Structured Settlement Taxes and IRS Filing Rules

Structured settlement taxes under IRC §104 can stay excluded, but one Form 1099 mistake may trigger IRS correspondence and amended returns.

In This Article

Why your settlement may be tax-free — or not entirely

You received structured settlement payments this year. Your attorney said the money is tax-free. Your tax software flagged an amount as income. Now you are not sure what — if anything — belongs on your return.

That confusion traces to one fact most articles skip: not all structured settlement income receives identical treatment under federal tax law.

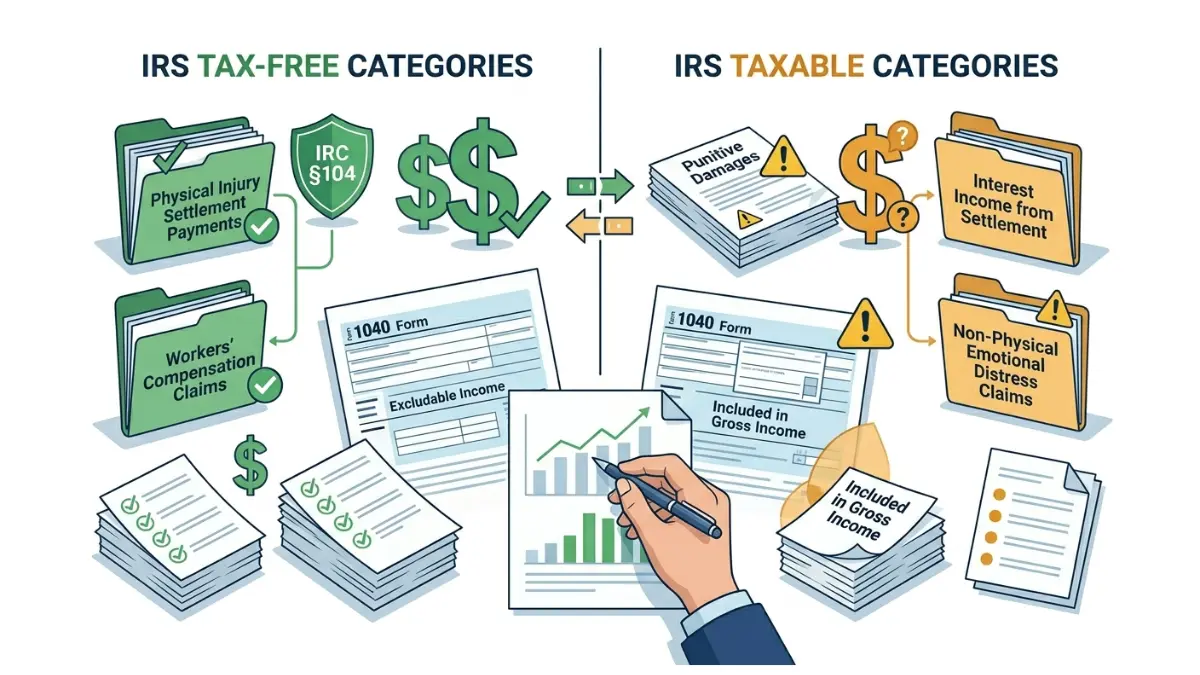

Payments from personal physical injury or sickness claims are excluded from federal gross income under Internal Revenue Code §104. For most recipients, that means no federal income tax owed and nothing entered on Form 1040 — whether the settlement paid as a lump sum or in monthly installments.

Three scenarios override that outcome: punitive damages included in your award, interest that has accrued on your settlement amount, and lump-sum proceeds from selling your payment rights to a factoring company.

This guide applies 2026 IRS rules to each scenario in plain terms. Use the budget calculator to map your after-tax settlement income against monthly expenses once your filing position is confirmed.

Are structured settlement payments taxable income?

Under IRC Section 104(a)(2), structured settlement payments from personal physical injury or physical sickness are excluded from federal gross income. Recipients owe no federal income tax on these payments in 2026 — whether received as a lump sum or in periodic installments.

