Life Insurance Calculator: Find Your Exact Coverage in 2026

Life Insurance Calculator

A needs-analysis calculator that estimates a coverage “gap” using DIME-style categories (Debt, Income, Mortgage, Education) plus optional items, then subtracts your current resources and coverage. DIME sums Debt + Income replacement + Mortgage + Education to estimate coverage needs. [web:300]

Inputs

Quick HLV-style view uses (retirement age − current age) × annual income. [web:304]

Income replacement is a common approach to estimate needs. [web:307]

Premium estimator (optional)

Results

Recommended starting point

—

Total needs: —

Total resources: —

Income replacement

Annual support need: —

PV of income stream: —

Real rate used: —

HLV quick view

Work years: —

HLV simple: —

Premium estimate (optional)

Annual: —

Monthly: —

Premium model details

Coverage used: — • Mode: —

Base (if simple mode): —

Multipliers: —

Needs breakdown (DIME-style)

| Category | Amount |

|---|

Step-by-step math

Quick check: Income multiples

| Multiple | Coverage amount | Monthly equivalent (coverage/12) |

|---|

Sensitivity (inflation/return)

| Inflation | Return | PV income | Total needs | Coverage gap |

|---|

Results appear after you click “Calculate.”

In This Article

A life insurance calculator gives you a precise coverage number based on your income, debts, mortgage, education costs, and existing assets. Most American families need between 10–15× their annual income in coverage. Use the free calculator above to get your number instantly, then read the expert breakdown below to understand exactly what drives it — and what your competitors’ calculators miss entirely.

How Our Life Insurance Calculator Works

What Inputs Does the Calculator Use?

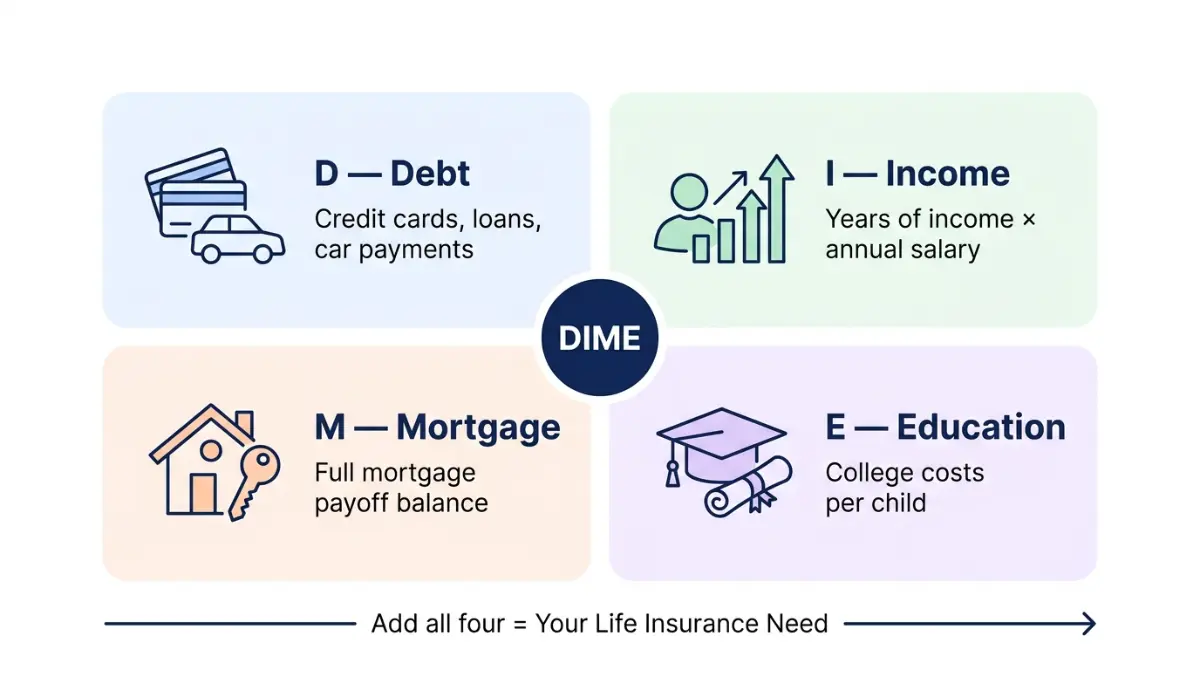

Our life insurance calculator uses the DIME method — the most comprehensive needs-analysis formula trusted by certified financial planners. DIME stands for Debt, Income, Mortgage, and Education.

