The Real Tax Rules for Structured Settlement Retirement Income

Structured settlement retirement income is federally tax-free — but one IRS carve-out and a factoring decision can erase $30,000. Know both rules first.

In This Article

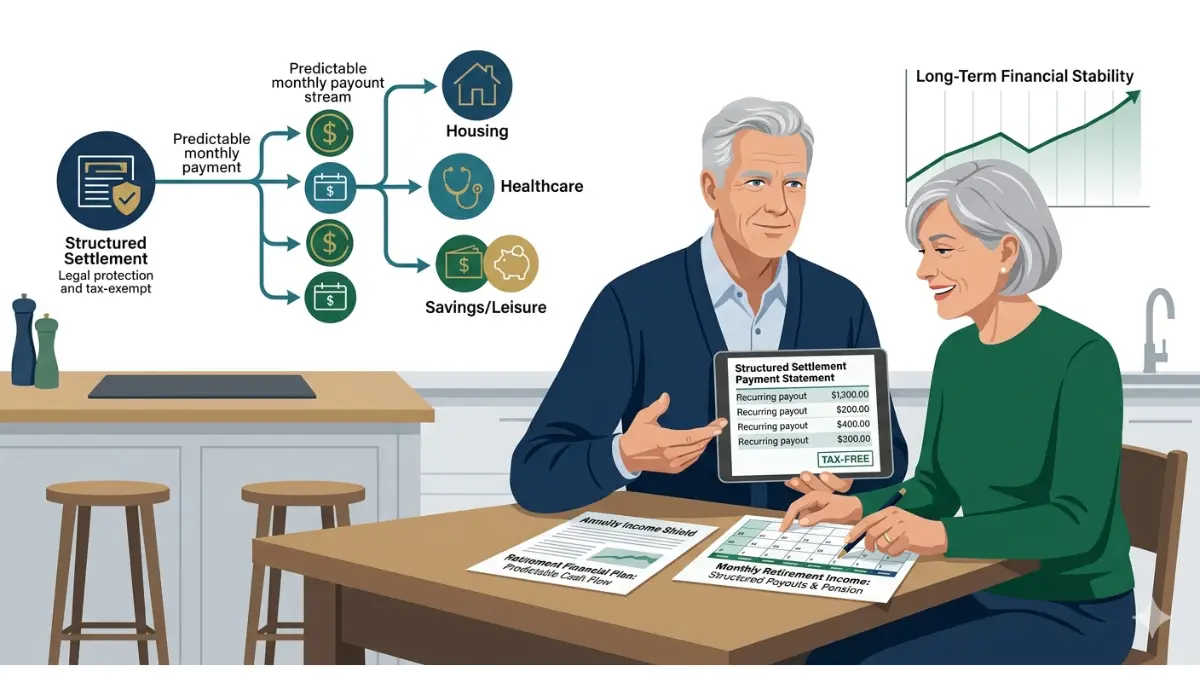

What structured settlement payments can do for your retirement

Most people who hold a structured settlement know the payments are “supposed to be tax-free.” Very few know exactly when that holds — and when it doesn’t.

That distinction is the difference between a retirement built on a confirmed income floor and one built on an assumption that could collapse under an IRS audit.

Why this income source is different from a pension or Social Security

A traditional pension is fully taxable as ordinary income. Social Security benefits become partially taxable once combined income exceeds $25,000 for single filers under 2026 IRS thresholds.

A qualifying structured settlement annuity is excluded from federal gross income under IRC §104(a)(2) — a statutory carve-out, not a general rule, that has survived every major federal tax revision since its 1982 enactment.

That means qualifying settlement recipients can retire with monthly income carrying no federal tax obligation at all — if the settlement qualifies under the statute.

Who this guide is for — and what decision it helps you make

This guide serves two readers: the near-retiree holding a payment schedule who needs to know whether the income is enough, and the current retiree already living on settlement payments who needs to confirm the tax treatment is correct.

The four-step framework in Section 3 is where both should start. [A full breakdown of structured settlement payment schedules and how they’re built covers the foundational mechanics if you need them before going further.]

