Home Loan Requirements: What Do Lenders Actually Look For in 2026?

Most home loan rejections are preventable. Discover the 6 core requirements lenders evaluate in 2026 — with real numbers, loan comparisons, and fix strategies.

In This Article

Most mortgage rejections happen before applicants even know they were at risk. Understanding exactly what lenders evaluate — and how each factor interacts — is the single biggest edge you can have in today’s competitive housing market.

In 2026, with rates settling near 6.19% (down from over 7% at the start of last year), millions of buyers are re-entering the market. Competition is fierce. Lenders are thorough. Here is everything you need to know to walk in prepared.

Quick Answer: Lenders evaluate six core factors — credit score, debt-to-income ratio (DTI), income stability, down payment, cash reserves, and property value. Meeting minimum thresholds gets you approved. Exceeding them gets you the best rates.

| Factor | Minimum Threshold | Ideal Target |

|---|---|---|

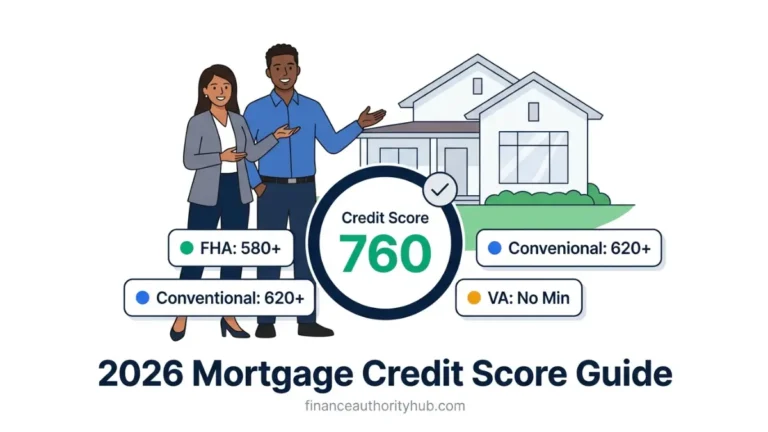

| Credit Score | 500 (FHA) / 620 (Conventional) | 740+ |

| DTI Ratio | Up to 50–55% (FHA) | Below 36% |

| Employment History | 2 years | Consistent, same industry |

| Down Payment | 0% (VA/USDA) | 20% (eliminates PMI) |

| Cash Reserves | 2 months | 4–6 months |

| LTV Ratio | Up to 97% | 80% or below |

Before applying, use the Home Affordability Calculator to understand your realistic price range based on your actual income and debt profile.

