Business Loan Calculator: See Exact Cost (2026)

Business Loan Calculator

Estimate payments and total cost for standard amortized loans, interest-only periods, and balloon structures (common in commercial lending).

Inputs

Interest-only and balloon loans are common in commercial lending and change how cashflow looks. [web:103][web:102]

Business loans can include fees that effectively increase the “real” cost of borrowing; this tool includes fees in the total cost view. [web:107]

Results

Loan principal used (includes rolled fees)

—

Fees: — (—)

Interest-only payment (if enabled)

—

Amortizing payment (planned)

—

Balloon

—

Balloon actually paid

—

Payoff

—

Payments/months: —

Totals (estimate)

Total interest: —

Total cost (payments + upfront fees): — • Upfront fees: —

Yearly amortization summary

| Year | Paid | Principal | Interest | Extra paid | Ending balance |

|---|

Monthly schedule

| Month | Type | Payment | Principal | Interest | Extra | Balance |

|---|

Results appear after you click “Calculate.”

A business loan calculator instantly shows your monthly payment, total interest charged, and the true cost of borrowing — including fees. Enter your loan amount, APR, and term to get a full amortization breakdown in seconds. Use this data to plan cash flow, compare lenders, and avoid hidden cost surprises before you sign anything.

What Makes This Business Loan Calculator Different

Most calculators online give you one number: an estimated monthly payment. That’s not enough information to make a smart borrowing decision.

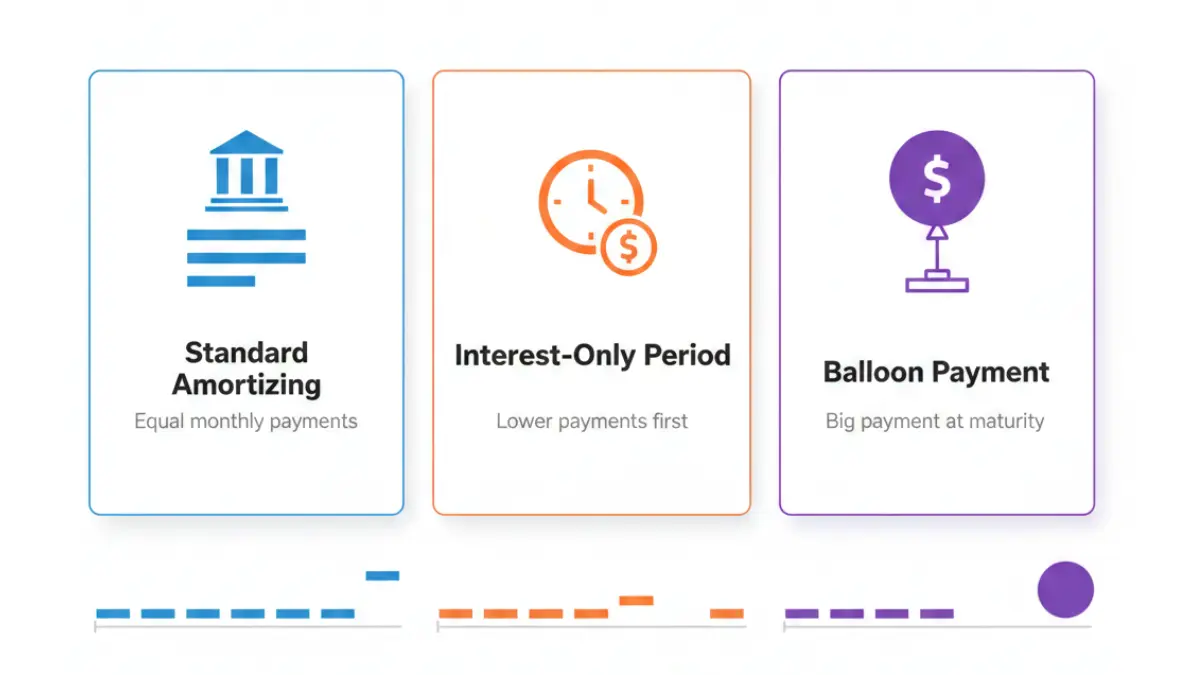

This business loan calculator goes further. It handles three loan structures that dominate commercial lending in 2026 — and that no top competitor’s tool covers:

