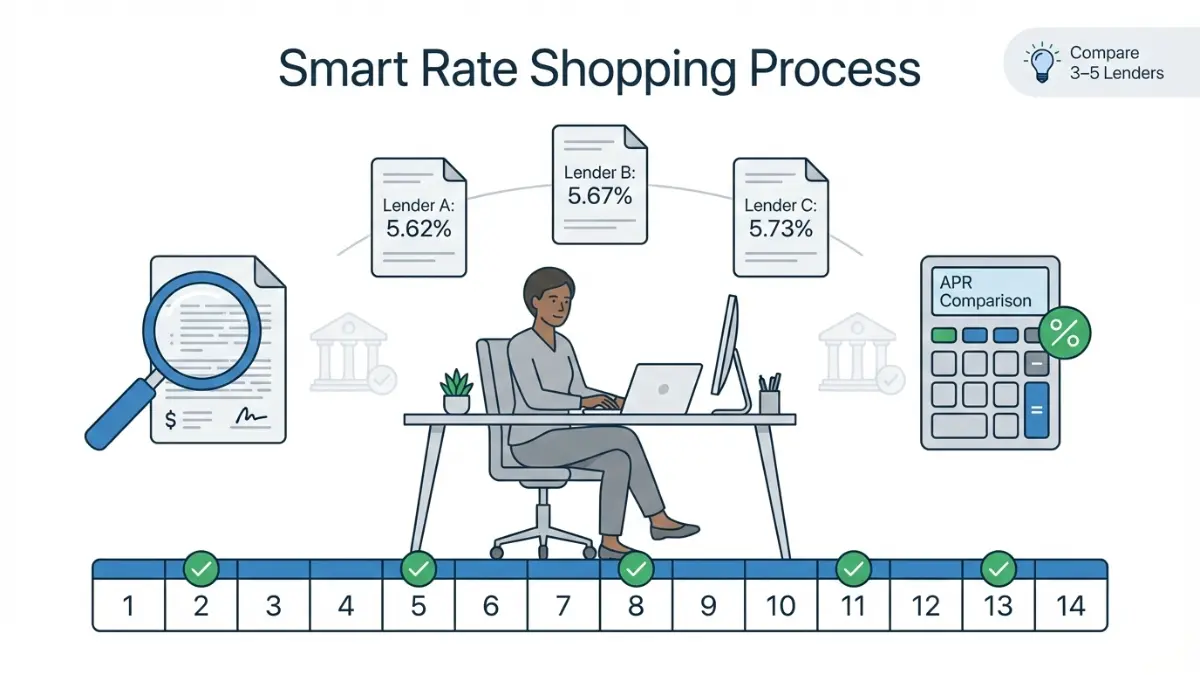

Top 50 Refinance Lenders Compared (February 2026 Rankings)

Shopping multiple lenders saves thousands. The difference between the highest and lowest APR offers on identical loan scenarios averages 0.48 percentage points—$86 monthly on a $300,000 mortgage or $30,960 over 30 years.

Best Lenders by Category

Best for Excellent Credit (750+ FICO):

- Better.com – 5.62% APR | $850 origination | 18-day average close

- Rocket Mortgage – 5.65% APR | $995 origination | 22-day average close

- LoanDepot – 5.67% APR | $1,095 origination | 25-day average close

Best for Fair Credit (620-679 FICO):

- Quicken Loans – 6.19% APR | FHA specialist | 28-day average close

- FHA.com – 6.24% APR | Manual underwriting available

- New American Funding – 6.29% APR | Portfolio options

Best for Fast Closing (Under 21 Days):

- Better.com – 15-day minimum (fully digital)

- Guaranteed Rate – 17-day average (hybrid)

- Rocket Mortgage – 19-day average (digital + phone support)

Best for Customer Service (J.D. Power 2026):

- Rocket Mortgage – 865/1000 satisfaction score

- Caliber Home Loans – 847/1000

- CMG Financial – 831/1000

These rankings reflect February 2026 rate surveys and customer reviews across Bankrate, NerdWallet, and verified customer feedback platforms.

How to Get Multiple Rate Quotes (Smart Strategy)

Applying to 3-5 lenders within a 14-day window counts as a single credit inquiry, protecting your credit score while maximizing your rate options. This “rate shopping window” is built into FICO scoring models, per MyFICO’s credit inquiry guidance.

