The Right Way to Calculate Structured Settlement Present Value

Structured settlement present value isn’t face value — a 2026 CFA calculation shows why $360,000 in payments may be worth just $124,200 to a buyer.

In This Article

Most structured settlement owners don’t know what their payments are really worth

A structured settlement paying $300,000 over 20 years might generate a buyout offer of $155,000. That gap is not an accident — it is the precise mathematical result of a discount rate applied to every future payment in your schedule.

Why the number on your settlement documents isn’t what you’ll actually receive

The total listed on your settlement agreement is face value — all future payments summed together without any adjustment for time or opportunity cost. A factoring company pricing those same payments applies a discount rate that reduces their present worth by 40% to 65%.

What this CFA analysis covers

With 28 years in capital markets, I have valued fixed income payment streams using the same present value methodology applied directly to structured settlement buyout analysis. This guide shows you how to calculate your settlement’s exact present value, evaluate any offer against 2026 market benchmarks, and understand the legal protections available before you sign anything.

For the complete mechanics of how these agreements are constructed from issuance to final payment, the structured settlement guide covering what these agreements pay and what they cost lays the full groundwork.

Face value vs. present value: why the gap can run into the tens of thousands

Face value and present value are not the same number — treating them as interchangeable is the most expensive misunderstanding a structured settlement holder can bring to any buyout negotiation.

