How Does a Home Loan Work Step by Step? (2026 Guide)

Confused about how a home loan works? This 2026 step-by-step guide covers pre-approval, underwriting, PITI payments, loan types, and closing costs — all in plain English.

In This Article

A home loan works like this: a lender gives you money to buy a property, you repay it in monthly installments over 15–30 years, and the home serves as collateral until the loan is paid off. In 2026, with mortgage rates hovering between 6.25%–7.5%, understanding exactly how the home loan process works — step by step — can save you tens of thousands of dollars.

What Is a Home Loan and How Does It Work?

A home loan (also called a mortgage) is a secured loan used to purchase real estate. The lender advances the full purchase price. You repay it monthly — with interest — over an agreed term, typically 15 or 30 years.

The home is the collateral. If you stop making payments, the lender has the legal right to foreclose and take ownership of the property.

The Core Components of How a Home Loan Works

Every mortgage payment is made up of these building blocks:

| Component | What It Means | Who Benefits |

|---|---|---|

| Principal | The original amount borrowed | You (builds equity) |

| Interest | The lender’s fee for lending money | Lender |

| Property Taxes | Annual taxes held in escrow | Local government |

| Homeowners Insurance | Required coverage for the property | You + lender |

| PMI | Required if down payment < 20% | Lender (protects against default) |

Fixed-Rate vs. Adjustable-Rate Mortgage

- Fixed-rate mortgage: Your interest rate stays the same for the life of the loan. Predictable monthly payments. Best for buyers staying long-term.

- Adjustable-rate mortgage (ARM): Rate is fixed for an initial period (e.g., 5 years), then adjusts annually based on market indexes. Lower starting rate, but carries risk.

What This Means For You: On a $350,000 loan at 6.5% (30-year fixed), your principal + interest payment is approximately $2,212/month. Use our Mortgage Calculator to calculate your exact number based on your loan amount, rate, and term — before you talk to a single lender.

To build a deeper foundation, read our full guide on what is a home loan before diving into the qualification process.

According to Fannie Mae’s homebuyer resource center, understanding terms like principal, interest, and APR before applying gives buyers a measurable advantage in negotiations.

Home Loan Requirements — Can You Qualify in 2026?

Before a lender approves your mortgage, they run a full financial background check. Four factors determine whether you qualify — and at what interest rate.

What Lenders Evaluate

✅ 1. Credit Score Your credit score is the single most powerful number in your mortgage application. It determines not just approval, but the interest rate you receive — and the difference is enormous.

2026 Credit Score → Interest Rate Impact Table

| Credit Score | Typical 2026 Rate | Monthly Payment ($350K, 30-yr) | 30-Year Total Interest |

|---|---|---|---|

| 760+ | ~6.25% | ~$2,156 | ~$426,160 |

| 700–759 | ~6.75% | ~$2,270 | ~$467,200 |

| 660–699 | ~7.25% | ~$2,389 | ~$510,040 |

| Below 660 | ~7.83%+ | ~$2,520+ | ~$557,200+ |

A 760 vs. 660 credit score = $364/month savings = $131,040 saved over 30 years on the same loan.

Before applying, check your standing with our free Credit Score Calculator.

✅ 2. Debt-to-Income Ratio (DTI) Your DTI is calculated by dividing total monthly debt payments by gross monthly income.

- Conventional loans: DTI ≤ 36–45%

- FHA loans: DTI ≤ 43–57%

- VA loans: DTI ≤ 41% preferred

If existing debt is dragging your DTI above lender limits, run your numbers through our Debt-to-Income Ratio Calculator before you apply.

✅ 3. Income & Employment History Lenders require a minimum 2-year employment history. W-2 employees, self-employed borrowers, and contract workers are all evaluated differently. Self-employed applicants typically need 2 years of tax returns showing consistent income.

✅ 4. Down Payment

| Loan Type | Minimum Down | Credit Score Required | PMI Required? |

|---|---|---|---|

| Conventional | 3% | 620 | Yes (if <20%) |

| FHA | 3.5% | 580 | Yes (for loan life) |

| VA | 0% | No minimum | No |

| USDA | 0% | 640 preferred | Low annual fee |

| Jumbo | 10–20% | 700+ | Varies |

What This Means For You: Use our Home Affordability Calculator to find your true purchase price ceiling based on your income, DTI, and down payment savings — before a lender tells you what you qualify for.

The U.S. Department of Housing and Urban Development (HUD) maintains an updated guide on FHA loan requirements, credit standards, and down payment assistance programs by state.