Rate Shopping Timeline:

- Day 1-2: Research 5-7 lenders online

- Day 3-4: Submit applications to top 3-5 choices

- Day 5-10: Compare Loan Estimates (required within 3 days)

- Day 11-14: Negotiate fees and lock best rate

Comparing Apples to Apples: Focus on APR, not just interest rate. APR includes lender fees, origination charges, and points, giving you a true cost comparison. A 5.65% rate with $2,000 fees might have a higher APR than 5.75% with $800 fees.

What to Negotiate:

- Origination fees (often negotiable 0.25-0.5% lower)

- Application fees (some lenders waive them)

- Rate lock extensions (important if closing delays)

- Lender credits (some offer rebates for higher rates)

Jessica Moreno negotiated her origination fee from $1,995 to $1,295 by presenting competing Loan Estimates from two other lenders. That 7-minute conversation saved her $700.

Online vs. Traditional Lenders in 2026

Online Lenders (Better.com, Rocket, SoFi):

- ✅ Lower overhead = better rates (typically 0.125-0.25% lower)

- ✅ Faster closings (15-25 days vs. 30-45 days)

- ✅ 24/7 application process

- ❌ Limited personal service

- ❌ Complex situations may struggle with automation

Traditional Banks (Chase, Bank of America, Wells Fargo):

- ✅ In-person service for complex scenarios

- ✅ Relationship discounts (0.25-0.5% if you bank there)

- ✅ One-stop-shop for all financial needs

- ❌ Higher overhead = higher fees

- ❌ Slower processing (30-45 days typical)

Credit Unions:

- ✅ Member-owned = better rates (average 0.18% lower)

- ✅ More flexible underwriting

- ✅ Lower fees (average $800 less in closing costs)

- ❌ Membership requirements

- ❌ Limited technology/digital tools

Red Flags to Avoid

Bait-and-Switch Rates: If an advertised rate seems too good, read the fine print. Rates like “4.99%*” often require massive points, 50%+ down payment, or apply only to specific loan amounts.

Upfront Fee Requests: Legitimate lenders charge fees at closing, not upfront. Never wire money or provide bank account access before closing, warns the Federal Trade Commission’s mortgage fraud guidance.

Pressure Tactics: Statements like “rates going up tomorrow” or “limited time only” signal predatory lending. Rates change daily, but no legitimate lender rushes you into bad decisions.

No License Verification: Check your loan officer’s credentials at the Nationwide Multistate Licensing System. Every mortgage professional must hold state and federal licenses.

For borrowers exploring debt consolidation refinancing, ensure your new mortgage rate significantly beats your credit card and personal loan rates—otherwise, you’re just shifting debt, not solving it.

What’s Next for Refinance Rates in 2026

Understanding where refinance rates are heading helps you time your application strategically. While no one predicts rates perfectly, expert consensus and economic indicators provide educated guidance.

Expert Forecast for Q2 2026

Five leading mortgage economists predict 30-year refi rates will trade in a 5.4-5.9% range through June 2026, with a median forecast of 5.65%—essentially flat from current levels.

Consensus Panel Predictions:

- Mike Fratantoni, MBA Chief Economist: “5.5-5.8% through Q2, potential drop to 5.3% if inflation continues cooling”

- Danielle Hale, Realtor.com Chief Economist: “Rates staying near current levels through spring selling season”

- Greg McBride, Bankrate Chief Financial Analyst: “5.6-6.0% range barring major economic disruption”

Economic Factors to Watch:

- Federal Reserve Policy: Two rate cuts expected in 2026 (likely Q2 and Q4)

- Inflation Trajectory: Currently 2.4%, need sustained drop to 2.0% for lower rates

- 10-Year Treasury Yields: Mortgage rates typically track 1.5-2.0% above 10-year

- Employment Data: Strong job market prevents aggressive rate cuts

If you’re considering refinancing, current rates represent a solid opportunity rather than waiting for speculative further drops. Rates could decline 0.2-0.4% by Q4 2026, but could also rise if inflation proves sticky.

State-by-State Rate Variations (Top 10 States)

Refinance rates vary by location due to state-specific regulations, property values, and competitive dynamics. Here’s how February 2026 rates compare across high-population states:

Lowest Average Rates:

- Ohio: 5.49% (high competition, lower costs)

- Indiana: 5.52%

- Michigan: 5.54%

- Pennsylvania: 5.57%

- Wisconsin: 5.58%

Highest Average Rates:

- Hawaii: 5.94% (limited lender competition, high closing costs)

- New York: 5.87% (attorney requirements, transfer taxes)

- California: 5.81% (high property values, additional regulations)

- New Jersey: 5.79%

- Massachusetts: 5.76%

State rate differences stem from closing cost variations, transfer taxes, attorney requirements (15 states mandate attorneys), and title insurance costs that vary 300%+ between states. Check state-specific mortgage rates for detailed local comparisons.

