How a Qualified Assignment Protects Your Settlement Payments

Qualified assignments make injury settlements tax-free under IRC 130—but selling those payments can trigger a 40% tax most sellers never see coming.

In This Article

What a qualified assignment really means for your settlement

A qualified assignment is the legal step that makes your structured settlement payments tax-free and moves the obligation off the defendant’s books. It is defined by IRC Section 130.

You probably met the term in one of two moments. Either you saw it in settlement paperwork after an injury claim, or a company called offering to buy your future payments for cash now.

Both moments matter, and most articles only cover one. This guide covers the full lifecycle — how the assignment is set up, and what happens if you later sell.

Here is the core idea in one line. The assignment is what protects you on the front end, and a federal excise tax plus a judge protect you on the back end.

ℹ️ Disclaimer: This article explains the federal tax treatment of structured settlements under Internal Revenue Code Sections 130, 104, and 5891 for educational purposes. The tax-free status of any settlement depends on the specific damages involved, and the rules for selling future payments — including state court approval and the 40% federal excise tax on non-approved transfers — vary by state and transaction. Consult a licensed tax professional (CPA or tax attorney) and a qualified financial advisor before accepting a structured settlement or selling future payments.

The players: who pays, who promises, who is on the hook

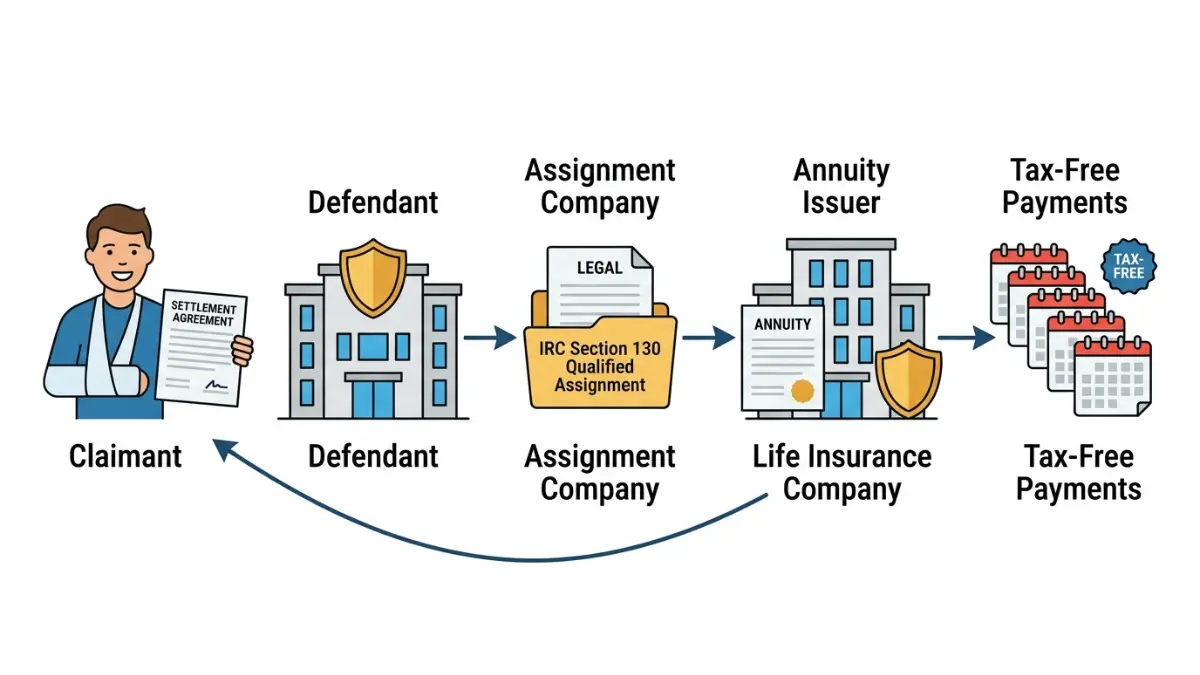

Four parties make a structured settlement work, and knowing them tells you who is actually responsible for your money.