Why origin of the claim determines the tax outcome

The IRS applies the “origin of the claim” standard: what the payment compensates determines taxability — not what the settlement agreement calls it. A $250,000 award labeled “pain and suffering” receives the same exclusion as one labeled “compensatory damages,” provided both trace to a qualifying physical injury or illness.

📊 Data Point: IRS Publication 4345 (2026) confirms that personal physical injury and physical sickness settlement proceeds qualify for the full gross income exclusion under IRC §104(a)(2). Workers’ compensation proceeds are excluded under the parallel provision at §104(a)(1). Source: IRS Publication 4345 on settlement taxability, January 2026.

Three types of settlement income that remain taxable in 2026

Punitive damages are always taxable as ordinary income — even in a physical injury case. Emotional distress payments not caused by physical injury, and interest accrued on any settlement amount, also fall outside §104 protection. For a full breakdown of settlement payment categories and how each is structured, see the structured settlement complete overview.

How to report a structured settlement on your 2026 tax return

Filing correctly starts with identifying which payment types — if any — belong on your return at all.

Step-by-step: when your settlement payments are fully tax-exempt

- Review your settlement agreement for written allocations between compensatory damages, punitive damages, and interest. No written allocation in the agreement? Stop and consult a CPA before proceeding.

- Confirm your IRC §104 eligibility. Use the IRS self-service tool for physical injury settlement income to verify that your specific claim type qualifies for exclusion.

- If fully excluded: Enter nothing on Form 1040. Retain your original settlement agreement in your tax file as exclusion documentation.

- If taxable components exist: Report them on Schedule 1 (Form 1040), Line 8z — “Other Income” for the 2026 tax year. Use the income tax calculator to estimate your liability before you file.

What to do if you receive a Form 1099-MISC for excluded income

💡 Expert Note (CFA): The costliest structured settlement filing error I encounter is a preparer entering excluded physical injury income on Schedule 1 after receiving a Form 1099-MISC — producing a tax bill that requires Form 1040-X and months of IRS correspondence to correct. Document your IRC §104 exclusion claim in writing before any number goes on the return. Leading tax software programs, including TurboTax and H&R Block, route you to the excluded-income pathway automatically when you select “physical injury settlement” as the income type.

Do not ignore a Form 1099-MISC you believe covers excluded settlement income. Document the exclusion, retain your settlement agreement, and review what each Form 1099 type triggers to understand your response options if an IRS notice follows.

Where taxable settlement components land on Schedule 1

Punitive damages and other taxable settlement income are reported on Schedule 1 (Form 1040), Line 8z for 2026. If this increases your adjusted gross income, see how AGI is calculated on Form 1040 for the downstream effects on deductions and credits.

Taxable vs. tax-free: classifying every type of structured settlement income

Which types of structured settlement payments are taxable? The table below provides the complete 2026 IRS classification for every major settlement payment category, sourced to IRS Publications 4345 and 525.

| Settlement Type | IRS Treatment (2026) | IRC Section | Report on Form 1040? |

|---|---|---|---|

| Physical injury / sickness damages | Excluded | §104(a)(2) | Not reported |

| Workers’ compensation | Excluded | §104(a)(1) | Not reported |

| Punitive damages (any case type) | Taxable | — | Schedule 1, Line 8z |

| Emotional distress — physical injury origin | Excluded | §104(a)(2) | Not reported |

| Emotional distress — no physical injury | Taxable | — | Schedule 1, Line 8z |

| Interest on settlement amount | Taxable | — | Schedule B or Line 2b |

| Employment discrimination award | Taxable | — | Schedule 1, Line 8z |

Sources: IRS Publication 4345; IRS Publication 525 (2026)

The §104 exclusion applied: physical injury and workers’ comp

The §104(a)(2) exclusion covers the compensatory portion of a physical injury award — regardless of how individual payment amounts are labeled in the settlement agreement. For the workers’ compensation application of this doctrine, see the workers’ comp structured settlement guide.

