Debt-to-Income Ratio for Home Loans: The Rule Every Borrower Must Know

One number silently blocks most home loan applications. Your debt-to-income ratio sets your approval odds and interest rate. Here are the 2026 rules every borrower must know.

In This Article

What Is a Debt-to-Income Ratio? (The 60-Second Answer)

One number can quietly block your home loan before you even fill out the application — and most borrowers never check it. Your debt-to-income ratio (DTI) is the percentage of your gross monthly income that goes toward monthly debt payments.

In simple terms: Lenders look at this ratio to decide if you can afford a new mortgage on top of what you already owe.

A DTI below 36% signals financial strength. Above 50%, most lenders pump the brakes. Getting this number right before you apply is the single most impactful step you can take toward home loan approval in 2026.

Key Takeaway: DTI is not just an approval checkbox — it directly determines your interest rate, loan program eligibility, and how much home you can actually afford.

Front-End DTI vs. Back-End DTI: Know the Difference

Most borrowers don’t realize there are two separate DTI ratios lenders calculate. Confusing them is a costly mistake.

| Ratio Type | What It Measures | What’s Included |

|---|---|---|

| Front-End DTI (Housing Ratio) | Housing costs ÷ gross income | Mortgage P&I, property taxes, homeowners insurance, HOA fees, PMI |

| Back-End DTI (Total Debt Ratio) | All debts ÷ gross income | Everything in front-end + car loans, student loans, credit card minimums, personal loans, child support |

Most lenders focus almost entirely on your back-end DTI. That’s the number that determines your fate in underwriting.

The front-end ratio still matters for FHA and some conventional programs, but if your back-end ratio is too high, the front-end number won’t save you.

How to Calculate Your Debt-to-Income Ratio (Step-by-Step)

Use this formula: Total Monthly Debt Payments ÷ Gross Monthly Income × 100 = DTI%

Step 1 — Add Up All Monthly Debts

Include every recurring obligation that appears on your credit report:

- Proposed mortgage payment (principal + interest + taxes + insurance + HOA)

- Auto loan payments

- Student loan minimums (even if in deferment — more on this below)

- Credit card minimum payments

- Personal loan payments

- Child support or alimony

Step 2 — Find Your Gross Monthly Income

Use your pre-tax income — not your take-home pay. This is the #1 calculation mistake borrowers make. Include salary, rental income, Social Security, freelance income (2-year average for self-employed), and other documented income sources. You can use the Salary Calculator to verify your gross monthly figure quickly.

Step 3 — Divide and Convert

Divide total monthly debts by gross monthly income, then multiply by 100.

Real-World DTI Scenarios (2026 Income Brackets)

No competitor shows you this. Here are three real borrower scenarios:

| Monthly Gross Income | Monthly Debts | DTI Ratio | Approval Outlook |

|---|---|---|---|

| $5,000/mo | $1,500 (car + credit cards) + $900 proposed mortgage = $2,400 | 48% | Tight — FHA or VA likely needed |

| $8,000/mo | $800 (car + student loans) + $2,000 proposed mortgage = $2,800 | 35% | Strong — Conventional approval likely |

| $12,000/mo | $1,200 (all debts) + $3,200 proposed mortgage = $4,400 | 36.7% | Excellent — Best rate tiers available |

Use our Home Affordability Calculator to run your own numbers before speaking with a lender.