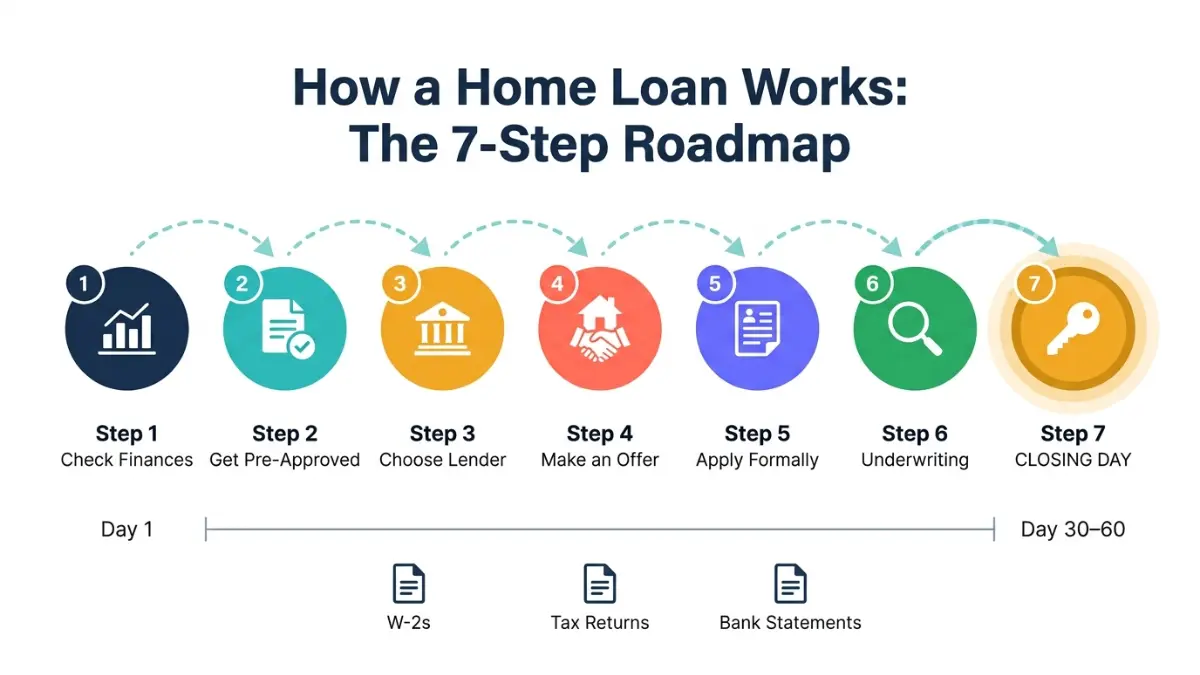

The Home Loan Process — 7 Steps Explained

This is where most buyers feel lost. Here is exactly how the home loan process works, step by step, with realistic timelines for 2026.

Step 1 — Review Your Finances and Credit (Week 1)

Pull your credit reports from all three bureaus (Equifax, Experian, TransUnion) at AnnualCreditReport.com — the only federally authorized free source. Dispute any errors before applying, as corrections can take 30–45 days.

Calculate your DTI, review savings for the down payment and closing costs, and assess whether your credit score needs improvement before applying.

Step 2 — Get Pre-Approved (Not Just Pre-Qualified) (Days 1–3)

Pre-qualification = an informal estimate based on self-reported data. No real weight.

Pre-approval = a lender verifies your income, assets, credit, and issues a written commitment for a specific loan amount. Sellers take pre-approved buyers seriously.

Documents needed for pre-approval:

- Last 2 years of W-2s or tax returns

- Most recent 30 days of pay stubs

- Last 2–3 months of bank statements

- Photo ID and Social Security number

Shop at least 3 lenders — the same borrower profile regularly receives meaningfully different rates across lenders. A 0.5% rate difference on a $400,000 loan = $30,000+ over 30 years.

Our full Mortgage Pre-Approval Guide walks you through exactly what each lender is looking for.

Step 3 — Choose Your Loan Type and Lender (Week 1–2)

Compare fixed vs. adjustable rates, loan terms, and program eligibility. Use our Mortgage Rate Calculator to compare rate scenarios side by side.

Not sure whether a 15-year or 30-year mortgage is smarter for your situation? Read our 15 vs. 30-Year Mortgage Comparison for a data-driven breakdown.

Step 4 — Make an Offer and Sign the Purchase Agreement (Week 2–4)

Work with a buyer’s agent to submit a competitive offer. Your pre-approval letter strengthens your position significantly, especially in low-inventory markets. In 2026, the national housing shortage remains near 3.8 million units — competitive offers are still the norm in desirable areas.

