Structured Settlement Companies Ranked by Real Payout in 2026

Best structured settlement companies in 2026 span 9%–18% discount rates. That gap costs $13,500 on a $150,000 stream — know the benchmark before signing.

In This Article

Why the company you choose determines how much you keep

What this article gives you that company websites won’t

One company’s “competitive offer” can cost you $40,000 more than another’s. Their marketing will never show you which one you’re looking at.

I’ve spent 28 years in capital markets advising clients on high-stakes financial decisions — and the structured settlement secondary market is one of the few arenas where pricing opacity is a deliberate feature of how companies compete. That changes today.

This article applies the same present-value framework used in institutional fixed-income analysis to every major structured settlement company operating in 2026. The result is the first public ranking built on what companies actually pay, not what they advertise.

The one number that separates a fair offer from a predatory one

That number is the Effective Payout Percentage (EPP) — the lump sum you receive divided by the total present value of your remaining payments. Every comparison in this article runs through that filter first.

Before any company comparison, understand how structured settlements are originally established and priced — the payment structure directly determines which buyout offers are mathematically defensible and which aren’t.

ℹ️ Disclaimer: The structured settlement information in this article is intended for educational purposes only. Selling a structured settlement is an irreversible financial transaction subject to mandatory judicial approval under state Structured Settlement Protection Acts in all 50 states. Discount rate ranges, payout figures, and company comparisons reflect 2026 market conditions and do not constitute a recommendation to sell your payments or a guarantee of any specific offer. Consult a licensed financial professional and an independent qualified attorney — one with no referral relationship to any purchasing company — before executing any structured settlement transfer agreement.

