Social Security Calculator: Find Your 2026 Exact Benefit

Social Security Calculator

Estimate U.S. Social Security retirement benefits across claiming ages using PIA-at-FRA (best input) or an optional “benefit at 62 → infer PIA” mode. Includes detailed timelines, break-even ages, PV, and exportable tables. Currency choice is for display.

Inputs

Social Security is USD-based; this is just for formatting in your UI.

Used for delayed-credit % banding; leave blank if unknown.

Used to project benefit increases over time (approx).

Results

PIA + ages

PIA at FRA: —

FRA: — • Claim: —

Benefit at claiming age

—

Annual (approx): —

Adjustment: — (—)

Lifetime totals (to life expectancy)

Nominal: —

Today’s $ (inflation-adj): —

Present value (PV): —

“Best” under your assumptions

Highest lifetime total: —

Highest PV: —

Break-even A→B: —

Break-even B→C: —

Claiming-age grid (every 3 months)

| Claim age | Monthly benefit | Factor vs PIA | Adjustment type |

|---|

Timeline (yearly snapshots)

| Age | Started? | Monthly benefit | Annual benefit | Cumulative nominal | Cumulative real | Cumulative PV |

|---|

Scenario comparison

| Claim age | Monthly at start | Lifetime nominal | Lifetime real | Lifetime PV | Note |

|---|

Results appear after you click “Calculate.”

In This Article

What Is a Social Security Calculator — And What Will You Get in 2026?

A Social Security calculator estimates your exact monthly retirement benefit based on three inputs: your Primary Insurance Amount (PIA), your Full Retirement Age (FRA), and the age you choose to claim. Use the calculator above to get your personalized estimate in under 60 seconds.

In 2026, the maximum monthly Social Security benefit is $5,251 — but only if you delay claiming until age 70 with a maximum earnings history. Most Americans receive far less.

Key insight most retirees miss: Your claiming age — not just your earnings — determines up to 77% of the difference in your monthly benefit. Getting this decision wrong costs the average American $100,000+ in lifetime benefits.

2026 Social Security Fast Facts

| Key Data Point | 2026 Figure |

|---|---|

| Maximum monthly benefit (age 70) | $5,251 |

| Average monthly retirement benefit | ~$1,976 |

| COLA increase (Jan 2026) | 2.8% |

| Social Security wage base | $184,500 |

| Full Retirement Age (born 1960+) | 67 years |

| Earliest claiming age | 62 years |

| Latest optimal delay age | 70 years |

| SSI maximum monthly (single) | $994 |

Sources: SSA.gov 2026 Fact Sheet | SSA COLA 2026 Announcement

What Our Social Security Calculator Does Differently

Our tool goes far beyond what NerdWallet, AARP, or SmartAsset offer. Here’s what you get:

- PIA-based precision — Enter your exact PIA from your SSA statement for the most accurate result

- Break-even age analysis — See exactly when delayed claiming overtakes early claiming in cumulative dollars

- 3-scenario comparison — Compare age 62 vs FRA vs 70 side-by-side with lifetime totals

- Inflation-adjusted lifetime value — Real dollars, not just nominal figures

- Downloadable CSV reports — Export your full timeline and scenario data

If you’re also planning your broader retirement strategy, our Retirement Calculator and 401(k) Calculator work directly alongside your Social Security projections.

How the Social Security Benefits Calculator Works — The Math Behind Your Benefit

Understanding how your benefit is calculated gives you a massive strategic advantage. Here’s the exact formula the Social Security Administration uses — explained in plain English.

Step 1 — Your AIME (Average Indexed Monthly Earnings)

The SSA takes your 35 highest-earning years, adjusts each year’s wages for inflation using national wage indexing, adds them up, and divides by 420 months (35 years × 12).

Real example: A worker who earned an average of $65,000/year over 35 years would have an AIME of approximately $4,583/month.

If you worked fewer than 35 years, the SSA fills the remaining years with $0 — which directly pulls your AIME down. This is one of the most overlooked ways Americans permanently reduce their benefit.

Step 2 — Your PIA (Primary Insurance Amount)

Your PIA is the monthly benefit you receive if you claim exactly at Full Retirement Age. It’s calculated by applying a progressive formula to your AIME using 2026 bend points.