The 6 Core Home Loan Requirements Every Lender Evaluates

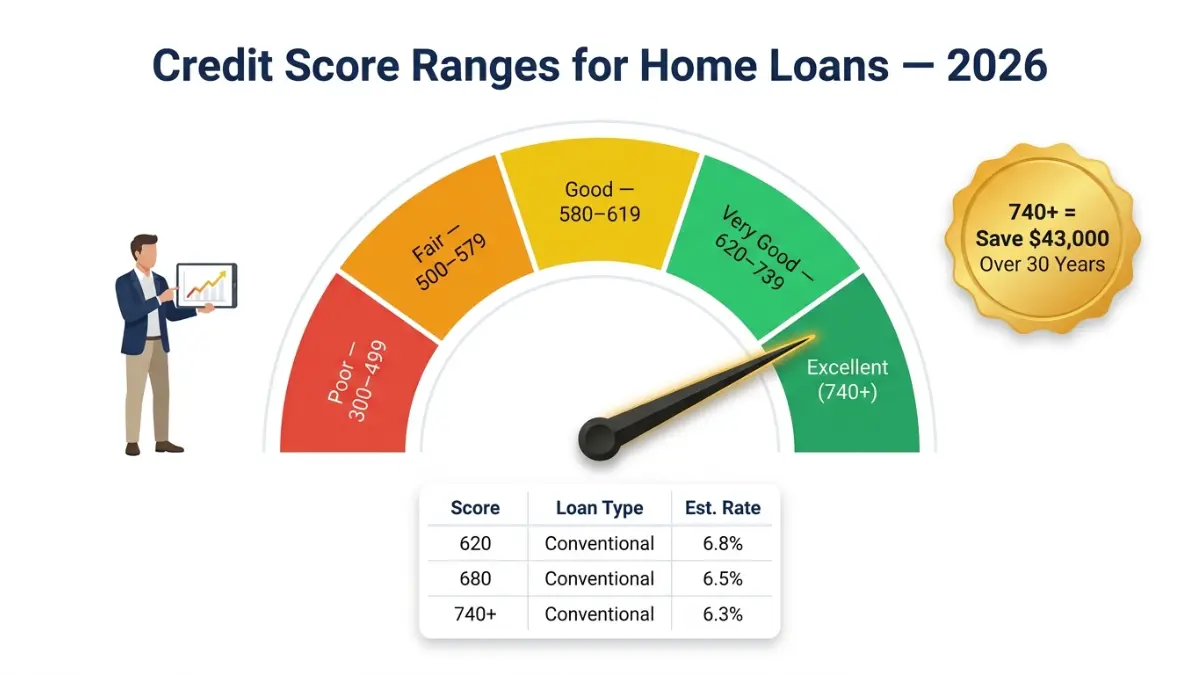

1. Credit Score — The Gateway Number

Your credit score is the first filter every lender applies. It determines not just whether you qualify, but how much your loan will cost you over 30 years.

2026 Minimum Requirements by Loan Type:

| Loan Type | Minimum Score | Down Payment Required |

|---|---|---|

| Conventional | 620 | 3%–20% |

| FHA | 580 (3.5% down) / 500 (10% down) | 3.5%–10% |

| VA | 620 (lender standard) | 0% |

| USDA | 640 | 0% |

| Jumbo | 700+ | 10%–20% |

Why this matters with real numbers: A buyer purchasing a $350,000 home in suburban Dallas with a 620 credit score might get a 6.8% rate. The same buyer with a 740 score could qualify for 6.3% — saving roughly $120/month or $43,000 over 30 years. According to the Federal Reserve Bank of New York, super-prime borrowers with scores of 720+ received the majority of new mortgage originations in recent quarters.

Fast fixes if your score needs work:

- Pull all three bureau reports free at AnnualCreditReport.com — dispute any errors immediately

- Pay revolving balances below 30% utilization

- Do NOT close old accounts — length of credit history matters

- Avoid new credit applications for 90+ days before applying

Use the Credit Score Calculator to model the impact of different scores on your loan options.

