What to Do First When You Receive a Large Settlement

Large settlement money is protected only to $250,000 per bank, and punitive damages are taxable. Here’s the first-30-days plan most people skip.

In This Article

The money has arrived, and the feeling is rarely pure relief.

A large settlement usually follows something hard — an injury, a lost job, the death of a family member. Now the biggest sum you have ever held sits in one account, and the pressure to do something with it is immediate.

Here is the part most people get backwards. The fastest ways to lose part of a lawsuit settlement are an unplanned tax bill and idle cash that outgrows its insurance protection — not a bad stock pick.

This is a 30-day financial plan for the first month, in the order a portfolio professional would actually run it. You protect the cash, wall off what you may owe in tax, then decide where the lump sum goes.

The single goal for month one is to make no permanent mistake while you assemble the right team and the right facts.

💡 Expert Note (CFA): The recipients who do best a year out are almost never the ones who moved fastest. They are the ones who did nothing they could not undo in the first 30 days.

ℹ️ Disclaimer: This article explains the tax treatment and investment handling of legal settlement proceeds for educational purposes only. How much of a settlement is taxable depends on your specific damages and how they are allocated under federal law as of 2026, and account yields and insurance limits change through the year. Before reserving for taxes, parking the funds, or investing any portion, consult a licensed tax professional — a CPA or tax attorney — and a fee-only fiduciary financial advisor about your situation.

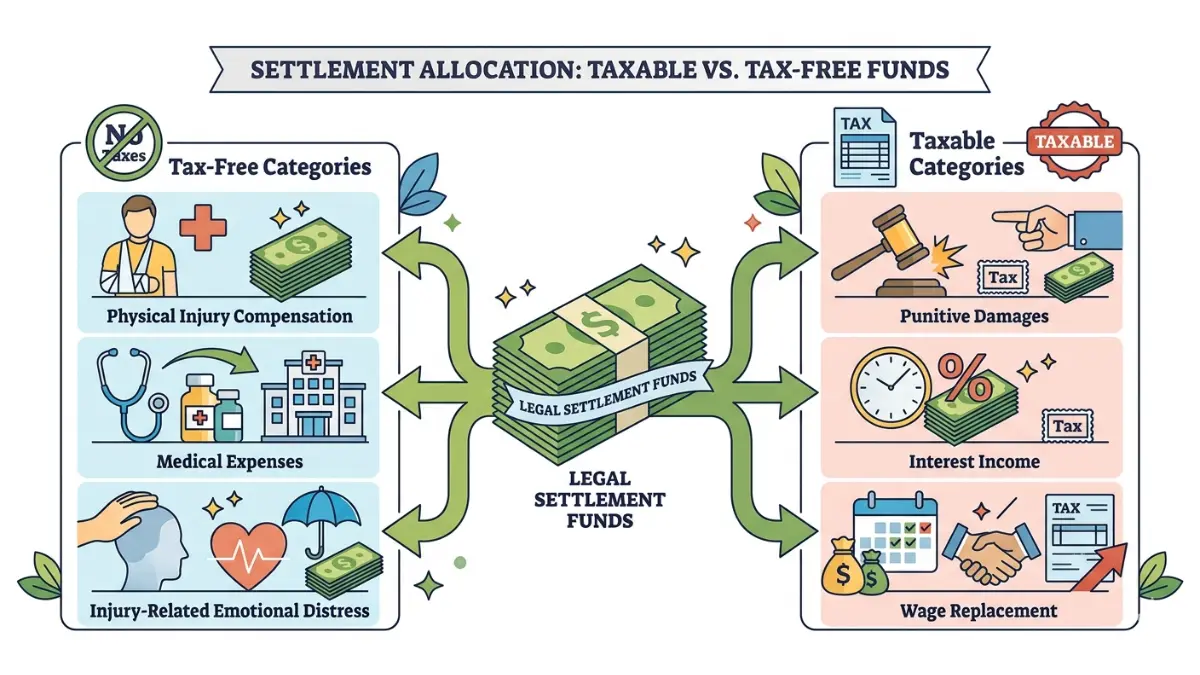

How much of your settlement is actually taxable?

Most settlement money for a physical injury or sickness is not taxable income, but punitive damages and interest are taxed as ordinary income.

That split is the most misunderstood fact about settlement money, and it decides how much you set aside.

What part of a settlement is tax-free?

Under IRC Section 104, compensation for a personal physical injury or physical sickness is excluded from gross income.

That gross income exclusion covers medical costs, pain and suffering, and even emotional distress — as long as the distress stems from the physical injury.

What part is always taxable?

