Conventional Loan 2026: $833K Max, 3% Down, 620 Score

Discover how to qualify for a conventional loan in 2026 with updated $832,750 limits, 3% minimum down payment, and 620 credit score floor. Compare conventional vs FHA/VA loans.

In This Article

What Is a Conventional Loan? (2026 Fast Facts)

A conventional loan is a mortgage not backed by any government agency, making it the most popular home financing option in the United States. Unlike FHA, VA, or USDA loans, conventional mortgages are offered by private lenders and follow guidelines set by Fannie Mae and Freddie Mac.

The 2026 game-changer: The Federal Housing Finance Agency (FHFA) increased the conforming loan limit to $832,750 for most U.S. counties—a $26,250 jump from 2025. This 3.26% increase means you can now borrow more while keeping the benefits of conforming loan rates and terms.

Here’s what makes conventional loans attractive in 2026:

- Minimum down payment: Just 3% for qualified first-time buyers

- Credit score floor: 620 minimum (but 740+ gets best rates)

- Loan limits: Up to $832,750 in standard-cost areas, $1,249,125 in high-cost regions

- Mortgage insurance: Removable once you reach 20% equity

Quick comparison: While government-backed loans require mortgage insurance for the life of the loan (FHA) or charge funding fees (VA), conventional loans let you cancel private mortgage insurance (PMI) once you’ve built sufficient equity. This flexibility makes conventional mortgages ideal for borrowers with good credit who want long-term savings.

Use our Mortgage Calculator to estimate your monthly payments based on the 2026 loan limits and current rates.

2026 Conventional Loan Requirements: Do You Qualify?

Understanding conventional loan requirements helps you prepare for approval and secure better terms. The 2026 standards remain accessible while rewarding borrowers with stronger financial profiles.

Minimum Credit Score (620 Floor, Rate Impact by Tier)

Your credit score directly impacts both approval odds and interest rates. While 620 is the minimum threshold, your rate improves dramatically as your score increases.

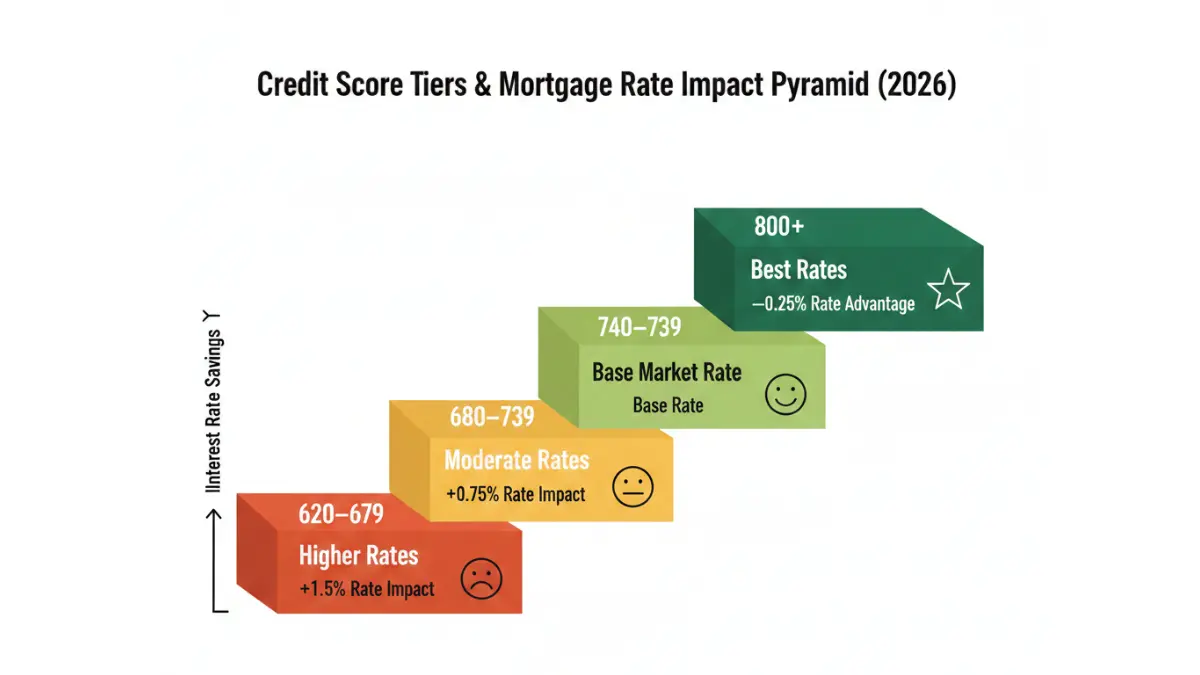

2026 Credit Score Impact Matrix:

| Credit Score Range | Rate Impact | Approval Likelihood |

|---|---|---|

| 620-679 | +1.25% to +1.75% above base | Moderate (additional scrutiny) |

| 680-739 | +0.50% to +0.75% above base | Good (standard terms) |

| 740-799 | Base rate | Excellent (best standard terms) |

| 800+ | -0.125% to -0.25% below base | Superior (premium pricing) |

Real example: On a $400,000 loan, the difference between a 680 score (6.75% rate) and a 760 score (6.00% rate) equals $179 more per month—that’s $64,440 over 30 years.