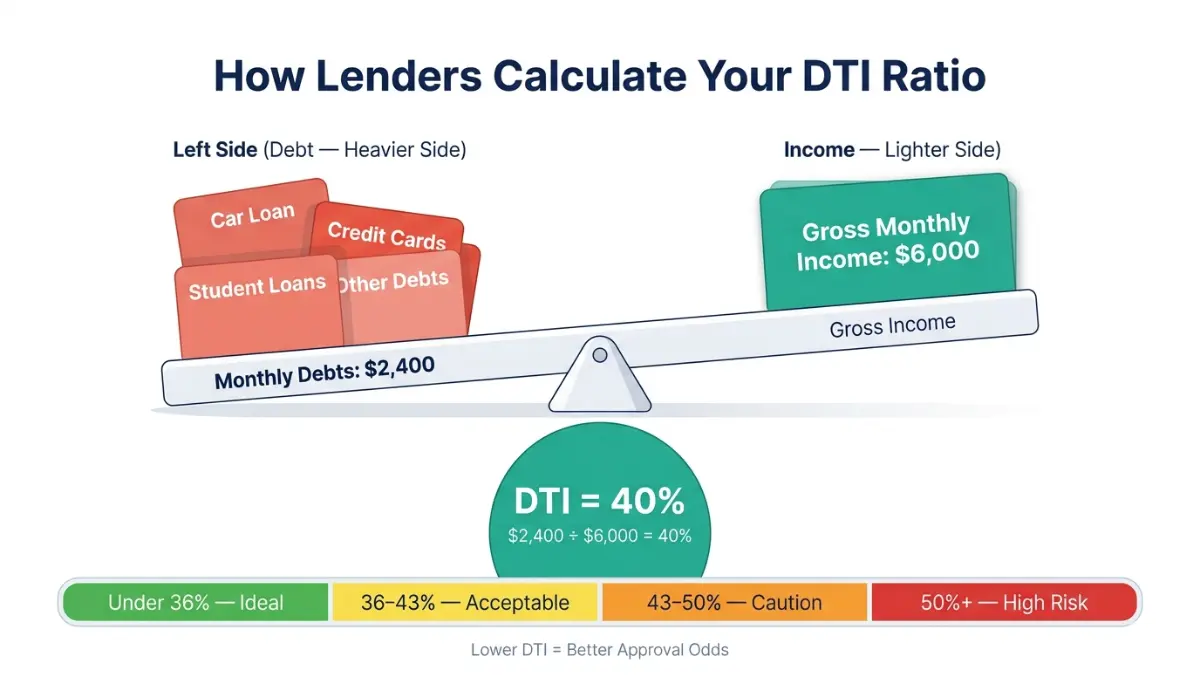

2. Debt-to-Income Ratio (DTI) — The Silent Dealbreaker

DTI is the #1 reason pre-approvals fall apart. Most applicants track their credit score but ignore this number entirely.

How to calculate your DTI:

Total Monthly Debt Payments ÷ Gross Monthly Income × 100 = DTI%

Example: $6,000 gross income / $2,400 monthly debts (mortgage + car + credit cards) = 40% DTI

2026 DTI Limits by Loan Type:

| Loan Type | Ideal DTI | Maximum Allowed |

|---|---|---|

| Conventional (manual) | 36% | 45% |

| Conventional (automated/DU) | 36% | 50% |

| FHA | 43% | 55% (with compensating factors) |

| VA | 41% | Flexible with residual income |

| USDA | 41% | 43–45% |

Per Fannie Mae’s official Selling Guide, automated underwriting (Desktop Underwriter) can approve DTIs up to 50% when borrowers have strong credit scores and meaningful cash reserves. This is where many qualified buyers actually get through when they’d otherwise be rejected.

What counts as monthly debt: car loans, student loans, credit card minimums, personal loans, child support, alimony — every recurring obligation.

Run your numbers instantly with the Debt-to-Income Ratio Calculator before you speak to a single lender.

3. Income and Employment History — Consistency Is King

Lenders don’t just want to know how much you earn. They want proof your income is stable, verifiable, and likely to continue.

Standard requirement: 2 years of consistent employment history in the same field.

What income lenders will count:

- Base salary and wages

- Documented overtime and bonuses (2-year average)

- Self-employment income (net, from tax returns)

- Rental income (typically 75% of gross)

- Social Security, disability, pension (must continue 3+ years)

- Investment/dividend income

- Alimony and child support (with legal documentation)

Self-employed borrowers face extra scrutiny. Lenders require 2 years of personal AND business tax returns, a year-to-date profit and loss statement, and sometimes a CPA letter confirming business stability. The critical trap: writing off too many expenses reduces your taxable income — and the income lenders use to qualify you. Learn more about navigating this through the SBA’s resource center.

Job changes are a red flag — especially if you switch industries during underwriting. Promotions or raises within the same field are generally fine. Switching from W-2 employment to self-employment right before closing can kill your application entirely.

For a broader picture of how income connects to mortgage costs, read How Does a Home Loan Work on our site.

4. Down Payment — More Paths Than You Think

The “20% rule” is a myth for many buyers. Multiple 2026 loan programs require far less — or nothing at all.

