Debt-to-Income Ratio Calculator — Know in 10 Seconds

Debt-to-Income (DTI) Ratio Calculator

Calculate front-end (housing) and back-end (total) DTI, residual income, and “what-if” targets. Add custom debts and export a CSV report.

Inputs

DTI is typically based on gross monthly income and recurring monthly debts.

Include rent/mortgage + taxes + insurance + HOA + mortgage insurance (if any).

Some mortgage contexts discuss front-end vs back-end ratios (e.g., 28% housing and 36% total are commonly cited guidelines).

Results

Income used (gross)

—

Annual equivalent: —

DTI ratios

Front-end (housing): —

Back-end (total): —

Back-end (with planned debt): —

Monthly totals

Housing total: —

Other debts: —

Total debt: —

Total debt (planned): —

Residual income (estimate)

—

With planned debt: —

Housing “what-if” (front-end target)

Max housing allowed at your front-end target: —

Housing room (positive = can add, negative = reduce): —

Front-end = housing expenses ÷ gross income. Back-end = (housing + all recurring debts) ÷ gross income.

DTI target scenarios (monthly)

| Scenario | Max total debt allowed | Room / Over | Required gross monthly income |

|---|

Debt breakdown (monthly + annual)

| Group | Item | Monthly amount | % of income | Annual amount |

|---|

This is an educational estimate; lender rules can differ by country, product type, and what they count as “debt.”

Results appear after you click “Calculate.”

In This Article

Your debt-to-income ratio (DTI) is the single number that controls whether lenders say yes or no. It compares your total monthly debt payments to your gross monthly income — and in 2026, most U.S. lenders require a back-end DTI of 43% or lower to approve a mortgage. Use our debt-to-income ratio calculator above to get your number in seconds, then read exactly what it means and how to fix it.

What Is a Debt-to-Income Ratio — and Why It Controls Your Financial Life

Your DTI ratio is one of the two most important numbers in personal finance. The other is your credit score. But here’s what most people don’t realize: a high DTI can block a loan even if your credit score is excellent.

According to the Consumer Financial Protection Bureau, lenders use DTI to measure your ability to manage monthly payments and repay borrowed money. The higher your DTI, the riskier you appear to any lender.

The Simple DTI Formula

DTI = Total Monthly Debt Payments ÷ Gross Monthly Income × 100

Example: If your monthly debts total $2,000 and your gross income is $6,000, your DTI is 33%.

- Monthly debts = mortgage/rent + car loan + student loan + credit card minimums + personal loan + alimony/child support