Want to improve your credit before applying? Check our Credit Score Complete Guide for proven strategies to boost your score 100+ points.

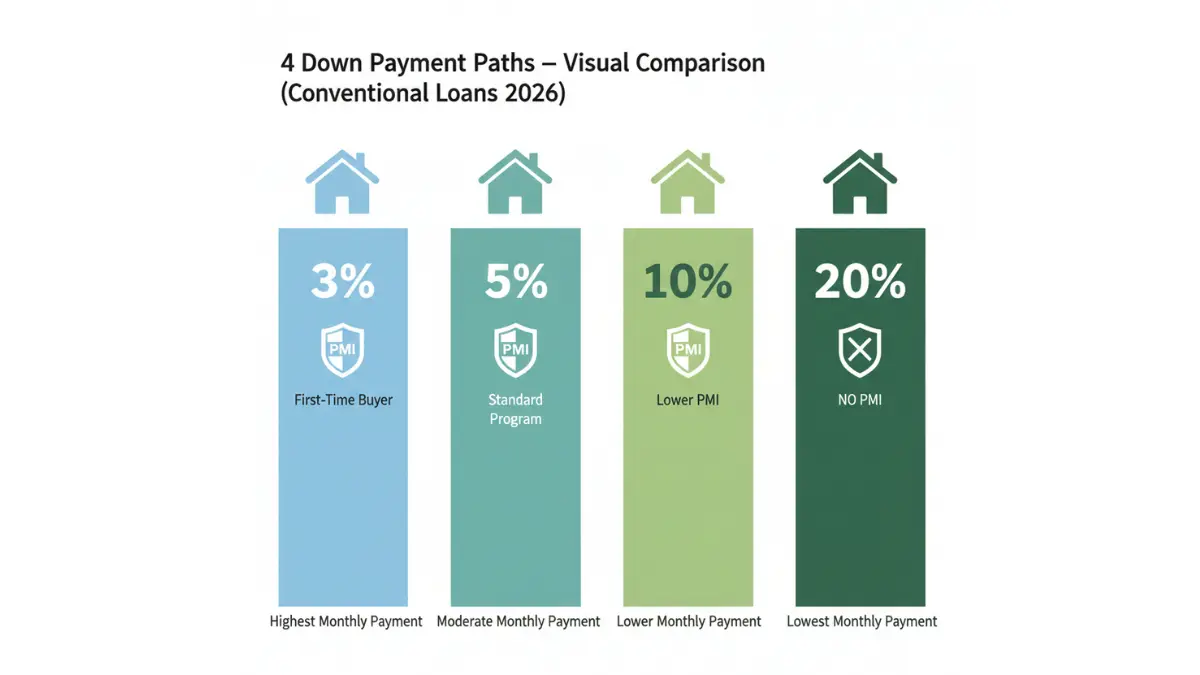

Down Payment Options (3%, 5%, 10%, 20% Scenarios)

Conventional loans offer flexibility based on your financial situation and homeownership goals.

Down Payment Breakdown:

3% Down Programs:

- Available through Fannie Mae HomeReady and Freddie Mac Home Possible

- Best for first-time buyers with good credit (typically 680+)

- Requires PMI until 20% equity

- Income limits may apply (varies by county)

5% Down (Standard Conventional):

- Most common option for non-first-time buyers

- Broader lender availability

- PMI required until 20% equity

- No income restrictions

10% Down:

- Reduces PMI costs by 30-40%

- Stronger negotiating position with sellers

- Faster path to 20% equity

20% Down (No PMI):

- Eliminates PMI completely ($100-$400/month savings)

- Best rates and terms

- Lower overall loan costs

- Immediate equity cushion

Case Study – Sarah (First-Time Buyer): Sarah purchased a $450,000 home with 5% down ($22,500). Her 685 credit score qualified her for a 6.625% rate. Monthly payment breakdown: $2,771 principal & interest + $168 PMI + $563 property tax = $3,502 total. She plans to request PMI removal once she reaches 20% equity in approximately 6 years.

Debt-to-Income Ratio Limits (36-45% Explained)

Lenders use your debt-to-income (DTI) ratio to assess whether you can afford monthly mortgage payments alongside existing obligations. According to Fannie Mae’s underwriting guidelines, conventional loans typically allow maximum DTI ratios of 36-45%, though some programs extend to 50% with compensating factors.

DTI Calculation: (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100

Example:

- Gross monthly income: $7,000

- Existing debts: $800 (car loan) + $200 (student loans) + $150 (credit cards) = $1,150

- Proposed mortgage payment: $2,300

- Total debt: $3,450

- DTI: ($3,450 ÷ $7,000) × 100 = 49.3%

This borrower would need to either increase income, reduce debts, or lower the target home price to meet standard DTI requirements.