The IRS tax rule that makes structured settlements work in retirement

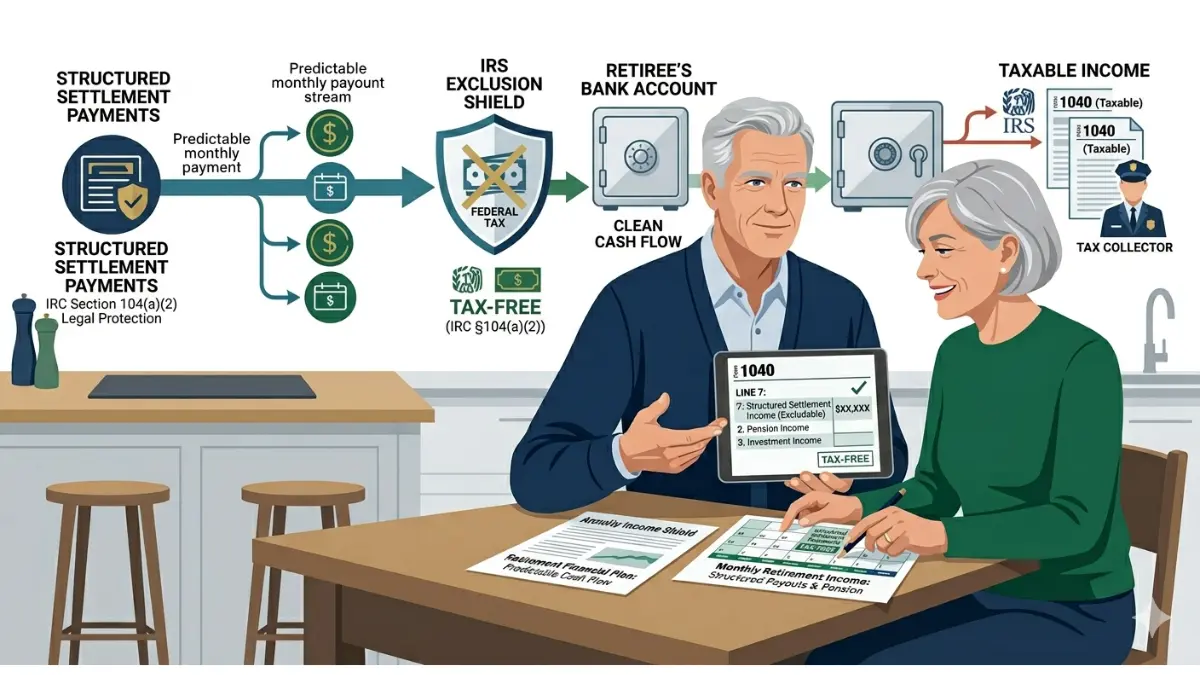

Under IRC Section 104(a)(2), structured settlement payments received as compensation for physical injury or physical sickness are excluded from federal gross income — including when received during retirement, regardless of the recipient’s age or other income sources.

This exclusion does not appear on your Form 1040. It does not affect your adjusted gross income. It does not trigger the Medicare IRMAA surcharge. The exclusion operates as if the payments do not exist for federal income tax purposes.

How IRC Section 104(a)(2) defines the tax-free exclusion

Three conditions must be met: the payments must originate from a legal settlement, the underlying claim must involve physical injury or physical sickness, and the payment stream must not include punitive damages or accrued interest.

When all three are satisfied, the tax-free income exclusion applies for the life of the payment stream — whether payments last 10 years or 40.

📊 Data Point: IRS Publication 525 (2026 edition) classifies qualifying personal injury compensation under §104(a)(2) as nontaxable income and governs the reporting rules for structured settlement recipients. Confirm the current edition at IRS Publication 525 — Source: Internal Revenue Service, 2026.