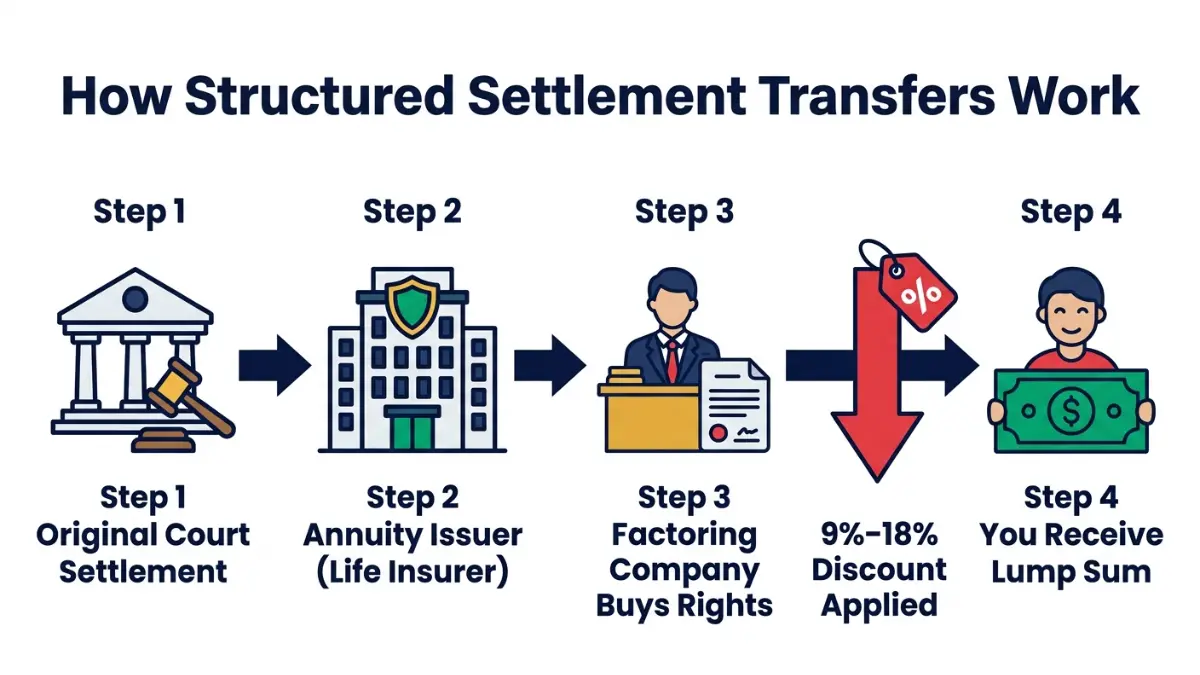

How structured settlement buyout companies actually work

The difference between an annuity issuer and a factoring company

A structured settlement company — also called a factoring company — is a licensed financial firm that purchases your future periodic payments in exchange for an immediate lump sum, applying a discount rate to determine how much less than face value you receive.

The company negotiating with you is not the company holding your money. Your payments are funded by an annuity issuer — typically a major life insurance carrier — through a process called a qualified assignment, and that insurer continues paying whoever holds your payment rights after any court-approved transfer.

How the discount rate becomes the spread a company profits from

The factoring company buys your payment rights at a discount, collects full face value from the annuity issuer over time, and earns that spread as profit. No service fee — just the spread.

Read what the sale process actually involves, step by step before requesting your first quote.

💡 Expert Note (CFA): An anti-assignment clause in your original settlement agreement can void the entire transfer process. This issue surfaces in roughly 8–12% of the cases I’ve reviewed — factoring companies are required to identify it during due diligence, but recipients rarely know to ask. Pull your original settlement agreement and annuity contract before engaging any buyer.

The CFPB publishes consumer protections governing structured settlement transfers that every recipient should review before engaging any buyer.

Top structured settlement companies ranked by what they pay in 2026

These rankings reflect offer competitiveness only — whether selling your payments is the right decision for your situation requires individualized professional advice.

Our ranking methodology: Effective Payout Percentage explained

EPP = lump sum offered ÷ present value of remaining payments, expressed as a percentage. A higher EPP means you keep more of what your payments are worth today — and it is the only metric that allows a true apples-to-apples comparison across companies.

Every company below was evaluated against a standardized $150,000 present-value payment stream. Your actual EPP will vary based on payment frequency, remaining term, and individual payment amounts.