What counts in DTI:

- Car loans and leases

- Student loans

- Credit card minimum payments

- Personal loans

- Alimony or child support

- Other mortgage or rent payments

What doesn’t count:

- Utilities

- Insurance premiums (except mortgage insurance)

- Groceries and living expenses

- 401(k) contributions

Use our Home Affordability Calculator to determine your maximum loan amount based on income and existing debts.

Income & Employment Verification

Lenders verify employment stability and income consistency through documentation review. Standard requirements include:

- W-2 employees: Last 2 years of W-2 forms, recent pay stubs (30 days), employment verification

- Self-employed: 2 years of personal and business tax returns, profit/loss statements, CPA letter

- Commission-based: 2-year average of commission income, employment contracts

- Multiple income sources: Documentation for each income stream

2026 trend: More lenders now accept alternative documentation like bank statements for self-employed borrowers (typically 12-24 months of statements).

2026 Conventional Loan Limits: How Much Can You Borrow?

The FHFA’s 2026 conforming loan limits represent the maximum amount you can borrow while maintaining conforming loan status—critical for accessing the best rates and terms.

Baseline Conforming Limit ($832,750)

For most U.S. counties, the 2026 limit stands at $832,750 for single-family homes. This represents a $26,250 increase from 2025’s $806,500 limit, reflecting the 3.26% annual home price appreciation measured by FHFA’s House Price Index.

What this means: If you were pre-approved for $806,500 in late 2025, you now have an additional $26,250 in borrowing power without switching to a jumbo loan—potentially saving thousands in interest over the loan term.

Multi-unit property limits (baseline areas):

- 2-unit property: $1,066,000

- 3-unit property: $1,289,300

- 4-unit property: $1,603,200

These limits apply to owner-occupied properties where you live in one unit and rent the others—an excellent strategy for reducing housing costs. Learn more about leveraging real estate in our Home Equity 4 Ways Use guide.

High-Cost Area Limits (Up to $1.249M)

Designated high-cost areas receive elevated limits up to 150% of the baseline, reaching $1,249,125 for single-family homes. These areas have median home values significantly above the national average.

Top 15 High-Cost Counties (2026):

| County | State | 2026 Limit | 2025 Limit | Increase |

|---|---|---|---|---|

| San Francisco | CA | $1,209,750 | $1,171,950 | $37,800 |

| San Mateo | CA | $1,209,750 | $1,171,950 | $37,800 |

| Marin | CA | $1,209,750 | $1,171,950 | $37,800 |

| Orange County | CA | $1,209,750 | $1,171,950 | $37,800 |

| Santa Clara | CA | $1,209,750 | $1,171,950 | $37,800 |

| Honolulu | HI | $1,209,750 | $1,171,950 | $37,800 |

| Maui | HI | $1,209,750 | $1,171,950 | $37,800 |

| New York | NY | $1,050,500 | $1,017,750 | $32,750 |

| Kings (Brooklyn) | NY | $1,050,500 | $1,017,750 | $32,750 |

| Queens | NY | $1,050,500 | $1,017,750 | $32,750 |

| Boulder | CO | $958,500 | $928,500 | $30,000 |

| Eagle | CO | $958,500 | $928,500 | $30,000 |

| Summit | CO | $958,500 | $928,500 | $30,000 |

| Washington | DC | $1,050,500 | $1,017,750 | $32,750 |

| Arlington | VA | $1,050,500 | $1,017,750 | $32,750 |

Check your specific county limit using the FHFA loan limit lookup tool.

Jumbo loan threshold: Any loan exceeding your county’s conforming limit becomes a jumbo loan, typically requiring:

- Minimum 10-20% down payment

- Credit scores of 700-720+

- Lower DTI ratios (typically 43% maximum)

- Larger cash reserves (6-12 months)

- Higher interest rates (0.25%-0.75% above conforming rates)

Understanding PMI: Costs, Removal & Strategies

Private mortgage insurance (PMI) protects lenders against default risk when borrowers put down less than 20%. While PMI increases monthly costs, it enables homeownership with smaller down payments—and it’s removable.

What Is PMI and How Much Does It Cost?

PMI typically costs between 0.5% and 1.5% of the original loan amount annually, paid in monthly installments. Your exact rate depends on credit score, down payment amount, and loan type.

PMI Cost Examples:

$350,000 Home Purchase:

- Loan amount (5% down): $332,500

- PMI at 0.75% annually: $2,494 per year = $208/month

- PMI at 1.0% annually: $3,325 per year = $277/month

$500,000 Home Purchase:

- Loan amount (10% down): $450,000

- PMI at 0.6% annually: $2,700 per year = $225/month

- PMI at 0.85% annually: $3,825 per year = $319/month

PMI cost factors:

- Credit score: 760+ pays 40-50% less than 680 score

- Down payment: 10% down pays 30-40% less than 5% down

- Loan type: Fixed-rate typically costs less than adjustable-rate

- Property type: Single-family homes cost less than condos or multi-units

According to the Consumer Financial Protection Bureau, PMI typically ranges from $30 to $70 per month for every $100,000 borrowed.