Step 5 — Submit the Full Mortgage Application (Within 3 Business Days of Accepted Offer)

Once your offer is accepted, submit your official mortgage application. Your lender will issue a Loan Estimate within 3 business days — a standardized document showing your interest rate, monthly payment, closing costs, and APR.

Critical: Do NOT open new credit cards, make large purchases, or change jobs during this period. Any change to your financial profile can delay or kill your approval.

Step 6 — Underwriting, Appraisal & Home Inspection (Weeks 3–5)

This is the most complex behind-the-scenes phase.

Underwriting: A licensed underwriter reviews your entire financial profile — income, assets, credit history, employment — to confirm you meet lending standards.

Appraisal: The lender orders an independent appraisal ($300–$600) to confirm the home’s market value supports the loan amount. If the appraisal comes in low, you may need to renegotiate or cover the gap.

Home Inspection: Not required by most lenders, but strongly recommended. An inspector checks the structure, roof, electrical, plumbing, and HVAC. Typical cost: $300–$500.

Mortgage Process Timeline at a Glance:

| Phase | Handled By | Typical Timeline |

|---|---|---|

| Pre-approval | Lender | Same day – 3 days |

| Offer + Contract | Agent + Seller | 1–3 weeks |

| Full Application | Borrower + Lender | Day 1 of contract |

| Underwriting | Underwriter | 1–3 weeks |

| Appraisal | Licensed Appraiser | 1–2 weeks |

| Clear to Close | Lender | Day 30–45 |

| Closing | Title Company | Day 30–60 |

The Consumer Financial Protection Bureau’s mortgage process guide is an excellent free resource that explains every stage in plain language, including your legal rights as a borrower.

Step 7 — Closing Day — You Get the Keys (Day 30–60)

On closing day, you’ll sign the final documents, pay your down payment and closing costs, and take legal ownership. Bring a government-issued photo ID and a cashier’s check or confirmation of wire transfer.

Three days before closing, you’ll receive a Closing Disclosure — review it line by line and verify it matches your Loan Estimate. If anything changed without explanation, ask your lender immediately.

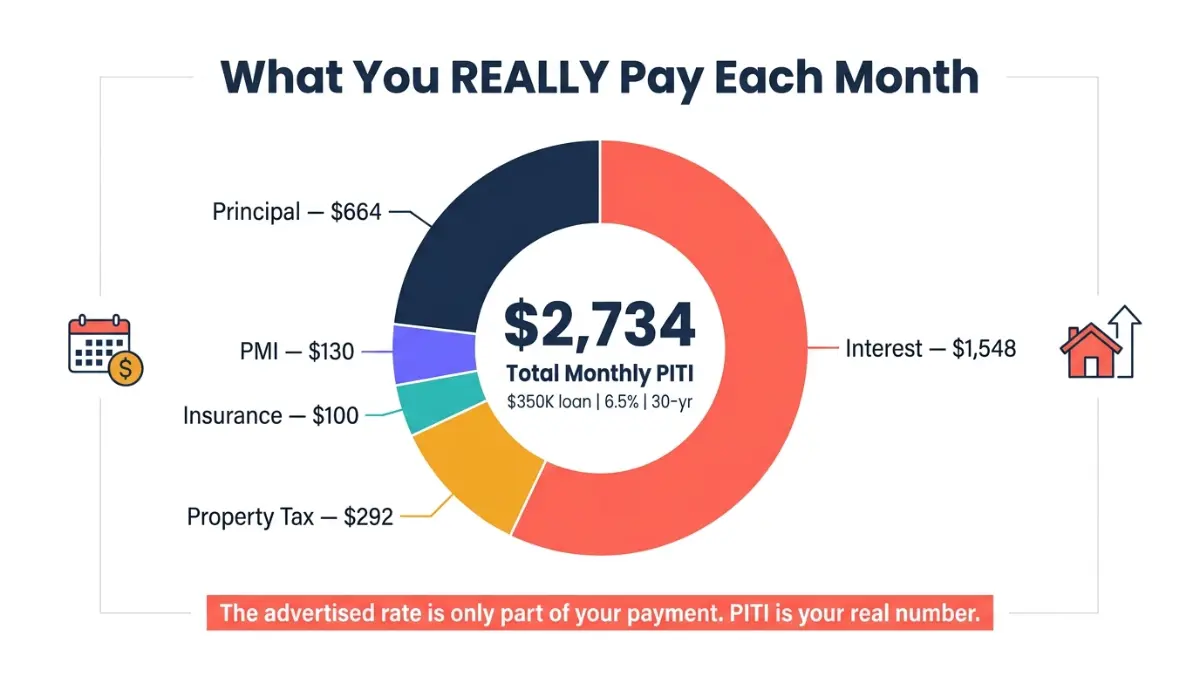

How Your Monthly Mortgage Payment Is Calculated (PITI Breakdown)

Most buyers focus only on the advertised interest rate. The real monthly cost is higher — because a home loan payment includes four components, commonly called PITI.