What’s Included vs. Excluded in DTI

| ✅ INCLUDE in DTI | ❌ EXCLUDE from DTI |

|---|---|

| Proposed mortgage payment | Utilities (electric, gas, water) |

| Car loan payments | Groceries and food |

| Student loan minimums | Health insurance premiums |

| Credit card minimum payments | 401(k) contributions |

| Personal loan payments | Streaming subscriptions |

| Child support / alimony | Cell phone bills |

| Co-signed loan payments | Gas and transportation costs |

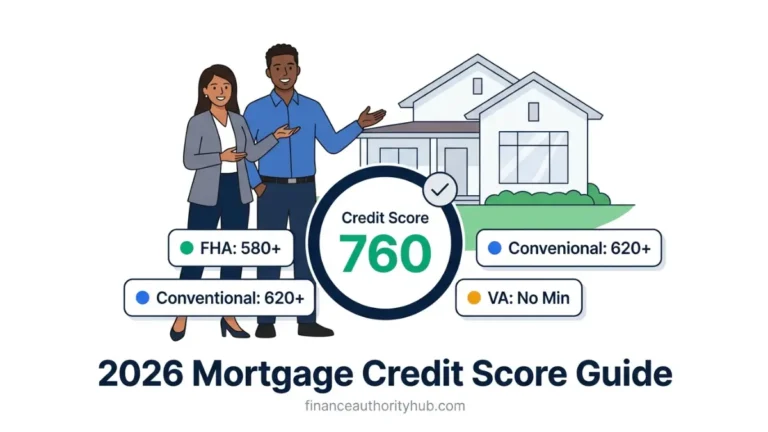

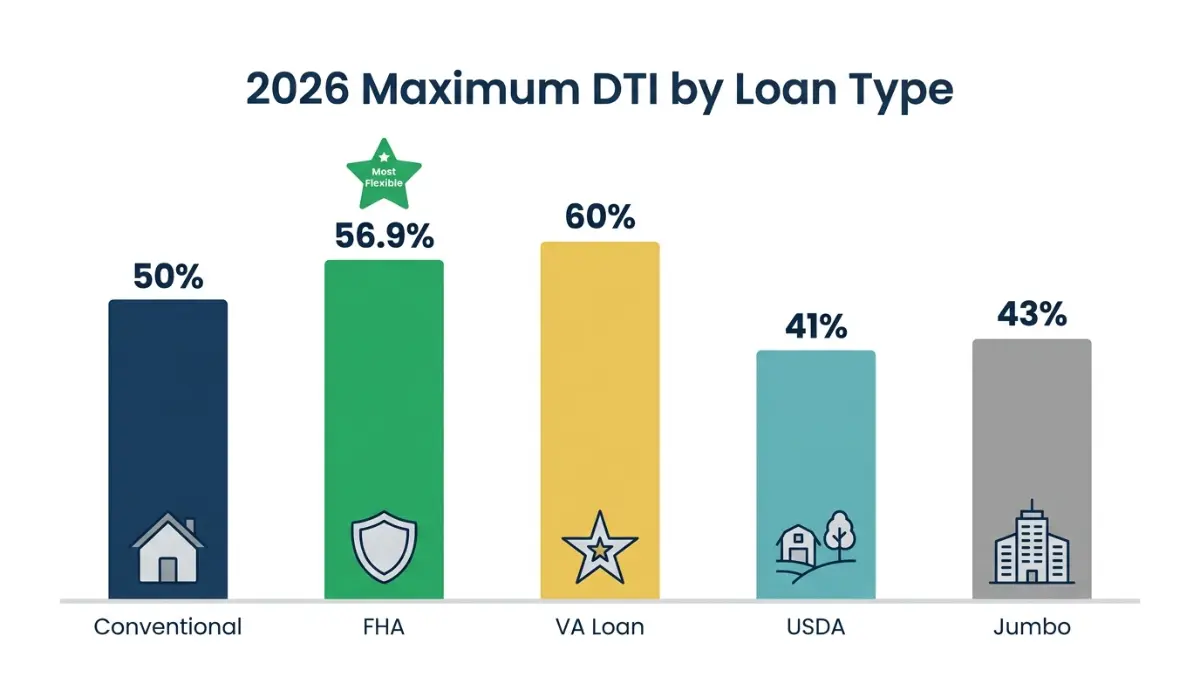

Maximum DTI Limits by Loan Type — 2026 Official Guidelines

This is the complete master table no other finance site has published in one place. Bookmark it.

| Loan Program | Front-End Max | Back-End Max | Key Notes |

|---|---|---|---|

| Conventional (Fannie Mae) | 28% ideal | 36–45% standard / up to 50% via DU | Strong credit + reserves needed above 45% |

| FHA Loan | 46.9% | 56.9% (2026 rule) | Most flexible first-time buyer program |

| VA Loan | No hard limit | 41% guideline / up to 60% | Residual income requirement applies |

| USDA Loan | 29% | 41% | Rural/suburban properties only |

| Jumbo Loan | 28% | 43% max | Stricter underwriting always applies |

According to Fannie Mae’s official selling guide, manually underwritten conventional loans cap at 36% DTI, with the maximum rising to 45% for borrowers meeting credit score and reserve thresholds. Automated underwriting (DU) can push this to 50%.

The 2026 FHA Rule Almost Nobody Talks About

In 2026, FHA loans follow the 46.9/56.9 rule — your front-end DTI must stay at or below 46.9% and your back-end at or below 56.9%. These are guidelines, not hard ceilings, which means lenders have flexibility for strong applicants.