4 Ways to Remove PMI Before Schedule

You don’t have to wait years to eliminate PMI. Strategic approaches can save thousands in unnecessary insurance premiums.

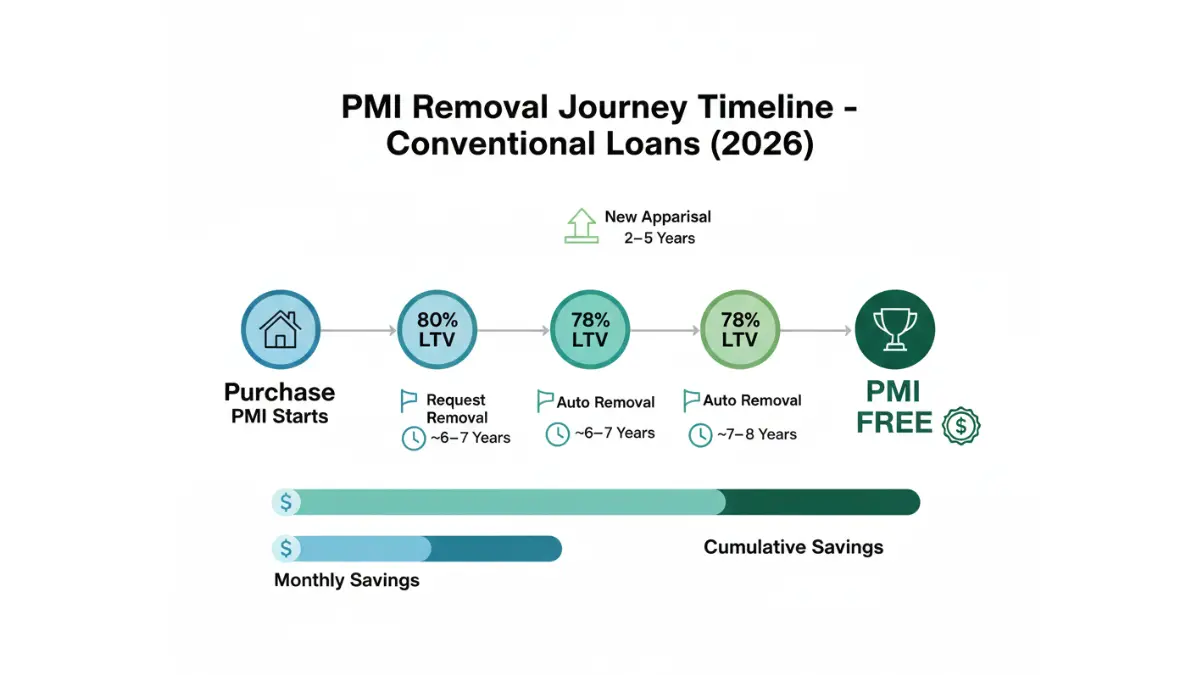

Method 1: Request Removal at 80% LTV

Once your loan balance reaches 80% of the home’s original value (20% equity), you can formally request PMI cancellation. Requirements:

- Written request to loan servicer

- Current on all payments (no 30+ day lates in past year)

- No subordinate liens (second mortgages or HELOCs)

- Verification that property value hasn’t declined

Timeline example: $400,000 home with 5% down ($380,000 loan). You’ll reach 80% LTV ($320,000 balance) after making approximately 84 monthly payments—about 7 years with standard amortization.

Method 2: Automatic Removal at 78% LTV

Federal law requires automatic PMI termination when your loan balance reaches 78% of the original property value, regardless of whether you request it. This happens at the loan’s midpoint (15 years for 30-year mortgages) if you haven’t reached 78% LTV through regular payments.

Method 3: Home Appreciation + New Appraisal

If your home value increases significantly, you may reach 20% equity faster than scheduled. Requirements:

- Typically 2-5 years of ownership (lender-specific)

- Professional appraisal ($400-$600 cost)

- Current loan balance must be ≤75-80% of new appraised value

- Excellent payment history

Real scenario: Maria bought a $380,000 home in 2023 with 5% down. By 2026, comparable homes sold for $445,000. Her new appraisal came in at $440,000, giving her 23% equity ($361,000 loan ÷ $440,000 value = 82% LTV). She requested and received PMI removal, saving $245/month.

Method 4: Refinance with 20% Equity

If interest rates drop or your home appreciates substantially, refinancing into a new loan with 20%+ equity eliminates PMI. Use our Mortgage Refinance Calculator to determine if refinancing makes financial sense after accounting for closing costs.

Break-even analysis: If refinancing costs $4,500 and saves $280/month (rate reduction + PMI elimination), you break even in 16 months. Any time beyond that represents pure savings.

PMI Removal Timeline (Automatic vs Requested)

Understanding the timeline helps you plan strategically and avoid paying PMI longer than necessary.