- Standard amortizing loans — equal monthly payments, principal + interest

- Interest-only loans — lower initial payments, then full amortization

- Balloon payment loans — reduced monthly payments with a lump sum due at the end

Additional features your lender won’t volunteer:

- Fee rolling — see exactly how rolling origination fees into the loan changes your total cost

- Extra monthly payments — see how paying $200/month more saves you thousands

- CSV export — download your full amortization schedule to share with your accountant or bank

- Multi-currency support — USD, GBP, CAD, AUD, EUR, INR and 16 more currencies

What This Means For You: Most business owners use a loan calculator to get a monthly payment. Smart business owners use it to understand the total cost — and then negotiate better terms.

How to Use This Business Loan Calculator (Step-by-Step)

Getting an accurate result takes under two minutes. Here’s exactly what each field means and why it matters.

Step 1 — Select your currency. The calculator supports 22 currencies. US-based businesses select USD by default.

Step 2 — Enter your loan amount. This is the principal you’re requesting. Example: $75,000.

Step 3 — Enter the APR (Annual Percentage Rate). Use the APR, not just the interest rate. The APR includes fees in the annualized cost. If your lender only quotes an interest rate, see the APR section below to understand the difference.

Step 4 — Enter your term in months. A 5-year loan = 60 months. A 7-year loan = 84 months.

Step 5 — Enter any origination or closing fees. This is where most calculators fail you. Entering your fees and choosing whether to roll them in or pay upfront will show you the true total cost of the loan — not just the interest.

Step 6 — Choose your loan structure (optional but important for commercial loans):

- Enable interest-only and enter how many months before amortization begins

- Enable balloon payment and enter the lump sum due at the end

Step 7 — Add extra monthly payments (optional). Even $100–$200 extra per month can cut months off your term and save thousands in interest.

Step 8 — Click Calculate. Your results appear instantly below the calculator.

Understanding Your Results

| Result Card | What It Tells You |

|---|---|

| Monthly payment | Your exact required payment per period |

| Total interest | The full interest cost over the loan’s life |

| Total cost | Principal + interest + all fees combined |

| Payoff date | The exact month your loan is paid off |

| Yearly summary table | Year-by-year breakdown of principal vs. interest |

| Monthly schedule | Every single payment, downloadable as CSV |

The Fee Rolling Decision — What No One Explains

When a lender charges a 2% origination fee on a $100,000 loan, that’s $2,000 due at closing.

Option A — Pay upfront: Your loan principal stays at $100,000. You pay $2,000 out of pocket at closing.

Option B — Roll into loan: Your loan principal becomes $102,000. You pay zero at closing but now pay interest on that extra $2,000 for the entire loan term.

On a 5-year loan at 10% APR, rolling in a $2,000 fee costs you approximately $580 in extra interest. For larger fees, this difference is significant. Use our Debt Consolidation Calculator to model the full picture if you’re refinancing existing debt alongside a new loan.

Pro Tip: Always download the CSV and hand it to your accountant. Lenders are not required to show you a complete amortization schedule before you sign — but you can demand one.

Which Business Loan Type Are You Calculating?

The structure of your loan determines which calculator fields you need. Here’s how to match your loan type to the right inputs.

Standard Amortizing Loans

This covers the majority of small business term loans, including SBA 7(a) loans, bank term loans, and credit union business loans.

How they work: Each monthly payment includes both principal and interest. Early payments are mostly interest. Later payments are mostly principal. By your final payment, your balance reaches exactly zero.

Use the calculator: Enter loan amount + APR + term. Leave interest-only and balloon fields disabled.