The calculator takes these inputs:

- Annual income and the percentage you want to replace

- Mortgage balance — the full remaining payoff amount

- Non-mortgage debts — car loans, credit cards, student loans, personal loans

- Education fund — future college costs per child

- Final expenses — funeral and burial costs (national average: $8,300–$12,000 in 2026)

- Childcare or caregiver costs — often overlooked by every major competitor

- Existing resources — savings, investments, current life insurance, employer coverage

Once the calculator adds up your total needs and subtracts your existing resources, it delivers your net coverage gap — the exact amount of new life insurance you should consider buying.

How Is Your Coverage Gap Calculated?

The formula is straightforward:

Coverage Gap = Total Needs − Total Resources

Total needs include the present value (PV) of your income replacement stream, adjusted for inflation and expected investment returns. This is where most basic calculators fail — they use nominal income numbers without adjusting for the real cost of money over time.

Our calculator uses a real discount rate: (1 + return%) ÷ (1 + inflation%) − 1. At a 5% return and 3% inflation, your real rate is approximately 1.94% — meaning every dollar of coverage today goes further than a flat 10× income estimate suggests.

What Is the DIME Method?

The DIME method breaks your life insurance needs into four core categories: Debt and final expenses (all debts plus funeral costs), Income (annual income multiplied by years of support needed), Mortgage (full payoff balance), and Education (estimated college costs per child).

Add all four figures together to get your total needs baseline.

DIME vs. 10× Rule vs. HLV — Side-by-Side Comparison

| Method | Formula | Best For | Key Weakness |

|---|---|---|---|

| 10× Income Rule | Annual income × 10 | Quick ballpark | Ignores debts, assets, dependents |

| DIME Method | Debt + Income PV + Mortgage + Education | Most families | Doesn’t subtract existing coverage |

| HLV (Human Life Value) | (Retirement age − current age) × income | High-earners | Ignores liabilities |

| Our Calculator | DIME + all resources subtracted + PV-adjusted | Everyone | None — most complete |

Bottom line: The 10× rule is a starting point, not an answer. If you have a $300,000 mortgage, two kids heading to college, and $25,000 in credit card debt, the 10× rule leaves your family dangerously underinsured. Use the DIME-based life insurance calculator above instead.

If you’re also carrying significant debt, run your numbers through our debt-to-income ratio calculator to see how your debt load affects your overall financial picture before finalizing your coverage amount.

How Much Life Insurance Coverage Do You Actually Need in 2026?

The 4 Factors That Determine Your Coverage Amount

Every life insurance coverage calculation comes down to four variables:

- Income replacement years — How many years would your family need your income? Most planners recommend until your youngest child turns 18, or until a non-working spouse reaches retirement age.

- Total debt load — Your mortgage, car loans, student loans, and credit card balances all get passed as obligations to your estate if unpaid.

- Number of dependents — Each child adds education costs and income replacement years to your total need.

- Existing assets — Savings, investments, employer coverage, and existing policies all reduce your net gap.

2026 Coverage Benchmark Table by Life Stage

| Life Stage | Typical Coverage Need | Primary Driver |

|---|---|---|

| Single, no dependents | 1–3× income | Final expenses + personal debt |

| Married, no children | 5–7× income | Mortgage + income replacement |

| Young family (2+ kids) | 10–15× income | Full DIME calculation |

| Mid-career, teens at home | 8–12× income | Education fund + mortgage payoff |

| Pre-retirement (50s+) | 3–5× income | Final expenses + spouse support |

| Retirement age | 1–2× income | Burial costs + estate planning |

Real Example: Family of 4, Income $75,000

Here’s a full DIME calculation for a 38-year-old parent earning $75,000 per year, with two kids (ages 6 and 10):

| DIME Category | Amount |

|---|---|

| Debt (credit cards + car loan) | $28,000 |

| Income replacement (70% × $75K × 15 years, PV-adjusted) | $680,000 |

| Mortgage payoff | $310,000 |

| Education (2 kids × $100,000 estimate) | $200,000 |

| Final expenses | $12,000 |

| Total Needs | $1,230,000 |

| Less: savings + investments + existing coverage | −$230,000 |

| Net Coverage Gap | $1,000,000 |

That’s the number your family actually needs — not a vague “10× income” estimate of $750,000.