This makes FHA loans by far the most accessible program for borrowers with higher debt loads. According to HUD’s official mortgage credit analysis guidelines, compensating factors such as documented savings, stable employment history, and minimal payment shock can support approval even above these thresholds.

For first-time buyers exploring this path, our complete breakdown of types of home loans explains when FHA makes sense vs. conventional programs.

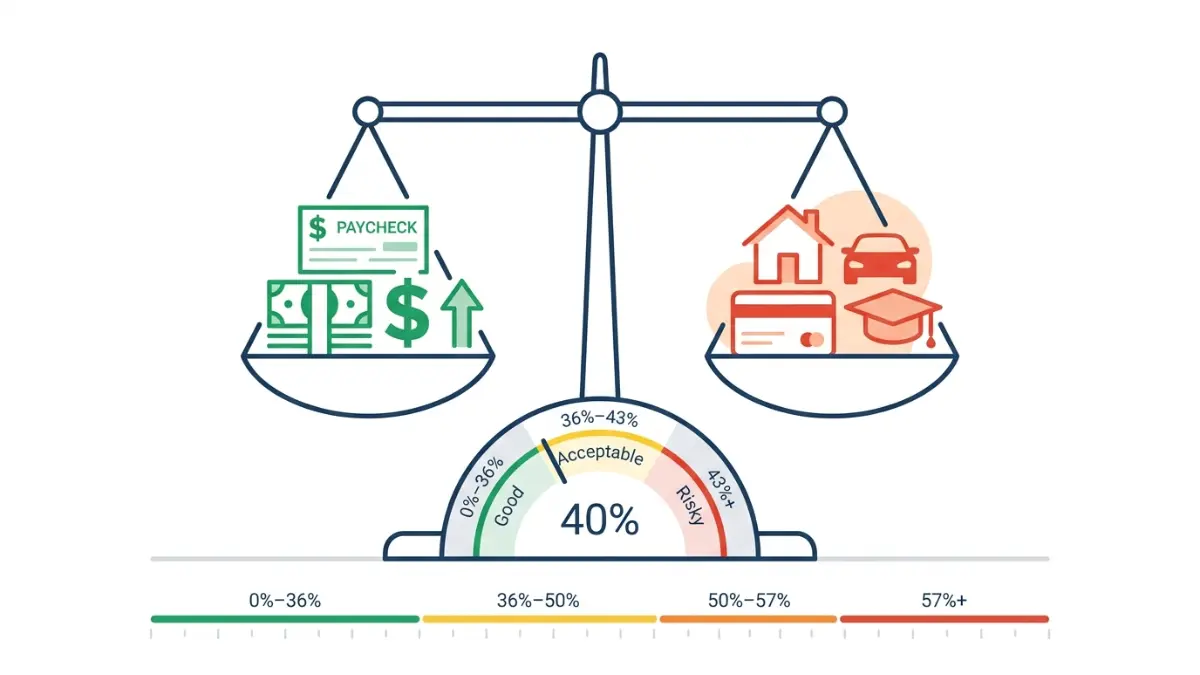

The 28/36 Rule — Still Relevant in 2026?

The 28/36 rule is the traditional benchmark:

- 28% = maximum front-end ratio (housing costs only)

- 36% = maximum back-end ratio (all debts combined)

This rule originated from conventional underwriting standards decades ago. It is still used as a benchmark by many lenders but is no longer a hard ceiling for most loan programs. In high cost-of-living cities like New York, San Francisco, or Seattle, strict adherence to 28/36 would disqualify most borrowers.

What This Means For You: The 28/36 rule is a target, not a disqualifier. FHA, VA, and even Fannie Mae’s automated systems regularly approve DTIs well above 36%.

VA Loans: Residual Income Matters More Than DTI

VA loans are unique. While the stated DTI guideline is 41%, the Department of Veterans Affairs places greater emphasis on residual income — the money left over after all monthly obligations are paid.

Residual income requirements vary by family size and region:

- A family of four in the Northeast needs approximately $1,003/month in residual income

- The same family in the South needs approximately $916/month

This means a veteran with a 50% DTI can still qualify if their residual income clears the threshold. No mainstream finance site explains this distinction clearly.