Interest-Only Business Loans

An interest-only period means you pay only the interest for a set number of months — your principal doesn’t decrease during that time. After the IO period ends, your payments jump to cover the remaining balance.

Who uses them: Commercial real estate investors, businesses expecting rapid near-term revenue growth, and seasonal businesses that need lower payments during slow periods.

The catch: Your total interest cost is higher than a standard loan of the same amount. You’re delaying principal repayment, which means interest accumulates longer. No top-ranking competitor explains this trade-off.

Use the calculator: Enable interest-only, enter the number of IO months (e.g., 12), then let the calculator show you the two payment amounts: IO payment vs. amortizing payment.

Balloon Payment Loans

A balloon loan has lower monthly payments for most of the term, then requires a large lump-sum payment at the end.

Common in: Commercial real estate loans, equipment financing, and business acquisition loans.

Example: A $500,000 commercial loan at 8% over 10 years with a $150,000 balloon. Your monthly payments are calculated as if the loan were fully amortizing, but you only pay down to $150,000 — the balloon is due at maturity.

Use the calculator: Enable balloon, enter the expected balloon amount, and your monthly payment and true total cost will calculate automatically.

SBA Loan Calculator

SBA 7(a) loan interest rates are negotiated between borrower and lender but subject to SBA maximums, which are pegged to the prime rate. Rates may be fixed or variable.

The current prime rate as of February 2026 is 6.75%, meaning SBA 7(a) fixed rates can range between 9.75% and 14.75% depending on your loan terms. Use this range to model best-case and worst-case scenarios in the calculator before your lender quotes you a rate.

If you’re also financing commercial property, compare borrowing costs side-by-side using our Mortgage Calculator and Home Affordability Calculator.

What Your Business Loan Really Costs in 2026

This is the section every competitor skips. Monthly payment is not cost. Total cost is cost.

APR vs. Interest Rate — The Difference That Costs Borrowers Thousands

Many lenders advertise an interest rate. The APR is always higher — and it’s the number that actually matters.

- Interest rate = the annual percentage of principal charged as interest only

- APR = interest rate + origination fees + guarantee fees + any other lender charges, annualized

For a complete breakdown of this critical distinction, read our expert guide on APR vs. interest rate — one of the most common traps business owners fall into.

Key Takeaway: Always ask your lender for the APR, not just the interest rate. Use the APR in this business loan calculator for accurate results.

How Fees Change Your True Loan Cost — Real Example

Scenario: $100,000 business loan, 10% APR, 5-year term (60 months), 2% origination fee ($2,000).

| Fee Scenario | Monthly Payment | Total Interest | Total Cost |

|---|---|---|---|

| No fees | $2,125 | $27,482 | $127,482 |

| $2,000 fee, paid upfront | $2,125 | $27,482 | $129,482 |

| $2,000 fee, rolled into loan | $2,167 | $28,063 | $130,063 |

Rolling in fees costs an additional $581 over the loan life. On larger loans with higher fees, this gap is much larger. The business loan payment calculator above handles all three scenarios automatically.

Factor Rate Loans vs. APR — What Most Small Business Owners Miss

Merchant cash advances and some short-term online lenders don’t use APR. They use factor rates (e.g., 1.25).

How to convert a factor rate to real cost:

- Loan: $50,000 at factor rate 1.3

- Total repayment = $50,000 × 1.3 = $65,000

- That’s $15,000 in fees on a 12-month term = approximately 30% effective APR

Factor rate products can have effective APRs exceeding 50–80%. The Federal Reserve’s E.2 Survey of Business Lending publishes quarterly data on commercial loan costs and is the most reliable government source for benchmarking whether your rate is reasonable.

Key Takeaway: If your lender quotes a factor rate, not an APR, calculate the effective APR before signing. Use the total repayment amount, subtract the principal, and divide by the term.