What the exclusion does not cover — three critical exceptions

The §104 exclusion is not universal. Three categories generate fully taxable ordinary income even when embedded in a structured settlement:

- Punitive damages — taxable as ordinary income regardless of how they are labeled in the settlement agreement, even when awarded alongside qualifying compensatory damages

- Accrued interest — if the settlement generates interest during any deferral period before payments begin, that interest income is taxable even if the underlying compensation is fully excluded

- Non-physical injury claims — emotional distress settlements where no physical injury underlies the claim do not qualify for the §104(a)(2) exclusion under current IRS guidance

⚠️ Warning: Workers’ compensation settlements are governed by a separate exclusion under IRC §104(a)(1) — not §104(a)(2). A workers’ compensation recipient who assumes the same tax protection applies as in a personal injury structured settlement is working from an incorrect premise. The rules are different, and confusing them is one of the most common tax errors I review in client situations.

How a qualified assignment preserves the tax-free status

When a settlement is reached, the defendant typically does not fund the annuity directly. Instead, the payment obligation is transferred to a qualified assignment company, which purchases an annuity from a life insurance carrier to fund the payments.

That transfer structure is what preserves the §104(a)(2) exclusion for the life of the payment stream — a detail that matters when readers are evaluating whether to supplement, sell, or restructure their payments. [For a deeper look at whether your specific settlement income qualifies as tax-free, our dedicated tax guide covers the conditions by settlement type.]

To model how your total retirement income intersects with your annual federal tax liability, the income tax calculator gives you a 2026 projection across all income sources.

How to build a retirement income plan around your settlement payments

To use structured settlement payments as retirement income effectively, map your existing payment schedule against your projected monthly expenses before claiming Social Security, before purchasing any supplemental product, and before any conversation with a factoring company.

These four steps produce the complete picture.

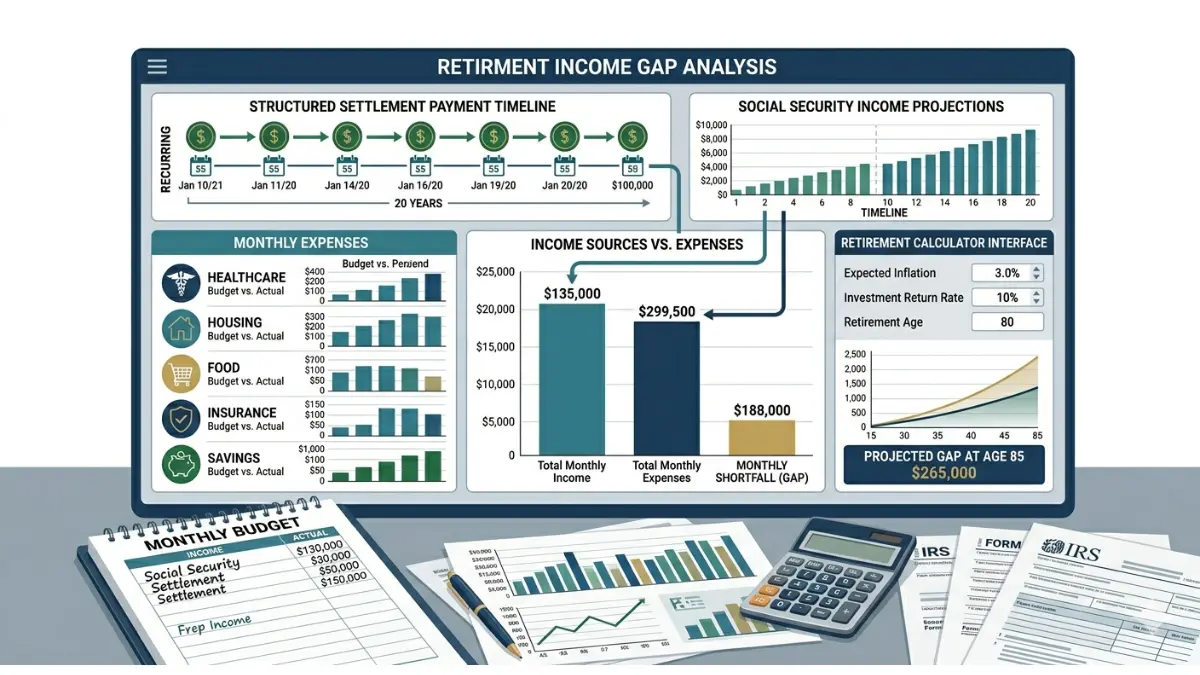

Step 1 — Map your payment schedule against your retirement timeline

Pull your settlement agreement and list every scheduled payment amount and its date through the final payment.