💡 What This Means For You: If you currently hold a $500,000 policy and earn $75,000 with two children and a mortgage, you are likely underinsured by $500,000 or more. Social Security survivor benefits can partially offset this gap — the SSA provides monthly payments to eligible family members of people who worked and paid Social Security taxes before they died — but these payments typically replace only 25–40% of lost household income.

What Competitors Get Wrong: Why the 10× Rule Fails

The “10 times income” guideline is commonly shared online, but it doesn’t take a detailed look at your family’s needs, nor does it consider your savings or existing life insurance policies. And it doesn’t provide a coverage amount for stay-at-home parents.

That’s why a life insurance calculator that uses real DIME methodology — not a single multiplier — gives your family the protection it actually needs.

Life Insurance Costs — What You’ll Actually Pay in 2026

2026 Average Term Life Insurance Premium Table

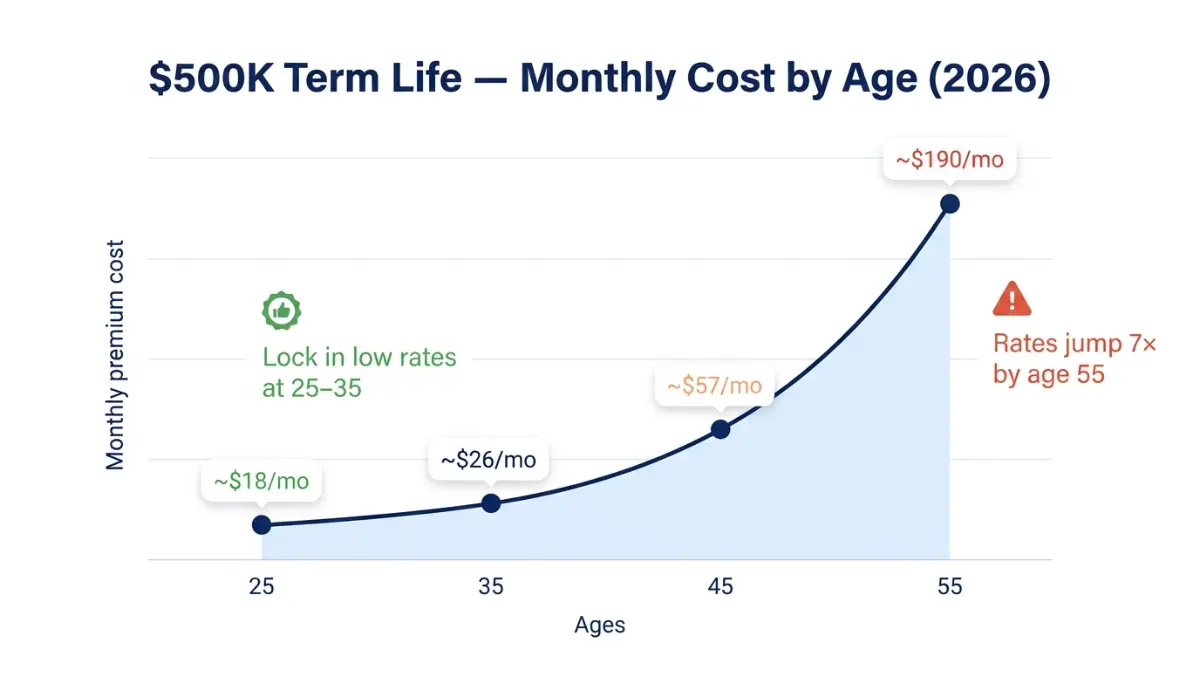

The average cost of life insurance is $26 a month, based on a healthy 40-year-old buying a 20-year, $500,000 term life policy. But your actual rate depends heavily on age, gender, health class, and smoking status. Here are 2026 benchmarks:

| Age | Gender | Health Class | $500K / 20-yr Term | $1M / 20-yr Term |

|---|---|---|---|---|

| 25 | Male | Excellent | ~$18/mo | ~$29/mo |

| 25 | Female | Excellent | ~$15/mo | ~$24/mo |

| 35 | Male | Excellent | ~$26/mo | ~$44/mo |

| 35 | Female | Excellent | ~$21/mo | ~$35/mo |

| 45 | Male | Excellent | ~$57/mo | ~$99/mo |

| 45 | Female | Excellent | ~$43/mo | ~$73/mo |

| 55 | Male | Average | ~$190/mo | ~$340/mo |

| 55 | Female | Average | ~$140/mo | ~$250/mo |

Key takeaway: A healthy 35-year-old can secure $1 million in 20-year term coverage for less than the average monthly cell phone bill.