Real Example: $350,000 Home | 10% Down | 6.5% Rate | 30-Year Fixed

| Component | Monthly Amount | Notes |

|---|---|---|

| Principal | ~$664 | Builds your equity over time |

| Interest | ~$1,548 | Decreases slowly over loan life |

| Property Taxes | ~$292 | National average (~1% of value/year) |

| Homeowners Insurance | ~$100 | Lender-required |

| PMI | ~$130 | Required with <20% down payment |

| Total Monthly PITI | ~$2,734 | Your real out-of-pocket cost |

This means the “advertised” $2,212/month (P+I only) becomes $2,734/month in real terms. Many first-time buyers are blindsided by this gap.

How Amortization Works

Amortization is the process of spreading loan repayments over time. In the early years, the majority of each payment goes toward interest — not principal.

- Year 1: ~70% of each payment goes to interest

- Year 15: The split is roughly equal

- Year 25+: Most of each payment goes to principal (equity-building accelerates)

Use our Amortization Calculator to see the exact breakdown year by year for your loan amount — a table no lender will voluntarily hand you.

When Can You Remove PMI?

PMI is automatically canceled when your loan-to-value (LTV) ratio reaches 78% (i.e., you’ve built 22% equity). You can request cancellation at 80% equity, which can happen faster if your home value increases. Use our Loan to Value Calculator to track your LTV.

What This Means For You: Your real home loan cost is PITI — not the P+I figure the bank advertises. Always budget for the full number. The CFPB’s guide on escrow accounts explains exactly how lenders collect and pay your taxes and insurance on your behalf.

Types of Home Loans — Which One Is Right for You in 2026?

Choosing the wrong loan type costs tens of thousands of dollars. Here is the complete 2026 comparison no competitor publishes.

2026 Home Loan Comparison Table

| Loan Type | Min Credit Score | Min Down | PMI Required | Best For | 2026 Loan Limit |

|---|---|---|---|---|---|

| Conventional | 620 | 3% | Yes (<20%) | Good credit buyers | $806,500 |

| FHA | 580 | 3.5% | Yes (for loan life) | First-time buyers, lower credit | $498,257–$1,209,750 |

| VA | No minimum | 0% | No | Veterans & active military | No national limit |

| USDA | 640 preferred | 0% | Small annual fee | Rural/suburban buyers | Area-based |

| Jumbo | 700+ | 10–20% | Varies | Loans above $806,500 | Lender-defined |

2026 Conforming Loan Limit: $806,500 (standard markets) | $1,209,750 (high-cost areas like parts of California, New York, and Hawaii).

How to Choose the Right Loan Type

- You’re a veteran or active military? VA loan is almost always the best option — $0 down, no PMI, and competitive rates make it the single most valuable mortgage benefit available in the U.S.

- First-time buyer with limited savings? FHA or Conventional 97 (3% down) are the most accessible paths. Check our Buy First Home 2026 Guide for a full strategy.

- Buying in a rural or suburban area? USDA loans offer 0% down with low ongoing costs — far more properties qualify than most buyers realize.

- Home price above $806,500? You’ll need a jumbo loan. Stronger credit and larger reserves are required.

For a deeper side-by-side breakdown of every loan type, see our Types of Home Loans guide.

The VA Home Loans program page at VA.gov and USDA Rural Development at rd.usda.gov are the authoritative sources for program eligibility, both updated for 2026.

Closing Costs, First-Timer Mistakes & Your Action Plan

Closing costs are the most underestimated expense in the entire home loan process. Most first-time buyers budget for the down payment — and forget that closing day brings a separate bill.

Closing Costs Breakdown: What You’ll Actually Pay

| Fee | Typical Range | Notes |

|---|---|---|

| Loan Origination Fee | 0.5%–1% of loan | Lender’s processing charge |

| Home Appraisal | $300–$600 | Required by lender |

| Title Insurance | $500–$1,500 | Protects against title disputes |

| Title Search | $200–$400 | Verifies ownership history |

| Escrow / Settlement Fee | $500–$800 | Paid to title/closing company |

| Prepaid Interest | Varies | Interest from closing date to month-end |

| Homeowners Insurance (Prepaid) | $800–$1,500 | 1-year policy paid upfront |

| Total Estimated Closing Costs | 2%–5% of loan amount | On $350K loan = $7,000–$17,500 |

Use our Closing Cost Calculator to get a personalized estimate based on your loan amount and state.