2026 Bend Point Formula:

| AIME Bracket | SSA Replaces At | 2026 Thresholds |

|---|---|---|

| First $1,286 of AIME | 90% | Up to $1,286 |

| $1,286 – $7,749 of AIME | 32% | Between bend points |

| Above $7,749 | 15% | Above $7,749 |

Estimated PIA by Earnings Level (2026):

| Earner Type | Annual Earnings | Estimated Monthly PIA |

|---|---|---|

| Low earner | ~$25,000 | ~$900 |

| Average earner | ~$65,000 | ~$1,976 |

| High earner | ~$100,000 | ~$3,200 |

| Maximum earner | $184,500+ | ~$4,152 |

Pro tip from Daniel Moreau, CPA/CFP: “Your PIA is the single most important number in retirement planning. Get it from your My Social Security account at SSA.gov — don’t estimate it.”

Step 3 — How Claiming Age Adjusts Your Benefit

Once your PIA is established, your actual monthly benefit is adjusted based on how early or late you claim relative to your FRA.

Early claiming reduction (per federal regulation 20 CFR 404.410):

- First 36 months early: benefit reduced 5/9 of 1% per month

- Beyond 36 months early: reduced 5/12 of 1% per month

Delayed retirement credits (20 CFR 404.313):

- Each month past FRA up to age 70: benefit increases 2/3 of 1% per month

- Total maximum increase from FRA to 70: +24% to +32% depending on birth year

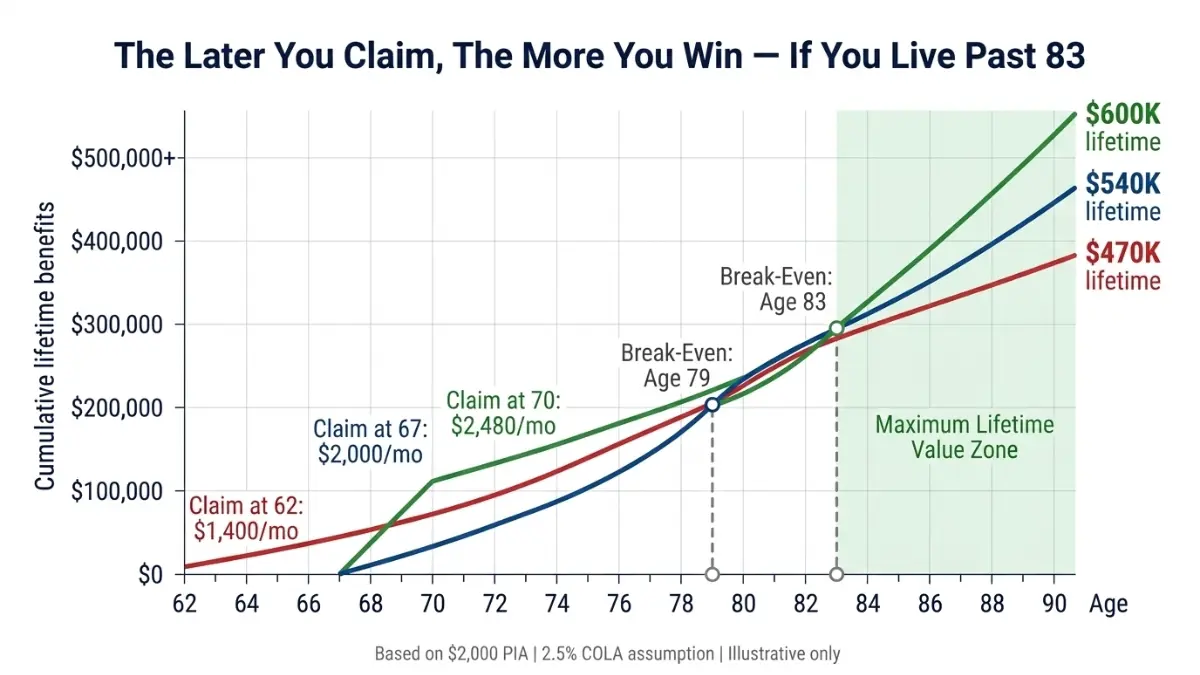

Benefit at Each Claiming Age (PIA = $2,000 example):

| Claiming Age | Monthly Benefit | vs. FRA |

|---|---|---|

| 62 | $1,400 | −30% |

| 64 | $1,600 | −20% |

| 67 (FRA) | $2,000 | Baseline |

| 68 | $2,160 | +8% |

| 70 | $2,480 | +24% |

How To Use Our Calculator — 5 Steps

- Enter your PIA from your official SSA statement (most accurate) — or enter your benefit at 62 and let the tool calculate PIA automatically

- Enter your birth year — this auto-populates your FRA and delayed credit percentage

- Set your claiming age — test age 62, 67, or 70 to see the immediate benefit difference

- Adjust COLA and inflation assumptions — default is 2.5% COLA and 3% inflation

- Run the 3-scenario comparison — compare all three claiming ages with lifetime nominal, real, and present value totals

When Should You Claim Social Security? The 62 vs 67 vs 70 Decision

This is the question every pre-retiree faces — and the answer directly determines hundreds of thousands of dollars in lifetime income. No competitor gives you this analysis in full. Here it is.