Then plot those payments against a retirement timeline showing when you plan to retire, when Social Security would begin at three possible claiming ages, and when your final settlement payment arrives — gaps on that timeline are where your income replacement ratio risk lives.

Step 2 — Calculate your monthly income gap using your expense baseline

📊 Data Point: The Bureau of Labor Statistics Consumer Expenditure Survey (most recent data released in 2026) shows average annual household expenditures for adults aged 65–74 at approximately $57,800 — roughly $4,820 per month. Verify current figures at the BLS Consumer Expenditure Survey — Source: Bureau of Labor Statistics, 2026.

Subtract your structured settlement periodic payments monthly total from your projected monthly expense figure.

The result is your income gap — the dollar amount that must come from Social Security, savings, or a supplemental income product to cover basic retirement costs without drawing down principal.

Step 3 — Layer in Social Security to find your coverage window

Social Security benefit amounts vary significantly by claiming age. For 2026, the average monthly retirement benefit at full retirement age is approximately $1,976, based on the Social Security Administration’s post-COLA 2026 figures.

The Social Security calculator estimates your specific benefit at ages 62, 67, and 70 — the three claiming points where the lifetime income difference is largest. The budget calculator establishes your actual monthly expense baseline before you run the gap analysis.

Step 4 — Identify the shortfall and choose a supplemental strategy

💡 Expert Note (CFA): The clients who closed their retirement income gaps most efficiently were the ones who delayed Social Security — not the ones who claimed at 62 to “get it started.” One client receiving $3,200 per month in structured settlement income eliminated a $740 monthly shortfall entirely by delaying Social Security from 62 to 67. Over a 20-year retirement horizon, that single timing decision produced an estimated $89,000 in additional lifetime income. The math on Social Security timing is not subtle — it is one of the highest-return decisions most near-retirees can make.

Once your gap is quantified, match it to one of the three strategies in Section 4.

The retirement calculator lets you model your complete income stack — settlement payments, Social Security at different claiming ages, and savings — in a single projection before committing to any strategy.

Keep, sell, or supplement — choosing your structured settlement strategy

A structured settlement annuity and a commercial annuity both deliver periodic income — but they differ on tax treatment, flexibility, insolvency protection, and what happens to the payment stream when an issuing company faces financial trouble.

The decision between keeping the settlement, selling future payments, or supplementing with another product is not a product comparison. It is a retirement income architecture decision that requires your specific payment schedule, your projected lifespan, and your monthly expense number before it has a correct answer.

Option 1 — Keep the settlement intact as primary retirement income

Keeping the settlement intact is the lowest-risk, lowest-cost option for most qualifying recipients. No transaction fees. No court appearances. No discount rate losses. The §104 tax-free income exclusion remains fully intact for the life of the payment stream.

The primary risk is inflexibility: if expenses spike — major medical care, housing repair, family emergency — you cannot accelerate your payment schedule without either a formal judicial process or a permanent factoring transaction.