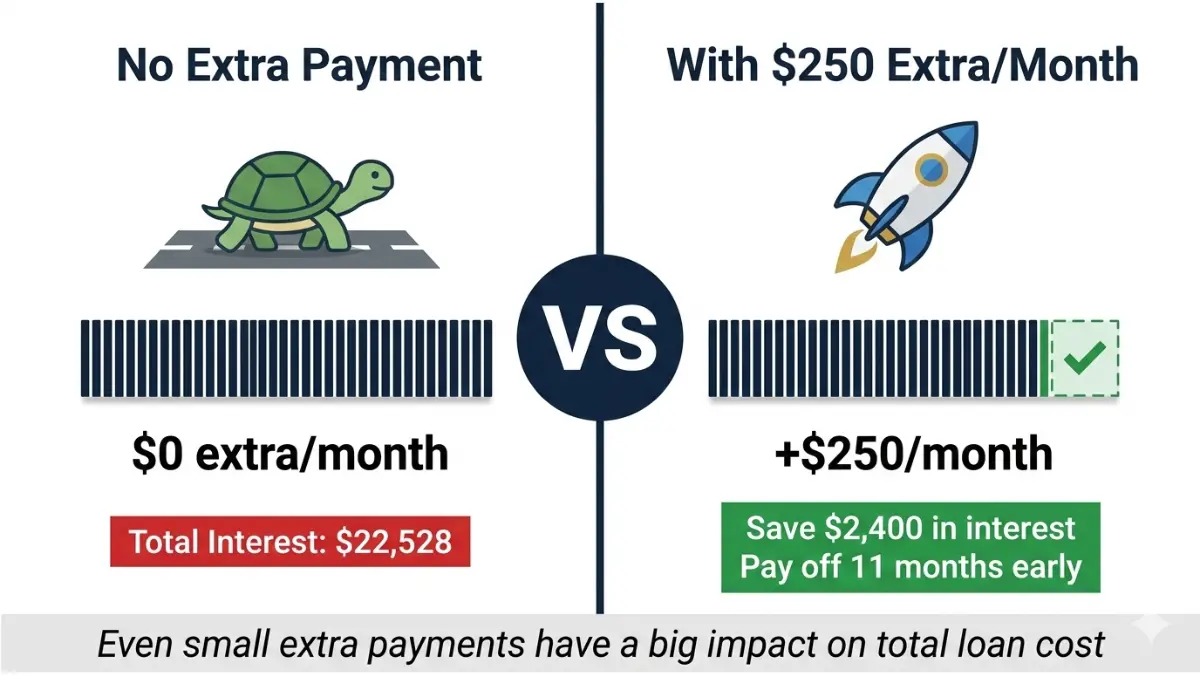

How Extra Monthly Payments Save You Thousands

This is one of the most underused features of any business loan payment calculator.

Example: $75,000 loan, 10.5% APR, 60-month term.

| Extra Payment | Monthly Total | Months Saved | Interest Saved |

|---|---|---|---|

| $0 extra | $1,614 | — | — |

| $100 extra | $1,714 | ~5 months | ~$1,100 |

| $250 extra | $1,864 | ~11 months | ~$2,400 |

| $500 extra | $2,114 | ~18 months | ~$3,800 |

Business Loan Interest Rates in 2026: What to Expect

Understanding current rate ranges helps you evaluate whether your lender’s offer is competitive before you commit.

