Structured Settlement vs Lump Sum The True Math Behind Each

Structured settlement or lump sum — the IRS AFR reveals a $64,000 gap most claimants miss. A CFA’s NPV framework shows which option actually wins.

In This Article

What the structured settlement vs. lump sum decision actually costs you

The financial mistake you cannot reverse is the one made before running the math.

A settlement offer — from a personal injury lawsuit, a workers’ compensation claim, or a lottery win — presents two options: a structured settlement paid in periodic installments over years or decades, or a lump sum delivered immediately in full. Most recipients choose on instinct. Those who choose on calculation consistently keep tens of thousands of dollars more.

Why “take the lump sum” is not always the right answer

The conventional wisdom says take the lump sum. It ignores the variable that determines everything: what the structured payment stream is worth in today’s dollars.

A $250,000 lump sum offer feels concrete. The same structured payment schedule — discounted at the 2026 IRS Applicable Federal Rate — may carry a present value of $314,000 or more, making the lump sum the financially inferior choice before a single investment decision is made.

The one calculation that determines which option wins

That $64,000 gap opens or closes based entirely on one number: the discount rate applied to the future payment stream.

Understanding what structured settlements actually pay — and how the annuity behind them is structured is the analytical foundation for every comparison in this article.

ℹ️ Disclaimer: The settlement, investing, and tax information in this article is for educational purposes only. Tax treatment under IRC § 104, investment return projections, and structured settlement valuations depend on settlement type, jurisdiction, and individual financial circumstances as of 2026. This article covers regulated activities in investing and federal income taxation. Before accepting, rejecting, or selling any structured settlement — or making any investment decision with a lump sum payment — consult a Chartered Financial Analyst (CFA), Certified Financial Planner (CFP), or Certified Public Accountant (CPA).

How structured settlements and lump sum payments actually work

Knowing who actually guarantees each option determines what you own — and what happens if the original defendant goes bankrupt.

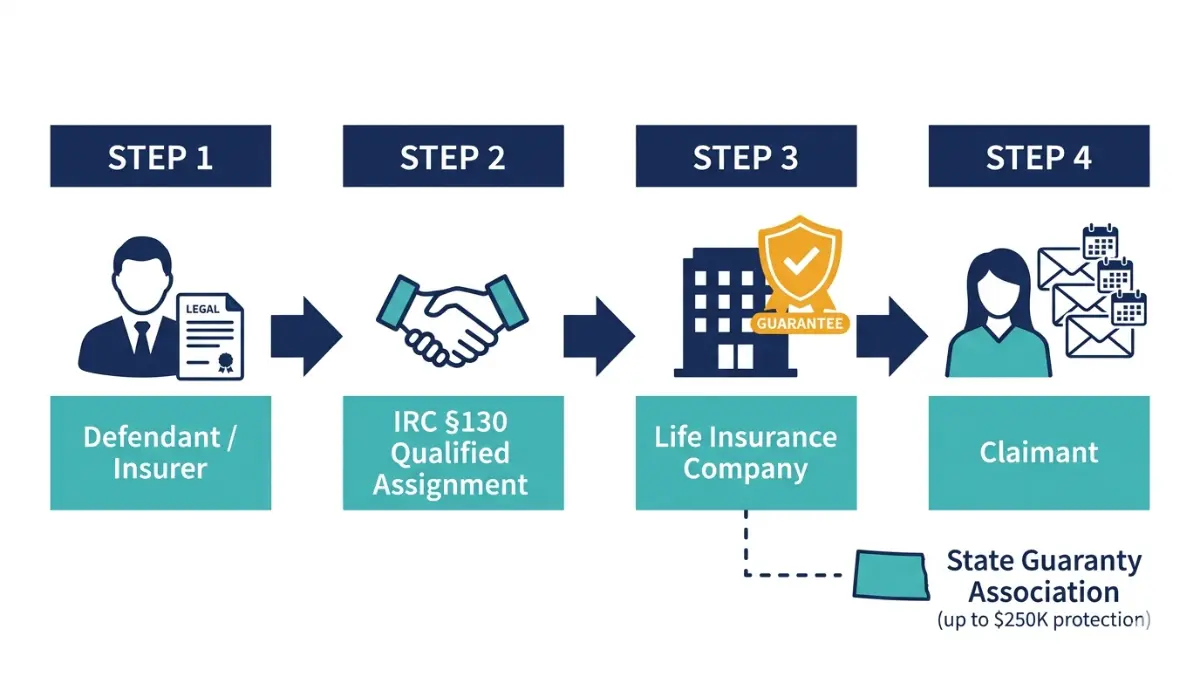

What a structured settlement annuity pays — and who guarantees it

A structured settlement annuity is not a direct payment agreement with the defendant. When a settlement is reached, the defendant’s insurer executes a qualified assignment under IRC § 130, transferring the full payment obligation to a life insurance company. That insurer — not the defendant — holds the annuity contract and guarantees every periodic payment.