First is you, the claimant. Second is the defendant or its insurer, which agreed to pay you over time.

Third is the assignment company, which takes over the payment obligation from the defendant. Fourth is the life insurer that issues the annuity funding those payments.

The defendant does not want a decades-long obligation on its books. So it transfers that periodic payment obligation to the assignment company, which extinguishes the defendant’s liability.

Most assignment companies are affiliates of large life insurers — names like Berkshire Hathaway subsidiaries, MetLife, Pacific Life, and Prudential. The annuity behind your payments is only as strong as the insurer that issues it.

💡 Expert Note (CFA): In my client work, the question that gets skipped is the simplest one — which insurer actually stands behind the annuity. I check the issuer’s financial-strength rating before anyone signs, because the payment promise can run 20 or 30 years and you are trusting that balance sheet the whole time. Because fixed payments lose purchasing power over decades, I also run the schedule through an inflation calculator that shows how rising prices erode a fixed dollar amount so clients see the real-terms value, not just the headline number.

How IRC 130 makes the payments tax-free

Under IRC Section 130, the assignment company can exclude the money it receives to fund your payments from its own income — and your payments stay tax-free under IRC Section 104(a)(2).

That second part is the one you care about. Damages for personal physical injury or physical sickness are excluded from gross income, and a qualified assignment preserves that treatment as the payments flow to you.

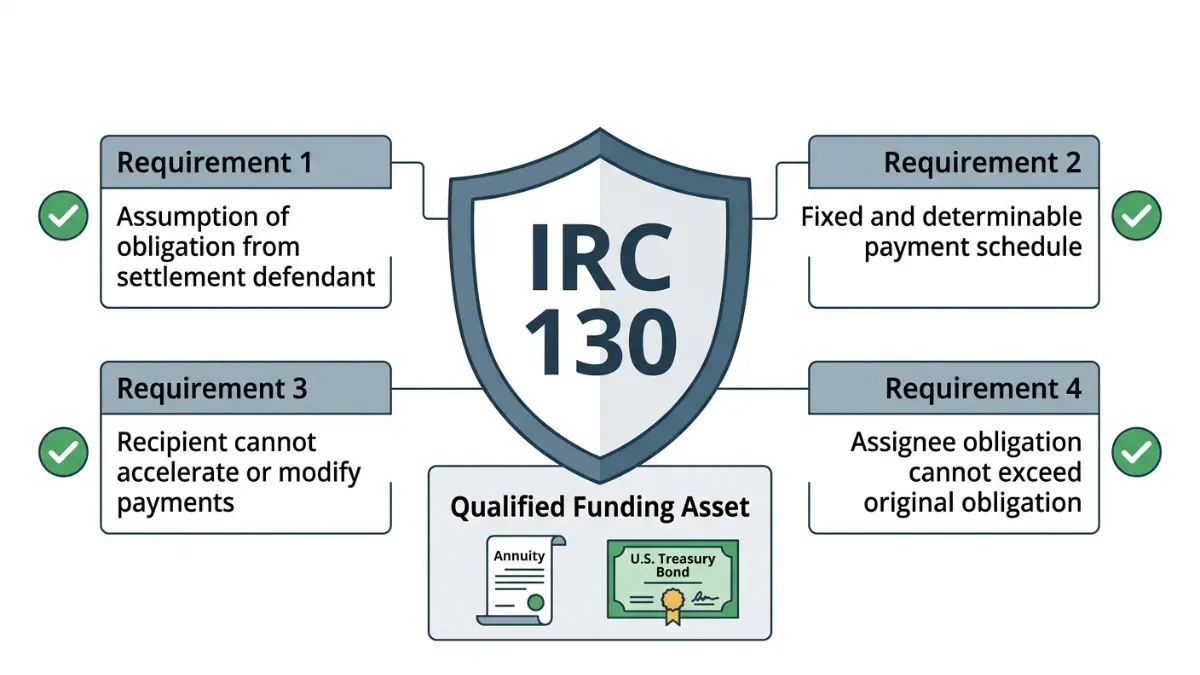

What IRC Section 130 actually requires

A qualified assignment has to clear a four-part test. Get one wrong and the tax benefit can fail.