PMI Removal Timeline Table:

| Equity Level | Action Required | Typical Timeframe | Key Considerations |

|---|---|---|---|

| 20% (80% LTV) | You must request in writing | Varies by payment amount | Fastest removal method; requires proactive action |

| 22% (78% LTV) | Automatic by lender | ~7-8 years with regular payments | No action needed; happens automatically |

| Midpoint | Automatic by lender | 15 years on 30-year loan | Safety net if 78% not reached |

| New appraisal | You must request + pay for appraisal | 2-5+ years ownership required | Best for appreciating markets |

Pro tip: Make extra principal payments to reach 80% LTV faster. Even $100-$200 extra monthly can shave 1-2 years off PMI payments, saving $3,000-$6,000 total.

For more strategies on managing housing costs, see our Lowest Mortgage Rates by State comparison.

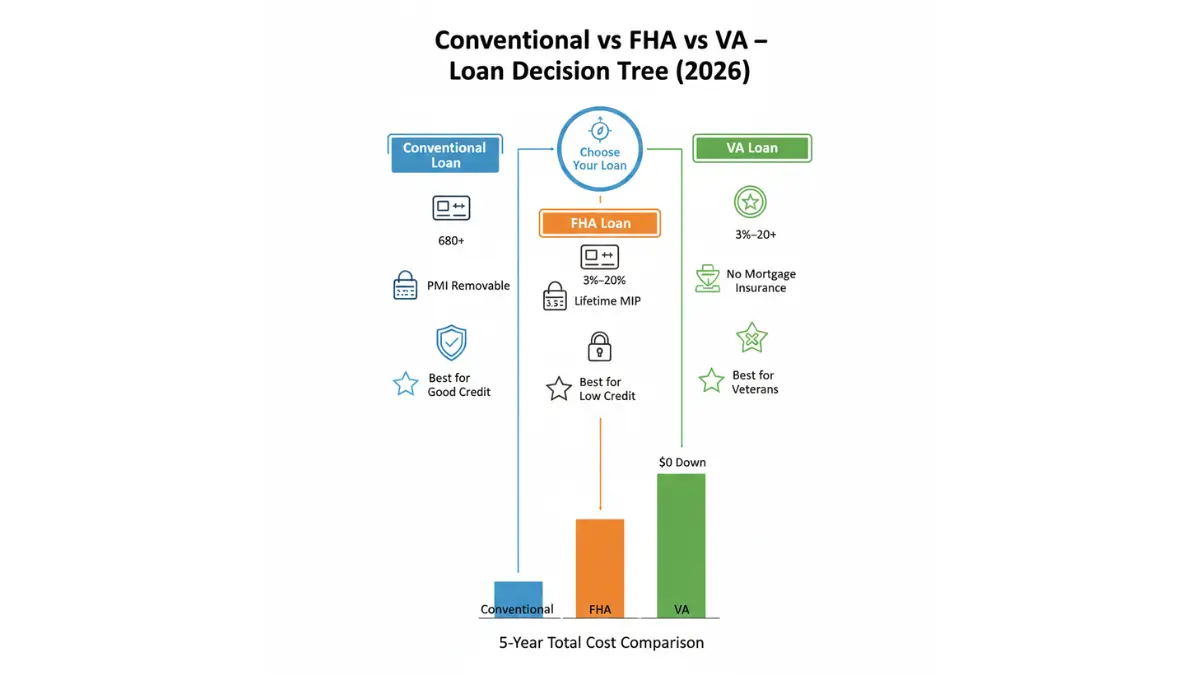

Conventional Loan vs FHA vs VA: Which Is Right for You?

Choosing between conventional, FHA, and VA loans depends on your credit profile, down payment capacity, and long-term cost analysis.

Side-by-Side Comparison (Table)

Complete Loan Type Comparison (2026):

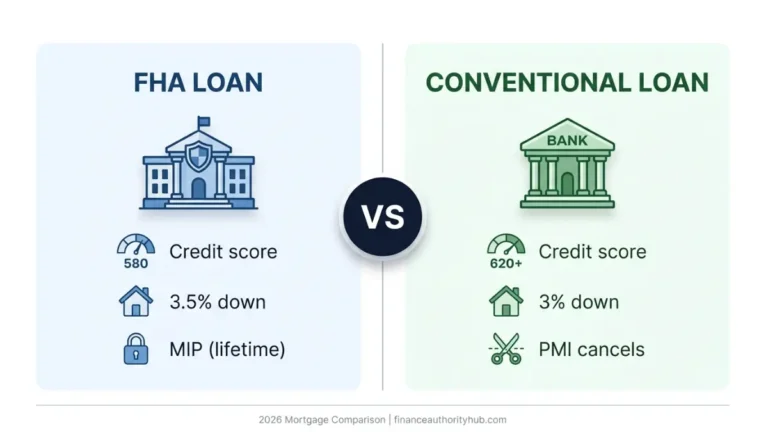

| Feature | Conventional | FHA | VA |

|---|---|---|---|

| Minimum Credit Score | 620 (740+ for best rates) | 580 (500 with 10% down) | No official minimum |