If the original defendant’s company ceases to exist, the life insurer’s contractual obligation survives intact. State guaranty associations provide a secondary layer of protection, typically covering up to $250,000 per contract depending on state law.

Use a savings calculator to project what your periodic payments accumulate to over the full term before comparing that figure against any lump sum offer.

How lump sum payment amounts are determined at negotiation

A lump sum is the defendant’s discounted present value of the total payment stream — discounted at a rate they select, not you. That rate is almost always above the IRS AFR, which means the opening lump sum offer starts below fair present value before any negotiation has occurred.

The pros and cons of each: a side-by-side comparison

| Factor | Structured Settlement | Lump Sum |

|---|---|---|

| Tax treatment | Tax-free — physical injury, IRC § 104(a)(2) | Taxable as ordinary income — lottery, punitive damages |

| Payment guarantee | Yes — life insurer backed, contractual | None — investment performance dependent |

| Flexibility | Fixed schedule, limited access | Full discretionary control |

| Inflation protection | Limited unless COLA rider negotiated | Depends entirely on investment strategy |

| Best For | Long-term predictable income needs | Disciplined investors with high, consistent returns |

Source: IRC § 130 qualified assignment rules; IRS Publication 4345 (2026).

Before committing to any payment schedule, test whether the structured payments cover your actual monthly obligations using a budget calculator — the number that matters is not the gross settlement amount, but the net monthly cash flow.

How to calculate whether your structured settlement is worth more

Three numbers determine the answer. Most settlement offers will not volunteer any of them.

The three inputs you need before running the calculation

Net present value of any structured payment stream requires three inputs: (1) the complete payment schedule — every payment amount and date; (2) the 2026 IRS long-term Applicable Federal Rate as the discount rate benchmark; and (3) the net after-tax lump sum figure you have been offered in writing.

The IRS AFR — not the prime rate, not the 10-year Treasury, not the S&P 500 average — is the correct benchmark because it is the rate the IRS itself uses to evaluate tax-exempt deferred payment streams. Any other rate introduces bias that typically favors the offering party.

Measure how purchasing power erodes on fixed structured payments over a 20-year horizon using an inflation calculator before finalizing any present-value comparison.

Step-by-step: NPV calculation using the 2026 IRS AFR

- Obtain the current IRS long-term AFR — published monthly at the IRS Applicable Federal Rates page.

- Divide the annual AFR by 12 to derive the monthly discount rate.