The Break-Even Age — The Most Important Number Nobody Tells You

Break-even age is the point where cumulative lifetime benefits from a later claiming age surpass cumulative benefits from an earlier age.

Real break-even example (PIA = $2,000):

| Comparison | Early Claimant Monthly | Later Claimant Monthly | Break-Even Age |

|---|---|---|---|

| Age 62 vs Age 67 | $1,400 | $2,000 | ~Age 78–79 |

| Age 67 vs Age 70 | $2,000 | $2,480 | ~Age 82–83 |

What this means: If you live past 79, claiming at 67 beats claiming at 62 — forever. If you live past 83, waiting until 70 beats everything.

Laura M. Bennett, CFP, advises: “For a healthy 62-year-old, the break-even math almost always favors waiting. The risk of living longer than expected is the biggest financial risk retirees face.”

5 Factors That Determine Your Best Claiming Age

- Health and family longevity — If you have serious health conditions, earlier claiming may make sense

- Spouse’s age and benefit level — Coordinating benefits can maximize your household’s lifetime total

- Other retirement income — If you have a pension, 401(k), or annuity income, you may have more flexibility to delay

- Current employment status — Earnings test applies if you claim before FRA while still working

- Break-even calculation result — Run your exact numbers in the calculator above

The True Cost of Claiming Too Early

Claiming at 62 instead of 70 on a $2,000 PIA means:

- Monthly difference: $1,080 less per month ($1,400 vs $2,480)

- Annual difference: $12,960 less per year

- Over 20 years of retirement: Over $200,000 in lost nominal benefits (before COLA growth)

“Waiting from age 62 to age 70 can increase your monthly Social Security benefit by up to 77%.” — SSA Delayed Retirement Credits data

What If You Keep Working After You Claim?

In 2026, if you claim before your FRA and continue working, the retirement earnings test applies:

- Under FRA in 2026: Benefits temporarily withheld if earnings exceed $22,320/year

- Year you reach FRA: Higher limit applies — approximately $59,520 in 2026

- After FRA: No earnings limit — you can work and collect full benefits simultaneously

Benefits withheld before FRA are not lost permanently — the SSA recalculates your benefit upward when you reach FRA. Use our Savings Calculator to model how bridge savings can replace income during a delayed claiming period.

How To Maximize Your Social Security Benefits in 2026

This is the section competitors skip entirely. Here are the proven strategies financial experts actually use with their clients.

Spousal Benefits — Up to 50% of Your Partner’s PIA

If your own retirement benefit is lower than 50% of your spouse’s PIA, you may be eligible to collect spousal benefits instead. Key rules in 2026:

- Your spouse must already be receiving retirement benefits

- Spousal benefit = up to 50% of spouse’s PIA (not their actual benefit)

- Divorced spouse rules: If you were married at least 10 years and are currently unmarried, you may qualify based on your ex-spouse’s record — without affecting their benefit

Official source: SSA.gov Spousal Benefits

Survivor Benefits — The Strategy Most Couples Get Wrong

When a spouse dies, the surviving spouse can receive the higher of the two benefits — not both. This makes the higher earner’s claiming decision critically important for the household.

- Survivors eligible from age 60 (or 50 if disabled), with marriage of at least 9 months

- Strategy: The higher earner delays to 70 to maximize the survivor benefit — even if the lower earner claims early

This connects directly to term life insurance planning and Medicare Advantage planning — all part of a coordinated retirement income strategy.

COLA — How Your Benefit Compounds Every Year

The 2026 COLA of 2.8% was applied to all Social Security benefits in January 2026. This is automatic — you do nothing.

Why delaying amplifies COLA: COLA is applied as a percentage of your benefit. A larger base benefit receives a larger dollar increase each year.

| Starting Benefit | After 10 Years at 2.5% COLA | After 20 Years |

|---|---|---|

| $1,400/month (age 62) | ~$1,794 | ~$2,299 |

| $2,000/month (age 67) | ~$2,563 | ~$3,285 |

| $2,480/month (age 70) | ~$3,178 | ~$4,073 |

Historical average COLA since 1975: 3.7% per year (SSA)

Social Security Tax Strategy — Up to 85% May Be Taxable

Many retirees are blindsided by Social Security taxes. Here’s the 2026 reality:

- Combined income = AGI + non-taxable interest + 50% of SS benefit

- Single filers: Up to 50% taxable above $25,000 combined; up to 85% above $34,000

- Joint filers: Up to 50% taxable above $32,000; up to 85% above $44,000

Key strategy: Roth IRA withdrawals do not count toward combined income. Converting pre-tax retirement assets to a Roth IRA before claiming Social Security can significantly reduce your taxable benefit — consult a licensed tax advisor for your situation. See also: 2026 Tax Brackets for full income tax planning context.