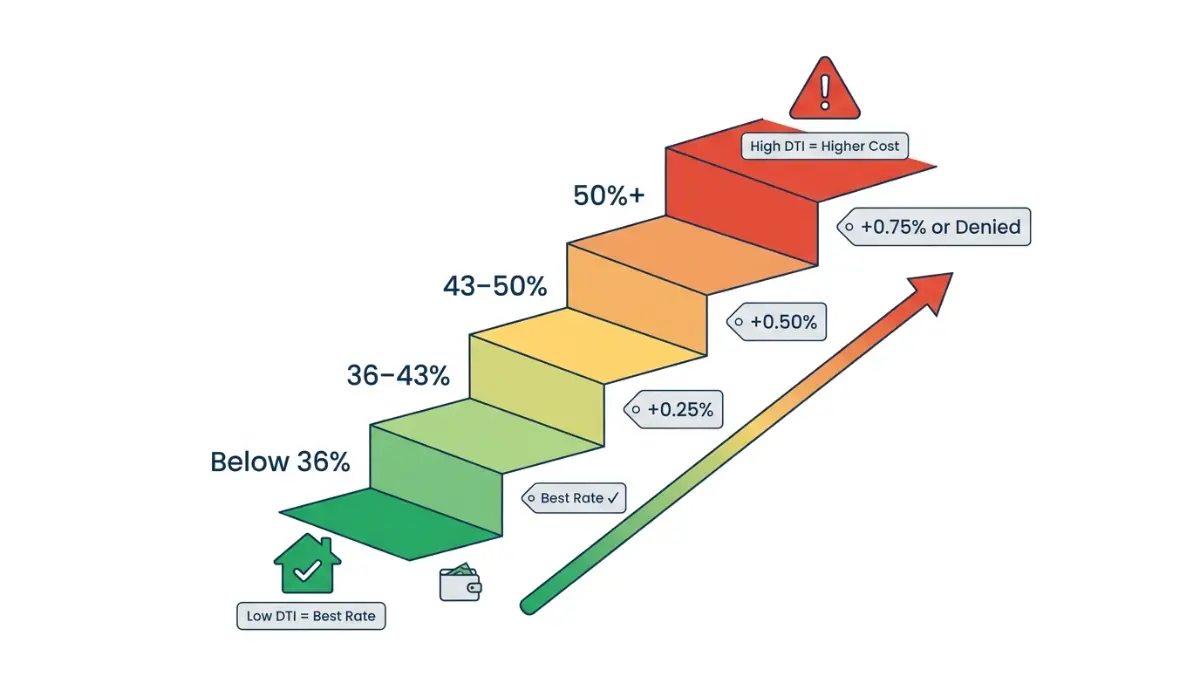

How Your DTI Ratio Affects Your Mortgage Interest Rate

Here’s what almost every competitor misses entirely: your DTI ratio doesn’t just affect whether you’re approved — it affects what interest rate you pay.

Lenders use Loan Level Price Adjustments (LLPAs) — a risk-pricing grid that factors in your DTI, credit score, loan-to-value ratio, and loan type. The higher your DTI, the higher the risk tier, and the higher the rate.

| DTI Range | Credit Score 740+ | Credit Score 680–739 | Credit Score 640–679 |

|---|---|---|---|

| Below 36% | Best rate tier | Strong approval | Moderate approval |

| 36%–43% | Strong approval | Good approval | Approval with conditions |

| 43%–50% | Conditional | Higher rate pricing | High rate or denial |

| Above 50% | FHA/VA only | FHA/VA only | Very limited options |

Key Takeaway: A DTI above 45% can add 0.25–0.75% to your mortgage interest rate even when you qualify. Over a 30-year loan, that means tens of thousands of dollars in extra interest.

How Student Loan Deferment Is Treated in 2026 (Updated)

This is a critical nuance that most articles skip entirely. If your student loans are in deferment, lenders still count them in your DTI — but the calculation method varies by loan program:

- Conventional loans (Fannie Mae/Freddie Mac): Use the actual payment shown on credit report, or 1% of outstanding balance if payment is $0 or unknown

- FHA loans: Use the actual payment or 1% of balance, whichever is greater

- VA loans: Use the actual payment — if truly $0, it may not be counted

This distinction can move your DTI by 3–8 percentage points depending on your student loan balance. Use our Student Loan Calculator to model your actual payments and see how different repayment plans affect your DTI picture.

Self-Employed and Gig Worker DTI: Different Rules Apply

If you’re self-employed, freelance, or earn gig income, lenders calculate your DTI differently:

- Income used: 2-year average from federal tax returns (Schedule C or Schedule E)

- Write-offs hurt you: Business deductions reduce your qualifying income

- Bank statement loans: Some non-QM lenders use 12–24 months of deposits instead of tax returns

- 1099 workers: Income averaged over 24 months; significant year-over-year swings may require explanation

The bottom line: a self-employed borrower earning $120,000 in deposits might only show $75,000 in qualifying income after deductions — pushing DTI much higher than expected.