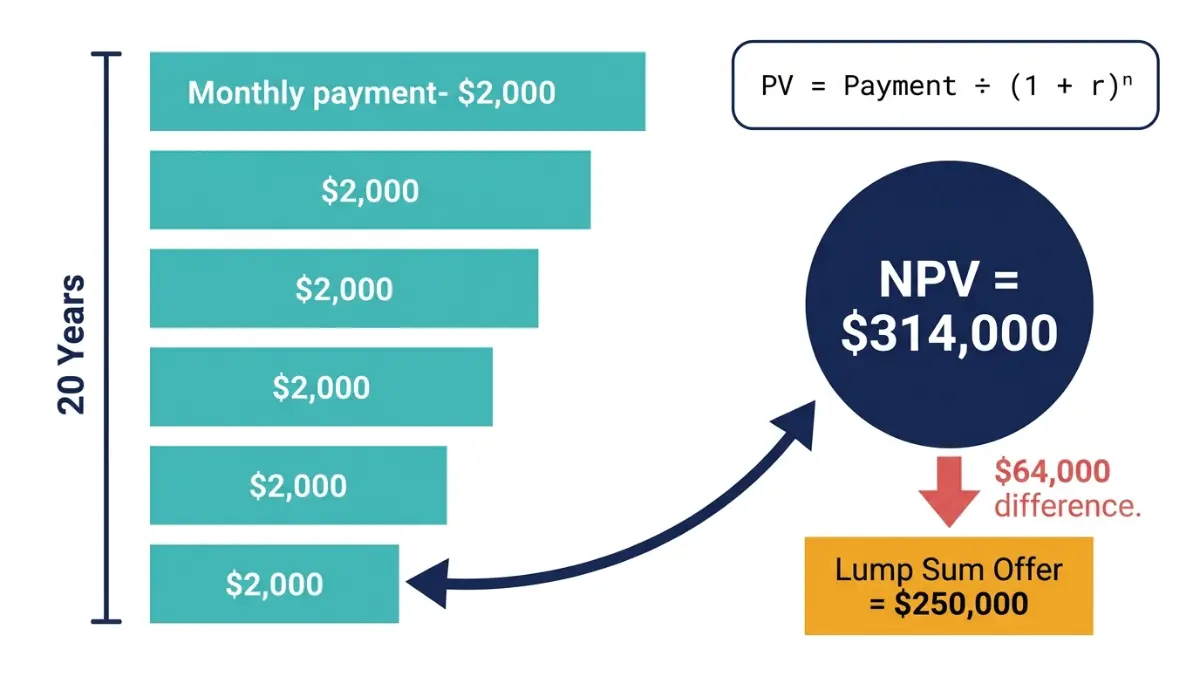

- Discount each individual payment: PV = Payment ÷ (1 + monthly rate)^n, where n equals the number of months until that specific payment date.

- Sum every discounted payment to produce the total net present value.

📊 Data Point: At an illustrative 2026 long-term AFR of 4.6% — verify the current monthly rate at irs.gov/applicable-federal-rates before applying to any live settlement — a $2,000 monthly payment for 20 years produces an NPV of approximately $314,000. A $250,000 lump sum offer sits $64,000 below that NPV. — Source: IRS Applicable Federal Rates, 2026 (verify monthly publication)

What the calculation result tells you — and its limits

| Discount Rate | NPV ($2,000/mo × 20 yrs) | vs. $250,000 Lump Sum |

|---|---|---|

| IRS Long-Term AFR (4.6%) | $314,000 | Structured wins by $64,000 |

| Market midpoint (6.0%) | $279,000 | Structured wins by $29,000 |

| Break-even return (~7.7%) | ~$250,000 | Equal |

| Typical factoring rate (12.0%) | $182,000 | Lump sum wins by $68,000 |

Note: Figures are illustrative. Verify the current 2026 IRS long-term AFR before applying to any real settlement analysis.

The NPV tells you which option is worth more at a given discount rate. It does not tell you whether you can reliably invest the lump sum at the break-even rate — that question requires an honest assessment of investment discipline, fees, and tax drag. Calculate a realistic return on lump sum deployment before assuming the lump sum investment scenario is achievable.

When a structured settlement pays more — and when it doesn’t

The NPV calculation from Section 3 tells you which option is worth more at a given rate. This section tells you what that rate means for your specific situation.

The break-even rule: what discount rate makes the lump sum worth taking

The lump sum wins only when you can invest it at a risk-adjusted, after-tax annual return that exceeds the structured settlement’s internal rate of return. Using the 2026 IRS AFR-based NPV framework above, the break-even return is approximately 7.7% annually — net of federal taxes, net of investment fees, sustained consistently over the full 20-year horizon.

📊 Data Point: After applying the 2026 federal long-term capital gains rate, average annual advisory fees of approximately 1.0%, and a conservative sequence-of-returns adjustment for a 20-year investment horizon, most retail investors achieve a real risk-adjusted return well below the 7.7% break-even. Review the most current investor return data at the SEC’s investor alerts and bulletins page. — Source: SEC Office of Investor Education, 2026

Three scenarios where structured settlement pays more

- Physical injury claimant receiving tax-free periodic payments under IRC § 104(a)(2) — the tax exemption raises the effective IRR equivalent substantially above what a fully taxable investment account must match to compete

- Claimant with limited investment experience or without consistent access to low-cost, tax-advantaged investment vehicles — the 7.7% break-even is genuinely difficult for most retail portfolios to sustain

- Any recipient with long-term guaranteed income obligations — ongoing medical costs, disability support, dependent care — where the certainty of payment matters more than the potential upside

💡 Expert Note (CFA): The scenario I have witnessed most consistently in my client practice over 28 years: a claimant accepts the lump sum based on long-run average market return assumptions, then encounters a 25–35% portfolio drawdown within the first two to three years. The structured settlement’s guaranteed payments represent a risk-free-rate equivalent return — a benchmark that is meaningfully harder to beat in a real taxable account than a 10-year backtest suggests.

