What Each Structured Settlement Payment Schedule Is Worth

Structured settlement payment schedule types differ by more than timing — at the May 2026 IRS rate of 5.00%, each carries a very different real value.

In This Article

What is a structured settlement payment schedule?

A structured settlement payment schedule is the legally binding timetable specifying when, how often, and in what amounts a plaintiff receives compensation from a settled legal claim.

Most plaintiffs receive an election form with five options and no explanation of what each type costs long-term — and the choice becomes permanent once the qualified assignment is executed.

Why the payment schedule matters more than the settlement total

The same $500,000 settlement as a pure life-contingent structure pays nothing to the estate if the recipient dies in year three; a period certain structure continues paying the full remaining term to beneficiaries regardless of death.

The schedule governs the actual financial outcome. Before comparing types, review how structured settlements work and what they pay from negotiation through final disbursement.

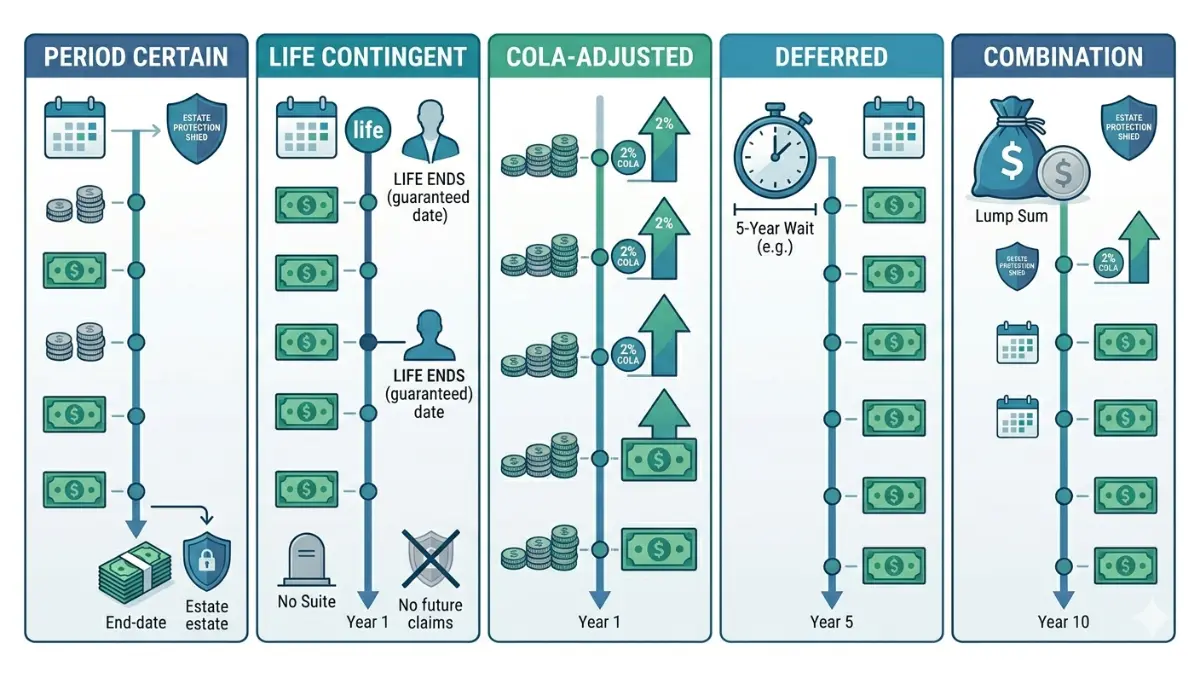

The 5 structured settlement payment schedule types at a glance

The five types — period certain, life contingent, COLA-adjusted, deferred, and combination — each carry different estate implications, tax treatment, and real lifetime value.

Use our savings calculator to model how different periodic payment amounts accumulate before selecting a structure.

ℹ️ Disclaimer: The structured settlement and annuity information in this article is intended for educational purposes only. Structured settlement payment schedules involve regulated financial instruments — including annuity contracts governed by state insurance law — with tax treatment under IRC Section 104(a)(2) that depends on the nature of the underlying legal claim. Consult a licensed tax professional or certified settlement planner (NSSTA member) before making any payment schedule election or entering into a structured settlement transfer agreement.