- Gross monthly income = your earnings before taxes and deductions

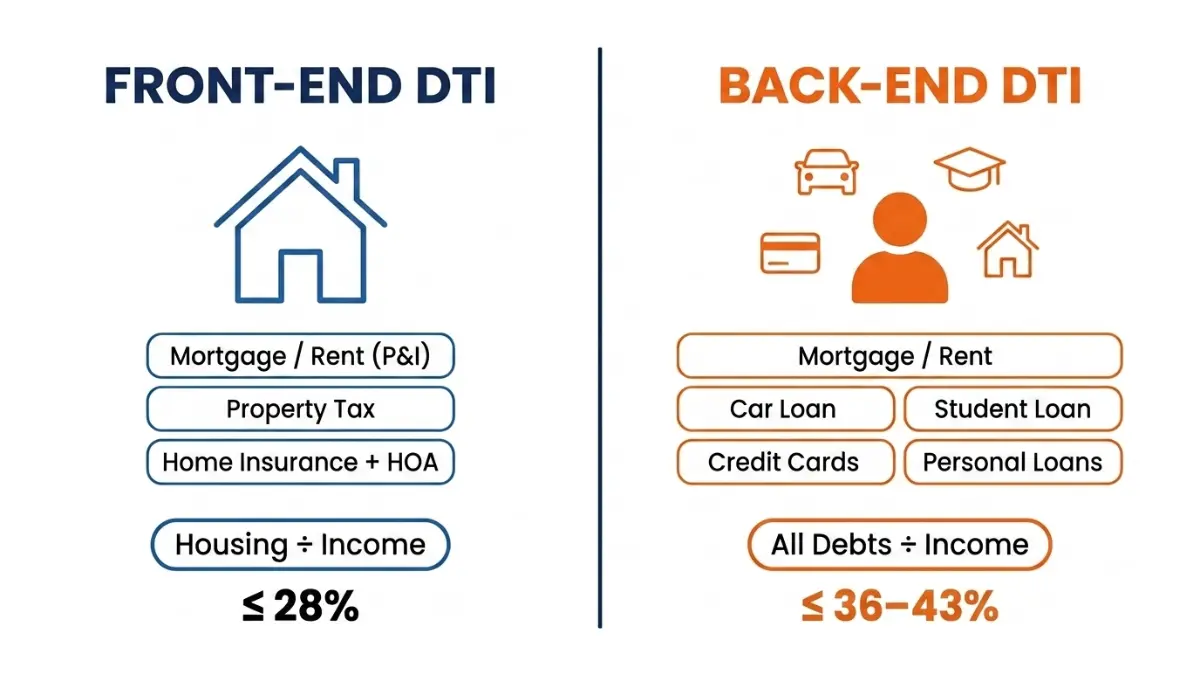

Front-End DTI vs. Back-End DTI — What’s the Difference?

Most borrowers don’t realize there are two DTI ratios. Lenders evaluate both separately.

| Front-End DTI | Back-End DTI | |

|---|---|---|

| Also called | Housing ratio | Total debt ratio |

| What it includes | Mortgage/rent + property tax + home insurance + HOA | Everything in front-end PLUS all other debts |

| Who uses it | Mortgage lenders | All lenders |

| 2026 guideline | ≤ 28% | ≤ 36–43% |

Back-end DTI is the number most lenders focus on. Your mortgage calculator can help you estimate housing costs before plugging them into your DTI.

What Does Your DTI Actually Mean?

| DTI Range | Rating | What Lenders Think |

|---|---|---|

| Under 20% | Excellent | Strong approval, best rates available |

| 20% – 35% | Good | Most loan types approved with ease |

| 36% – 43% | Borderline | Increased scrutiny; compensating factors needed |

| 44% – 50% | High Risk | Limited loan options; may need co-borrower |

| Over 50% | Danger Zone | Most conventional lenders will decline |

Key takeaway: A DTI under 36% is your target for the smoothest mortgage approval process in 2026.

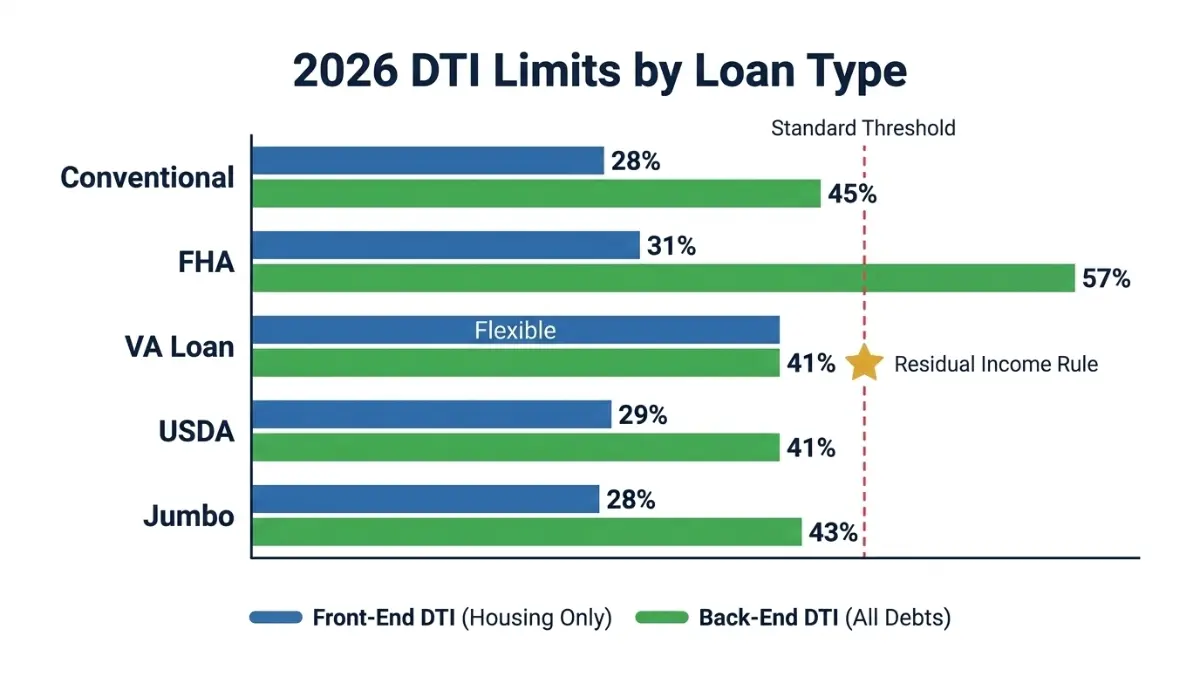

2026 DTI Limits by Loan Type — Exact Numbers Lenders Use Right Now

This is where most borrowers get blindsided. DTI limits are not universal — they vary dramatically depending on which loan type you’re applying for. Here are the exact 2026 thresholds.