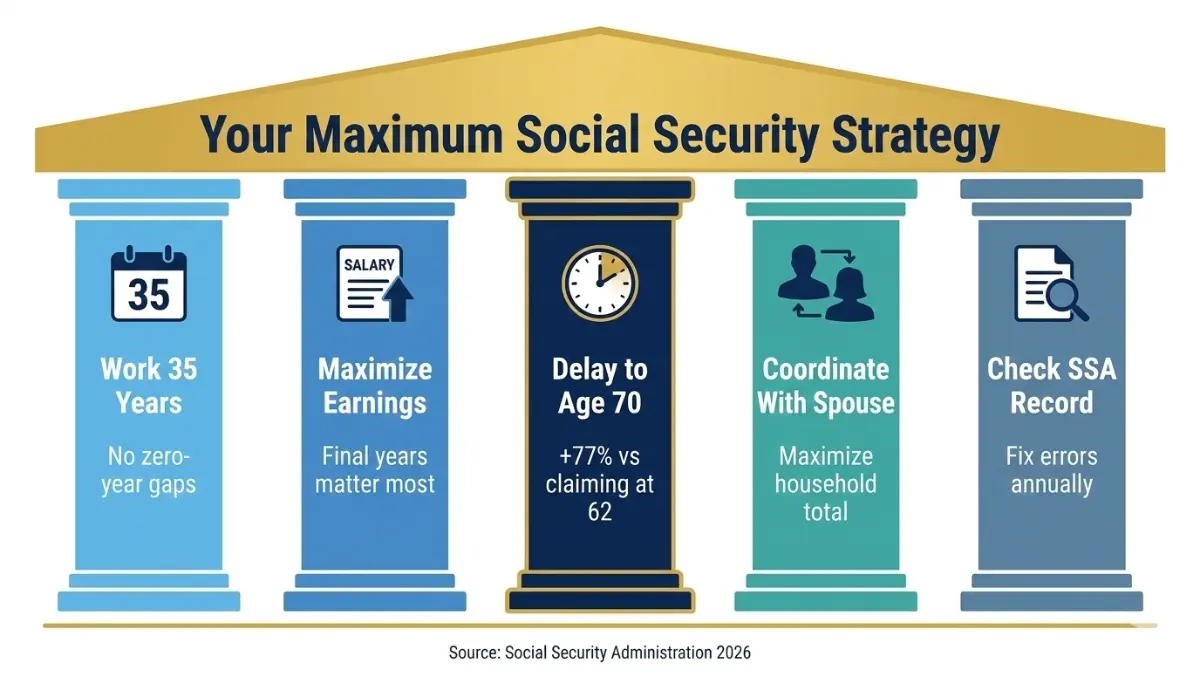

5 Proven Ways to Increase Your Social Security Benefit

- Work at least 35 years — Every year under 35 gets a $0 average that pulls your benefit down

- Maximize earnings in your final working years — High-income years replace low-income years in your 35-year average

- Delay claiming toward age 70 — Each month past FRA adds 2/3 of 1% to your benefit permanently

- Coordinate with your spouse — One delays, one claims early to optimize household cash flow and survivor protection

- Check your SSA earnings record annually — Errors in your record directly reduce your PIA; fix them at SSA.gov My Account

Social Security in 2026 — Key Numbers, Changes, and What’s Coming

Google Discover users scan this type of data table first. Here’s every major 2026 Social Security update in one place — something no single competitor has assembled.

Complete 2026 Social Security Changes Table

| What Changed | 2025 Figure | 2026 Figure | Impact |

|---|---|---|---|

| COLA increase | 2.5% | 2.8% | Higher monthly payments for all recipients |

| Maximum monthly benefit (age 70) | $5,108 | $5,251 | Top earners benefit most from delay |

| Social Security wage base | $176,100 | $184,500 | Higher earners pay SS tax on more income |

| Earnings credit per quarter | $1,810 | $1,890 | Slightly harder to earn work credits |

| Bend Point 1 | $1,226 | $1,286 | Progressive benefit formula threshold |

| Bend Point 2 | $7,391 | $7,749 | Higher earners see benefit growth cap |

| SSI maximum (single) | $943 | $994 | Low-income recipients get modest increase |

| Earnings test limit (under FRA) | $21,240 | $22,320 | You can earn more before benefits are withheld |

Source: SSA.gov 2026 Press Release

The Trust Fund Question — Is Social Security Going Bankrupt?