2026 Down Payment Requirements:

| Loan Type | Minimum Down | PMI Required? | Notes |

|---|---|---|---|

| Conventional | 3% | Yes, if < 20% | 20% eliminates PMI |

| FHA | 3.5% (score 580+) | Yes (MIP) | 10% if score 500–579 |

| VA | 0% | No | Veterans/active military only |

| USDA | 0% | No (guarantee fee instead) | Rural/suburban areas |

| Jumbo | 10%–20% | Varies | Above $832,750 in most areas |

2026 Conforming Loan Limits (per FHFA):

- Standard U.S. counties: $832,750

- High-cost areas (CA, NY, WA, DC metro): $1,249,125

- FHA standard limit: $541,287

Gift funds are allowed — but must be documented with a gift letter confirming the money is not a loan. Conventional loans allow gifts from family members; FHA loans allow gifts from employers, unions, and qualified first-time homebuyer programs.

Use the Down Payment Calculator to see exactly how different down payment amounts affect your monthly payment and total interest paid. Also explore the Down Payment Help Guide for assistance programs available in 2026.

5. Cash Reserves — Your “Safety Net” Score Booster

Having 2–6 months of mortgage payments in reserves after closing significantly strengthens your application — and can compensate for a higher DTI or slightly lower credit score.

What counts as reserves:

- Checking and savings accounts

- Investment and brokerage accounts

- Vested 401(k) or IRA funds (usually 60–70% counted)

- Certificates of deposit

What does NOT count: Borrowed funds, unsourced cash deposits, funds needed for down payment or closing costs.

Lenders will want 2–3 months of statements for all financial accounts. Large unexplained deposits are a red flag — they trigger sourcing requirements that can delay or derail your closing.

6. Property Appraisal and LTV Ratio

The home itself must pass lender scrutiny. No matter how strong your financials are, the property must appraise at or above the purchase price.

Loan-to-Value (LTV) Ratio = Loan Amount ÷ Appraised Property Value

| LTV | Meaning | PMI Impact |

|---|---|---|

| 80% or lower | Strong — no PMI on conventional | Best rates |

| 81–95% | Acceptable — PMI typically required | Higher monthly cost |

| 96–97% | Minimum for most conventional programs | Maximum PMI |

| 100%+ | Only VA/USDA eligible | Strict eligibility |

The Consumer Financial Protection Bureau’s appraisal guide explains your rights as a borrower — including the requirement that lenders provide you with a free copy of any appraisal ordered on your behalf.

Use the Loan to Value Calculator to check your current LTV before applying.