Punitive damages are taxed as ordinary income even when the case involved a physical injury.

Interest on the award and lost wages from non-physical claims, such as discrimination or wrongful termination, are taxable too.

| Settlement component | Federal tax treatment (2026) | Key consideration |

|---|---|---|

| Physical-injury compensatory damages | Tax-free | The core exclusion under IRC §104 |

| Medical expenses for a physical injury | Tax-free | Tax-free even if unused for care |

| Emotional distress from a physical injury | Tax-free | Must trace to the bodily injury |

| Lost wages from a non-physical claim | Taxable | Treated as ordinary income |

| Interest on the award | Taxable | Reported as interest income |

| Punitive damages | Taxable | Taxable even in injury cases |

Source: IRS, Tax Implications of Settlements and Judgments, 2026.

The allocation written into your settlement agreement drives the result, and the IRS does not have to accept the parties’ labels — the agency’s own guidance on how settlement proceeds are taxed explains how it characterizes each payment.

Before assuming the whole check is yours, estimate what you might owe on the taxable slice with an income tax calculator and keep a tool for projecting tax on investment gains for the money once it is invested.

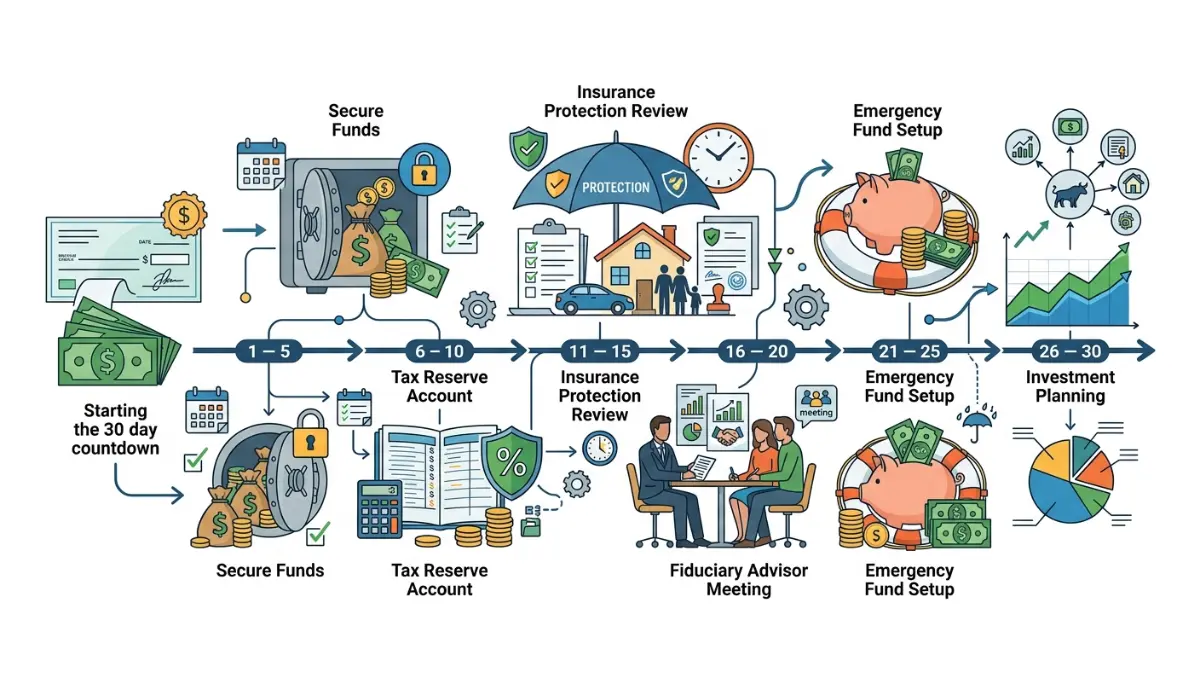

What to do in your first 30 days after a settlement

When you receive a large settlement, take these steps in your first 30 days:

- Days 1–3: Park the full amount in one safe account and tell no one outside your household until you have a plan.

- Week 1: Estimate the taxable portion and move that cash into a separate reserve so it is never spent.

- Week 1: Confirm the funds sit within federal deposit-insurance limits, or spread them so they do.

- Weeks 2–4: Book a fee-only fiduciary and a tax professional before committing a dollar.

- Weeks 2–4: Top up your emergency fund, then plan the long-term deployment.

Days 1–3: pause and protect

The first move is not investing — it is preventing loss.

Leave the net amount where it is, decline family requests for now, and ignore any “act today” pitch.

Week 1: wall off the tax reserve

Open a separate account and move your estimated tax there, out of spending reach.