The 5 types of structured settlement payment schedules

The five main structured settlement payment schedule types are: (1) period certain, (2) life contingent, (3) COLA-adjusted, (4) deferred, and (5) combination — each recognized by the National Structured Settlements Trade Association (NSSTA) with distinct payout rules, estate coverage, and cost structures.

| Schedule Type | Ends at Death? | Estate Protected? | Inflation Adjusted? | Best For |

|---|---|---|---|---|

| Period Certain | No | Yes — full remaining term | No | Dependents, estate planning |

| Life Contingent | Yes | No | No | Healthy plaintiffs, no dependents |

| COLA-Adjusted | No | Yes | Yes (locked rider %) | Long-term medical cost coverage |

| Deferred | Depends on structure | Depends | No | Near-retirement income needs |

| Combination | Depends on structure | Partial | Partial | Complex income replacement |

Period certain vs. life contingent: what the difference actually costs you

A period certain payment guarantees the contracted term to the estate regardless of death. A life contingent payment terminates at the recipient’s death with zero residual value to beneficiaries.

For a 45-year-old plaintiff with dependents, the lifetime expected value of a pure life-contingent election can fall 30–40% below a period certain structure of identical nominal total. Use our compound interest calculator to model how COLA-adjusted payment escalations compound over a 20-year settlement term.

COLA-adjusted, deferred, and combination schedules

A COLA-adjusted schedule increases payments by a fixed annual percentage — typically 2–4%, locked at election — designed to offset consumer price increases over the settlement term.

📊 Data Point: Per the 2026 BLS Consumer Price Index, medical care price growth has been outpacing general CPI, meaning a 2% COLA rider may not fully protect purchasing power for settlements covering ongoing medical expenses over a 20+ year term. Verify the current medical CPI at BLS.gov. — Source: Bureau of Labor Statistics, May 2026.

Deferred schedules delay the first payment to a future date, serving plaintiffs who have sufficient current income. Combination structures blend a lump sum with periodic payments for complex income replacement scenarios that neither a pure lump sum nor a pure periodic structure addresses.

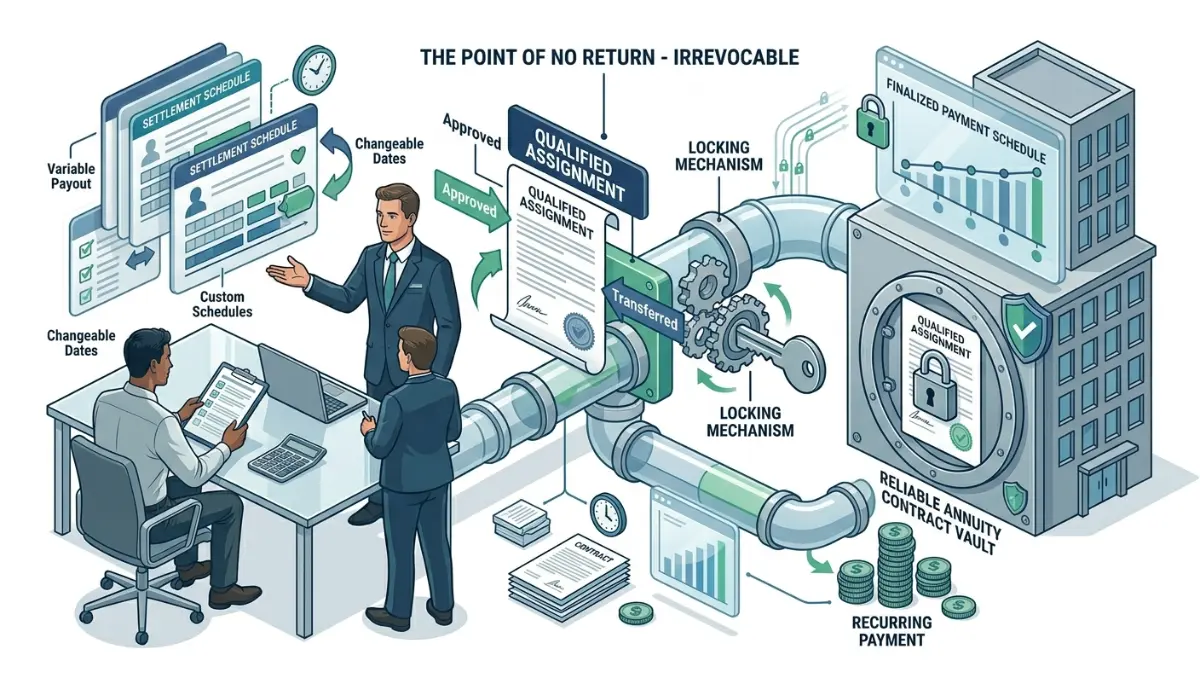

How a structured settlement payment schedule is established

A structured settlement payment schedule is established through five steps — and Step 2 is the only point where the plaintiff has direct control over the election type.