Conventional Loan DTI Limits 2026

Fannie Mae and Freddie Mac set the standard for conventional loans. The classic 28/36 rule remains the benchmark:

- Front-end max: 28% (housing costs only)

- Back-end max: 36% standard; up to 45–50% with strong compensating factors (high credit score, large down payment, significant reserves)

Use our home affordability calculator to model how different home prices affect your front-end DTI before you apply.

FHA Loan DTI Limits 2026

FHA loans are more flexible, making them popular with first-time buyers. According to HUD’s official underwriting guidelines:

- Front-end max: 31%

- Back-end max: 43% standard; up to 57% through automated underwriting with strong compensating factors

- Energy-efficient homes: Stretch ratios of 33%/45% apply

VA Loan DTI + The Residual Income Rule (What Competitors Miss Completely)

VA loans for U.S. veterans work differently from every other loan type. The VA benchmarks DTI at 41%, but exceeding this threshold does not automatically disqualify you. According to the VA Lender’s Handbook Chapter 3, VA underwriters rely equally on residual income — the money left over after all debts and housing expenses are paid.

If your residual income exceeds the VA’s regional minimums by 20% or more, a DTI above 41% can still be approved. This is a critical advantage that Bankrate, NerdWallet, and Ramsey fail to explain.

2026 Master DTI Benchmark Table — All Loan Types

| Loan Type | Front-End Max | Back-End Max | Special Rule |

|---|---|---|---|

| Conventional | 28% | 36–45% | 28/36 rule (Fannie/Freddie) |

| FHA | 31% | 43–57% | Automated underwriting stretch |

| VA Loan | No hard limit | 41% guideline | Residual income overrides DTI |

| USDA | 29% | 41% | Rural property only |

| Jumbo | 28% | 36–43% | No GSE backing; stricter |

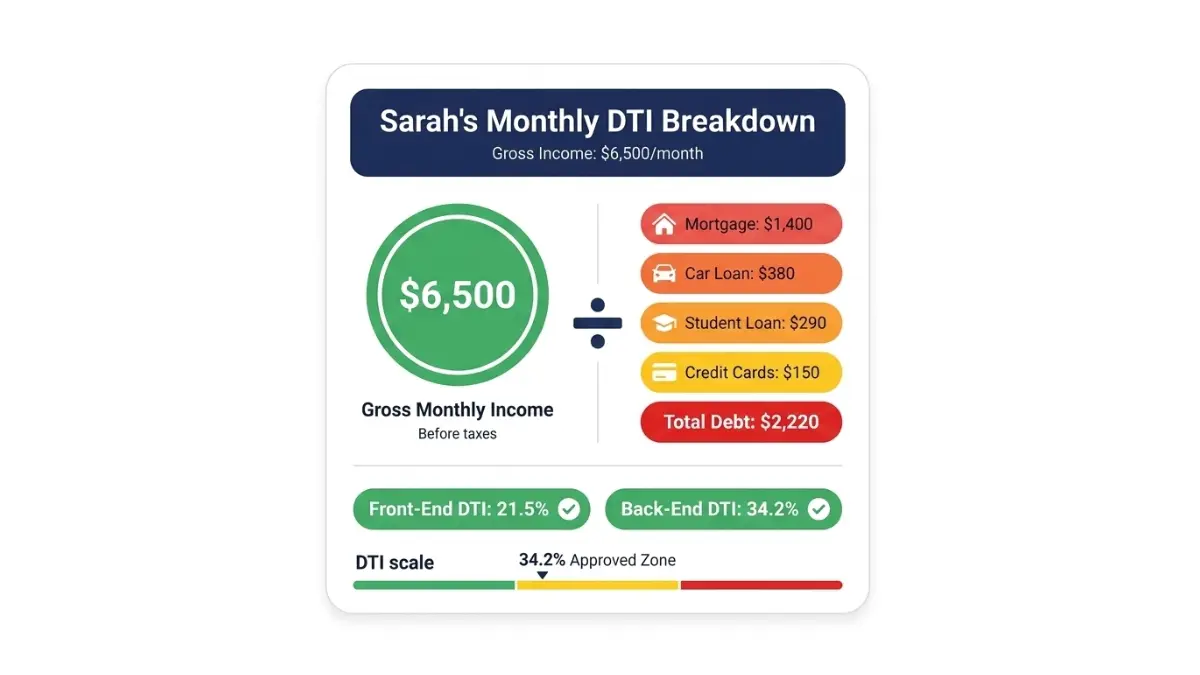

Real Example — How Sarah Used Her DTI Calculator to Get Mortgage Approved

This is what competitors never show you: real numbers, a real person, and a real outcome.