What structured settlement face value actually means

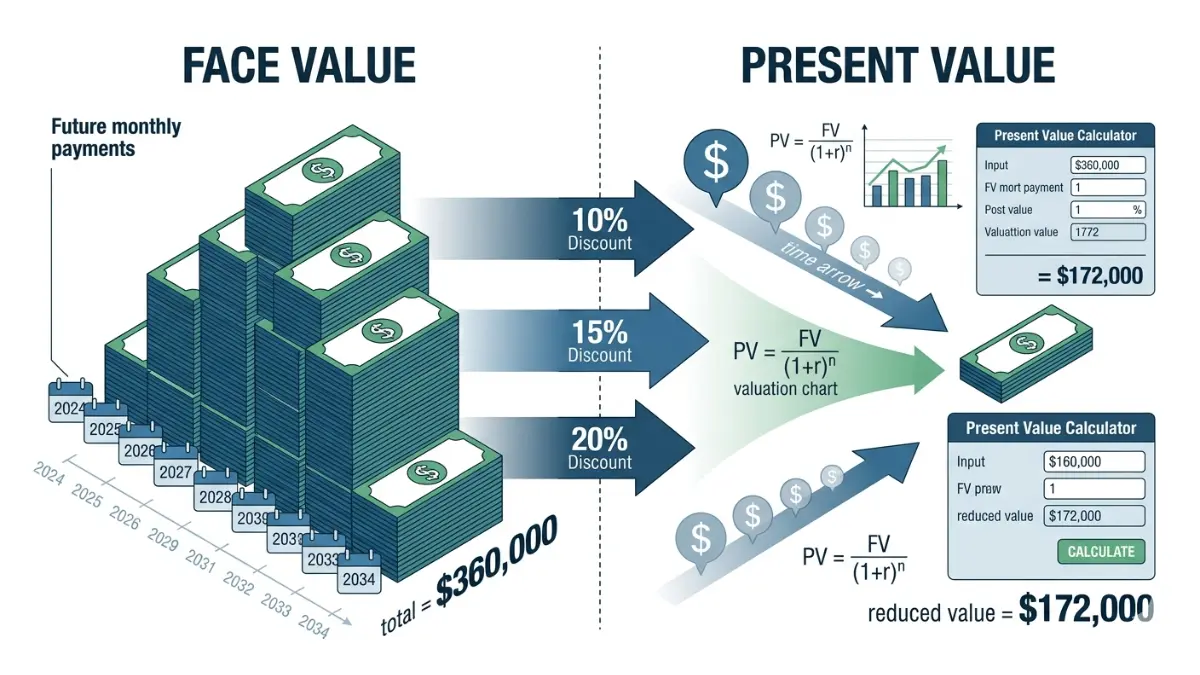

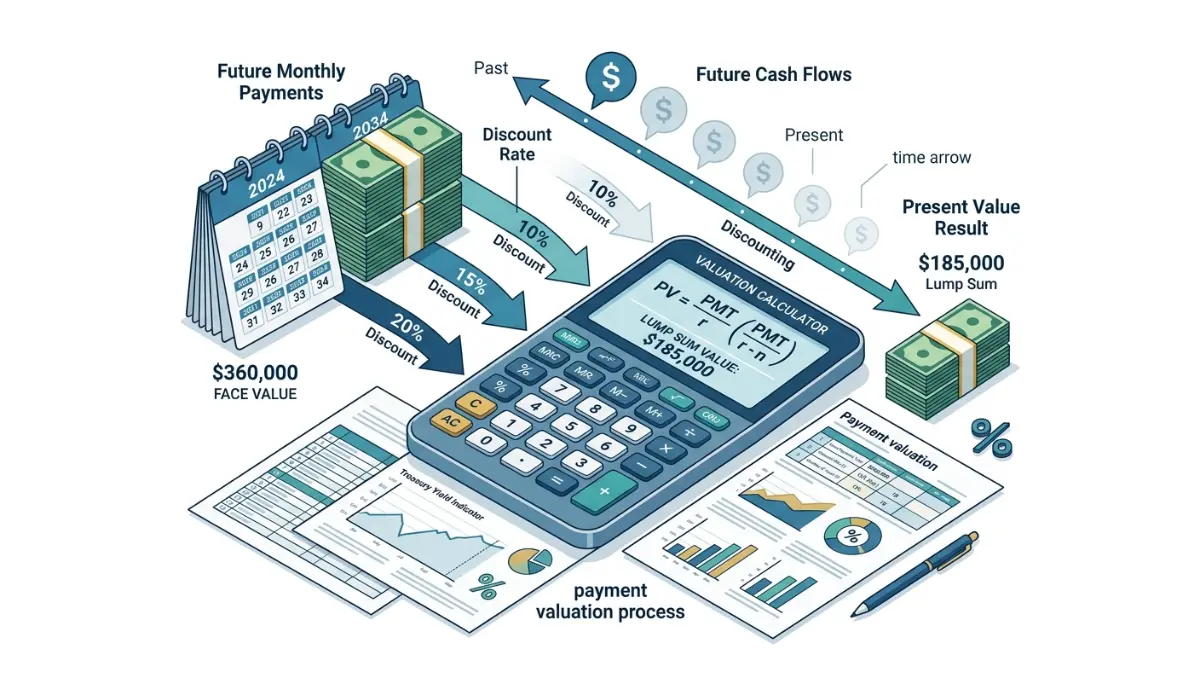

Face value is the undiscounted sum of all future scheduled payments. A settlement paying $2,000 per month for 15 years carries a face value of $360,000 — regardless of when those payments arrive.