- Settlement negotiation — payment schedule structure is discussed alongside damages

- Schedule election — the plaintiff selects the payment type ← the decision window

- IRC Section 130 qualified assignment — obligation is transferred to an assignment company

- Annuity purchase by the assignee — an insurance carrier funds the payment stream

- First payment issuance — disbursements begin under the elected schedule

The negotiation window: when the schedule choice is made

Step 2 closes before Step 3. After the qualified assignment under IRC Section 130 is executed, the schedule is embedded in a life insurance annuity contract and cannot be changed by any party.

Refer to IRS Publication 4345 on settlements and taxability for the federal tax framework governing settlement payments and the qualified assignment process.

⚠️ Warning: Most plaintiffs do not realize the schedule election window closes before the annuity is purchased, not after. A change requested 90 days post-signing cannot be processed. The only protection is making the right election during Step 2 — before negotiations conclude.

Qualified assignment and why the election window closes permanently

The qualified assignment transfers the payment obligation from the defendant or liability insurer to an assignment company, which purchases a life insurance annuity to fund the payment stream. Once the annuity is in force, the schedule is contractually fixed inside an insurance product.

💡 Expert Note (CFA): In 28 years reviewing settlement agreements, the single most costly error I see is a plaintiff requesting a schedule change 60–90 days after signing. That window is permanently closed. Every structured settlement discussion should explicitly address the schedule election before the qualified assignment stage — not after.

Before the assignment closes, use our percentage calculator to convert the insurer’s stated discount rate into a specific dollar figure — making the real cost of each schedule type concrete and comparable before you commit.

Which structured settlement payment schedule fits your situation

No single structured settlement payment schedule type fits every plaintiff. The decision depends on three variables: dependent status, current age and health, and whether the settlement’s primary function is income replacement or capital provision.

Age, health, and dependents: why life contingent risk is different at 35 vs. 65

A 35-year-old with two dependents has a fundamentally different risk profile than a 67-year-old retiree in good health. Life-contingent payments for the younger plaintiff represent a substantial estate risk — family financial security terminates at the recipient’s death.

💡 Expert Note (CFA): In 28 years advising settlement clients, the most regret-generating choice I have observed is a 40-something plaintiff electing a pure life-contingent schedule without running a dependent impact analysis. The actuarial expected loss to the estate is real and consistently significant. Use our retirement calculator to model long-term income scenarios across different life-expectancy assumptions before finalizing any election.

Income replacement vs. long-term purchasing power goals

A plaintiff replacing lost wages should elect a structure that mirrors their former income pattern — typically period certain or COLA-adjusted. A plaintiff with no dependents may optimize for life-contingent or life-contingent-with-period-certain-guarantee, which delivers a higher periodic payment.

For plaintiffs over 62, settlement income interacts directly with retirement benefits. Use our Social Security calculator to model how the settlement payment stream coordinates with projected Social Security income. For COLA-adjusted schedule elections, use our inflation calculator to determine whether the locked COLA percentage adequately tracks 2026 medical cost trends through the full settlement term.

What each payment schedule type is actually worth in 2026

The same nominal payment stream produces dramatically different present values depending on the discount rate applied — and the rate an insurer uses is not always disclosed or explained to plaintiffs.

📊 Data Point: The IRS Section 7520 rate for May 2026 is 5.00% (IRS Rev. Rul. 2026-9). This is the government-published reference rate for determining the present value of annuity streams. The May 2026 mid-term applicable federal rate is 4.08% (annual compounding). Both rates are published monthly at the IRS applicable federal rates page. — Source: IRS, Revenue Ruling 2026-9, May 2026.

How the 2026 IRS Section 7520 rate affects your payment schedule’s real value

The applicable federal rate (AFR) is the IRS reference under IRC Section 1274; the Section 7520 rate is the specific government rate governing annuity valuations. The May 2026 Section 7520 rate is 5.00%.