📊 Data Point: IRS Publication 525 (2026) explicitly classifies punitive damages and interest on settlement amounts as taxable ordinary income — even in cases where the compensatory portion is fully excluded under IRC §104(a)(2). Source: IRS guidance on taxable and nontaxable income categories, January 2026.

Mixed settlements: allocating between taxable and excluded amounts

When a settlement covers both physical injury damages and punitive damages, only a written payment allocation in the settlement agreement determines the correctly reportable amount. Without that written breakdown, the IRS applies a case-by-case analysis — and the tax outcome is not predictable without professional guidance. Use the 2026 income tax brackets to estimate your rate on any taxable portion, and the take-home pay calculator to model the net effect on your after-tax income.

Tax consequences of selling your structured settlement

Selling structured settlement payment rights to a factoring company creates a separate tax question that the §104 exclusion does not answer — and that most online guides ignore entirely.

How the IRS treats factoring transaction proceeds

When you sell your settlement rights, the lump-sum proceeds may be taxable depending on your cost basis in the original payments and whether the underlying claim was itself excludable under IRC §104. Cost basis, the applicable discount rate, and the nature of the original claim all factor into the analysis. See the guide to selling structured settlement payments for a full explanation of how discount rates affect your actual net proceeds.

⚠️ Warning: As of 2026, the IRS has not issued a uniform ruling covering all structured settlement factoring transactions. Tax treatment is determined case by case. Consult a licensed CPA or enrolled agent before filing any return that includes proceeds from a settlement rights transfer. The CFPB’s consumer overview of structured settlements also explains the court-approval requirements most states impose before a factoring transaction closes.

Estimating the taxable gain

Use the capital gains tax calculator to model a potential taxable gain once your cost basis is established with a CPA. Use the inflation calculator to see how inflation has eroded the real purchasing power of deferred payments — a figure that often surprises sellers when they compare nominal proceeds to actual buying power at the time of sale.

Common filing mistakes that create IRS problems with settlement income

Three structured settlement filing errors generate the most IRS problems — and the most expensive one is the opposite of what most people expect.

Entering excluded income as taxable: the most common costly error

Most guides warn about under-reporting income. The more widespread and more damaging error is the reverse: entering excluded physical injury settlement proceeds on Schedule 1 after receiving a Form 1099-MISC — creating an inflated tax bill that requires Form 1040-X to reverse. Retain your settlement agreement and document your IRC §104 exclusion before any figure goes on the return.

Ignoring a Form 1099-MISC: why silence generates an IRS notice

The IRS matches every Form 1099 to your return through its automated CP2000 program. An unmatched 1099 for excluded settlement income will trigger a notice — and a potential balance-due assessment — even when no federal tax is actually owed on those payments. Respond to any CP2000 notice promptly with your §104 exclusion documentation and a copy of the original settlement agreement.

✅ Pro Tip: If you have already filed with a taxable-income error that overstated your income, file Form 1040-X to correct it. The IRS allows a refund claim on an amended return for up to three years from the original filing date — every day you wait reduces your window.

File with confidence: your 2026 structured settlement tax summary

For the majority of recipients, structured settlement payments from personal physical injury or sickness claims owe zero federal tax under IRC §104(a)(2). The correct tax return reflects that by simply not including those payments anywhere on Form 1040.

Three situations require additional analysis before you file: punitive damages in your award, interest accrued on your settlement, and proceeds from selling your payment rights to a factoring company. Each creates a reportable income event, and each belongs on Schedule 1, Line 8z.

If your settlement includes any of those components — or if your settlement agreement contains no written payment allocation — consult a licensed CPA or enrolled agent before submitting your 2026 return.

For recipients whose settlement proceeds are fully excluded and who want to put that tax-free income to work long term, the savings calculator can model how consistent contributions compound into a meaningful financial position over time.

Frequently asked questions about reporting structured settlement taxes

Here are answers to the 11 most common questions about how structured settlement payments are handled at tax time in 2026. Each answer draws on IRC §104, IRS Publication 4345, and current Form 1040 guidance — and identifies where professional consultation is required.