Three scenarios where the lump sum wins

- Professionally managed, tax-advantaged portfolio with documented, consistent net returns above the 7.7% break-even threshold over a comparable time horizon

- Taxable punitive damages, emotional distress awards, or lottery winnings — where the lump sum at least allows immediate full deployment before future payments add to ordinary income in subsequent tax years

- A specific, verified, high-return capital allocation with a documented ROI above the break-even rate — a business acquisition, a cash-flowing real estate purchase, or a qualified opportunity zone investment with confirmed projections

Project lump sum growth under different annual return assumptions before concluding the investment scenario is realistic. Use a compound interest calculator to model compounded growth across the exact payment horizon of the structured settlement. A break-even calculator pinpoints the precise return threshold at which the lump sum surpasses the structured settlement’s present value — run that number before any decision.

Before signing any settlement agreement, consult a fiduciary CFA or CFP who can model both scenarios against your actual payment schedule, tax classification, and realistic portfolio assumptions.

How taxes change the real value of structured settlements and lump sums

The gross settlement figure on the offer letter is not the number that matters. The after-tax number is.

IRC Section 104: which settlements qualify for tax exemption

Physical injury and physical sickness structured settlements are fully excluded from gross income under IRC § 104(a)(2). Workers’ compensation settlements also qualify for exclusion under § 104(a)(1). This exemption applies to both the tax-free income stream itself and any interest component generated within the qualifying annuity contract.

The exemption does not extend to: punitive damages (always taxable), emotional distress damages not originating from physical injury, back pay, or interest awarded separately from the compensatory damages.

📊 Data Point: IRS Publication 4345 — the governing federal reference for structured settlement taxation — confirms that personal physical injury and physical sickness payments qualify for full income exclusion under IRC § 104. Verify the 2026 edition at IRS Publication 4345 — Structured Settlements and Periodic Payment Judgments. — Source: IRS Publication 4345 (2026)

How lottery and punitive damage lump sums are taxed in 2026

Lottery winnings — whether taken as a lump sum or as a structured annuity — are taxed as ordinary income in full. Federal mandatory withholding on lottery payments applies at 24% at the time of payment, with the balance owed at the recipient’s marginal rate at tax filing.

Punitive damages and emotional distress awards follow the same ordinary income treatment. A $500,000 lottery lump sum received in a high-income year could face a federal effective rate above 35% depending on total adjusted gross income — meaning the real after-tax value may be $325,000 or less before state taxes are applied.

Estimate your 2026 federal tax liability on a taxable settlement payment before finalizing any comparison with a tax-exempt structured settlement stream. Calculate the taxes owed on lump sum investment gains if you plan to immediately invest the lump sum in a taxable account.

The net value gap: after-tax comparison of both options

| Settlement Type | Gross Amount | IRC Tax Treatment | Effective 2026 Federal Rate | Estimated Net Retained |

|---|---|---|---|---|

| Physical injury — structured | $480,000 | Tax-free (§ 104) | 0% | $480,000 |

| Physical injury — lump sum | $300,000 | Tax-free (§ 104) | 0% | $300,000 |

| Lottery — structured annuity | $480,000 | Fully taxable | ~28% effective | ~$346,000 |

| Lottery — lump sum | $300,000 | Fully taxable | ~32% effective | ~$204,000 |

Estimates are illustrative. Verify 2026 federal rates at irs.gov. State tax rates apply additionally and vary significantly.

The tax classification of your settlement type should be confirmed by a CPA or tax attorney before you accept or reject any offer. For the complete analysis of how structured settlement payments are treated under federal tax law, the full IRC § 104 breakdown covers every payment category in detail.

⚠️ Warning: Misclassifying a punitive damages award as a physical injury payment is a reportable tax error. If your settlement combines physical injury damages and punitive damages in a single payment, each component must be allocated separately in the settlement agreement and reported accordingly to the IRS.

Structured settlement vs. lump sum: how the math differs by scenario

The break-even rate and tax framework above apply across all settlement types — but the starting conditions are not the same.