- The assignment company must assume the obligation from a party to the suit or settlement agreement, not a stranger to the case.

- The periodic payments must be fixed and determinable in amount and timing.

- You, the recipient, cannot accelerate, defer, increase, or decrease the payments once they are set.

- The assignee’s obligation cannot be greater than the obligation the original defendant had.

The payments also have to be funded by a qualified funding asset — almost always an annuity, occasionally a U.S. government obligation. You can confirm how the IRS treats injury damages in the IRS guidance on the tax implications of settlements and judgments.

Qualified versus non-qualified assignment

The difference decides when you pay tax. A qualified assignment delivers tax-free payments for physical-injury cases; a non-qualified assignment, used for cases that fall outside Section 104, generally defers tax until you receive each payment.

| Feature | Qualified assignment | Non-qualified assignment |

|---|---|---|

| Governing rule | IRC Section 130 | Outside Section 130 |

| Typical case | Physical injury or sickness | Non-physical claims, some attorney fees |

| Tax to recipient | Tax-free under 104(a)(2) | Deferred until received |

| Best for | Injury victims wanting tax-free income | Cases that cannot meet 130(c) |

If part of your settlement covers lost wages or punitive damages, that portion may be taxable — a point worth modeling with an income tax calculator that estimates federal tax on different income components.

How to vet the company holding your payments

Before you accept a structured settlement, vet the structure the same way a professional would.

The annuity is a long-dated promise, so the issuer’s strength is the first thing to confirm. A high financial-strength rating is what tells you the payments will still arrive in year 25.

Run through these checks before signing:

- Confirm the assignment document explicitly references IRC Section 130 and names the assignment company assuming the obligation.

- Verify the issuing life insurer carries a strong financial-strength rating from a recognized agency.

- Check that the payment schedule is fixed, dated, and matches what you were told verbally.

- Ask whether the funding asset is an annuity and who issues it.

If part of your plan is to use the income in later years, it helps to see how that stream fits a broader plan using a retirement calculator that projects income against future expenses or a 401(k) calculator that models employer-plan growth alongside it.

✅ Pro Tip: Within 48 hours of receiving a settlement offer, ask your attorney for the assignment company name and the issuing insurer, then look up that insurer’s current financial-strength rating yourself. A reputable settlement planner will hand this over without hesitation.