1. Are structured settlement payments taxable income?

Under IRC Section 104(a)(2), structured settlement payments from personal physical injury or physical sickness claims are excluded from federal gross income. Most 2026 recipients owe no federal income tax on these payments and report nothing on Form 1040. The exclusion applies to both lump-sum awards and periodic payment arrangements, regardless of the total settlement amount.

2. Do I need to report structured settlement payments on my 2026 tax return?

Most structured settlement recipients from physical injury or sickness claims do not enter payments on Form 1040, because those amounts are excluded from gross income under IRC §104. However, punitive damages, interest on settlement amounts, and emotional distress payments unconnected to physical injury must be reported. Review your settlement agreement carefully to identify every payment category before filing.

3. What IRS form do I use to report structured settlement income?

Fully excluded structured settlement proceeds from physical injury claims are not entered on any Form 1040 line. Taxable components — punitive damages, accrued interest, or emotional distress not arising from physical injury — are reported on Schedule 1 (Form 1040), Line 8z for the 2026 tax year. Major tax software programs route you to the correct line when you select the appropriate income type.

4. Are proceeds from selling a structured settlement taxable?

Lump-sum proceeds from selling structured settlement payment rights to a factoring company may be taxable depending on your cost basis in the original payments and the nature of your underlying claim. IRS guidance on factoring transactions is not uniform as of 2026. Consult a licensed CPA or enrolled agent for guidance specific to your settlement type and filing situation.

5. Are punitive damages from a structured settlement taxable?

Yes. Punitive damages are taxable as ordinary income in 2026 — even when awarded in a physical injury case. The IRC §104 exclusion applies only to compensatory damages. Punitive amounts are reported on Schedule 1, Line 8z at your applicable ordinary income rate. Consult a licensed CPA or enrolled agent for guidance specific to your settlement type and filing situation.

6. Do I get a Form 1099 for structured settlement payments?

Payers of structured settlement proceeds from physical injury claims are not required to issue a Form 1099-MISC under current IRS rules — but some issue one regardless. If you receive a 1099-MISC for what you believe is excluded income, document your IRC §104 exclusion claim in writing and retain a copy of your original settlement agreement as supporting documentation.

7. Are workers’ compensation structured settlement payments taxable in 2026?

Workers’ compensation structured settlement payments are excluded from federal gross income under IRC §104(a)(1) — a provision separate from but parallel to the personal injury exclusion at §104(a)(2). Both provisions provide a full federal gross income exclusion. This exclusion applies to both lump-sum and periodic workers’ comp settlements under 2026 IRS guidance.

8. What is IRC Section 104 and how does it apply to structured settlements?

IRC Section 104 is the federal statute that excludes certain damage payments from gross income. Section 104(a)(2) covers personal physical injury and sickness; Section 104(a)(1) covers workers’ compensation. The operative test is the “origin of the claim” — what the payment compensates determines excludability, not its label. Consult a licensed CPA or enrolled agent for guidance on your specific filing situation.

9. How do I report interest income from my structured settlement?

Interest earned on structured settlement amounts is taxable as ordinary income in 2026 — regardless of whether the underlying settlement is otherwise excluded under IRC §104. Report interest on Schedule B when total interest income exceeds $1,500, or on Form 1040, Line 2b for smaller amounts. Structured settlement interest is treated identically to bank account interest under IRS rules.

10. What should I do if I received a Form 1099-MISC for excluded settlement income?

Do not ignore a Form 1099-MISC even if your structured settlement proceeds are fully excluded. The IRS CP2000 automated matching program flags every unmatched 1099 and may generate a balance-due notice even when no tax is owed. Document your IRC §104 exclusion claim, retain your original settlement agreement, and consult a licensed CPA or enrolled agent for guidance specific to your filing situation.

11. Can I deduct attorney fees paid from my structured settlement proceeds?

Attorney fees from a structured settlement for physical injury are generally not deductible, because the underlying income is excluded from gross income — you cannot deduct an expense against income that was never taxed. For taxable components such as punitive damages, limited deductibility may apply under IRC §62. Consult a licensed CPA or enrolled agent for the correct treatment for your specific settlement type.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.