Every percentage point above 5.00% that an insurer applies in their present value model reduces what a plaintiff’s payment stream is worth to them — and increases the insurer’s economic advantage.

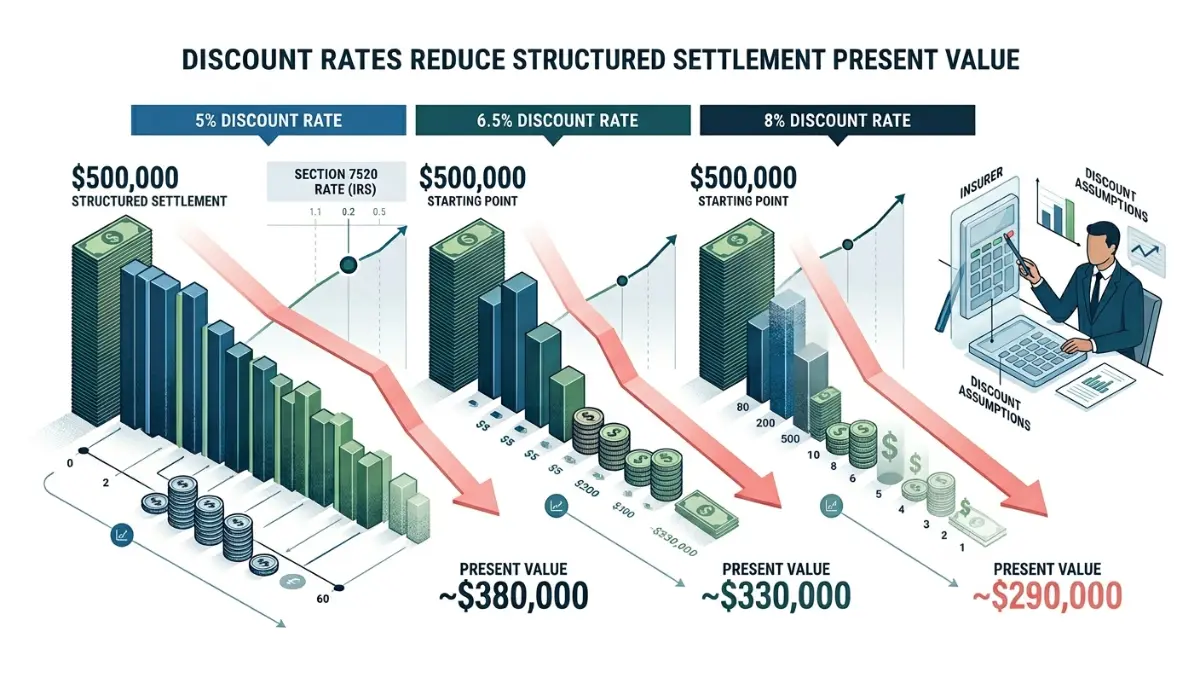

A $500,000 settlement compared at three discount rate scenarios

The table below models a $500,000 period certain schedule — 20 years at $25,000 per year — at the May 2026 IRS Section 7520 rate and two higher insurer scenarios. Use our investment calculator to model your settlement amount, and our ROI calculator to compare return profiles across all five schedule types.

| Discount Rate Applied | Present Value | vs. IRS 5.00% Baseline |

|---|---|---|

| 5.00% — IRS Section 7520 rate, May 2026 | $311,550 | Baseline |

| 6.50% — mid-range insurer assumption | $275,450 | −$36,100 |

| 8.00% — upper-range insurer assumption | $245,450 | −$66,100 |

Note: Calculations based on $25,000/year for 20 years using standard annuity present value formula. Source: IRS Rev. Rul. 2026-9 for the 5.00% baseline rate.

💡 Expert Note (CFA): A 3-percentage-point difference in the insurer’s discount rate assumption transfers $66,100 of present value from the plaintiff to the insurer on a $500,000 structured settlement. Plaintiffs almost never ask which rate was applied. Ask for it in writing during negotiations — it is a legitimate and consequential question.

Tax rules and legal protections for your payment schedule

IRC Section 104(a)(2) excludes from gross income any compensation received for physical injury or physical sickness — making most structured settlement payments income-tax-free when the underlying claim and assignment are properly structured.