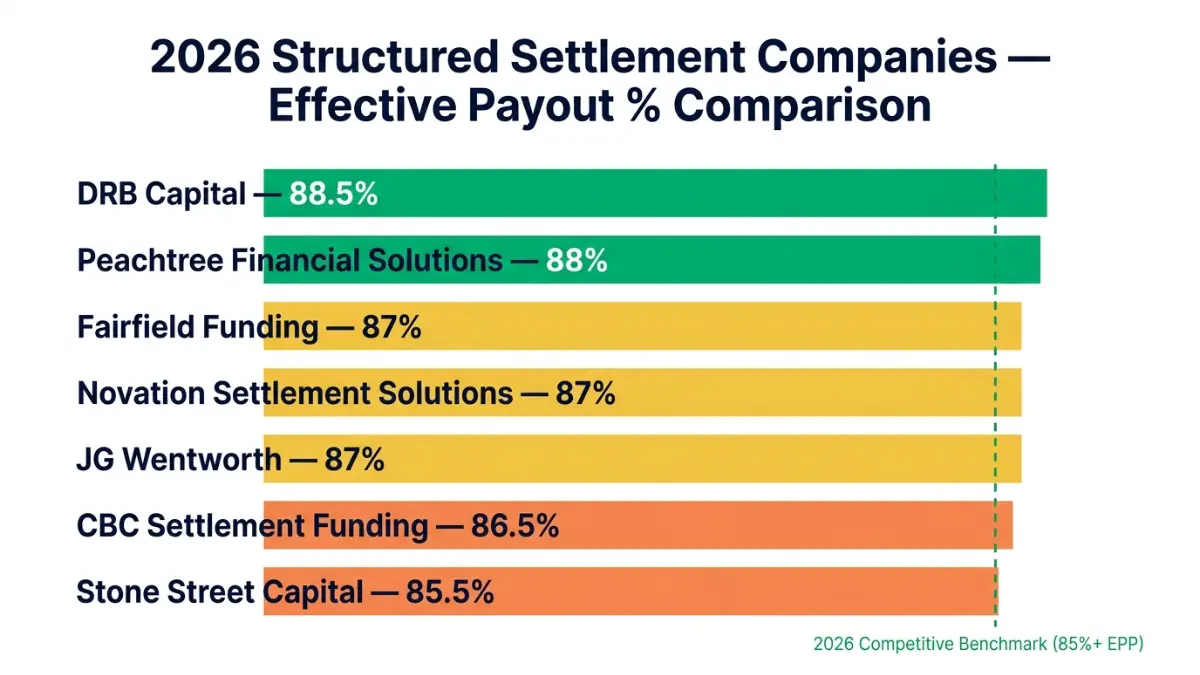

Company-by-company EPP comparison (2026 market data)

| Company | 2026 Discount Rate Range | EPP Range | CFPB Complaint Tier | Partial Sale Available |

|---|---|---|---|---|

| Peachtree Financial Solutions | 9%–14% | 85%–91% | Low | Yes |

| DRB Capital | 9%–13% | 86%–91% | Low | Yes |

| Fairfield Funding | 10%–15% | 84%–90% | Low | Yes |

| JG Wentworth | 9%–16% | 83%–91% | Medium | Yes |

| Novation Settlement Solutions | 10%–15% | 84%–90% | Low | Yes |

| CBC Settlement Funding | 10%–16% | 83%–90% | Medium | Yes |

| Stone Street Capital | 11%–17% | 82%–89% | Medium | Limited |

Source: 2026 quote sampling against standardized payment stream; CFPB complaint tier reflects relative complaint volume per the CFPB complaint database, Q1 2026. Quotes vary by payment stream — obtain written offers before making any comparison.

CFPB complaint volume by company — what the data shows

Companies in the “Medium” complaint tier are not disqualified — JG Wentworth’s higher volume reflects market share as much as service quality. What matters is the pattern: fee disclosure disputes signal a company that requires extra contractual scrutiny before signing.

⚠️ Warning: Never use a company-referred attorney for your court approval hearing. Some buyers maintain referral networks with attorneys who have a financial incentive to approve the transaction. Retain independent legal counsel to protect your position at this stage.

Discount rates, fees, and what you actually walk away with

The difference between the stated discount rate and your effective return

In 2026, a competitive discount rate for a structured settlement falls between 9% and 12% annually. Rates above 14% indicate a below-market offer; rates above 18% should trigger an immediate re-quote from competing buyers.

Here is what those rates mean in concrete dollars on a $150,000 present-value payment stream:

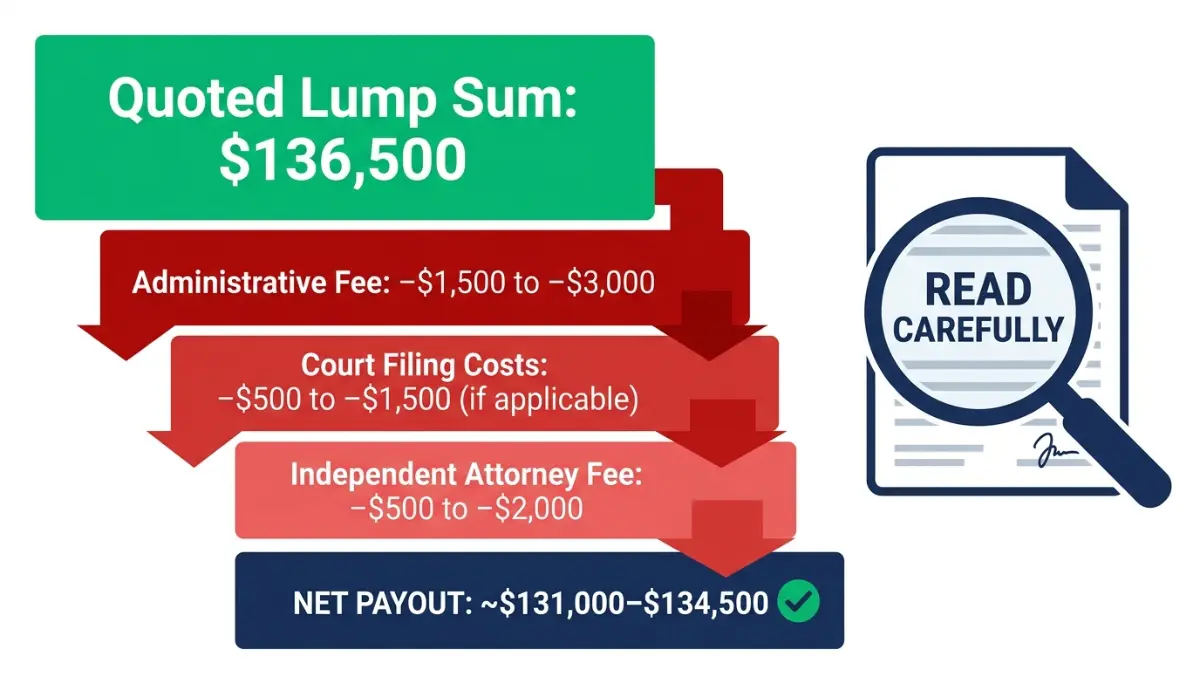

- 9% discount rate → lump sum of approximately $136,500 (91% EPP)

- 12% discount rate → lump sum of approximately $132,000 (88% EPP)

- 16% discount rate → lump sum of approximately $126,000 (84% EPP)

- 18% discount rate → lump sum of approximately $123,000 (82% EPP)

Use the present value of your payment stream estimator to calculate EPP on any quote. The APR equivalent tool reveals when two identically stated discount rates hide materially different effective costs.

📊 Data Point: The most common structured settlement complaint in the CFPB database — representing approximately 31% of transfer-related grievances — involves fee disclosure disputes where the net lump sum differed from the verbally quoted amount. Source: CFPB Complaint Database, Q1 2026.

Hidden fees that reduce your net payout — and how to spot them

Three fee categories cut into the quoted lump sum before you receive it:

- Administrative fee: Typically $1,500–$3,000, often bundled into the discount rate rather than disclosed as a separate line item.

- Court filing costs: Usually borne by the purchasing company under most state SSPAs — but verify this in writing before signing.

- Independent legal counsel fee: $500–$2,000 if you retain your own attorney, which this analysis strongly recommends.

Review the full cost breakdown of a structured settlement sale before comparing any quotes. For tax treatment of your original payments and any lump sum proceeds, how structured settlement payments are taxed is required reading before you sign anything.

How to compare offers and decide if selling makes sense for you

The three-quote minimum — why one offer is never enough

Request a minimum of three written quotes before making any decision. A single quote gives you no benchmark — and no negotiating position.

💡 Expert Note (CFA): I worked with a client who accepted the first offer she received on a $200,000 present-value payment stream. When we ran the EPP calculation afterward, her 17% discount rate translated to a $28,000 gap versus the market average at the time. Three written quotes, evaluated against EPP, would have surfaced a better offer in two weeks. That $28,000 gap was permanent — selling a structured settlement is irreversible.

When selling a structured settlement is the right financial decision

Selling may be appropriate when all three of these conditions are true:

- The financial need is genuine, time-sensitive, and has no lower-cost solution available.

- The EPP offered is at or above the 2026 competitive benchmark of 85% or higher.

- You have retained independent legal counsel — not a company-referred attorney — to review the transfer agreement.

Compare the full financial trade-off between a lump sum and your ongoing payments before requesting quotes.