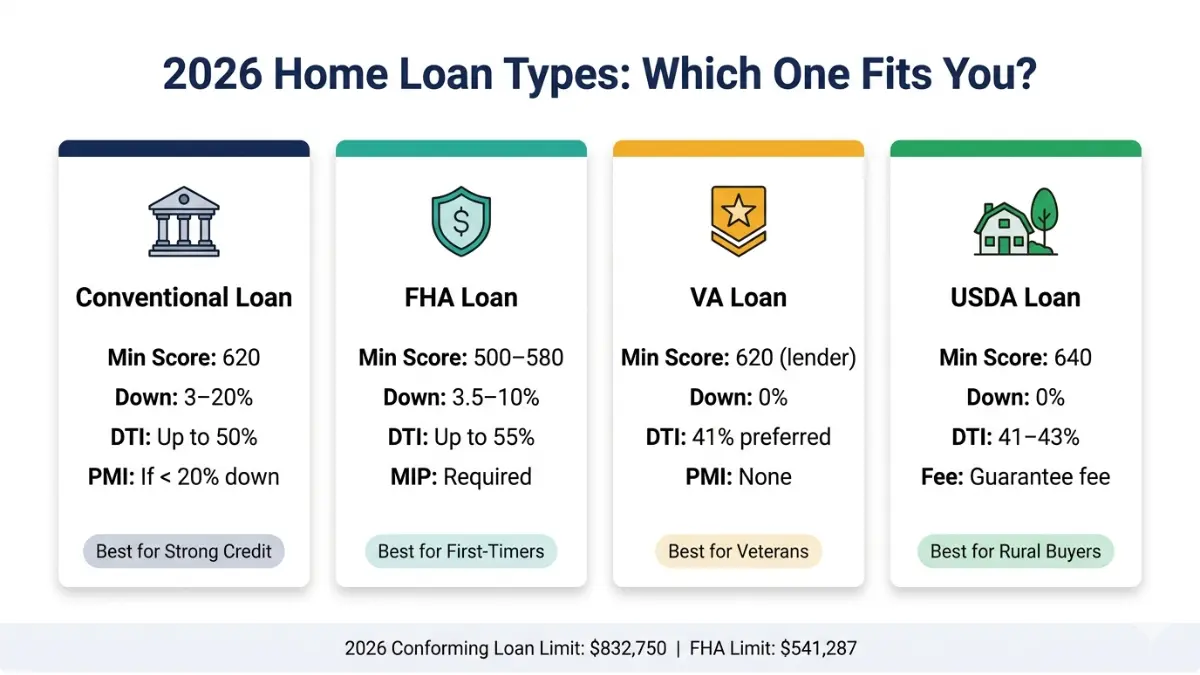

Conventional vs. FHA vs. VA vs. USDA: Which Requirements Fit Your Profile?

| Factor | Conventional | FHA | VA | USDA |

|---|---|---|---|---|

| Min. Credit Score | 620 | 500–580 | 620 (lender) | 640 |

| Down Payment | 3%–20% | 3.5%–10% | 0% | 0% |

| DTI Maximum | 45–50% | 43–55% | 41% preferred | 41–43% |

| Mortgage Insurance | PMI if < 20% | MIP (required) | None | Guarantee fee |

| Best For | Strong credit borrowers | First-timers, lower credit | Veterans, active military | Rural/suburban buyers |

| 2026 Loan Limit | $832,750 | $541,287 | No limit (full entitlement) | Area-based |

Which loan is right for you?

- Score below 620 + limited savings? → FHA is your best path

- Veteran or active service member? → VA loan — zero down, no mortgage insurance

- Buying in a rural or suburban area with modest income? → USDA may qualify you for 0% down

- Strong credit + stable income? → Conventional gives you the most flexibility and lowest long-term cost

Before choosing, compare loan costs using the Mortgage Calculator and review Types of Home Loans for a full breakdown of every available program.

For refinancing an existing loan, the Mortgage Refinance Calculator shows your break-even point and total savings.