Personal injury and lawsuit settlements: why IRC § 104 changes everything

A physical injury structured settlement is the most financially competitive against a lump sum of any settlement type. The tax-free income stream under IRC § 104(a)(2) means the effective IRR equivalent for the structured option is substantially higher than the face-value rate suggests. A structured settlement with a nominal annual payout rate of 4.0% is effectively competing against a 5.5% to 6.0% taxable investment return for a claimant in the 32% federal bracket — a threshold few retail investment accounts clear consistently after fees.

Lottery winnings: why the lump sum is almost always smaller than it looks

Lottery winners face a structural disadvantage neither settlement type avoids: all payments are fully taxable. The advertised jackpot is the annuity total; the lump sum option is typically offered at 50–60% of the jackpot face value, and that reduced figure is then subject to federal withholding at 24%, followed by the marginal rate balance at filing. A $1 million jackpot announced as a lump sum choice of $600,000 may net $384,000 or less after federal withholding alone — before state taxes apply.

✅ Pro Tip: If you have won a lottery or received a large taxable settlement, use the Social Security calculator to estimate how settlement income interacts with your Social Security benefit calculation if you are within 10 years of claiming — large ordinary income years can affect benefit taxation thresholds.

Workers’ compensation: guaranteed income vs. investment uncertainty

Workers’ compensation structured settlements qualify for tax exclusion under IRC § 104(a)(1), making them structurally similar to physical injury settlements from a tax perspective. The key difference is duration: workers’ comp settlements frequently involve lifetime payment streams tied to disability, which creates a longevity risk consideration the NPV calculation cannot fully capture.

In most states, any sale of a workers’ compensation structured settlement requires court approval under the Structured Settlement Protection Act, and courts apply a best-interest standard before approving any factoring transaction. For the full breakdown of how workers’ compensation claim resolutions work, understanding workers’ compensation settlement terms before agreeing to any payment structure is the appropriate first step.

Making the structured settlement vs. lump sum decision with confidence

The math does not lie. The settlement offer does not do the math for you.

Your three-step action sequence before signing anything

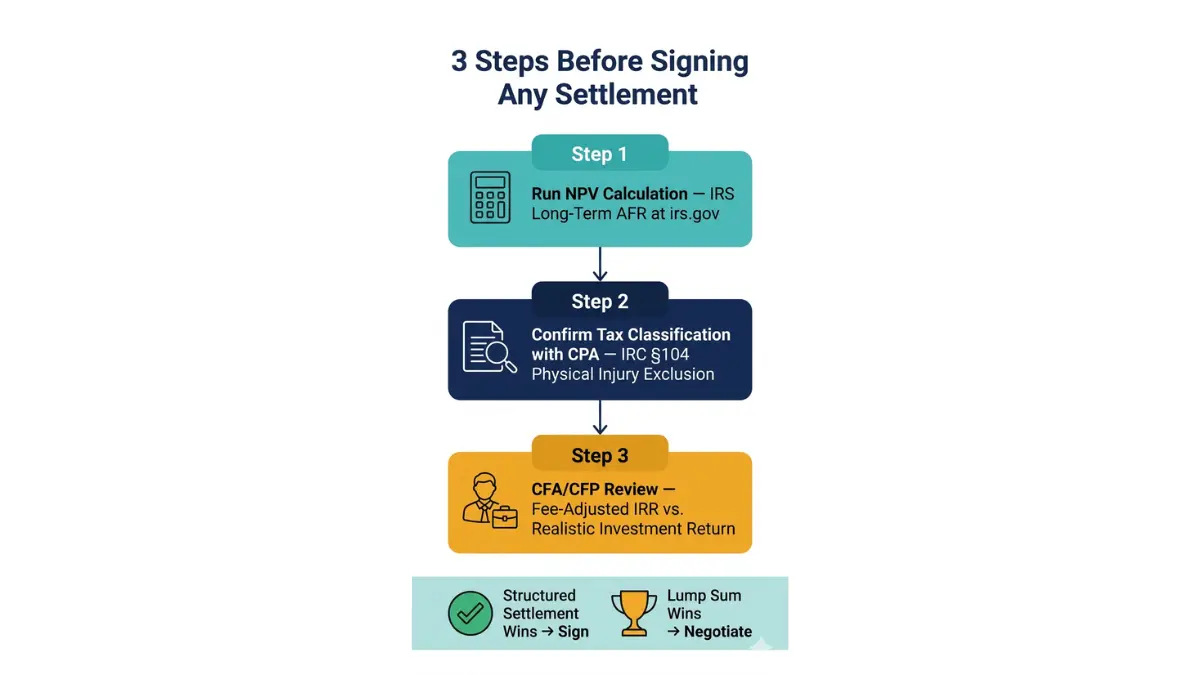

Before you accept or reject any settlement offer, execute these three steps in order:

- Run the NPV calculation using the current 2026 IRS long-term AFR from irs.gov/applicable-federal-rates. Sum every discounted payment and compare to the after-tax lump sum offer.

- Confirm the tax classification of your specific settlement with a CPA or tax attorney. Physical injury exclusion under IRC § 104 is not automatic — the settlement agreement must specify it.

- Have a fiduciary CFA or CFP review the IRR comparison using your exact payment schedule, your actual 2026 marginal tax rate, and a realistic, fee-adjusted investment return assumption — not a best-case market scenario.

Use a retirement calculator to model how either settlement option integrates with your long-term retirement income plan before treating the settlement as a standalone decision.

When to involve a CFA, CFP, or settlement attorney

A CFA is the appropriate professional when the core question is quantitative: which option produces the higher present value after taxes and fees. A CFP addresses the broader financial planning integration. A settlement attorney is required when any modification, assignment, or sale of structured settlement payments is involved — particularly in states where court approval is mandatory under the Structured Settlement Protection Act.

For consumer protection context on structured settlement transactions, the CFPB’s consumer tools section provides additional guidance on your rights before and after a settlement is finalized.

The one decision that is never justified by these numbers: signing a structured settlement buyout with a factoring company without first running the NPV comparison at the factoring company’s discount rate — typically 9% to 18% — against the full present value of your remaining payments at the IRS AFR.

Structured settlement vs. lump sum: answers to every question

1. Is a lump sum or structured settlement better?

Whether a structured settlement or lump sum pays more depends on one number: the net present value of the payment stream, discounted at the 2026 IRS long-term Applicable Federal Rate, compared against the after-tax lump sum offer. When the NPV exceeds the lump sum, structured wins. Consult a fiduciary CFA or CFP before making any final decision.

2. How much do you lose when you sell a structured settlement?

Factoring companies apply discount rates of 9% to 18% to your remaining structured settlement payments in 2026, substantially below the IRS AFR-based present value. On a $300,000 remaining payment stream, a 15% factoring discount can reduce your cash payout to approximately $180,000 or less. Consult a licensed financial advisor and settlement attorney before agreeing to any buyout.

3. Are structured settlements tax-free?

Physical injury and physical sickness structured settlements are fully excluded from gross income under IRC § 104(a)(2). Workers’ compensation settlements qualify under § 104(a)(1). Punitive damages, emotional distress not tied to physical injury, and lottery winnings do not qualify — those payments are taxed as ordinary income. Confirm your settlement’s tax classification with a CPA before signing.

4. What is the average structured settlement discount rate in 2026?

Factoring companies purchasing structured settlement payment streams typically apply discount rates between 9% and 18% in 2026, depending on payment duration, carrier quality, and remaining payment schedule. The IRS long-term Applicable Federal Rate — the fair-value benchmark — is substantially lower. The spread between the two rates directly measures the value transferred from you to the factoring company. Consult a licensed financial professional before any sale.

5. Can you sell a structured settlement for cash?

You can sell a structured settlement to a factoring company, but most states require court approval under the Structured Settlement Protection Act before any transfer is binding. Courts apply a best-interest standard to each proposed sale. You should obtain independent legal counsel and consult a licensed financial advisor who can calculate the present value gap before agreeing to any factoring transaction terms.

6. How long do structured settlement payments typically last?

Structured settlement payment durations are negotiated at settlement and vary widely. Common structures include fixed terms of 5, 10, 20, or 30 years; lifetime payments; or hybrid arrangements combining both. Lifetime structures end at death unless a joint-life or guaranteed-period rider is included in the annuity contract. Review your specific contract terms with a licensed settlement consultant before finalizing.

7. What happens to a structured settlement when you die?

What happens at death depends entirely on your annuity contract structure. Fixed-term structured settlements continue to your named beneficiary or estate. Lifetime-only structures cease immediately at death with no further payments to heirs. Joint-life structures continue to a surviving spouse. Review the beneficiary, survivorship, and guaranteed-period provisions with a licensed financial advisor before accepting any settlement structure.