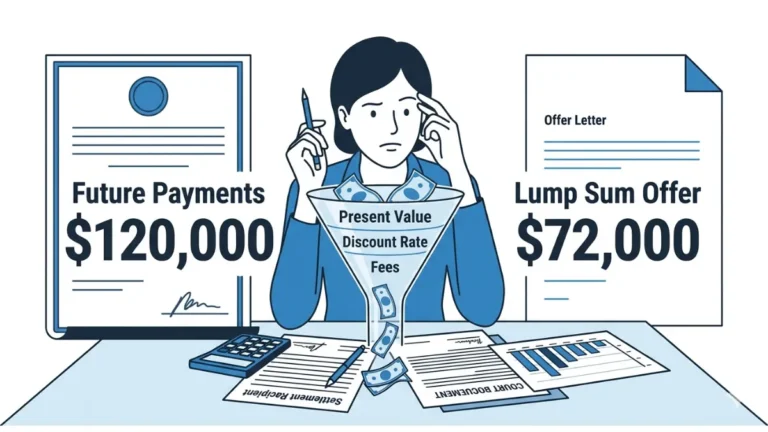

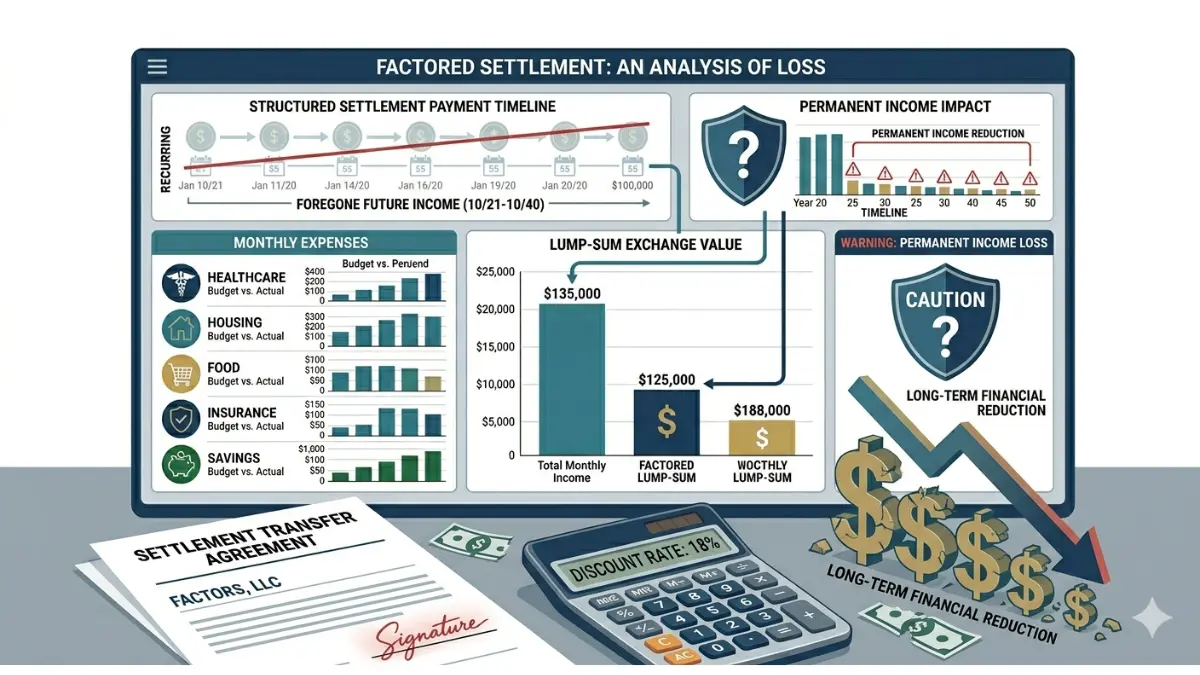

Option 2 — Sell a portion of future payments for a lump sum

Selling future payments through a factoring transaction converts scheduled income into an immediate lump sum — at a permanent and non-recoverable cost. A 15% discount rate applied to $200,000 of present-value payments means $170,000 received and $30,000 permanently gone.

Section 5 covers the full cost structure and the red flags every recipient should know before this conversation goes further.

Option 3 — Supplement with a commercial annuity or bridge strategy

A commercial annuity can fill the income gap between when settlement payments end and when Social Security begins, or bridge early retirement before Social Security eligibility. Unlike a structured settlement, commercial annuity payouts are only partially excluded from income under the exclusion ratio method — not fully excluded under §104.

[Our dedicated guide to how annuities function as income vehicles compares payout rates, tax treatment, and product types side by side for 2026.]