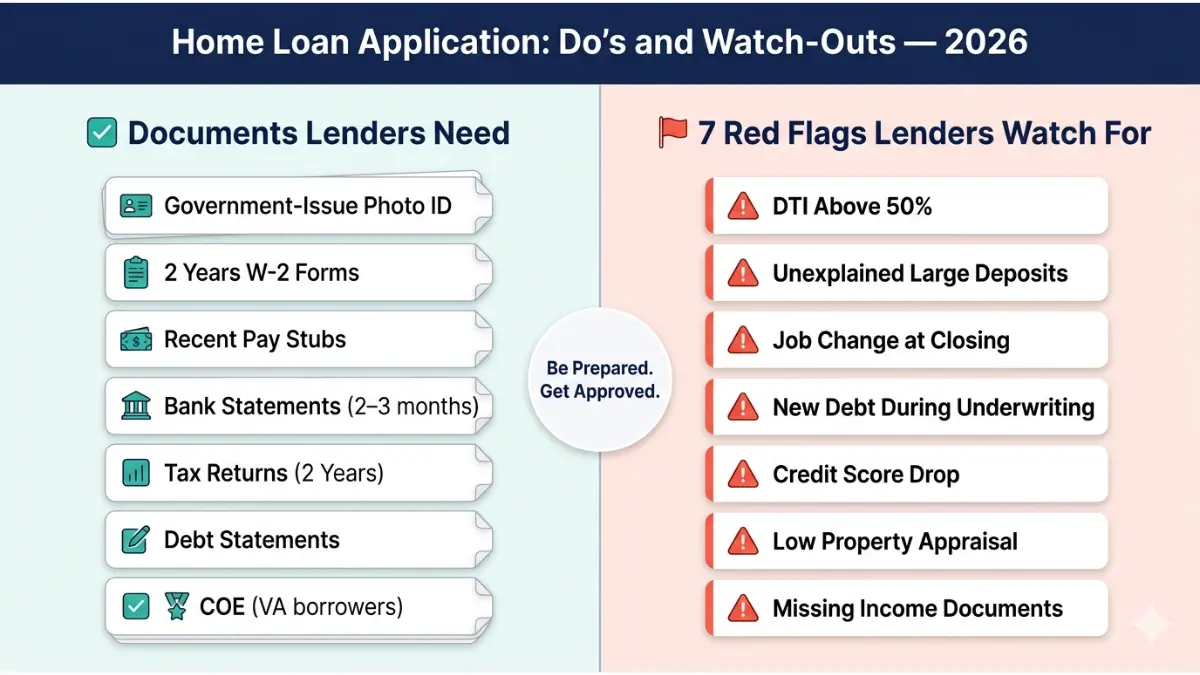

Complete 2026 Document Checklist + 7 Red Flags That Kill Applications

Master Document Checklist

Identity Verification:

- Government-issued photo ID (driver’s license or passport)

- Social Security Number or ITIN

Income Documentation:

- Last 2 pay stubs (most recent)

- 2 years of W-2 forms

- 2 years of federal tax returns (all pages)

- Year-to-date profit & loss statement (self-employed)

- Business tax returns, 2 years (self-employed)

- Award letters for Social Security, disability, or pension income

Employment:

- Current employer’s name, address, and contact information

- 2-year employment and residence history

Assets:

- 2–3 months bank statements (checking, savings, all accounts)

- Most recent retirement account statements (401k, IRA)

- Investment account statements

- Gift letter (if using gifted funds)

Debts:

- Auto loan, student loan, and credit card statements

- Any existing mortgage statements

Loan-Specific Extras:

- VA: Certificate of Eligibility (COE) + DD-214 discharge papers

- USDA: Income eligibility documentation

The CFPB’s Mortgage Key Terms guide is a reliable free resource for understanding every document’s purpose in the process.

7 Red Flags That Trigger Mortgage Rejections

1. DTI above 50% with no compensating factors A high ratio with nothing to offset it — no reserves, no high credit score — almost always results in denial.

2. Unexplained large bank deposits Any deposit over 50% of monthly income that can’t be sourced raises underwriting red flags. Document everything.

3. Job change within 60 days of closing Switching employers — especially industries — can force a full re-underwrite. Notify your lender immediately if this happens.

4. New debt opened during underwriting Taking on a car loan or opening a new credit card between pre-approval and closing directly increases your DTI and can void your approval.

5. Credit score drop before closing Lenders pull your credit again before funding. A score drop — even 10 points — can change your rate or kill your loan.

6. Property appraisal below purchase price If the home appraises under the agreed price, you must renegotiate, increase your down payment, or walk away.

7. Inconsistent or missing income documentation Gaps, discrepancies between tax returns and pay stubs, or income that can’t be verified are among the most common reasons for delays and denials.

If debt load is part of your concern, the Debt Consolidation Calculator can show whether consolidating existing obligations before applying would lower your DTI enough to qualify.

How to Strengthen Your Home Loan Application Before You Apply

Fix Your Credit Score (3–12 Months Out)

- Pull all three reports free at AnnualCreditReport.com — errors on up to 20% of reports negatively affect scores

- Dispute inaccuracies with each bureau directly

- Keep credit utilization below 30% on all revolving accounts

- Avoid closing old accounts — credit age is a scoring factor

- Make zero late payments for at least 12 months

A 20-point increase can unlock a meaningfully lower rate. A 60-point increase can shift you from FHA to conventional loan eligibility — saving thousands in mortgage insurance over the life of the loan.