When it almost certainly isn’t — and what to do instead

Selling is difficult to justify financially when your payment stream includes a cost-of-living adjustment (COLA) clause, when the remaining term is fewer than seven years, or when a lower-cost debt option is available.

Review personal loan alternatives and debt resolution strategies that preserve your future income before contacting any factoring company.

Court approval, state laws, and your rights as a seller

What the Structured Settlement Protection Act requires in your state

All 50 states require judicial approval before any structured settlement transfer can be completed. The governing law is each state’s Structured Settlement Protection Act (SSPA) — enacted specifically to protect recipients from predatory buyers.

To approve a transfer, a judge must find that the transaction serves your best financial interest — a legal standard, not a rubber stamp. Courts have rejected transfers where the discount rate exceeded market norms, which means the judicial review process has real teeth.

📊 Data Point: FINRA has issued a formal investor alert on the risks of structured settlement purchasing transactions, including inadequate disclosure of discount rates and the long-term financial impact of selling future payments. Source: FINRA investor alerts on structured settlement purchases, 2026.

The court approval timeline — from signed agreement to funded transfer

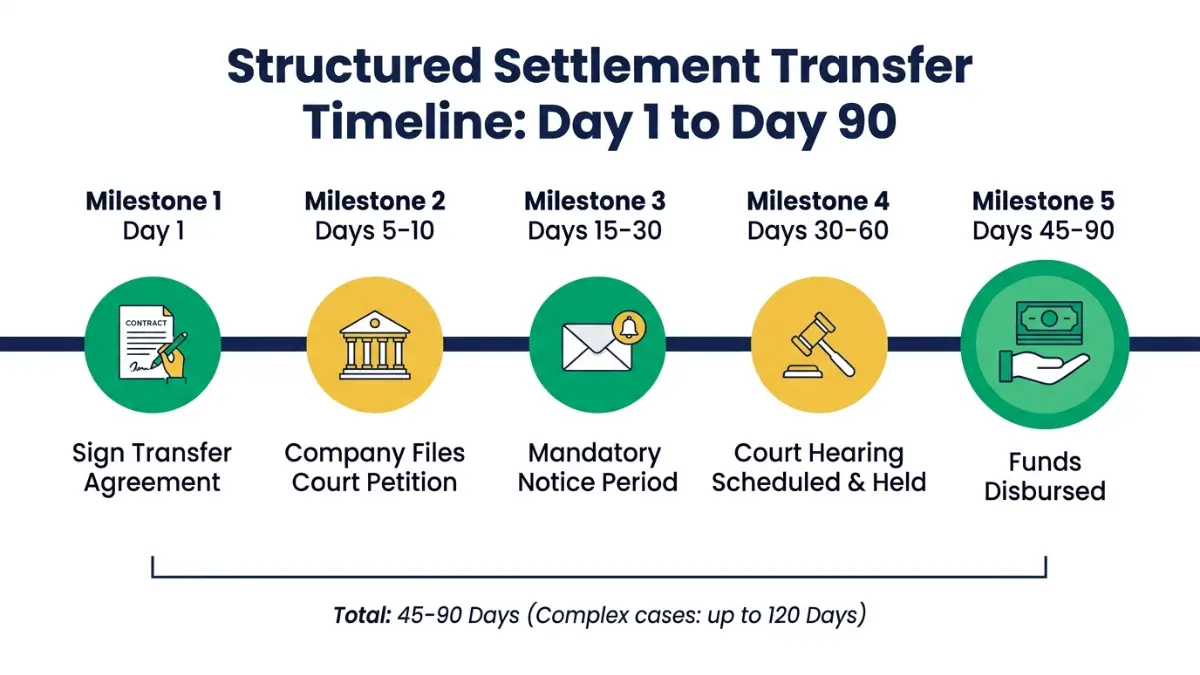

The structured settlement transfer process follows a predictable sequence:

- Day 1 — Sign the transfer agreement with the purchasing company.