Decision matrix — which option fits your income profile

| Strategy | Tax Treatment | Flexibility | Monthly Income Certainty | Best For |

|---|---|---|---|---|

| Keep settlement intact | Tax-free (§104(a)(2)) | Low — fixed schedule | High | Recipients whose payment term covers full retirement horizon |

| Sell payments (factoring) | Lump sum may be taxable | One-time — irreversible | Eliminates future income | Emergency liquidity only — highest permanent cost |

| Add commercial annuity | Partially taxable (exclusion ratio) | Low once purchased | High | Closing income gap after settlement payments end |

| Delay Social Security | Partially taxable above threshold | Timing decision — reversible before claim | Increases permanently at claim | Recipients with 5+ years before full retirement age |

Source: IRS §104(a)(2); SSA 2026 benefit tables; FINRA investor education — 2026

💡 Expert Note (CFA): The table above is the starting framework, not the final answer. A recipient whose settlement pays $1,800 per month with a $4,800 monthly expense baseline has a fundamentally different problem than one whose settlement covers 95% of projected expenses. Run your specific numbers before evaluating any product — the math changes everything.

[The comparison of keeping structured settlement payments versus taking a lump sum walks through the long-term income math in full detail for readers who are still deciding between Option 1 and Option 2.]

What to know before selling structured settlement payments in retirement

The secondary market for structured settlement payments is one of the most aggressively marketed financial transactions in personal finance. It is also one of the most permanent.

Once a factoring transaction is court-approved and executed, no future payment can be recovered at any price.

How factoring companies calculate your discount — and what it costs you

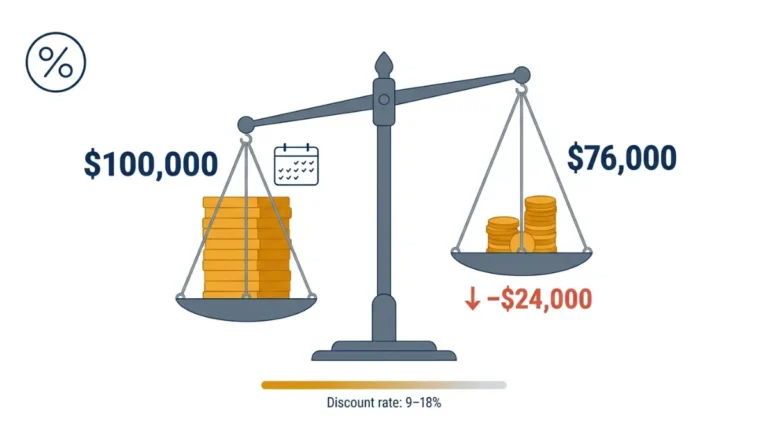

Factoring companies apply a discount rate — typically between 9% and 18% in the current market — to the present value of your remaining payments. That rate is their profit margin, and it comes directly out of your retirement income.

A recipient with $180,000 in remaining payment present value who accepts a 15% discount rate receives $153,000. The $27,000 difference is permanently gone — not deferred, not recoverable, gone.

📊 Data Point: FINRA’s investor guidance on structured settlement factoring warns that discount rates are not regulated at the federal level and vary substantially by company, making independent rate comparison essential before any agreement is signed. Verify current FINRA guidance at the FINRA structured settlement investor alert — Source: FINRA, 2026.

[Our detailed breakdown of how factoring companies calculate your discount rate shows you how to evaluate competing offers — and which numbers actually matter.]

The court-approval requirement most sellers do not know exists

Every structured settlement factoring transaction in the United States must be reviewed and approved by a judge before it becomes legally binding.

That court hearing exists specifically to protect the seller. A judge must determine whether the transaction is in your “best interest” — a standard that the factoring company’s paperwork is not designed to satisfy.

Red flags that signal a predatory factoring offer

⚠️ Warning: Do not sign any factoring agreement before a court hearing takes place. Any company that pressures you to sign before judicial review — or offers to expedite, waive, or “handle” the court process for you — is operating in direct conflict with your state’s Structured Settlement Protection Act. End the conversation and contact an attorney before responding further.