How Smoking Adds Up to 70% to Your Premium

Smokers pay dramatically more for life insurance. Our calculator applies a 1.70× smoker multiplier — meaning a non-smoker paying $44/month for $1M in coverage would pay approximately $75/month as a smoker. Over a 20-year term, that’s nearly $7,500 in extra premiums.

Term Life vs. Whole Life Insurance Cost Comparison

| Policy Type | $500K Coverage | Duration | Cash Value |

|---|---|---|---|

| 20-yr Term | ~$26/mo (age 40) | 20 years only | None |

| Whole Life | ~$460/mo (age 40) | Lifetime | Yes, grows slowly |

| Universal Life | ~$200–$350/mo (age 40) | Lifetime (flexible) | Yes, market-linked |

For most American families, term life insurance is the right choice — it’s 10–20× cheaper than whole life and covers you through your highest-need years. Read our full term life insurance honest guide and whole life insurance truth guide to understand exactly which policy fits your situation.

If you’re planning around a mortgage purchase, pairing your life insurance coverage calculation with our mortgage calculator helps ensure your coverage amount matches your actual home loan obligations.

For consumer protections and insurer complaint records, the National Association of Insurance Commissioners (NAIC) maintains a free consumer information database where you can verify any insurer’s complaint ratio before buying.

7 Life Events That Mean You Need to Recalculate Your Life Insurance

Most people buy life insurance once and forget it. That’s a costly mistake. A life insurance calculator is a snapshot, not a permanent answer. These seven events should trigger an immediate recalculation:

1. New Baby or Adoption

Each new dependent adds years of income replacement and education costs to your total need. Action: Rerun the calculator adding $100,000–$200,000 per child for education and income support.

2. Home Purchase or Refinance

Your mortgage is often the single largest line item in any DIME calculation. When you buy or refinance, your balance changes — so should your coverage. Use our home affordability calculator when evaluating a new purchase to understand how your mortgage commitment affects your life insurance gap simultaneously.

3. Divorce or Remarriage

Divorce can create new obligations (alimony, child support) or remove them. Remarriage adds new dependents. Action: Recalculate DIME entirely and update your beneficiary designations immediately.

4. Major Income Change

A significant raise means your family has adapted to a higher standard of living — your coverage should match. A job loss may mean temporarily reducing premium costs by adjusting coverage. Action: Recalculate income replacement with your new salary figure.

5. Paying Off Major Debt

If you pay off your mortgage or eliminate significant debts, your coverage need drops. Action: Rerun the calculator — you may be able to reduce your policy size or redirect premium savings to your retirement calculator targets.

6. Children Reaching Adulthood

Once your youngest child turns 18 and becomes financially independent, your income replacement years drop sharply. Action: Reassess whether you still need the same coverage amount or can reduce to a final-expenses-only policy.

7. Approaching Retirement

By 60–65, most people have reduced debt, grown savings, and have fewer dependents. Action: Evaluate whether a smaller whole life policy for final expenses makes more sense than maintaining a large term policy.

Special Situations — Stay-At-Home Parents, Business Owners & Seniors

How to Calculate Coverage for a Stay-At-Home Parent

This is the gap every competitor either ignores or handles poorly. A stay-at-home parent provides services that would cost significantly to replace:

| Service | Annual Replacement Cost (2026) |

|---|---|

| Childcare (full-time, 2 children) | $16,000–$32,000/yr |

| Housekeeping (weekly) | $5,000–$8,000/yr |

| Meal preparation + grocery management | $3,000–$5,000/yr |

| Transportation/school runs | $2,000–$3,000/yr |

| Total annual replacement value | $26,000–$48,000/yr |

To use the DIME method for a stay-at-home parent, first add up how much it would cost each year to pay someone else to handle that parent’s tasks. Then plug that number into the formula as if it were the stay-at-home parent’s annual income.

Bottom line: A stay-at-home parent with two young children typically needs $400,000–$700,000 in life insurance coverage — not zero.

Does Employer Life Insurance Count?