| Minimum Down Payment | 3% (first-time buyers) | 3.5% | 0% |

| Maximum Loan Limit | $832,750 baseline | $498,257 baseline | $832,750 baseline |

| Mortgage Insurance | PMI (removable at 20% equity) | MIP (lifetime for most loans) | None (funding fee instead) |

| Upfront Costs | None | 1.75% of loan amount | 2.15-3.3% funding fee |

| Monthly Insurance | 0.5-1.5% annually | 0.55% annually (most loans) | $0 |

| Property Standards | Standard appraisal | Strict FHA appraisal | VA appraisal required |

| Best For | Good credit, want PMI removal | Lower credit, minimal down payment | Veterans, active military, eligible spouses |

| 5-Year Total Cost (on $300K) | Lowest with good credit | Higher due to lifetime MIP | Lowest overall (no insurance) |

3 Real Borrower Scenarios

Understanding how different loan types perform in real situations helps you choose wisely.

Scenario 1: Emily (First-Time Buyer, Good Credit)

Profile:

- Credit score: 705

- Annual income: $85,000

- Savings: $25,000

- Target home: $420,000

- Down payment capacity: 5% ($21,000)

Best Option: Conventional Loan

Why it wins:

- Qualifies with 705 score for competitive rates

- 5% down payment ($21,000) keeps $4,000 emergency fund

- PMI of $245/month is removable in 6-7 years

- Total monthly payment: $3,187 (principal, interest, PMI, taxes, insurance)

Long-term savings: Compared to FHA, Emily avoids lifetime MIP, saving approximately $52,000 over 30 years after PMI removal.

Scenario 2: Carlos (Lower Credit, Limited Savings)

Profile:

- Credit score: 615

- Annual income: $62,000

- Savings: $15,000

- Target home: $280,000

- Down payment capacity: 3.5% ($9,800)

Best Option: FHA Loan

Why it wins:

- 615 credit score makes conventional loan difficult/expensive

- 3.5% down payment ($9,800) leaves emergency cushion

- FHA’s flexible underwriting accommodates lower credit

- Total monthly payment: $2,145 (includes lifetime MIP)

Trade-off: Lifetime MIP costs approximately $45,000 over 30 years, but Carlos can refinance to conventional once credit improves (typically 2-3 years of on-time payments can boost scores 80+ points).

Check our Mortgage Pre Approval 2026 Guide to understand approval requirements across all loan types.

Scenario 3: Lieutenant James Rodriguez (Active Military)

Profile:

- Credit score: 735

- Annual income: $78,000

- Savings: $18,000

- Target home: $465,000

- Eligibility: Active duty Air Force

Best Option: VA Loan

Why it wins:

- Zero down payment required ($465,000 financed)

- No mortgage insurance (saves $280-$350/month)

- Competitive interest rates (often 0.25-0.5% below conventional)

- One-time funding fee: $10,255 (2.15% for first-time use, 0% down)

- Total monthly payment: $3,024 (no insurance component)

Total savings vs conventional: Approximately $68,000 over loan life (down payment not required + no PMI/MIP).

Learn about VA benefits in detail at the U.S. Department of Veterans Affairs official site.

When to Choose Conventional Over Government Loans

Conventional loans offer the best value for borrowers who can meet these criteria:

Choose conventional if you have:

- Credit score of 680+ (700+ for maximum benefits)

- Down payment of 5-20% available

- Stable employment with documented income

- DTI ratio below 43%

- Goal to eliminate mortgage insurance

5-year cost comparison ($400,000 loan):

Conventional (10% down, 720 credit):

- Down payment: $40,000

- Monthly payment years 1-5: $2,687

- PMI years 1-5: $200/month = $12,000 total

- Total 5-year cost: $173,220

FHA (3.5% down, 720 credit):

- Down payment: $14,000

- Upfront MIP (1.75%): $6,863

- Monthly payment years 1-5: $2,841

- Monthly MIP: $193/month = $11,580 total

- Total 5-year cost: $202,903

Conventional saves $29,683 over 5 years for this borrower profile, even accounting for the higher down payment.

For comparison between different mortgage term lengths, review our 15 vs 30 Year Mortgage Comparison analysis.

How to Apply for a Conventional Loan in 2026

Navigating the application process efficiently increases approval odds and helps you secure better terms.

5-Step Application Process

Step 1: Check Credit & Calculate DTI (Months 1-2 Before Application)

Pull credit reports from all three bureaus (Equifax, Experian, TransUnion) through AnnualCreditReport.com. Dispute any errors immediately—corrections typically take 30-45 days.

Calculate your DTI using our Debt Consolidation Calculator to identify if you need to pay down debts before applying.

Quick DTI improvement strategies:

- Pay off small credit card balances

- Avoid taking on new car loans or credit cards

- Consider debt consolidation if carrying high-interest balances

- Increase income through side work (needs 2-year history for lender consideration)

Step 2: Get Pre-Approved (3-5 Lenders)

Pre-approval involves full credit checks and documentation review, providing a reliable loan amount estimate. Shop at least 3-5 lenders within a 14-day window—credit bureaus count multiple mortgage inquiries as a single pull.