You can watch that reserve sit and grow with a savings calculator while the rest of your plan comes together.

Weeks 2–4: plan before you deploy

This is when asset allocation decisions get made — with professionals, not in a panic.

💡 Expert Note (CFA): Before any money is invested, the balance goes into a government-backed vehicle and the tax reserve gets separated. Returns can wait a month; a tax penalty or an uninsured loss cannot be undone.

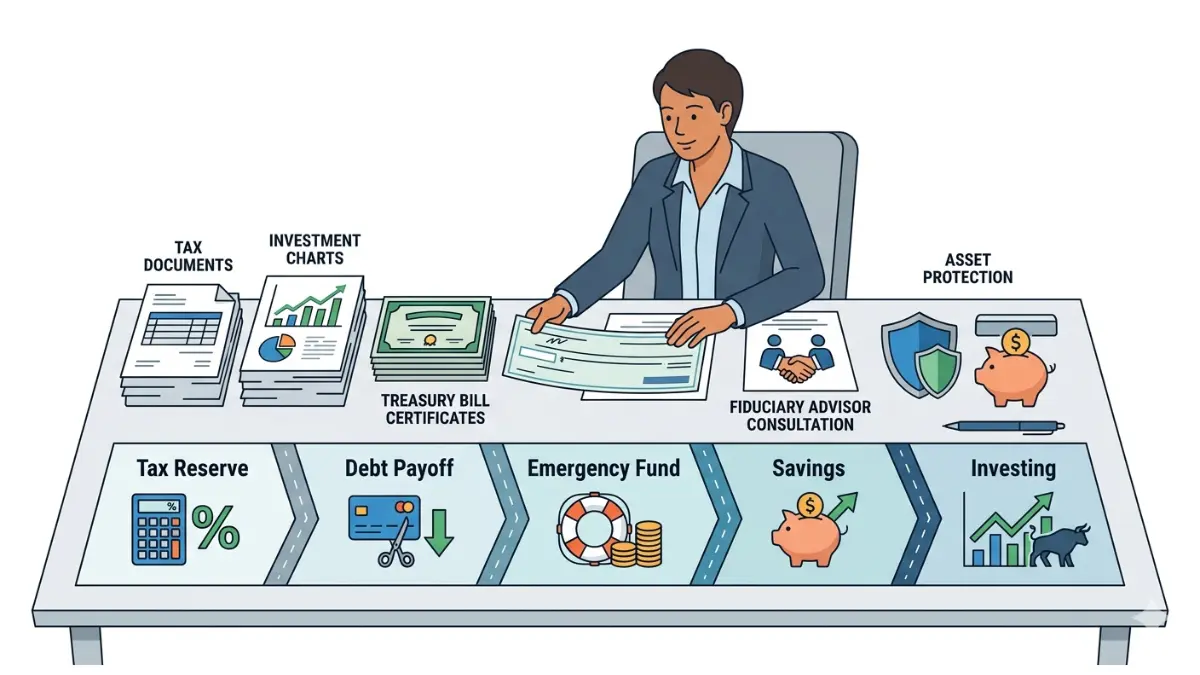

Should you pay off debt, save, or invest the money?

Set aside tax only on the taxable portion — punitive damages, interest, and lost wages from non-physical claims — at your marginal rate, then follow a fixed order.

The sequence matters more than the math: reserve tax, clear high-interest debt, fund the cushion, then invest.

How much to set aside for taxes first

Reserve against the taxable components at your top federal rate, and check whether quarterly estimated payments apply.

📊 Data Point: You may owe estimated tax if you expect to owe $1,000 or more after withholding and credits — Source: IRS Publication 4345, 2026.

The threshold and reporting rules sit in the IRS publication covering settlement taxability.

When paying off debt beats investing

Clearing a balance that charges more than a safe account can earn is a guaranteed return.

A credit card payoff calculator shows the interest you save, and a debt consolidation calculator compares that with rolling balances into one lower-rate loan.

What to do with the remainder

What is left after tax, debt, and the cushion is your long-term money.

Model its growth with a compound interest calculator, then compare options with an investment calculator; the SEC’s plain-language guide to spreading money across asset categories is a sound starting point.

Where to park a large settlement safely right now

The safest short-term homes for a large settlement are:

- A high-yield savings account (APY) at an FDIC-insured bank — liquid and protected to the coverage limit.

- A money market fund, which holds short-term government and high-grade debt.

- Treasury bills, backed by the U.S. government, useful for amounts above deposit-insurance limits.

- A certificate of deposit (CD) when you can lock the cash for a set term.