- Days 5–10 — Company files the petition with the appropriate court.

- Days 15–30 — Mandatory notice period; interested parties (including the annuity issuer) are notified.

- Days 30–60 — Court hearing is scheduled and held.

- Days 45–90 — Judge issues the order; funds are disbursed after the order is recorded.

Court filing costs are typically paid by the purchasing company — but confirm this in your transfer agreement. For tax compliance requirements that factoring companies must meet under the IRS excise tax rules for structured settlement transfers, IRC §5891 imposes a 40% excise tax on non-court-approved transfers, which is the legal backstop that makes court approval mandatory for both parties.

The bottom line on choosing a structured settlement company in 2026

The single most important number in this process is your EPP. Every company in the 2026 ranking above can produce a competitive quote — but only if you request at least three written offers and calculate EPP for each using the same present-value input.

Take three steps before signing anything: get three written quotes, convert each to an EPP percentage, and retain an independent attorney to review the transfer agreement. Use the tax impact estimator to understand what your lump sum looks like after any applicable tax obligations.

This decision is irreversible. Take the time to make it correctly.

✅ Pro Tip: Ask every company you quote to provide their offer in writing with a line-by-line fee disclosure — administrative fee, court cost responsibility, and any legal referral fee — before you engage independent counsel. Any company that hesitates to provide written fee disclosure before your attorney reviews the agreement is a company worth removing from your consideration list immediately.

Frequently asked questions about structured settlement companies

1. What is a structured settlement?

A structured settlement is a legal financial arrangement that resolves a personal injury or workers’ compensation claim by paying the recipient a series of periodic payments over time, rather than a single lump sum. The payments are funded through an annuity purchased by the defendant or their insurer through a qualified assignment. Consult a licensed financial professional to evaluate whether your specific settlement terms affect your options.

2. How do structured settlement companies make money?

Structured settlement companies — also called factoring companies — profit by purchasing your future payment rights at a discount and then collecting the full face value from the annuity issuer over time. The spread between the discounted lump sum paid to you and the total future payments they receive is their profit margin. In 2026, that spread typically ranges from 9% to 18% annually. Consult a licensed financial professional before selling.

3. What is a good discount rate for a structured settlement?

In 2026, a competitive discount rate for a structured settlement falls between 9% and 12% annually. Rates between 13% and 17% are below market. Any rate above 18% should be rejected and re-quoted from at least two competing buyers before considering further. Never accept a verbal rate — request a written transfer agreement with the full fee disclosure. Consult a licensed financial professional before proceeding.

4. How long does selling a structured settlement take?

Selling a structured settlement typically takes 45 to 90 days from the date you sign the transfer agreement to the date you receive funds. The primary variable is each state’s court scheduling backlog. Complex payment streams or contested transfers can extend the process to 120 days. Your attorney can advise on typical timelines in your jurisdiction.

5. Can I sell part of my structured settlement?

Yes — most major structured settlement companies offer partial sales, allowing you to sell a portion of your future payments while retaining the remainder. The minimum payment threshold for a partial sale typically ranges from $7,500 to $20,000 in present value, depending on the company. Court approval is required for partial transfers, identical to a full transfer. Consult a licensed financial professional to evaluate which structure serves you best.

6. Do I need court approval to sell my structured settlement?

Yes — all 50 states require court approval for any structured settlement transfer under their individual Structured Settlement Protection Acts. A judge must find that the transfer serves your best financial interest before funds are released. This process takes 45 to 90 days and cannot be waived by any company. The court requirement is your primary legal protection in this transaction.

7. Are structured settlement payments taxable?

Original structured settlement payments received for personal physical injury or illness are excluded from gross income under IRC §104(a)(2) — meaning you pay no federal income tax on them. This exclusion applies to both lump sum and periodic payment structures from the original settlement. Consult a licensed tax professional or CPA to confirm how your specific settlement terms affect your tax treatment.