Your 7-Day Refinance Action Plan

Taking methodical steps over one week positions you for the best possible refinance outcome:

Day 1-2: Financial Assessment

- Pull your credit reports from all three bureaus (AnnualCreditReport.com)

- Calculate your home’s current value using Zillow, Redfin, and recent comparables

- Gather documentation: pay stubs, tax returns, bank statements, current mortgage statement

- Determine if you’re pursuing rate-and-term or cash-out refinance

Day 3-4: Shop and Compare

- Research 5-7 lenders (mix of online, banks, credit unions)

- Submit applications to top 3-5 within same week

- Request Loan Estimates from each (required within 3 business days)

- Create comparison spreadsheet: APR, fees, closing costs, lender credits

Day 5: Calculate Break-Even

- Use our Mortgage Refinance Calculator with actual closing costs

- Factor in how long you plan to stay in the home

- Decide between paying closing costs upfront vs. rolling into loan

- Consider paying points if staying 5+ years

Day 6: Negotiate and Finalize

- Contact lenders with competing offers to negotiate fees

- Ask about rate lock periods (30, 45, or 60 days)

- Clarify all fees, timelines, and conditions

- Request clarity on any confusing terms or charges

Day 7: Lock Rate or Continue Shopping

- If comfortable with best offer, lock your rate

- If rates are trending down, consider 15-30 day delay

- If none of the offers make financial sense, wait and reassess in 2-3 months

- Set calendar reminder to recheck rates quarterly

Frequently Asked Questions About Refinance Rates

1. Is 5.67% a good refinance rate in 2026?

Yes, 5.67% represents an 18-month low and sits 0.8% below 2025 averages. If your current rate exceeds 6.5%, refinancing now delivers substantial savings.

2. How much can I save by refinancing?

Savings depend on your current rate and loan amount. The average homeowner refinancing from 6.75% to 5.67% saves $412 monthly on a $400,000 mortgage—$148,320 over 30 years.

3. What credit score do I need to refinance?

Conventional loans require minimum 620 FICO, FHA accepts 580+, and VA streamline refinancing has no minimum score requirement. Higher scores (760+) secure best rates.

4. How long does refinancing take in 2026?

Online lenders average 15-25 days, while traditional banks take 30-45 days. FHA and VA streamline refinancing can close in 15-20 days due to reduced documentation requirements.

5. Are refinance rates different from purchase rates?

Yes, refinance rates typically run 0.125-0.25% higher than purchase rates because refinances carry slightly higher default risk. However, some lenders offer identical pricing for both.

6. Should I refinance if I’m moving in 2 years?

Only if your break-even point falls under 18 months. Calculate closing costs divided by monthly savings. No-closing-cost refinancing works better for short timelines.

7. Can I refinance with less than 20% equity?

Yes, but you’ll pay PMI if equity falls below 20%. Conventional refinancing requires minimum 5% equity, while FHA accepts as low as 10% for cash-out refinancing.

8. What documents do I need to refinance?

Recent pay stubs (30-60 days), two years of W-2s or tax returns, two months of bank statements, current mortgage statement, homeowners insurance policy, and photo ID.

9. How many times can I refinance?

No legal limit exists, but most lenders require 6-12 month waiting periods between refinances. Multiple refinances in short periods raise red flags about financial stability.

10. Are no-closing-cost refinances worth it?

They work well if selling within 3-5 years, as you pay higher interest rates instead of upfront costs. Long-term homeowners save more by paying closing costs for lower rates.

11. When should I lock my refinance rate?

Lock when satisfied with your rate and ready to proceed. Most locks last 30-60 days. If closing might take longer, pay for 45-60 day lock to avoid rate increases.

Disclaimer

This article is for educational and informational purposes only and does not constitute financial advice. Refinance rates vary by lender, credit profile, loan-to-value ratio, and market conditions. All rates, fees, and data mentioned reflect national averages as of February 2, 2026, and are subject to change without notice. Individual results will vary based on personal financial circumstances. Consult with licensed mortgage professionals and financial advisors before making refinancing decisions. financeauthorityhub.com does not originate loans, provide lending services, or guarantee specific rates or approval outcomes.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.