How insurance limits affect a large sum

Coverage is capped, so a settlement above that line is only partly protected in one bank.

📊 Data Point: Deposit insurance covers $250,000 per depositor, per insured bank, for each ownership category — Source: CFPB, 2026.

Spreading the money across institutions, or laddering short terms with a CD calculator, restores full protection — and the CFPB’s explanation of how bank deposits are protected details the limit.

Cash options and their 2026 yields

Top high-yield accounts have paid roughly 4% to 5% APY in 2026, far above the national average.

📊 Data Point: The Federal Reserve held its federal funds target range at 3.50%–3.75% in 2026, which keeps cash yields elevated — Source: Federal Reserve, 2026.

Rates move with the Fed, so verify the current APY at your bank first; see how idle cash loses value over time with an inflation calculator, and the Federal Reserve’s record of its rate decisions tracks the latest move.

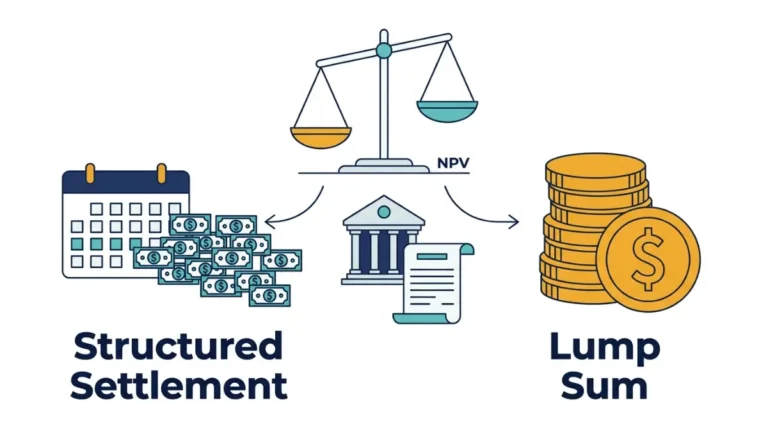

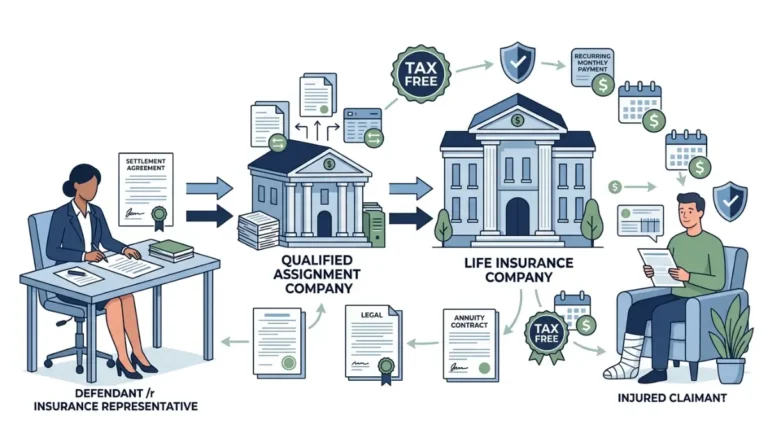

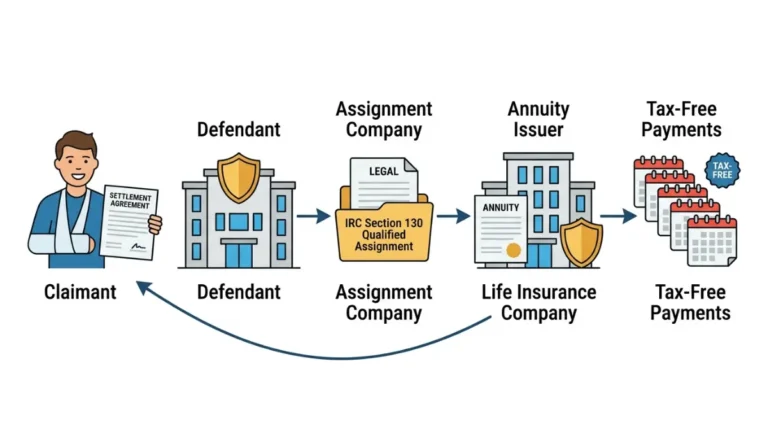

Lump sum, structured settlement, or annuity — what to watch for

A lump sum gives you control; a structured settlement trades flexibility for guaranteed payments over time.

Neither is automatically better, and the right answer depends on your discipline, taxes, and goals.

Lump sum vs. structured settlement

A structured settlement pays on a fixed schedule and can keep injury-related income tax-free, but you cannot easily change it later.