Lower Your DTI Before Applying

- Pay off the smallest debts first — eliminating even a $200/month car payment can move DTI from 47% to 43%

- Add documented income sources — rental income, freelance income, part-time work all count if verifiable

- Do not take on any new debt — not a car, not furniture financing, nothing

- Avoid balance transfers that reset credit card minimums upward

Model the impact of paying off specific debts using the Credit Card Payoff Calculator before deciding which accounts to target first.

Build Your Down Payment and Reserves

- Start with state and local down payment assistance programs — many offer $10,000–$25,000 in grants or forgivable loans for first-time buyers

- Explore the Down Payment Help Guide for 2026-specific programs

- Aim for reserves beyond your down payment — lenders want to see you won’t be wiped out at closing

- Retirement accounts can be accessed in some cases for first-time homebuyers — but IRS rules on early distributions apply and must be factored in

What This Means For You: The 3 Highest-Impact Actions

If you’re serious about buying in 2026, these three moves deliver the most return on effort:

1. Check your credit 6 months early — this gives you enough time to fix errors and improve your score before a lender does a hard pull.

2. Calculate your DTI before talking to any lender — know your number going in. Use the Debt-to-Income Ratio Calculator to see exactly where you stand.

3. Get pre-approved — not just pre-qualified — pre-qualification is a rough estimate. Pre-approval involves verified documentation and is what competitive sellers require. Read the Mortgage Pre-Approval 2026 Guide for a step-by-step walkthrough.

Frequently Asked Questions: Home Loan Requirements

1. What credit score do I need for a home loan in 2026?

The minimum is 500 for FHA loans (with 10% down) and 620 for conventional loans. A score of 740 or higher typically unlocks the best rates and lowest fees.

2. What is the maximum DTI ratio for mortgage approval?

Most lenders prefer 43% or below. FHA loans allow up to 55% with strong compensating factors. Conventional automated underwriting can approve up to 50% with a solid credit profile.

3. How much income do I need to qualify for a home loan?

There is no fixed income minimum. Lenders focus on your DTI ratio and income stability — not a dollar amount. Your income must be verifiable and consistent.

4. How many years of employment do I need for a home loan?

Two years of consistent employment history in the same field is standard. Recent graduates and military members may qualify with less, provided income is well-documented.

5. Can I get a home loan with bad credit?

Yes. FHA loans accept scores as low as 500 with a 10% down payment. VA and USDA loans offer flexible credit paths for eligible borrowers. Expect higher rates and stricter conditions.

6. What documents do I need for a home loan application?

Government-issued photo ID, 2 years of W-2s and tax returns, recent pay stubs, 2–3 months of bank statements, and documentation of all existing debts.

7. How much down payment is required?

VA and USDA loans require 0%. FHA requires 3.5% (score 580+). Conventional loans start at 3%. Putting down 20% eliminates private mortgage insurance entirely.

8. What is the 2026 conforming loan limit?

The baseline is $832,750 for most U.S. counties. High-cost areas reach $1,249,125. FHA’s standard limit is $541,287, rising to $1,249,125 in high-cost markets.

9. Does changing jobs affect mortgage approval?

Yes — significantly. Changing employers during underwriting, especially across industries, is a major underwriting red flag. Always notify your lender immediately if your employment changes.

10. Can self-employed borrowers qualify for a home loan?

Absolutely. Lenders require 2 years of personal and business tax returns showing stable income. Bank statement loans are an alternative if your tax returns underrepresent actual income.

11. What is LTV and why does it matter for home loan approval?

LTV (Loan-to-Value) is your loan amount divided by the home’s appraised value. An LTV of 80% or below eliminates PMI and typically secures better rates. Most conventional programs cap LTV at 97%.

📌 Disclaimer: This article is for educational and informational purposes only. It does not constitute financial, mortgage, or legal advice. Home loan requirements vary by lender, loan program, borrower profile, and location. Always consult a licensed mortgage professional or HUD-approved housing counselor before making borrowing decisions. See financeauthorityhub.com/tools for free financial calculators to support your planning.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.