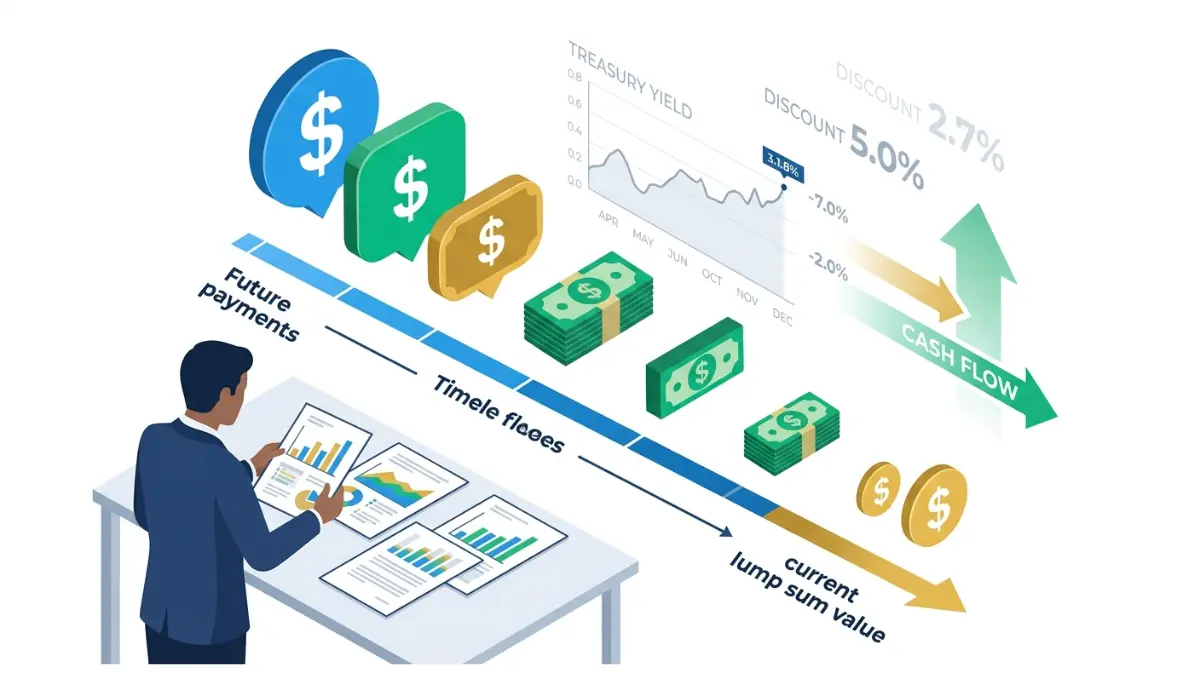

How present value discounts future payments back to today’s dollars

Present value is what that $360,000 payment stream is actually worth to a buyer today, after applying a rate that accounts for the cost of receiving money in the future rather than now. At a 12% annual discount rate — well within the 2026 market range for structured settlement transactions — that $360,000 face value carries a present value of approximately $172,000.

📊 Data Point: The Federal Reserve’s H.15 Selected Interest Rates release shows the 10-year Treasury yield at approximately 4.3%–4.6% as of Q2 2026. Factoring company discount rates reflect this risk-free Treasury baseline plus a spread for payment schedule length and buyer return requirements. — Source: Federal Reserve H.15 Selected Interest Rates, Q2 2026.

Why a $500,000 face value settlement can be worth far less right now

Each year separating today from a future payment compounds the discount — payments scheduled 15 or 20 years out contribute far less to present value than payments due in the next three years. A $500,000 face value settlement spread over 25 years at a 13% discount rate may carry a present value below $195,000 in 2026.

The payments in any structured settlement are backed by an annuity contract from a rated insurance carrier; our overview of how annuities are priced and structured explains the fixed income mechanics behind your payment stream. To see how inflation separately erodes the purchasing power of those future payments, the inflation calculator shows the combined long-term effect on delayed payment schedules.

| Face Value | Present Value | |

|---|---|---|

| Definition | Sum of all future payments, not discounted | Future payments discounted to current dollar value |

| 2026 Example ($2,000/mo × 180 months) | $360,000 | ~$172,000 at 12% discount rate |

| Who uses it | Settlement attorneys, tax authorities, courts | Factoring companies, CFAs, financial analysts |

| Key limitation | Ignores time value of money entirely | Changes with every discount rate assumption |

Source: Calculation based on Federal Reserve H.15 benchmark data, Q2 2026.

How to calculate structured settlement present value step by step

The formula behind every structured settlement buyout offer is straightforward — once you know it, no factoring company can obscure what your payments are actually worth.

The present value formula: what each variable means in a settlement context

The core equation is PV = FV ÷ (1 + r)^n, applied once to each payment in your schedule:

- PV — the present value of a single scheduled payment

- FV — the dollar amount of that future payment

- r — the periodic discount rate (annual rate divided by payment frequency)

- n — the number of periods between today and that specific payment

Apply the formula to every payment, then sum the results. The total is your settlement’s present value.

💡 Expert Note (CFA): I apply this same discounted cash flow framework when valuing corporate bond payment streams for institutional portfolios. The mechanics are identical to a structured settlement — the critical difference is that settlement payments are backed by a rated insurance carrier, not a corporation, making the discount rate itself the primary variable. When a factoring company applies an 18% discount rate to a payment stream guaranteed by an A-rated carrier, that 18% is their embedded profit margin, not a reflection of any real underlying payment risk.

A worked example: $2,000/month for 15 years at three real-world discount rates

The table below applies the formula to the same payment stream at three discount rates reflecting the actual 2026 market range for structured settlement buyout transactions.

| Discount Rate | Present Value | Face Value | Seller’s Haircut ($) | Haircut (%) |

|---|---|---|---|---|

| 9% (seller-favorable) | $197,200 | $360,000 | $162,800 | 45.2% |

| 13% (market median) | $158,000 | $360,000 | $202,000 | 56.1% |

| 18% (unfavorable) | $124,200 | $360,000 | $235,800 | 65.5% |

Source: Author calculations using Federal Reserve H.15 10-year Treasury benchmark, Q2 2026. Payment stream: $2,000/month for 180 months.