Sarah’s Numbers — Before the Calculator

Sarah is a registered nurse in Dallas, Texas. She earns $6,500/month gross and is applying for a conventional mortgage.

Her monthly debts:

- Mortgage (proposed): $1,400 (P&I + tax + insurance)

- Car loan: $380

- Student loan: $290

- Credit card minimums: $150

- Total monthly debt: $2,220

Her back-end DTI = $2,220 ÷ $6,500 = 34.2% ✅ Approved under the 36% conventional guideline.

Her front-end DTI = $1,400 ÷ $6,500 = 21.5% ✅ Well under the 28% limit.

What the Calculator Revealed She Could Fix

Sarah originally had a $4,800 credit card balance with a $180/month minimum. She paid it off before applying. That one move dropped her back-end DTI from 37.0% → 34.2% — pushing her from the borderline zone into clean approval territory.

What This Means For You: Every $100/month reduction in debt payments improves your DTI by approximately 1.5% on a $6,500/month income. On a $5,000/month income, each $100 monthly reduction equals 2.0% DTI improvement.

To model your own payoff scenarios, use our debt consolidation calculator or credit card payoff calculator.

How to Lower Your Debt-to-Income Ratio Fast — 7 Proven Strategies (2026)

There are only two ways to lower your DTI: reduce monthly debt or increase income. Here are the seven most effective tactics, ranked by impact.

Strategy 1 — Pay Off Small Debts First (Snowball Impact on DTI)

Eliminating a small balance completely removes that monthly payment from your DTI calculation. A $3,000 auto loan with $350/month in payments left delivers instant DTI relief once paid off — far more powerful than making small extra payments on a large mortgage. Learn more about the snowball vs. avalanche approach to structuring your payoff plan.

Strategy 2 — Consolidate Multiple Debts Into One Lower Payment

Rolling three high-interest debts into one consolidation loan often reduces total monthly payment obligations. If your combined minimums drop from $750 to $480/month, your DTI improves by 4.2% on a $6,500 income immediately.

Strategy 3 — Remove Debts With Fewer Than 10 Payments Remaining

Many lenders — including FHA and conventional underwriters — will exclude installment debts with 10 or fewer monthly payments left. Ask your loan officer if this applies. It costs you nothing and could swing your DTI by 2–5%.

Strategy 4 — Add a Co-Borrower’s Income

Adding a spouse or co-borrower who earns income but carries little debt can dramatically lower your combined back-end DTI. On a $2,000/month additional income, your qualifying DTI improves by roughly 6–8 percentage points.

Strategy 5 — Refinance Existing Debt to Lower Payments

Refinancing a car loan or personal loan to a longer term lowers your monthly payment obligation, reducing DTI even if the total balance stays the same. Use our mortgage refinance calculator to model payment reductions on housing debt.

Strategy 6 — Avoid All New Debt 90 Days Before Applying

Opening a new credit card, financing furniture, or leasing a car within 90 days of a mortgage application can add new monthly obligations that immediately push your DTI over the threshold. This is one of the most common and most avoidable mortgage killers in 2026.

Strategy 7 — Increase Verifiable Gross Income

Part-time income, freelance work, rental income, or a pay raise all count — provided you can document them. The IRS requires a 2-year income history for self-employment, so plan ahead. Our retirement calculator can help you model how income growth over time affects your long-term debt picture.

DTI Improvement Impact Table

| Action | Monthly Debt Reduction | DTI Impact ($6,500 Income) |

|---|---|---|

| Pay off $5K credit card | -$150/month | -2.3% DTI |

| Consolidate 3 loans | -$270/month | -4.2% DTI |

| Remove near-paid auto loan | -$380/month | -5.8% DTI |

| Add co-borrower (+$2,500/mo) | Income increase | -7.1% DTI |

| Refinance car to lower payment | -$100/month | -1.5% DTI |

Good Debt-to-Income Ratio in the USA — 2026 Benchmarks That Matter

Since 95% of our readers are in the United States, let’s focus on exactly what American lenders, the federal government, and credit experts consider a “good” DTI in 2026.

What Is a Good DTI Ratio in the USA (2026)?

The CFPB and mainstream lenders align on these benchmarks:

- Under 36%: Considered healthy. Most loan types available at competitive rates.

- 36%–43%: Acceptable but monitored. Mortgage approval possible with strong credit score (720+) and reserves.