Lender types to compare:

- National banks (Chase, Bank of America, Wells Fargo)

- Credit unions (often 0.125-0.25% lower rates for members)

- Online lenders (Rocket Mortgage, Better.com)

- Local/regional banks (personalized service, portfolio loans)

- Mortgage brokers (access to multiple lenders)

Questions to ask each lender:

- What’s your interest rate AND APR? (APR includes fees)

- What are total closing costs?

- Can you match or beat competitor offers?

- What’s your average time to close?

- Do you sell loans to servicers or service in-house?

Step 3: Compare Loan Estimates (Within 3 Business Days)

Federal law requires lenders to provide standardized Loan Estimates within three business days of application. Compare these documents side-by-side, focusing on:

- Page 1: Loan amount, interest rate, monthly payment, cash to close

- Page 2: Closing costs breakdown (origination, appraisal, title, etc.)

- Page 3: Comparisons showing total interest over loan life

Red flags:

- Origination fees exceeding 1% of loan amount

- Junk fees (document prep fees, courier fees over $50)

- Significantly higher APR than interest rate (indicates high fees)

For first-time buyers, our Buy First Home 2026 Guide provides additional application insights.

Step 4: Submit Full Application & Documents

Complete applications typically require:

Income verification:

- Last 2 years W-2 forms

- Last 30 days of pay stubs

- Last 2 years tax returns (if self-employed)

- Verification of Employment (VOE) form

Asset documentation:

- Last 2 months bank statements (all pages)

- Retirement account statements

- Investment account statements

- Gift letter (if using gift funds for down payment)

Additional documentation:

- Photo ID (driver’s license)

- Social Security card

- Proof of residency

- Divorce decree (if applicable for alimony/child support)

- Bankruptcy discharge papers (if applicable)

Underwriting timeline: 30-45 days from application to closing for conventional loans (faster for purchase, slower for refinance).

Step 5: Close on Your Loan

Final steps before closing:

- Final walkthrough (24-48 hours before closing)

- Review Closing Disclosure (delivered 3 days before closing)

- Wire closing funds (typically due day before closing)

- Bring valid ID to closing appointment

- Review all documents carefully before signing

Typical closing costs: 2-5% of loan amount ($8,000-$20,000 on $400,000 loan).

Expert Tips to Improve Approval Odds

Tip #1: Improve Credit 6-12 Months Before Applying

Every 20-point credit score increase saves approximately $15-$30 monthly per $100,000 borrowed.

Fast credit improvements:

- Pay down credit card balances below 30% utilization (below 10% is ideal)

- Become authorized user on someone’s excellent credit card

- Don’t close old credit cards (reduces average account age)

- Set up automatic payments to ensure no missed payments

Visit our Good Credit Score 2026 Tiers guide for targeted improvement strategies.

Tip #2: Lower DTI Below 36% for Best Rates

Borrowers with DTI ratios below 36% receive preferential pricing—typically 0.125-0.25% lower rates than those with 43% DTI.

Quick DTI reduction tactics:

- Pay off car lease early if only 6-12 months remaining

- Pay down credit card balances (even temporarily with savings)

- Refinance student loans to lower monthly payment

- Wait to buy new car until after mortgage closes

Tip #3: Shop 3+ Lenders (Saves $1,500-$3,000)

According to Freddie Mac research, borrowers who obtain just one additional rate quote save an average of $1,500 over the loan life. Getting 5+ quotes saves approximately $3,000.

Rate shopping strategy:

- Complete all applications within 14-day window

- Compare both rate and total closing costs

- Negotiate fees (many are negotiable)

- Ask about lender credits vs. lower rates

Tip #4: Time Your Application Strategically

Best timing:

- Apply 60-75 days before desired closing (allows buffer for delays)

- Lock rate when rates dip or after favorable Fed announcements

- Close at month-end to reduce prepaid interest

- Avoid holiday periods (slower processing)

Rate lock duration: Typically 30, 45, or 60 days. Longer locks cost more but provide protection. If rates drop during lock period, ask about float-down options.

Tip #5: Avoid New Credit During Process

From application through closing, don’t:

- Apply for new credit cards

- Finance furniture or appliances

- Buy a car

- Change jobs (if possible)

- Make large deposits without explanation

Lenders often re-pull credit 1-3 days before closing. New accounts or inquiries can delay or derail approval.

Bonus tip: Consider points/lender credits trade-off. Paying 1 point (1% of loan amount) typically reduces rate by 0.25%. Break-even is usually 4-6 years, making it worthwhile if you plan to stay in the home long-term.

Frequently Asked Questions (FAQs)

Q1: Can I get a conventional loan with 5% down in 2026?

Yes. Conventional loans accept down payments as low as 3% for first-time buyers and 5% for repeat buyers. You’ll pay PMI until reaching 20% equity, but PMI is removable unlike FHA’s lifetime mortgage insurance.