Every 1% increase in the discount rate on this stream reduces present value by approximately $6,200–$9,000. That reduction belongs to the factoring company — not to you.

Using the Federal Reserve’s H.15 data to anchor your discount rate

The Federal Reserve’s H.15 Selected Interest Rates release publishes current Treasury yields for maturities from 3 months to 30 years. Use the yield closest to your remaining payment schedule length as the risk-free baseline when assessing any discount rate a factoring company applies.

To model how a lump sum could grow if invested rather than spent, our compound interest calculator applies the same time-value mechanics to investment projections. For multi-scenario return modeling on different lump sum sizes, the investment calculator runs parallel assumptions in seconds.

Should you accept a structured settlement buyout? A CFA’s decision checklist

Calculating present value gives you the foundation — deciding whether to act on a buyout offer requires a framework that integrates the math with your specific financial reality.

Five questions to ask before accepting any buyout offer

Work through all five before responding to any factoring company:

- What is the implied discount rate? Solve PV = FV ÷ (1 + r)^n for r using the offer price and your payment schedule. A result above 15% means the transaction economics heavily favor the buyer.

- Is there a documented, genuine liquidity need? Accepting a buyout for convenience rather than necessity means paying 45%–65% of face value as the price of immediate cash access.

- Have you exhausted lower-cost financing? Personal loans, HELOCs, and other borrowing options are frequently available at rates well below the 9%–18% factoring company range.

- Have you obtained at least three competing offers? A 4-point discount rate difference between buyers on the same settlement can represent $25,000–$40,000 in lump sum value.

- Has an independent professional reviewed the offer? A CFA or CFP with no financial relationship to the factoring company is the only source of a genuinely unbiased implied rate calculation.

💡 Expert Note (CFA): In 28 years of capital markets work, I have reviewed structured settlement buyout offers with implied discount rates as high as 22%. At that level, the factoring company’s return exceeds the long-run U.S. equity market average — meaning the seller’s cost of accessing their own future payments is higher than borrowing from virtually any regulated financial institution. If your back-calculated implied rate exceeds 15% and any alternative financing exists, accepting that offer is almost never in your financial interest.

When keeping your structured settlement payments is the stronger financial choice

Retaining payments is the stronger choice when no genuine liquidity emergency exists, when the remaining payment term is long and predictable, and when the implied discount rate in any offer exceeds 14%. To model the long-term value of periodic payment income versus deploying a lump sum conservatively, our savings calculator shows what regular income contributions generate over time.

When a lump sum makes sense — and the threshold that separates the two

A buyout may be worth pursuing when the implied discount rate falls below 12%, a documented urgent need exists, and all alternative financing has genuinely been exhausted. For a full financial comparison of both payout structures across multiple income and investment scenarios, our analysis of structured settlement vs. lump sum outcomes walks through the numbers with 2026 market rate assumptions.

| Criterion | Favors Keeping Payments | Favors Accepting Buyout |

|---|---|---|

| Urgency of liquidity need | None or low | High and documented |

| Implied discount rate | Above 13% | Below 12% |

| Access to alternative financing | Available | Fully exhausted |

| Remaining payment term | 10+ years | Under 7 years |

| Health / life expectancy | Excellent | Meaningfully reduced (life-contingent payments only) |

What structured settlement factoring companies actually charge — and what they earn

The discount rate applied to your settlement is not a neutral market price — it is a profit structure built into a transaction where you are always the only seller.

The 2026 discount rate range: what factoring companies actually apply

Structured settlement factoring companies applied discount rates ranging from 9% to 18% in 2026, with the median transaction near 12%–14%.

📊 Data Point: FINRA has issued specific investor guidance warning that no federal cap on structured settlement discount rates exists and that state Structured Settlement Protection Acts represent the primary regulatory constraint on these transactions. — Source: FINRA Investor Alerts, 2026.

Four variables drive the rate applied to your settlement:

- Payment schedule length — longer terms increase discount rates because the buyer’s capital is committed for more years

- Annuity issuer credit quality — payments backed by lower-rated carriers attract higher discount rates

- Payment certainty — life-contingent payments are discounted more aggressively than fixed guaranteed-term payments

- Buyer competition — more competing buyers in a state directly compresses the rate any single buyer will accept

How a 4-point rate difference translates to real dollars on your settlement

On the $2,000/month for 15 years example from Section 3, the spread between a 9% and a 13% discount rate equals $39,200 in lump sum value. Every dollar of that difference belongs to the buyer.