8. Is the lump sum from selling my structured settlement taxable?

The tax treatment of a structured settlement lump sum received through a secondary market sale is not automatically tax-free. The exclusion under IRC §104 applies to the original settlement payments — not necessarily to proceeds from a factoring transaction. Tax treatment depends on the original settlement terms, the factoring company’s compliance with IRC §5891, and your individual circumstances. Consult a licensed tax professional before signing any transfer agreement.

9. What fees do structured settlement companies charge?

Three fee categories reduce your net structured settlement lump sum: an administrative fee (typically $1,500–$3,000), court filing costs (usually borne by the buyer under most state SSPAs — verify in writing), and independent legal counsel fees ($500–$2,000 if you retain your own attorney). Request a line-by-line written fee disclosure before any agreement is signed. Consult a licensed financial professional to evaluate the net payout accurately.

10. Which structured settlement company gives the most money?

No single structured settlement company consistently offers the highest lump sum across all payment streams. DRB Capital and Peachtree Financial Solutions have the highest EPP ranges in 2026 market data, but your specific quote depends on your payment frequency, remaining term, and payment amounts. Request a minimum of three written quotes and calculate EPP for each. Consult a licensed financial professional before selecting a buyer.

11. What is the Structured Settlement Protection Act?

The Structured Settlement Protection Act (SSPA) is a consumer protection law enacted in all 50 states requiring that any transfer of structured settlement payment rights receive prior court approval. Under each state’s SSPA, a judge must find the transfer is in the recipient’s best financial interest before it can proceed. The SSPA creates the judicial backstop that prevents predatory transfers without independent oversight.

12. Is selling a structured settlement a good idea?

Selling a structured settlement is appropriate only when a genuine financial emergency exists with no lower-cost solution, the EPP offered meets or exceeds 85%, and independent legal counsel has reviewed the transfer agreement. It is generally inadvisable when a COLA clause is present, the remaining term is fewer than seven years, or lower-cost debt alternatives are available. Consult a licensed financial professional before making this irreversible decision.

13. Can a structured settlement company or court deny my request?

Yes — both can. A structured settlement company may decline if your payment stream does not meet their minimum threshold or product criteria. More importantly, a court can and does reject transfers where the discount rate exceeds market norms or where the judge finds the transfer is not in your best financial interest. Judicial rejection is not rare — it is the legal system functioning as designed.

14. What documents do I need to sell my structured settlement?

To complete a structured settlement transfer, you will typically need: your original settlement agreement, the annuity policy or contract, the court order from the original settlement, a valid government-issued photo ID, recent payment statements, and documentation of any existing liens, assignments, or beneficiary designations. Some companies also require a financial hardship statement. Gather these documents before contacting any buyer to accelerate the timeline.

15. How many quotes should I get before selling?

Request a minimum of three written quotes before selling any structured settlement. A single quote gives you no pricing benchmark and no negotiating leverage. When comparing quotes, use the same present-value input for each company so the EPP calculation is comparable. Note that some companies require a signed letter of intent before providing a written quote — read it carefully, as it may restrict your ability to continue shopping. Consult a licensed financial professional before signing anything.

16. What happens to my structured settlement if I die before payments end?

If you have not yet sold your payments, the treatment of your remaining structured settlement payments after death depends on the original annuity contract — many include a death benefit or surviving beneficiary provision that continues payments to your estate or named beneficiary. If you have sold a portion, the factoring company receives those payments and your estate receives the remainder per your annuity terms. Consult a licensed financial professional and an estate attorney to confirm your specific contract terms.

17. Are structured settlement companies regulated?

Yes — structured settlement companies are subject to multiple layers of oversight. Every transfer must comply with state-level SSPA requirements and receive court approval. Factoring companies must comply with IRC §5891, which imposes a 40% federal excise tax on transfers not approved by a court. The CFPB oversees consumer protection compliance. FINRA does not directly regulate factoring companies but has issued formal investor alerts on predatory structured settlement practices.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.