A lump sum lets you invest and access the money, which suits people who will work with a fiduciary and a written plan.

If retirement is the goal, a retirement calculator and a Roth IRA calculator show how settlement dollars can fund tax-advantaged accounts.

📊 Data Point: For 2026 you can contribute up to $24,500 to a 401(k) and $7,500 to an IRA — $8,600 if you are 50 or older — Source: IRS, 2026.

The products to be cautious about

Be wary of “settlement advance” or factoring offers that buy your future payments at a steep discount. Note that brokerage holdings are protected by SIPC, not deposit insurance.

⚠️ Warning: Commission-paid sellers of annuities and whole-life policies often target new settlement recipients. Have a fee-only financial advisor review any product before you sign, and confirm a broker’s record before handing over money.

Your 30-day settlement plan, in one place

The plan for month one fits in a single line: protect the cash, reserve the tax, then deploy with help.

A large settlement does not reward fast decisions — it rewards careful ones.

Set aside what you may owe under IRC Section 104, hold the rest in insured or government-backed accounts, and bring in a licensed tax professional and a fiduciary before you commit the money.

Then handle the human side. Decide in advance how you will answer relatives, because the requests usually arrive faster than the wire did.

✅ Pro Tip: Within 48 hours, open one separate account labeled “taxes,” move your estimated reserve into it, and do not link a debit card to that account.

The people who keep their settlement are the ones who treat month one as a holding pattern, not a starting gun.

Frequently asked questions about handling a large settlement

1. Do I have to pay taxes on a lawsuit settlement?

It depends on what the money replaces. Compensation for a physical injury or sickness is usually tax-free, while punitive damages, interest, and lost wages from non-physical claims are taxable. The allocation written into your settlement agreement shapes how much of your lawsuit settlement the IRS treats as taxable income.

2. What should I do first after receiving a large settlement?

First, park the full amount in one safe, insured account and avoid any immediate spending or investing. Within the first week, estimate the taxable portion and move it into a separate reserve. After you receive a large settlement, every major decision can wait until a fiduciary and tax professional review your situation.

3. Is a personal injury settlement considered income?

Mostly no. Money awarded for a personal physical injury or sickness is excluded from gross income, so a personal injury settlement is generally not taxable. However, punitive damages and interest are taxable, and any portion labeled as lost wages from a non-physical claim counts as ordinary income.

4. Where is the safest place to put a large settlement?

The safest short-term homes are an FDIC-insured high-yield savings account, a money market fund, short-term Treasury bills, or a certificate of deposit. For a large settlement above deposit-insurance limits, Treasury bills or spreading cash across several banks keeps the full balance protected while you plan.

5. How much money is protected in a single bank account?

Federal deposit insurance protects up to $250,000 per depositor, per insured bank, for each ownership category. A large settlement that exceeds that amount in one bank is only partly protected, so splitting the money across institutions or using Treasury securities restores full coverage of your balance.

6. Are punitive damages taxable?

Yes. Punitive damages are taxed as ordinary income even when they are part of a settlement for a physical injury, because they punish the defendant rather than compensate you for harm. Report them as other income, and set aside tax on this portion of your settlement at your marginal rate.

7. Should I pay off debt with my settlement?

Often yes, for high-interest debt. Using settlement money to clear a balance charging more than a safe account can earn is a guaranteed return. Pay off costly credit card or payday debt before investing, but reserve your tax obligation and emergency fund from the settlement first.

8. Do I need to make estimated tax payments on a settlement?

Possibly. If you expect to owe $1,000 or more after withholding and credits on the taxable part of your settlement, you may need quarterly estimated tax payments. Punitive damages and interest commonly trigger this, so set the tax reserve aside as soon as the money arrives.

9. How long should I wait before investing a settlement?

There is no fixed rule, but most people benefit from waiting until the tax reserve is set and a plan exists — often 30 days or more. Investing a settlement too quickly, before your asset allocation is decided, is a frequent and avoidable mistake that is hard to reverse.

10. What’s the difference between a structured settlement and a lump sum?

A lump sum pays everything at once, giving full control and flexibility. A structured settlement pays fixed amounts over years and can keep injury-related income tax-free. The right choice between a structured settlement and a lump sum depends on your spending discipline, tax situation, and long-term goals.

11. Will I receive a 1099 for my settlement?

Sometimes. You generally will not get a 1099 for a fully tax-free physical-injury settlement, but you may receive one for taxable portions such as punitive damages or interest. Keep every settlement document, since the allocation determines what is reported and what tax you owe.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.