For a deeper analysis of how structured settlement discount rates are set and why they vary so widely between buyers and states, our guide to structured settlement discount rates covers the full mechanics. To compare licensed buyers before committing to any offer, our review of the best structured settlement companies in 2026 evaluates the competitive landscape.

Why the first offer is rarely the best offer

No federal regulation caps structured settlement discount rates as of 2026, and the CFPB’s consumer guidance on structured settlement transfers specifically recommends obtaining multiple competing offers before accepting any buyout. On a mid-size settlement, three competing offers can generate $20,000–$50,000 in additional lump sum value before you sign a single document.

Your legal protections before any structured settlement transfer is final

Signing a transfer agreement with a factoring company is not the endpoint in this process — it is one of the first steps in a legally controlled sequence that exists specifically to protect sellers.

State Structured Settlement Protection Acts: what they require before you can sell

Every U.S. state has enacted a form of the Structured Settlement Protection Act, which mandates that a court independently determine whether a proposed transfer is in your best interest before it takes effect. Court review periods typically run 20–45 days, depending on the state.

Court approval and your right to independent counsel

The factoring company cannot receive your payments until a court approves the transfer — and most state acts explicitly give you the right to independent legal representation during that review.

⚠️ Warning: If a factoring company pressures you to sign documents quickly, skip required court filings, or rush past the approval period, stop the transaction immediately. That behavior violates state Structured Settlement Protection Act requirements and is a documented characteristic of predatory buyout transactions.

For the full step-by-step breakdown of what the court review process requires and how long it typically takes, our guide to the structured settlement court approval process covers each stage.

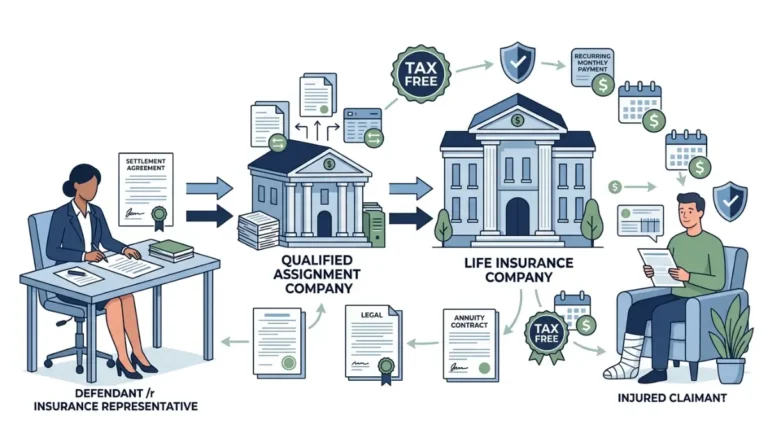

Tax treatment of structured settlement proceeds under federal law

Original periodic structured settlement payments are generally excluded from federal gross income under Internal Revenue Code Section 130, as confirmed by IRS Publication 4345. A lump sum received through a secondary-market transfer may carry different tax consequences — the outcome depends on individual circumstances and how the transaction is structured.

Our guide to structured settlement payment taxability covers the full federal and state-level tax framework, and the income tax calculator can help estimate potential tax exposure before you engage a CPA.

Know your present value before anyone makes you an offer

Every buyout offer is built on a discount rate someone else chose — for reasons that benefit them. The calculation in Section 3 of this guide gives you the tools to reverse-engineer that rate before any conversation with a factoring company begins.

If the implied rate falls below 12%, the offer may be worth pursuing with multiple competing bids in hand. If it exceeds 15%, the transaction economics strongly favor the buyer and alternative financing should be the first option exhausted.

The single most protective step any structured settlement holder can take is knowing their settlement’s present value before the first offer arrives. Request three competing bids, verify your state’s court approval requirements, and have an independent professional calculate the implied discount rate — before you respond to anything.

Structured settlement present value: frequently asked questions

These 11 questions reflect the most common issues structured settlement holders bring to me before any buyout decision. All 2026-specific rate figures are drawn from Federal Reserve and FINRA published data.

1. What is the present value of a structured settlement, and how does it differ from face value?

The present value of a structured settlement is the current dollar value of all future guaranteed payments, discounted back to today using an assumed rate of return. A settlement paying $2,000 per month for 15 years has a face value of $360,000 — but a present value of roughly $172,000–$197,000 at 2026 market discount rates of 9%–12%. Present value, not face value, is what drives any buyout offer.