Five warning signs of a predatory offer:

- Discount rate exceeds 15% — reputable offers on standard payment streams typically fall between 9–12%; above 15% warrants a competing bid before any further discussion

- Unsolicited contact — the offer arrived by phone, mail, or online ad rather than originating from your own inquiry

- Independent counsel is discouraged — any company that discourages or delays your access to independent legal advice is signaling the offer cannot withstand scrutiny

- No verifiable state license — structured settlement purchasers must hold state-specific licenses; request the license number and verify it independently

- Artificial deadline — a same-day or 48-hour deadline on a transaction of this permanence has no legitimate financial basis

[Our structured settlement scams and red flag guide documents the most common predatory patterns reported from 2024–2026.]

Your legal rights as a structured settlement recipient in retirement

Every structured settlement recipient in the United States operates within two layers of legal protection that most people do not know exist until they need them — and by then, it is often too late to use them effectively.

What the Structured Settlement Protection Act actually protects

The Structured Settlement Protection Act (SSPA) is not a single federal law. It is a model statute adopted in 49 states and the District of Columbia, each with state-specific variations in enforcement standards and review timelines.

Its core function: no structured settlement payment can be sold, transferred, or assigned to a third party without a court issuing a formal approval order — and that order cannot be issued unless a judge concludes the transaction is in the seller’s “best interest.”

[The CFPB’s plain-language explanation of structured settlements and what consumer protections apply is the clearest independent starting point for recipients unfamiliar with their rights.

Anti-assignment clauses and why they matter for retirement planning

Many structured settlement agreements contain an anti-assignment clause — a provision that explicitly prohibits the recipient from voluntarily transferring or selling future payments to any third party.

If your agreement contains one, a factoring transaction may not be legally possible regardless of what a factoring company’s sales representative tells you. Pull your original settlement documents before any conversation with a buyer advances past initial inquiry.

When court approval is required — and what it reviews

💡 Expert Note (CFA): Anti-assignment clauses are among the most misunderstood — and most costly — provisions in structured settlement agreements. I have reviewed situations where clients paid application fees to factoring companies, moved through preliminary paperwork, and only discovered the anti-assignment clause during the court hearing process. Read your agreement first. If you no longer have a copy, contact the original attorney who negotiated the settlement — that copy exists somewhere.

Court approval is required for every factoring transaction in every SSPA-jurisdiction state, with no exceptions for urgency, financial hardship, or agreement between the parties.

[The complete court approval process — what documents the judge reviews, how long approval typically takes, and what causes petitions to be denied — is covered in our structured settlement court approval guide. For recipients on Medicaid, how structured settlement payments interact with Medicaid income and asset thresholds is a separate question this guide addresses in full with 2026 state threshold data.]

Your structured settlement can fund retirement — if you plan it correctly

A structured settlement retirement strategy is not complicated. The income is real, the tax protection is statutory, and the planning framework is four steps.

The mistake most recipients make is treating the settlement as background financial fact rather than an active retirement income tool that requires sequencing, gap analysis, and professional review before any structural change is made.

Three steps to take this week

- Pull your original settlement agreement and confirm the §104(a)(2) exclusion applies to your specific claim type — punitive damages and workers’ comp operate under different rules

- Use the Social Security calculator to model your benefit at 62, 67, and 70 against your settlement payment timeline — the gap that emerges is your planning problem to solve

- Before changing anything about your settlement structure, retain a fiduciary financial advisor who holds no financial relationship with any factoring company — that independence is not optional

Your next conversation should be with a fiduciary

💡 Expert Note (CFA): In 28 years of portfolio strategy work, the clients who reached retirement with the most financial stability shared one trait: they treated professional financial counsel as a planning tool, not a last resort. A structured settlement is a significant income asset. A fiduciary CFA or CFP can model your specific payment schedule, income gap, and Social Security timing in a single session — and that conversation is worth considerably more than any amount of time spent processing it alone.

The retirement calculator lets you run your first projection right now — settlement payments, Social Security, and savings in one view — before your advisor conversation begins.