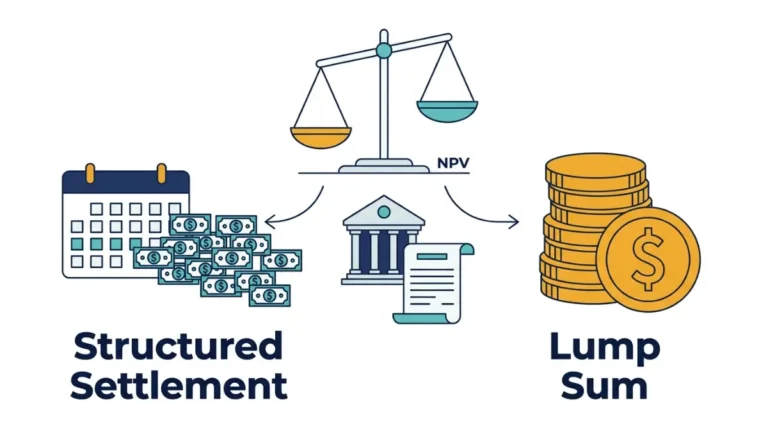

What it really costs to sell your future payments

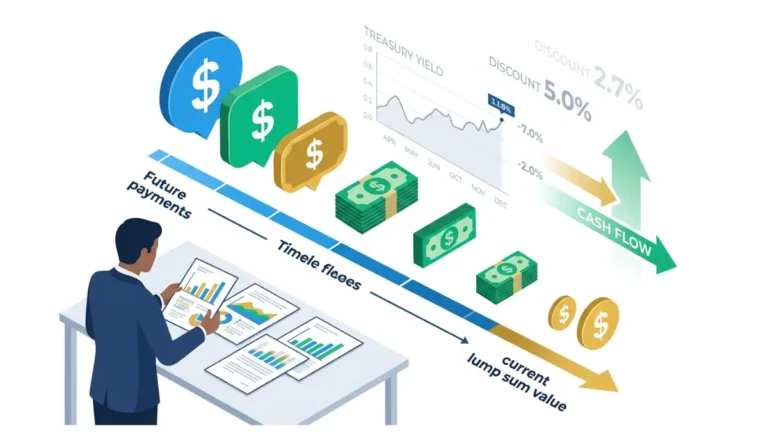

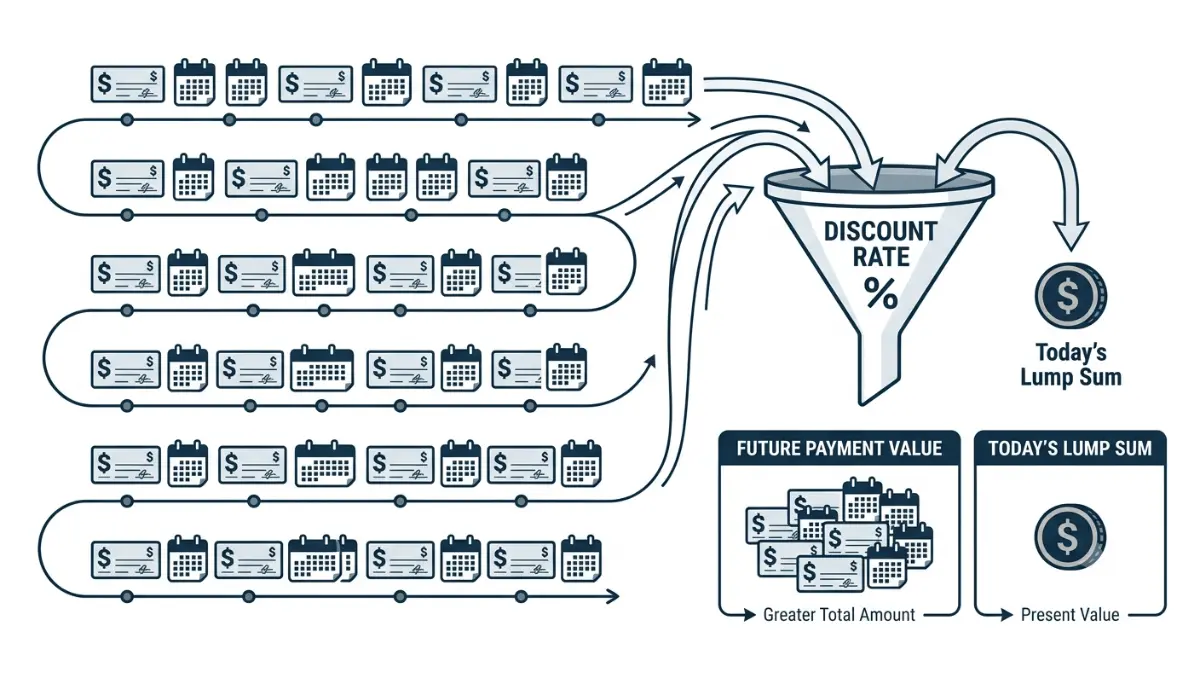

Selling your payments is legal, but the discount rate — not a flat fee — is where most of the money disappears.

When you sell, a factoring company pays you a lump sum today that is worth less than the total future payments. The gap between those two numbers is the factoring discount.

📊 Data Point: Federal law imposes a 40% excise tax on the factoring discount of a structured settlement transfer that is not approved in advance by a court — Source: IRS, About Form 8876 (Rev. December 2025).