2. How is structured settlement present value calculated step by step?

Structured settlement present value is calculated using PV = FV ÷ (1 + r)^n, applied to each scheduled payment separately. FV is the future payment amount, r is the periodic discount rate, and n is the number of periods until that payment arrives. Summing all discounted payments gives total present value. Standard financial calculator software or a spreadsheet can apply this methodology to any payment schedule.

3. What discount rate range do structured settlement companies typically use in 2026?

Structured settlement factoring companies applied discount rates ranging from 9% to 18% in 2026, with the median transaction near 12%–14%, per FINRA guidance. The rate applied to your settlement depends on payment schedule length, annuity issuer credit quality, and buyer competition in your state. Rates above 15% indicate the transaction economics favor the buyer significantly more than the seller.

4. Is it generally better to take a lump sum or keep your structured settlement payments?

Neither option is universally better — the right choice depends on your liquidity needs, the implied discount rate of the buyout offer, and your access to lower-cost financing alternatives. Retaining payments is generally more advantageous when no urgent financial crisis exists. Our comparison of structured settlement vs. lump sum financial outcomes models both structures using 2026 market rate assumptions.

5. How much of a structured settlement’s value do factoring companies typically retain as profit?

Structured settlement factoring companies typically retain 15%–35% of a settlement’s face value as embedded profit within the discount rate they apply. On a $360,000 face value settlement with a 15-year term, a company applying a 14% discount rate pays approximately $152,000 — generating a margin exceeding $100,000 on guaranteed future payments. Obtaining multiple competing offers directly compresses this margin before you commit to any buyer.

6. What is the exact difference between the face value and present value of a structured settlement?

Face value is the undiscounted total of all future payments — a settlement paying $2,000 per month for 15 years has a face value of $360,000. Present value discounts those same payments to their current dollar worth; at a 12% discount rate, that stream has a present value of approximately $172,000. The present value is always lower than face value — often by more than half on long-dated schedules.

7. Are lump sum proceeds from a structured settlement buyout considered taxable income?

Original structured settlement payments are generally excluded from federal gross income under Internal Revenue Code Section 130 when received periodically. A lump sum received through a secondary-market transfer may carry different tax treatment depending on how the transaction is structured and individual circumstances. The gap between periodic payment tax treatment and lump sum treatment can be significant and is determined on a case-by-case basis.

8. How do I know if the buyout offer I received for my structured settlement is fair?

Back-calculate the implied discount rate by solving PV = FV ÷ (1 + r)^n for r, using the offer price and your payment schedule. If the result falls between 9% and 13%, the offer is within the 2026 market range and worth evaluating with competing bids alongside it. If the implied rate exceeds 15%, the economics of that transaction heavily favor the buyer over the seller.

9. What discount rate range is generally considered fair for a structured settlement in 2026?

A discount rate between 9% and 13% is generally considered market-rate for structured settlement buyouts in 2026, benchmarked against the Federal Reserve’s current 10-year Treasury yield plus a spread for payment schedule risk. Rates above 14% begin to significantly favor the buyer. Rates above 15% represent a return premium for the buyer that meaningfully compresses the value delivered to the seller.

10. Is it possible to sell only a portion of my structured settlement payments rather than all of them?

Yes — structured settlement holders can sell a portion of their future payments while retaining the remainder, a transaction known as a partial transfer. A partial sale provides immediate liquidity without surrendering the full income stream. The same court approval requirements under your state’s Structured Settlement Protection Act apply to partial transfers as to full ones. Partial transfers can target specific upcoming payments or defined payment blocks.

11. What happens to remaining structured settlement payments if the original payee passes away?

The disposition of structured settlement payments after the original payee’s death depends entirely on the underlying annuity contract terms. Life-contingent payment structures terminate at death; guaranteed payment structures may continue to a named beneficiary or the estate. Review your specific settlement documents to confirm which structure applies before making any financial plan that depends on payments continuing beyond the original payee’s lifetime.

✅ Pro Tip: Before calculating your settlement’s present value, download the Federal Reserve’s most recent H.15 interest rate table and use the current 10-year Treasury yield as your discount rate baseline. It takes two minutes and gives your calculation the strongest possible 2026 market anchor before you evaluate any offer.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.