This is the #1 fear among pre-retirees under 55 — and the answer is more nuanced than headlines suggest.

- The SSA trustees project the Old-Age and Survivors Insurance (OASI) trust fund could be depleted around 2033–2035 without legislative action

- If that happens, Social Security would not disappear — ongoing payroll taxes would still fund approximately 77–80% of scheduled benefits

- Congress has modified Social Security every time a funding crisis approached (1983 being the most significant reform)

Michael R. Thompson, CFA, notes: “The trust fund situation is a real policy issue — but claiming Social Security early out of fear is almost never the right financial decision. The break-even math still favors delay for most healthy Americans.”

For broader retirement planning context, read our guide on Retirement Savings by Age and Retirement Planning in Your 30s.

What This Means For You — Action Steps

- ✅ Log into SSA.gov My Social Security and verify your earnings record for errors

- ✅ Run all three claiming-age scenarios (62, FRA, 70) in the calculator above with your actual PIA

- ✅ Calculate your break-even age — it’s the most important number in your claiming decision

- ✅ Factor COLA compounding into your lifetime projections — the tool does this automatically

- ✅ Coordinate with your spouse before either of you files — household lifetime value depends on both decisions together

Social Security Calculator — Most Asked Questions (2026)

1. What is a Social Security calculator?

A Social Security calculator estimates your monthly retirement benefit using your PIA, your FRA, and your chosen claiming age. Our tool also models lifetime totals, break-even ages, and inflation-adjusted values.

2. How much Social Security will I get at age 62?

Benefits claimed at 62 are permanently reduced by 25–30% compared to your FRA benefit. On a $2,000 PIA, that means approximately $1,400/month instead of $2,000.

3. What is the maximum Social Security benefit in 2026?

$5,251 per month — available only to workers who earned at or above the wage base ($184,500) for 35+ years and delayed claiming until age 70.

4. What is Full Retirement Age in 2026?

Age 67 for anyone born in 1960 or later. For those born between 1955–1959, FRA ranges from 66 years and 2 months to 66 years and 10 months. See the full FRA chart at SSA.gov.

5. What is PIA in Social Security?

PIA (Primary Insurance Amount) is the exact monthly benefit you receive if you claim at your Full Retirement Age — neither early nor late. It’s the baseline from which all adjustments are calculated.

6. What is the break-even age for Social Security?

Typically age 78–79 when comparing early (62) vs FRA claiming, and age 82–83 when comparing FRA vs delayed (70) claiming. Our calculator shows your exact break-even based on your PIA and life expectancy assumption.

7. Can I work and collect Social Security at the same time?

Yes. If you’re under FRA, benefits are temporarily reduced if earnings exceed $22,320 in 2026. After you reach FRA, there is no earnings limit — you collect your full benefit regardless of income.

8. How is Social Security taxed in 2026?

Up to 85% of your Social Security benefit can be subject to federal income tax. This depends on your combined income. Single filers above $34,000 and joint filers above $44,000 in combined income reach the 85% taxable threshold. See our full 2026 Income Tax guide for details.

9. What is the 2026 Social Security COLA?

2.8%, applied automatically to all benefits beginning January 2026. This is determined by the change in the Consumer Price Index for Urban Wage Earners (CPI-W) from Q3 2024 to Q3 2025.

10. How do I find my official Social Security benefit estimate?

Create or log into your free My Social Security account at ssa.gov/myaccount. Your statement shows your projected benefit at 62, FRA, and 70 based on your actual earnings record.

11. Should I claim Social Security early because of trust fund concerns?

Most financial experts say no. The break-even math still strongly favors delay for healthy Americans. Even in a worst-case scenario, Social Security would pay approximately 77–80% of scheduled benefits — not zero. Fear-based early claiming typically costs far more than it protects.

Expert Panel: This article was reviewed by Laura M. Bennett, CFP (claiming strategy and spousal coordination), Daniel Moreau, CPA/CFP (tax strategy on Social Security benefits), and Michael R. Thompson, CFA (lifetime value optimization and present value analysis).

⚠️ Disclaimer: This article and the Social Security calculator above are for educational and informational purposes only. They do not constitute financial, tax, or legal advice. Benefit estimates are approximations based on published SSA formulas and may differ from your official SSA calculation. Always verify your benefits directly at ssa.gov and consult a licensed financial advisor before making retirement or claiming decisions.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.