IRC Section 104(a)(2): the physical injury requirement

The exclusion requires the underlying legal claim to be for physical injury or physical sickness. Emotional distress payments without an accompanying physical component do not qualify and may be subject to income tax.

📊 Data Point: The 26 USC Section 5891 excise tax imposes a 40% federal tax on structured settlement factoring transactions that do not comply with state Structured Settlement Protection Act (SSPA) court approval requirements. Every transfer of structured settlement payment rights without court authorization triggers this penalty. — Source: IRS, Internal Revenue Code Section 5891, 2026.

Before entering any transfer agreement, review what to know before giving up structured settlement payments with the CFPB’s consumer guide. For COLA-adjusted schedules, review current medical inflation data against your locked COLA rate.

💡 Expert Note (CFA): The IRC 104(a)(2) physical injury distinction is the most frequently misrepresented point in structured settlement discussions. If your settlement agreement characterizes damages primarily as emotional distress without an explicit physical component, the tax-free exclusion may not apply — and you could owe income tax on every payment received for the life of the schedule. Confirm the claim basis in writing with your attorney before signing.

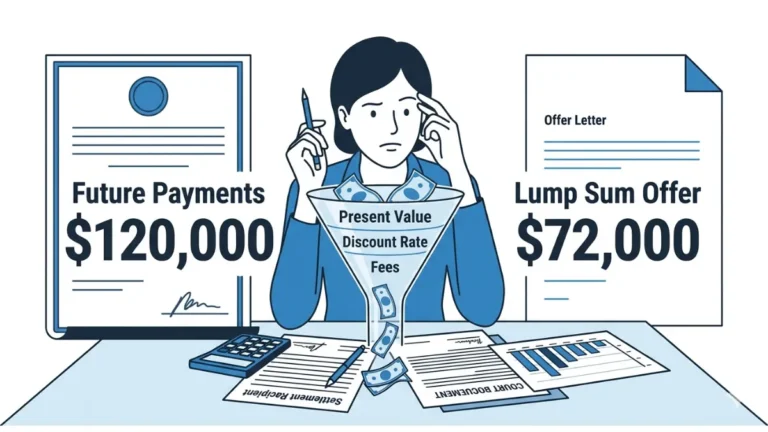

Selling future payments: court approval and the SSPA requirement

State Structured Settlement Protection Acts require court approval for every transfer of structured settlement payment rights. Courts evaluate whether the transaction is in the payee’s best interest — and regularly deny petitions that do not meet this standard.

Use our income tax calculator to model tax exposure on any settlement amounts that may not qualify for the IRC 104 exclusion. For life-contingent schedule analysis connected to annuity and insurance contract terms, our life insurance calculator provides supplementary projections.

Your structured settlement payment schedule action plan

Three questions determine whether a plaintiff finalizes the right structured settlement payment schedule or carries regret into a structure that cannot be changed:

- What happens to my payments if I die before the elected term ends?

- What discount rate is the insurer applying to the present value calculation?

- Has an independent settlement planner — not the insurer’s representative — reviewed this election?

The decision window is the only leverage point

The qualified assignment makes the schedule permanent. The only protection is acting at Step 2, before the annuity is purchased. Use our budget calculator to map how each payment schedule type fits into a long-term household income plan before the election is finalized.

When to contact a certified settlement planner

A certified settlement planner (NSSTA member) charges a flat fee or hourly rate — not a commission tied to the settlement amount. That fee structure distinguishes them from factoring company representatives, who profit from transferring payment rights.

Contact an NSSTA-certified settlement planner before the qualified assignment is executed, not after. The election discussion should happen during settlement negotiation while all schedule options are still available.

✅ Pro Tip: Ask the insurer for their discount rate assumption in writing during negotiations. On a $500,000 structured settlement, a 3-percentage-point difference in the applied discount rate shifts more than $66,000 of present value. This question costs nothing to ask and creates meaningful negotiating leverage.

Frequently asked questions: structured settlement schedules

1. What is a structured settlement payment schedule?

A structured settlement payment schedule is the legally binding timetable specifying when, how often, and in what amounts a plaintiff receives compensation from a settled legal claim. The five schedule types — period certain, life contingent, COLA-adjusted, deferred, and combination — each carry distinct estate implications, tax treatment, and total lifetime value.