Frequently asked questions about structured settlements and retirement

1. Are structured settlement payments taxable when I receive them in retirement?

Structured settlement payments qualifying under IRC §104(a)(2) — compensating for physical injury or physical sickness — are excluded from federal gross income regardless of the recipient’s age or retirement status. Payments involving punitive damages or accrued interest are taxable regardless. Consult a licensed tax professional to confirm your specific settlement type qualifies under current IRS guidelines.

2. Can I use my structured settlement income instead of Social Security?

A qualifying structured settlement provides tax-free periodic income that can delay or supplement Social Security — but it cannot permanently replace it for most retirees. Settlement payments have a defined end date; Social Security does not. Recipients who delay Social Security while receiving settlement income typically capture substantially more in lifetime benefits than those who claim early.

3. What happens to my structured settlement payments when I die?

It depends on your agreement. Some structured settlements include a guaranteed payment schedule that continues to a named beneficiary after the recipient’s death; others terminate with the recipient. Review the “certain payments” or “guaranteed period” provisions in your original agreement and confirm beneficiary designations with an estate attorney before assuming any survivor benefit exists.

4. Can I sell my structured settlement payments to fund my retirement?

Selling structured settlement payments through a factoring transaction is legally permitted in most states but carries permanent income cost. Factoring companies apply discount rates of 9–18%, meaning $200,000 in present-value payments may yield $164,000–$182,000 in cash. Every state with a Structured Settlement Protection Act requires court approval before the sale is legally binding.

5. How much monthly income can a structured settlement realistically provide in retirement?

Structured settlement monthly payment amounts vary widely based on the original settlement size and payment term negotiated at settlement. A $500,000 settlement structured over 20 years may generate $2,200–$3,500 per month depending on the annuity rate at the time of settlement. The BLS 2026 Consumer Expenditure Survey puts average monthly retirement household spending at approximately $4,820.

6. Is a structured settlement better than buying an annuity for retirement income?

For tax treatment, a qualifying structured settlement annuity is superior — payments are fully excluded from federal income under §104(a)(2). Commercial annuity payouts are only partially excluded under the exclusion ratio method and generate taxable ordinary income for the remainder. For flexibility and inflation protection, commercial annuities offer more customization options than a fixed structured settlement schedule.

7. Do structured settlement payments affect my Social Security disability benefits?

Structured settlement periodic payments are not earned income and generally do not reduce Social Security retirement benefits. For recipients receiving SSDI, lump-sum structured settlement payments may trigger a review under offset rules, while smaller periodic payments are typically not treated as countable income. Verify your specific SSDI interaction directly with the Social Security Administration before any settlement modification.

8. What is the Structured Settlement Protection Act and does it protect me?

The Structured Settlement Protection Act is a model statute adopted in 49 states and the District of Columbia requiring court approval before any structured settlement payment is sold or transferred. The presiding judge must find the transaction is in the seller’s best interest — a standard no factoring company paperwork satisfies unilaterally. SSPA protections vary by state; know your jurisdiction’s specific requirements.

9. Can I change my structured settlement payment schedule after I retire?

Standard structured settlement agreements cannot be unilaterally modified after execution — both the original defendant and the qualified assignment company are bound by the agreed payment terms. The only legal mechanism to alter payment timing or amounts is a factoring transaction requiring court approval, or a structured settlement modification agreement requiring written consent from all original parties to the settlement.

10. Are structured settlement payments counted as income for Medicaid eligibility?

Whether structured settlement payments count toward Medicaid income eligibility depends on state methodology, program type, and payment frequency. Federal Medicaid income thresholds and asset rules vary significantly between standard Medicaid expansion and long-term services programs — and between states. Verify current 2026 thresholds at Medicaid.gov and confirm with a benefits counselor how your specific payment schedule is treated before filing.

11. What is a qualified assignment in a structured settlement?

A qualified assignment transfers the defendant’s structured settlement payment obligation to a third-party company — typically an insurance company subsidiary — which then purchases an annuity to fund the payments. This structure is what preserves the IRC §104(a)(2) tax-free exclusion for the life of the payment stream. Without a proper qualified assignment, the exclusion may not apply to the recipient’s payments.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.