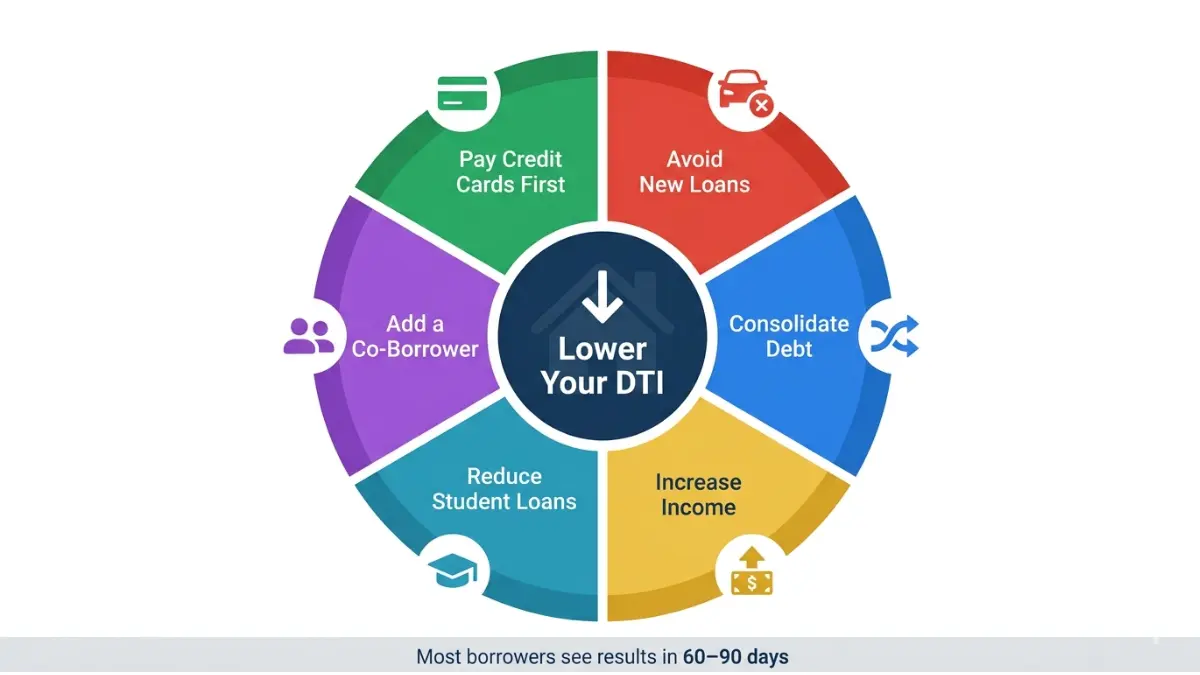

How to Lower Your Debt-to-Income Ratio Fast (2026 Action Plan)

Your DTI has exactly two levers: reduce debt or increase income. Here’s how to move the needle quickly, ranked by speed of impact.

Lever 1: Reduce Monthly Debt Obligations

Fastest-impact moves:

- Pay off revolving credit card balances — minimum payments on $8,000 in credit card debt could be adding $200–$320/month to your DTI calculation. Our Credit Card Payoff Calculator shows exactly how fast you can eliminate this

- Consolidate multiple debts into one lower monthly payment — use our Debt Consolidation Calculator to model the DTI impact before you commit

- Avoid new auto loans or personal loans in the 6–12 months before applying

- Remove co-signed debts you’re no longer responsible for — provide 12 months of cancelled checks showing the primary borrower pays

- Request student loan income-driven repayment to legally reduce your monthly payment

Lever 2: Increase Qualifying Income

- Document all income sources: rental income, freelance work, investment dividends, Social Security

- A verifiable raise or promotion letter can be used immediately

- Adding a co-borrower with strong income can lower the combined DTI significantly

- For investment properties, rental income (at 75% of lease value) can offset the mortgage payment

Real Scenario: From 49% DTI to 41% in 90 Days

Borrower profile: $7,500/month gross income, $3,675/month in debts = 49% DTI. Denied for conventional loan.