Q2: What credit score do I need for the best conventional loan rates?

A score of 740+ typically qualifies for top-tier pricing. Scores of 760-780+ may receive additional rate discounts of 0.125-0.25%. While 620 is the minimum, expect rates 1-1.5% higher than prime rates.

Q3: How does the $832,750 limit affect me if I live in an expensive area?

High-cost areas receive elevated limits up to $1,249,125. Check your specific county limit at the FHFA website. If you need to exceed your area’s limit, you’ll need a jumbo loan with stricter requirements.

Q4: Can I remove PMI before reaching 20% equity?

Yes, through home appreciation and new appraisal (typically requires 2-5 years ownership) or by refinancing once you have 20% equity. Your home must appraise at a value that gives you 20-25% equity for removal approval.

Q5: Is a conventional loan better than FHA for first-time buyers?

If your credit score is 680+, conventional typically costs less long-term due to removable PMI. FHA works better for scores between 580-679 or when you need maximum down payment flexibility (3.5% vs 3% isn’t significantly different).

Q6: Do conventional loans work for investment properties in 2026?

Yes, but require higher down payments (typically 15-25%), charge higher interest rates (0.50-0.75% above primary residence rates), and have stricter qualification standards. Investment property loans also have lower DTI thresholds around 43%.

Q7: What’s the difference between conforming and conventional loans?

All conforming loans are conventional, but not all conventional loans are conforming. Conforming means the loan meets Fannie Mae/Freddie Mac standards including staying within FHFA loan limits. Jumbo loans are conventional but non-conforming because they exceed limits.

Q8: Can I get a conventional loan if I have student loan debt?

Yes. Lenders include your student loan monthly payment in DTI calculations. If loans are in deferment, lenders typically use 0.5-1% of the balance as the monthly payment for qualification purposes. Income-driven repayment plans can help lower DTI.

Q9: How long does conventional loan approval take in 2026?

Standard timeline is 30-45 days from application to closing. Well-prepared borrowers with complete documentation can close in 21-30 days. Complex files (self-employed, multiple properties, etc.) may take 45-60 days.

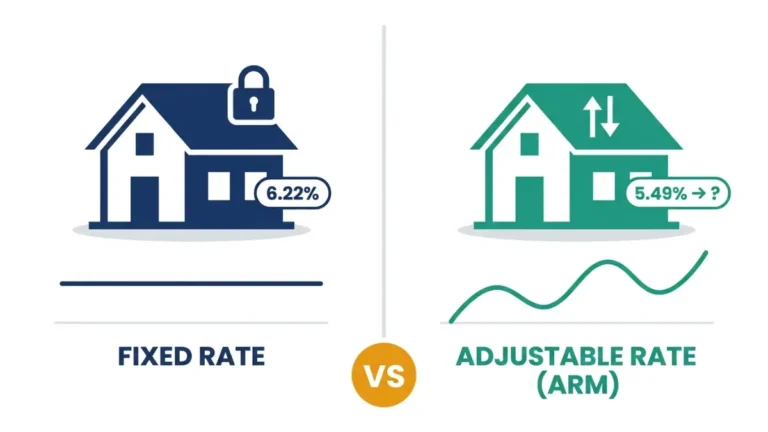

Q10: Are conventional loan rates fixed or adjustable in 2026?

Both options are available. Fixed-rate mortgages (30-year most common) maintain the same rate for the loan’s life. Adjustable-rate mortgages (ARMs) offer lower initial rates (typically 0.5-1% below fixed) that adjust after 5, 7, or 10 years based on market indexes.

Q11: Can first-time homebuyers qualify for 3% down conventional loans?

Yes, through Fannie Mae HomeReady and Freddie Mac Home Possible programs. Requirements include credit scores typically 680+, income limits (varies by county), and homebuyer education course completion. These programs often beat FHA’s 3.5% down option for qualified borrowers.

Disclaimer

This article is for educational purposes only and does not constitute financial, legal, or tax advice. Conventional loan terms, rates, requirements, and limits vary by lender, geographic location, property type, and individual borrower circumstances. The 2026 conforming loan limits and program requirements are based on FHFA announcements and current industry standards but may change.

Interest rate examples and cost projections are illustrative and do not represent guaranteed rates or terms. Actual rates depend on credit profile, loan-to-value ratio, debt-to-income ratio, property type, occupancy status, and market conditions at time of application.

Mortgage products carry significant financial obligations extending 15-30 years. Borrowers should carefully evaluate their financial situation, compare multiple lenders, and consider consulting with licensed mortgage professionals, financial advisors, and tax professionals before making borrowing decisions.

Loan approval is subject to credit approval, income verification, appraisal, and underwriting review. Not all borrowers will qualify for advertised programs or rates. This content is not sponsored by or affiliated with any lender, government agency, or financial institution.

Information current as of February 2026. Federal Housing Finance Agency conforming loan limits, Fannie Mae and Freddie Mac guidelines, and federal lending regulations are subject to change. Always verify current requirements with official sources and licensed professionals.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.