2. What are the main types of structured settlement payment schedules?

The five main types are: (1) period certain — guaranteed payments for a fixed term to the estate; (2) life contingent — payments terminating at the recipient’s death; (3) COLA-adjusted — payments increasing by a locked annual percentage; (4) deferred — payments starting at a future date; and (5) combination — blending lump sum and periodic payments.

3. Are structured settlement payments taxable in 2026?

Under IRC Section 104(a)(2), structured settlement payments received for physical injury or physical sickness are excluded from gross income and received income-tax-free. Payments arising from emotional distress claims without an underlying physical component may not qualify for this exclusion and could be subject to income tax. Confirm the basis of your claim with a tax attorney.

4. Can you change your structured settlement payment schedule after signing?

In nearly all cases, no. After the IRC Section 130 qualified assignment is executed and the annuity is purchased, the structured settlement payment schedule is embedded in an insurance contract and cannot be modified. The election window closes at the qualified assignment stage — not after signing. Selling future payments with court approval is the only alternative.

5. What is a period certain structured settlement payment?

A period certain structured settlement guarantees payments for a specified number of years regardless of whether the recipient survives the full term. If the recipient dies before the term expires, payments continue to the designated beneficiary or estate. This payment schedule type protects dependents and preserves estate value absent from pure life-contingent structures.

6. What is a life contingent structured settlement payment?

A life contingent structured settlement payment schedule continues for as long as the recipient is alive and terminates completely at death. No payments pass to the estate or beneficiaries. This structure delivers the highest per-period payment amount but provides zero estate protection — a significant financial risk for any plaintiff with dependents.

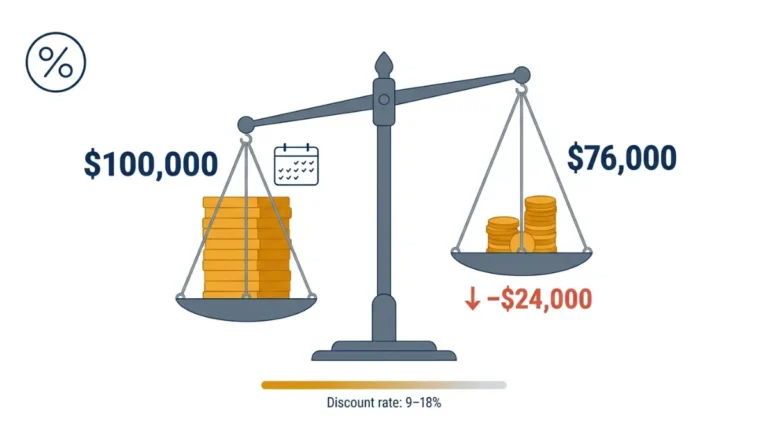

7. How much does it cost to sell structured settlement payments?

Factoring companies apply annual discount rates of 9–18%, reducing the lifetime value of a structured settlement payment schedule by 30–60% compared to holding payments to term. Separately, any transfer not approved by a court under state SSPA law triggers a 40% federal excise tax under 26 USC Section 5891. Evaluate these costs carefully before pursuing any sale.

8. What is the best structured settlement payment schedule?

No single structured settlement payment schedule type is universally best. Period certain suits plaintiffs with dependents. Life contingent suits healthy plaintiffs with no dependents who prioritize per-period payment size. COLA-adjusted suits long-term medical cost coverage. A certified settlement planner (NSSTA member) can model the optimal structure for a specific plaintiff’s financial profile.

9. What happens to structured settlement payments when you die?

The outcome depends entirely on the structured settlement payment schedule elected. Period certain payments continue to the estate or named beneficiary for the remaining guaranteed term. Pure life-contingent payments stop immediately at death with no residual value. A life-contingent-with-period-certain-guarantee hybrid continues until the guaranteed period expires, then terminates.

10. Can you sell your structured settlement payments?

Yes, but the process involves legal and financial costs. Selling structured settlement payment rights requires a court petition and approval under the applicable state Structured Settlement Protection Act, with the court finding the transaction to be in the payee’s best interest. Non-court-approved transfers trigger a 40% federal excise tax under 26 USC Section 5891.

11. How are structured settlement payment schedules negotiated?

Structured settlement payment schedule terms are negotiated during the settlement agreement phase, before the IRC Section 130 qualified assignment is executed. During this window, the plaintiff and their attorney can propose specific payment patterns, COLA rates, deferral periods, or combination structures. Once the qualified assignment is made, the schedule is final and cannot be renegotiated.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.