- 43%–50%: High risk zone. FHA and VA may still approve with compensating factors.

- Over 50%: Most lenders decline. Focus on debt reduction before applying.

The 28/36 rule — spend no more than 28% of gross income on housing and no more than 36% on all debt combined — remains the gold standard for financial planning in the U.S.

How DTI Interacts With Your Credit Score

DTI and credit score work together in lender decisions. A high credit score can partially compensate for a borderline DTI — but there are hard limits.

| Credit Score | Max DTI Most Lenders Accept |

|---|---|

| 760+ | Up to 50% (with compensating factors) |

| 720–759 | Up to 45% |

| 680–719 | Up to 43% |

| 640–679 | Up to 41% |

| Below 640 | Under 36% strongly preferred |

To understand where your credit score stands, our credit score calculator provides an instant estimate. You can also review what constitutes a good credit score in 2026 for a full tier breakdown.

Does DTI Affect Your Credit Score?

No — DTI is not a credit score factor. Your credit score is calculated from payment history, credit utilization, length of credit history, and new inquiries. DTI is calculated and evaluated separately by each lender during underwriting. The debts that make up your DTI do, however, contribute to your credit utilization ratio, which is a major credit score component.

Frequently Asked Questions — Debt-to-Income Ratio Calculator

1. What is a good debt-to-income ratio?

A DTI under 36% is considered good by most U.S. lenders. For mortgage approval, staying under 43% is typically the threshold. Under 20% puts you in the strongest possible borrowing position.

2. How do I calculate my debt-to-income ratio?

Add up all recurring monthly debt payments — mortgage, car, student loan, credit card minimums, personal loan, alimony. Divide by your gross (pre-tax) monthly income. Multiply by 100. That’s your back-end DTI percentage.

3. What debts are included in DTI?

Included: Mortgage/rent, car loans, student loans, personal loans, credit card minimum payments, alimony, child support, and any installment loan payments. Not included: Utilities, groceries, cell phone bills, streaming subscriptions, health insurance premiums, and 401(k) contributions.

4. Does rent count in DTI ratio?

For renters applying for a mortgage: Most lenders exclude your current rent from DTI because they assume you’ll stop paying rent once you purchase the home. The proposed mortgage payment replaces it in the calculation.

5. What is the maximum DTI for a mortgage in 2026?

It depends on loan type. Conventional loans allow up to 45–50% with compensating factors. FHA loans can stretch to 57% through automated underwriting. VA loans use the 41% benchmark but heavily weigh residual income. Most borrowers should target under 43%.

6. Can I get a mortgage with a 50% DTI?

Possibly, but your options narrow significantly. FHA loans with automated underwriting approval are your best path. You’ll typically need a credit score above 680, significant cash reserves, and a stable employment history. Working to reduce DTI before applying will get you better terms.

7. What is front-end vs. back-end DTI?

Front-end DTI only includes housing expenses (mortgage, taxes, insurance, HOA). Back-end DTI includes all monthly debt obligations including housing. Lenders evaluate both — with back-end DTI being the more critical number.

8. How fast can I lower my DTI before applying for a mortgage?

Realistically, 60–90 days. Paying off a credit card or eliminating a small installment loan can improve DTI immediately in the next month’s statements. Avoid opening new credit during this period. Use our debt consolidation calculator to model your timeline.

9. Is DTI the same as credit utilization ratio?

No. Credit utilization is the percentage of your available revolving credit you’re using — it directly affects your credit score. DTI is the percentage of your gross income going toward all monthly debt payments. They measure different things, but high balances in either metric signal financial stress to lenders.

10. What is residual income and how does it relate to DTI?

Residual income is the money remaining after subtracting all monthly debt payments and housing expenses from gross income. The VA uses residual income as a primary approval criterion — meaning veterans with DTI above 41% can still qualify if their residual income exceeds VA’s regional minimums by 20% or more. This is the most overlooked mortgage qualification factor in the entire industry.

11. What income counts toward DTI?

Lenders include: salary, hourly wages, overtime (if consistent for 2+ years), bonuses (2-year average), rental income, alimony received, Social Security, and documented self-employment income. Income must be verifiable, stable, and likely to continue. Cash income that isn’t documented on tax returns cannot be counted.

📌 Disclaimer: This article and calculator are for educational and informational purposes only. They do not constitute financial, mortgage, or legal advice. DTI calculations and lender requirements vary by institution, loan product, and individual circumstances. Always consult a licensed mortgage professional or financial advisor before making borrowing decisions. FinanceAuthorityHub.com is not a lender and does not guarantee loan approval based on any DTI calculation.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.