Here is the part that confuses most sellers. That 40% excise tax falls on the buyer, not on you, and a court-approved sale removes it entirely.

The cost you actually feel is the discount rate the buyer builds into its offer. Industry discount rates on these transfers commonly fall somewhere in the low-to-high teens annually, which is why a large face value can convert to a much smaller check.

A simple illustration shows the gap. A stream of payments worth a high face value over a decade can net far less than half of that face value once a double-digit discount rate is applied — the exact figure depends entirely on your rate and timing.

To see what a future stream is worth in today’s dollars, model it with a present-value style compound interest calculator and compare the result against any offer using an investment calculator that projects what a lump sum could earn if invested instead. If part of what you sell is taxable, estimate that bite with a capital gains tax calculator.

💡 Expert Note (CFA): The most expensive mistake I see is reading the offer as a “fee” instead of a rate. A company can quote a friendly-sounding lump sum while the implied annual discount rate runs well into the teens — always ask for the discount rate in writing, then compare it to what those payments would be worth invested elsewhere.

The steps to sell payments legally with court approval

You cannot simply sign a contract and cash out — a judge has to approve the transfer first.

Every state with a Structured Settlement Protection Act requires court review, and that review is what keeps the federal excise tax from applying. The judge’s job is to decide whether the sale is in your best interest.

The process runs in a clear sequence:

- Request a quote from a buyer and get the discount rate and net payout in writing before agreeing to anything.

- File a transfer petition in court under your state’s structured settlement protection act.

- Attend the court review, where a judge weighs whether the sale serves your best interest.

- Receive the qualified order if the judge approves, which legally clears the transfer.

- Complete the transfer and receive your lump sum once the order is final.

📊 Data Point: Late filing of the excise-tax return carries a penalty of 5% per month up to 25%, and late payment adds 0.5% per month up to 25% — Source: IRS, Instructions for Form 8876 (December 2025).

A judge can and does reject sales that look predatory. You can read the federal filing rules and the court-approval exception in the IRS instructions for Form 8876.

When selling your settlement is the wrong move

Selling is permanent, so the decision deserves the same scrutiny as the day you accepted the settlement.

Watch for pressure tactics. A buyer rushing you toward signing, dodging the discount-rate question, or downplaying the court step is showing you exactly who they are.

Red flags worth stopping for:

- The buyer will not put the discount rate and net payout in writing before you commit.

- You are being steered to an “independent” advisor the buyer is paying.

- A lump sum could push you into a higher tax bracket or affect benefit eligibility.

- You are selling to cover a short-term gap that other tools could bridge.

Often the better fix is a smaller, reversible one. Before trading away tax-free income, price the alternatives with a budget calculator that maps income against expenses, build a buffer using a savings calculator that shows how fast an emergency fund grows, or compare the math on a debt consolidation calculator if high-interest debt is the real problem.

⚠️ Warning: The Consumer Financial Protection Bureau has taken enforcement action against factoring companies that steered injury victims into bad transfers. Before signing away future payments, review the CFPB’s guidance on giving up structured settlement payments for a lump sum and talk to the lawyer who handled your case.

Frequently asked questions

1. What is a qualified assignment structured settlement?

A qualified assignment structured settlement is an arrangement where the defendant transfers its payment obligation to an assignment company under IRC Section 130. This makes injury payments tax-free for you and removes the long-term liability from the defendant. The assignment company funds the payments through an annuity it owns.

2. What is IRC Section 130?

IRC Section 130 is the tax rule that lets an assignment company exclude from income the money it receives to fund your settlement payments. Without it, the qualified assignment structured settlement structure would not work, because the company would owe tax with no matching source to pay it.

3. Are structured settlement payments taxable?

Structured settlement payments for personal physical injury or sickness are not taxable, under IRC Section 104(a)(2). The qualified assignment preserves that tax-free treatment. Portions tied to lost wages, punitive damages, or interest can be taxable, so allocation in your settlement agreement matters. Confirm specifics with a licensed tax professional.