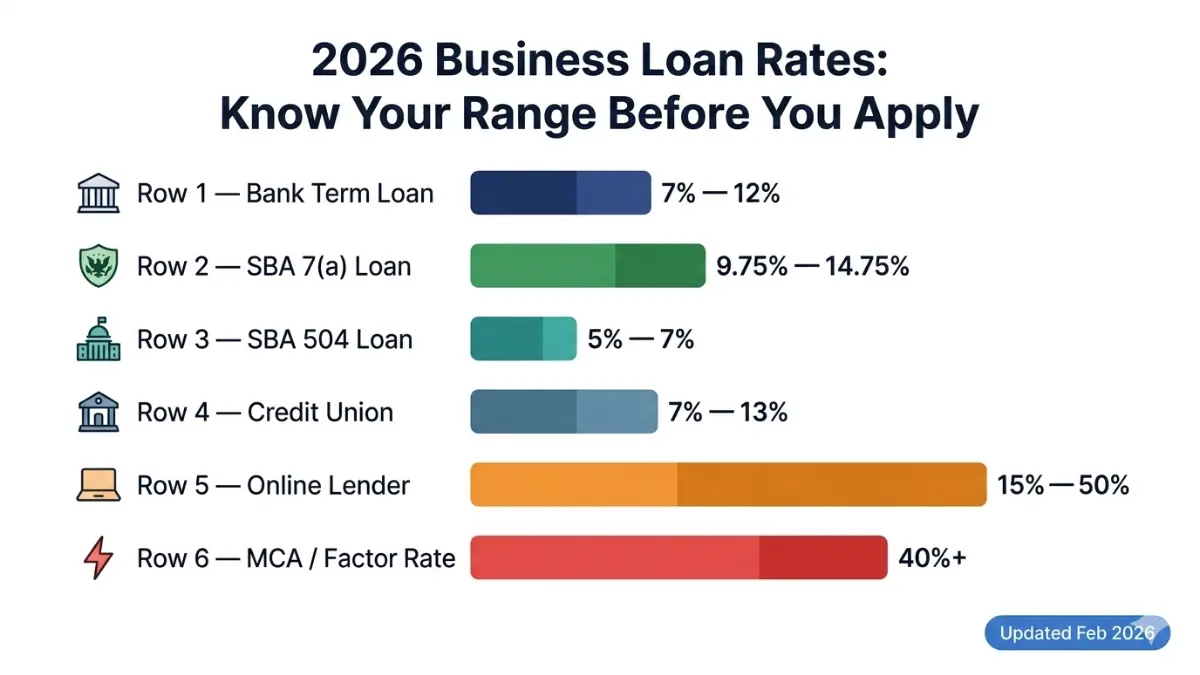

Current Business Loan Rates by Lender Type (2026)

| Lender Type | APR Range | Best For | Typical Term |

|---|---|---|---|

| Bank term loan | 7% – 12% | Established businesses, strong credit | 2–7 years |

| SBA 7(a) loan | 9.75% – 14.75% | Most small businesses | Up to 10–25 years |

| SBA 504 loan | 5% – 7% | Real estate, major equipment | 10, 20, 25 years |

| Credit union | 7% – 13% | Members with solid history | 1–7 years |

| Online lender | 15% – 50% | Newer businesses, lower credit | 3–36 months |

| MCA / factor rate | 40%+ effective APR | Fast cash, last resort | 3–18 months |

Traditional bank loans remain the cheapest option for businesses that can qualify, with rates typically falling between 7% and 12% APR, though the best-qualified borrowers might see rates below 7%.

Real Calculation: $75,000 Loan at Today’s Rates

Inputs: $75,000 loan | 10.5% APR | 60-month term | $750 origination fee (rolled in)

- Monthly payment: $1,621

- Total interest: $22,528

- Total cost (with fee): $98,278

- Payoff date: March 2031

Same loan, different terms:

| Term | Monthly Payment | Total Interest | Total Cost |

|---|---|---|---|

| 36 months | $2,437 | $12,728 | $88,478 |

| 60 months | $1,621 | $22,528 | $98,278 |

| 84 months | $1,240 | $32,119 | $107,869 |

Shorter terms save significantly on interest but require higher monthly cash outflow. Use the Auto Loan Calculator if you’re financing a vehicle separately and want to model that payment in parallel.

If you’re a student or early-stage founder comparing personal financing options, our Student Loan Calculator can help separate personal from business borrowing costs.