8. Is lottery income taxed differently than a lawsuit settlement?

Yes — significantly. Physical injury structured settlements are fully tax-free under IRC § 104(a)(2). Lottery structured settlements are taxable as ordinary income at every payment, with federal mandatory withholding applied at 24% upfront and additional taxes owed at your marginal rate. In 2026, lottery recipients in higher income brackets face total federal effective rates above 30%. Consult a CPA to model your net after-tax lottery value.

9. What is a structured settlement annuity exactly?

A structured settlement annuity is a financial product issued by a life insurance company following a qualified assignment from the defendant’s insurer under IRC § 130. The life insurer guarantees each periodic payment per the court-approved schedule. Unlike annuities purchased directly, structured settlement annuities are funded entirely by the defendant’s insurer and carry specific tax treatment under federal law. Consult a licensed settlement consultant for your contract details.

10. Who benefits most from a structured settlement?

Claimants with long-term income needs, significant ongoing medical expenses, or limited investment experience benefit most from a structured settlement. The guaranteed, tax-exempt income stream eliminates investment risk for those unlikely to consistently beat the settlement’s effective IRR after taxes and fees. Retirees, individuals with long-term disabilities, and minors receiving injury awards are among the most common beneficiaries. A fiduciary financial advisor can assess your specific profile.

11. Can I invest a lump sum and beat a structured settlement return?

It depends on your after-tax, fee-adjusted investment return versus the structured settlement’s effective IRR. A tax-free structured settlement yielding an IRR equivalent of 5.5% to 7% is difficult to beat consistently in a taxable account after advisory fees and capital gains taxes. Most retail investors underestimate this benchmark. Consult a Chartered Financial Analyst to model both scenarios against your specific payment schedule and risk tolerance.

12. What is a structured settlement factoring company?

A structured settlement factoring company purchases your future payments in exchange for a discounted lump sum today. These companies profit by applying a discount rate — typically 9% to 18% in 2026 — to your payments’ present value. Courts in most states must approve the transaction under the Structured Settlement Protection Act. Consult both a settlement attorney and a licensed financial advisor before agreeing to any factoring terms.

13. Is a lawsuit settlement considered taxable income?

Whether a structured settlement or lump sum from a lawsuit is taxable depends on what the damages compensate. Physical injury and sickness payments are excluded under IRC § 104(a)(2). Punitive damages are always taxable. Emotional distress is taxable unless it directly results from a physical injury. Your settlement agreement should specify the nature of each payment component. Confirm the tax classification with a CPA or tax attorney before filing.

14. What is the present value of a structured settlement?

The present value of a structured settlement is the sum of all future payments discounted to today’s dollars at an appropriate rate. At an illustrative 2026 IRS long-term AFR of 4.6%, a $2,000 monthly payment for 20 years has a present value of approximately $314,000. A higher discount rate reduces this figure. A fiduciary financial advisor can calculate the exact present value for your specific payment schedule and timing.

15. How do I negotiate a structured settlement offer?

Negotiate by knowing the NPV of the payment schedule before the defendant’s first offer is presented. Request the complete payment schedule in writing. Calculate the structured settlement’s present value at the IRS AFR. Compare that figure against the lump sum alternative. Most defendants prefer structured settlements for cash-flow reasons, giving you leverage once you can demonstrate the NPV gap. Work with a licensed settlement consultant and fiduciary CFA for best results.

16. What are the main pros and cons of a structured settlement?

The primary advantages of a structured settlement include full tax exemption for physical injury awards under IRC § 104, guaranteed contractual income, elimination of investment risk, and protection from impulsive spending. Disadvantages include payment inflexibility, no inflation adjustment without a COLA rider, and complete loss of remaining payments at death in lifetime-only structures. A licensed financial advisor can weigh these against your specific financial situation and obligations.

17. Can a structured settlement be garnished by creditors?

In most states, structured settlement payments receive significant creditor protection because the claimant owns a contractual right to future payments, not a lump sum of money. However, protection varies by state law and settlement type. Federal tax liens and child support obligations may create exceptions regardless of state protections. Consult a settlement attorney familiar with your state’s Structured Settlement Protection statutes before assuming full creditor protection.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.