Actions taken:

- Paid off $6,200 credit card balance (freed $186/month minimum)

- Cancelled unused personal line of credit

- Documented $400/month side income with 6-month bank statements

Result: $3,675 → $3,075/month in debts = 41% DTI. Approved for conventional loan with competitive rate.

The Debt-to-Income Ratio Calculator lets you test these scenarios in real time.

60-Second Pre-Application DTI Checklist

Run through this before you contact any lender:

- [ ] Know your exact gross monthly income (pre-tax)

- [ ] List every debt minimum payment from your credit report

- [ ] Calculate your front-end DTI (housing costs only)

- [ ] Calculate your back-end DTI (all debts including proposed mortgage)

- [ ] Compare your number against the loan type limit table above

- [ ] Identify 1–2 quick payoff targets to reduce DTI before applying

- [ ] Check your credit score — compensating factors matter (see credit score guide)

- [ ] For VA borrowers: calculate your residual income separately

According to the Consumer Financial Protection Bureau’s homebuying guide, borrowers who review their DTI before applying are significantly less likely to be denied and more likely to secure favorable loan terms.

Understanding your full home loan requirements alongside your DTI gives you the complete picture before your first lender conversation.

Frequently Asked Questions About Debt-to-Income Ratio

1. What is a good debt-to-income ratio for a home loan?

Below 36% is considered excellent by most lenders. The range of 36%–43% is still strong for conventional loans. Anything above 43% typically requires compensating factors or a government-backed loan program.

2. What is the maximum DTI for a conventional loan in 2026?

Fannie Mae’s automated underwriting system allows up to 50% DTI with strong compensating factors. For manually underwritten loans, the ceiling is 45%. Most lenders prefer 43% or below for the best approval odds and rate pricing.

3. Can I get a mortgage with a 50% debt-to-income ratio?

Yes — primarily through FHA or VA programs. FHA allows back-end DTI up to 56.9% in 2026 with compensating factors. VA loans can approve up to 60% in some cases when residual income requirements are met.

4. Does my DTI ratio affect my mortgage interest rate?

Yes, directly. Lenders use risk-based pricing grids (LLPAs) that factor in DTI alongside your credit score. A DTI above 45% can add 0.25–0.75% to your rate, costing thousands over the loan term.

5. What debts are not counted in my DTI calculation?

Utilities, groceries, insurance premiums, 401(k) contributions, phone bills, and subscriptions are not included. Only recurring debt obligations that appear on your credit report are counted.

6. How do student loans count in DTI for a mortgage?

It depends on your loan program. Conventional lenders use 1% of the balance if payments are deferred. FHA uses the actual payment or 1% of balance — whichever is higher. VA loans use only the actual payment amount.

7. What is the 28/36 rule for mortgages?

The 28/36 rule suggests housing costs stay below 28% of gross income and total debts below 36%. It’s a traditional benchmark, not a hard ceiling — most loan programs in 2026 allow higher ratios with qualifying factors.

8. Can I get an FHA loan with a high debt-to-income ratio?

Yes. FHA’s 2026 guidelines allow a front-end DTI of 46.9% and a back-end DTI of 56.9%. With strong compensating factors, some lenders approve even higher ratios under automated underwriting.

9. How fast can I lower my DTI before applying?

Paying off a high-balance credit card can shift your DTI by 3–5% within the same billing cycle. A full DTI reduction of 5–10 percentage points is achievable within 60–90 days with focused debt payoff.

10. Do lenders use gross or net income for DTI?

Always gross income — your pre-tax earnings. Using your take-home (net) pay is the most common calculation error borrowers make. It produces a falsely high DTI ratio.

11. What is the difference between front-end and back-end DTI?

Front-end DTI covers housing costs only (mortgage, taxes, insurance, HOA). Back-end DTI includes all recurring debts. Lenders primarily evaluate your back-end ratio for mortgage qualification — it gives them a complete picture of your monthly financial obligations.

What to Do Next

If your DTI is in range, your next step is understanding the full picture of home loan income requirements and checking whether your credit score meets the 2026 thresholds for your target loan program.

If your DTI needs work, start with the Mortgage Calculator to find a loan amount that fits your current ratio, then build your payoff plan using the Amortization Calculator to model exactly when your debt load reaches the approval zone.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, mortgage, or lending advice. Debt-to-income ratio guidelines vary by lender, loan program, and individual financial profile. DTI thresholds and underwriting standards are subject to change. Always consult a licensed mortgage professional or financial advisor before making borrowing decisions. Loan approval depends on complete underwriting review and individual lender requirements.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.