When to Consider Refinancing

If you took out a business loan in 2022–2024 at rates above 15%, refinancing in 2026 could lower your monthly payment and total cost substantially. Our Mortgage Refinance Calculator models break-even points for refinancing — the same logic applies to business loan refinancing decisions.

The SBA’s official 7(a) loan program page is the definitive source for current program terms, eligibility requirements, and maximum loan amounts directly from the government.

Frequently Asked Questions — Business Loan Calculator

1. What is a business loan calculator?

A business loan calculator is a digital tool that estimates your monthly payment, total interest, and full repayment cost based on your loan amount, interest rate, and term. Advanced versions like this one also factor in origination fees, interest-only periods, balloon payments, and extra payments.

2. How do I calculate my business loan monthly payment?

Enter your loan amount, annual interest rate (APR), and term in months into the calculator. The tool applies the standard amortization formula automatically. For a $50,000 loan at 9% APR over 48 months, your monthly payment would be approximately $1,244.

3. What is a good interest rate for a business loan in 2026?

For bank loans and SBA financing, anything under 10% is a strong rate in 2026. Online lenders typically charge 15%–50% APR. Rates depend on your credit score, time in business, and loan size.

4. What is an amortization schedule and why does it matter?

An amortization schedule is a month-by-month breakdown showing how much of each payment goes to principal versus interest, and your remaining balance after each payment. It lets you see the exact payoff date and plan for early repayment.

5. What is the difference between APR and interest rate on a business loan?

The interest rate is the annual cost of the loan principal only. The APR includes interest plus all fees — origination, guarantee, processing — giving you the true annual cost of borrowing. Always compare loans using APR, not interest rate alone.

6. How does an interest-only business loan work?

During the interest-only period, your monthly payment covers only the interest accruing on the principal. The principal balance doesn’t decrease. After the IO period ends, your payment increases to cover both principal and remaining interest over the remaining term.

7. What is a balloon payment on a business loan?

A balloon payment is a large lump-sum amount due at the end of a loan term. Monthly payments are calculated on a longer amortization schedule, but the loan matures before it’s fully paid off — leaving a balloon balance due in full at maturity.

8. How do origination fees affect my total loan cost?

A 2% origination fee on a $100,000 loan adds $2,000 to your cost. If rolled into the loan, you also pay interest on that $2,000 for the entire term, increasing your total cost further. This calculator shows both scenarios.

9. Can I pay off my business loan early?

Most business term loans allow early repayment, but some charge prepayment penalties — typically 1%–5% of the remaining balance. Always confirm prepayment terms with your lender before signing. The SBA’s official terms page clarifies prepayment rules for federally backed loans.

10. What is the SBA loan calculator used for?

The SBA loan calculator estimates monthly payments and total cost for SBA 7(a) and 504 loans. Enter the loan amount, your quoted APR (based on prime rate + lender spread), and the term to see your full payment breakdown. This is especially useful for comparing SBA loans against conventional bank offers.

11. How accurate is a business loan calculator?

A business loan calculator gives a close estimate but not a guaranteed quote. Actual payments may vary based on your final approved APR, exact fee structure, and any variable-rate adjustments over time. Use this calculator for planning and comparison — get a formal loan offer from your lender for final numbers.

📋 Disclaimer: This business loan calculator and all content on this page are for educational and informational purposes only. Results are estimates based on the inputs provided and do not constitute financial, legal, or lending advice. Interest rates, fees, and terms vary by lender and borrower qualification. Always consult a licensed financial advisor or qualified lender before making any borrowing decisions. financeauthorityhub.com is not a lender and does not guarantee loan approval or specific terms.

Explore More Financial Tools: Plan your complete financial picture with our full suite of calculators — including mortgage, auto, student loan, and debt consolidation tools. For deeper reading on debt strategy, our guide on debt types, risks, and how to break free in 2026 is a must-read before you borrow.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.