Pro Tip: In 2026’s more balanced market, negotiating seller credits to cover 1–2% of closing costs is common — especially on existing homes. That’s $3,500–$7,000 you don’t pay out of pocket.

5 Costly Mistakes First-Time Buyers Make

- Skipping rate comparison: Not shopping 3+ lenders costs an average of $1,500–$3,000+ in the first year alone. Always compare a bank, a credit union, and an online lender.

- Confusing pre-qualification with pre-approval: Pre-qual is essentially meaningless in a competitive market. Pre-approval is the only number that matters.

- Opening new credit during the loan process: A new credit card or car loan mid-process changes your DTI and can collapse your approval. Freeze all new credit from pre-approval through closing.

- Forgetting closing costs in the budget: If you’re buying a $350,000 home with 3% down ($10,500), add $7,000–$17,500 in closing costs. Total cash needed at closing: potentially $28,000+.

- Choosing a loan term without running the numbers: A 15-year mortgage saves massive interest but has higher monthly payments. Use our Mortgage Calculator to stress-test both scenarios against your budget.

If existing debt is limiting your purchasing power, our Debt Consolidation Guide shows proven strategies to reduce DTI before applying.

Your 5-Step Home Loan Action Plan

1. Check your credit score today and dispute any errors — allow 30–45 days for corrections before applying.

2. Calculate your true DTI with our Debt-to-Income Ratio Calculator and confirm it’s below 43%.

3. Use the Home Affordability Calculator to set a realistic price ceiling before speaking with any agent or lender.

4. Get pre-approved from at least 3 lenders — compare Loan Estimates line by line, not just the quoted interest rate.

5. If you need personalized guidance on programs, down payment assistance, or credit counseling, connect with a HUD-approved housing counselor — free of charge.

For buyers also evaluating whether to rent first, our Rent vs. Buy Calculator runs the full long-term financial comparison for your specific market.

Frequently Asked Questions (FAQs)

1. How does a home loan work step by step?

You get pre-approved → find a home → apply formally → the lender underwrites and appraises the property → you close. The full process typically takes 30–60 days from accepted offer.

2. What credit score do I need for a home loan?

Minimum 620 for conventional loans, 580 for FHA, and no set minimum for VA. The higher your score, the lower your rate and total cost.

3. How much down payment do I need for a home loan?

As little as 3% (conventional), 3.5% (FHA), or 0% (VA and USDA). Putting down less than 20% adds PMI to your monthly payment.

4. What is the difference between pre-qualification and pre-approval?

Pre-qualification is an informal estimate. Pre-approval is a verified commitment from a lender after reviewing your income, credit, and assets — the only version sellers respect.

5. How is my monthly mortgage payment calculated?

Your payment includes principal, interest, property taxes, homeowners insurance, and PMI if applicable (PITI). The advertised P+I rate is never the full monthly number.

6. What are typical closing costs on a home loan?

Generally 2%–5% of the loan amount. On a $350,000 loan, expect $7,000–$17,500 due at closing, on top of your down payment.

7. How long does mortgage underwriting take?

Typically 1–3 weeks. Delays happen when documents are missing or income is complex (self-employed, commission-based, etc.). Respond to lender requests immediately.

8. Can I get a home loan with bad credit?

Yes. FHA loans accept scores as low as 580 (3.5% down) or 500 (10% down). VA loans have no credit score minimum set by the government, though individual lenders set overlays.

9. What is PMI and when can I remove it?

Private Mortgage Insurance protects the lender if you default. Required when down payment is less than 20%. You can request cancellation at 80% LTV; it auto-cancels at 78%.

10. What happens at mortgage closing?

You sign all final loan documents, pay your down payment and closing costs, and receive the deed. You should receive and review the Closing Disclosure 3 business days before this date.

11. Should I choose a 15-year or 30-year home loan?

A 30-year loan offers lower monthly payments; a 15-year loan saves significantly on total interest paid. On a $350,000 loan, a 15-year at 5.75% saves approximately $140,000 in interest vs. a 30-year at 6.5%. Run both scenarios in our Mortgage Calculator.

Disclaimer: This article is for educational purposes only and does not constitute financial, mortgage, or legal advice. Mortgage rates, loan limits, and program eligibility are subject to change. All rate and payment examples are illustrative based on 2026 market data. Consult a licensed mortgage professional or HUD-approved housing counselor before making any home loan decision.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.