4. Who is the assignment company in a structured settlement?

The assignment company is the party that legally assumes the defendant’s obligation to pay you and owns the annuity that funds it. In a qualified assignment structured settlement, it is usually an affiliate of a major life insurer, which is why the insurer’s financial strength deserves a careful look.

5. What is a qualified funding asset?

A qualified funding asset is the investment the assignment company uses to fund your payments under IRC Section 130. It is almost always an annuity from a life insurer, and occasionally a U.S. government obligation. The asset must match the payment schedule promised in your qualified assignment structured settlement.

6. Can I sell my structured settlement payments?

Yes, you can sell some or all of your structured settlement payments, but the sale requires court approval in nearly every state. A judge must find the transfer is in your best interest. Selling converts tax-free future income into a discounted lump sum, so weigh it carefully against your long-term needs.

7. How much do you lose when selling a structured settlement?

When selling a structured settlement, you lose the difference between the total future payments and the discounted lump sum you receive. Discount rates commonly run into the teens annually, which can cut a large face value to a much smaller payout. Always get the discount rate in writing.

8. Do I need court approval to sell a structured settlement?

Yes, nearly every state requires a judge to approve the sale of a structured settlement before it is valid. The court reviews whether the transfer serves your best interest. This court approval, issued as a qualified order, is also what prevents the federal 40% excise tax from applying to the buyer.

9. What is the 40% excise tax on structured settlements?

The 40% excise tax applies to a buyer who acquires structured settlement payment rights without advance court approval. It equals 40% of the factoring discount and falls on the buyer, not the seller. A court-approved transfer through a qualified order removes the tax entirely.

10. Is the money I get from selling my settlement taxable?

The lump sum from selling injury-based structured settlement payments generally keeps the tax-free character of the original payments, because federal law preserves that treatment after a court-approved transfer. Receiving a large amount at once can still affect your tax bracket or benefits, so review the timing with a licensed tax professional.

11. What is the difference between a qualified and non-qualified assignment?

A qualified assignment under IRC Section 130 delivers tax-free payments for physical-injury cases and lets the assignment company exclude the funding amount from income. A non-qualified assignment, used when a case cannot meet Section 130 requirements, generally defers your tax until you actually receive each payment.

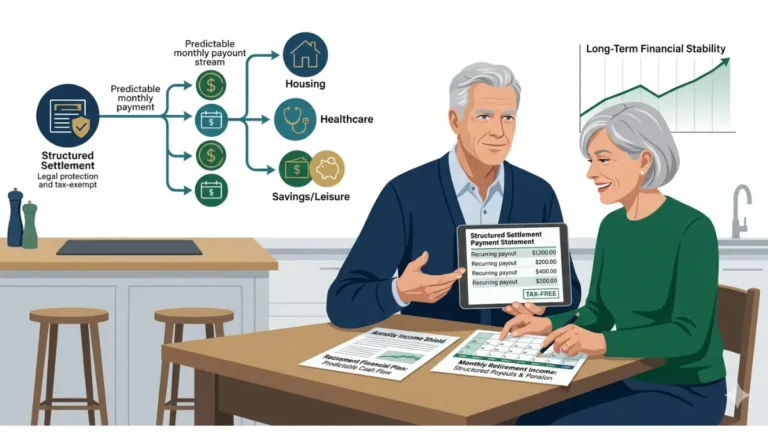

The bottom line on qualified assignments

A qualified assignment is the quiet mechanism that makes a structured settlement work — it shifts the obligation off the defendant and keeps your injury payments tax-free under IRC Section 130.

If you are accepting a settlement, vet the assignment company and the insurer behind the annuity before you sign. If you are thinking about selling, remember that a judge must approve it and the discount rate is the real cost.

The structure was built to protect you. Treat any decision to give it up with the same care you would give the original claim.

Run your own numbers, get every rate in writing, and have a licensed tax professional and a qualified financial advisor review the decision before you commit.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.