Yes — but it’s rarely enough. Most employer group life plans provide 1–2× your annual salary. On a $70,000 income, that’s $70,000–$140,000 in coverage. Based on the DIME method, most families need 10–15× income. Your employer coverage fills roughly 10–15% of your actual need.

The IRS confirms that employer-provided coverage above $50,000 creates a taxable fringe benefit — another reason to understand exactly how much employer coverage you actually have.

Additionally, employer coverage ends if you change jobs. It is not portable. Always account for this in your own personal policy calculation.

Life Insurance for Seniors Over 60

As you approach retirement, your life insurance calculation shifts significantly:

- Income replacement need drops — You may be retiring soon, so years of replacement shrink

- Mortgage may be paid off — Reducing your largest DIME line item

- Final expenses remain — Funeral costs of $8,300–$12,000 still apply

- Estate planning goals may increase — Whole life can fund estate tax needs or leave a legacy

The CDC’s life expectancy data shows U.S. life expectancy at 75.8 years for men and 81.1 years for women — useful for calibrating how many years of coverage a senior actually needs.

For seniors considering a smaller whole life or final expense policy, also explore whether a Roth IRA or annuity strategy can supplement income needs in retirement rather than insurance.

Frequently Asked Questions about Life Insurance Calculator

1. What is a life insurance calculator?

A life insurance calculator is a free online tool that estimates how much coverage your family needs if you pass away. It factors in your income, debts, mortgage, education costs, and existing resources to calculate a coverage gap using methods like DIME or HLV.

2. How much life insurance do I need?

Most families need 10–15× their annual income. The exact amount depends on your mortgage balance, number of dependents, existing debts, education costs, and current savings. Use the DIME-based life insurance calculator above for a precise number rather than relying on the 10× rule alone.

3. Is $500,000 life insurance enough?

For a single person or a couple with no children and a modest mortgage, $500,000 may be sufficient. For a family of four with a $300,000+ mortgage and children under 12, $500,000 is likely not enough. Run your full DIME calculation to find out.

4. What is the DIME method for life insurance?

DIME stands for Debt, Income, Mortgage, and Education. You add up your total non-mortgage debts, multiply your income by years of support needed, add your mortgage payoff balance, and add estimated education costs per child. The total is your gross coverage need before subtracting existing assets.

5. How does age affect life insurance premiums?

Premiums increase with age because life expectancy decreases and health risks rise. A healthy 25-year-old pays roughly $15–$18/month for $500K in term coverage; a healthy 45-year-old pays $43–$57/month for the same coverage. Locking in a policy young saves tens of thousands over a 20-year term.

6. Can I use this calculator for both term and whole life insurance?

Yes. The calculator estimates your coverage need (the death benefit amount), which applies to any policy type. Use the premium estimator section to get a ballpark term life cost based on that coverage amount. For whole life, costs run 10–20× higher for the same death benefit.

7. What is HLV (Human Life Value) in the calculator?

Human Life Value (HLV) is a quick estimate calculated as: (retirement age − current age) × annual income. A 35-year-old earning $80,000 who plans to retire at 65 has an HLV of $2,400,000. It’s a ceiling estimate — the DIME gap method typically produces a more realistic, lower number.

8. Does the calculator include employer-provided life insurance?

Yes. Enter your employer coverage amount in the “Employer coverage” field. The calculator subtracts it from your total resources, reducing your net gap accordingly. Remember: employer coverage is not portable and typically covers only 10–15% of your actual DIME need.

9. How often should I recalculate my life insurance needs?

Review your coverage annually or after any major life event: new child, home purchase, divorce, remarriage, significant income change, or major debt payoff. Your coverage need in your 30s with young children looks very different from your need at 55 with a nearly paid-off mortgage.

10. Is life insurance coverage taxable?

Generally, no. Life insurance proceeds you receive as a beneficiary due to the death of the insured person aren’t includable in gross income and you don’t have to report them. However, any interest you receive is taxable. The IRS provides full guidance on this at irs.gov.

11. What’s the difference between a death benefit calculator and a premium calculator?

A death benefit calculator (like the coverage/needs section above) tells you how much coverage to buy. A premium calculator estimates what you’ll pay monthly for that coverage. Most competitors offer one or the other. Our calculator provides both in a single tool — a key advantage over NerdWallet, Bankrate, and Policygenius.

Related Tools & Resources

Planning your financial protection doesn’t stop at life insurance. Use these tools from financeauthorityhub.com to complete your financial picture:

- Retirement Calculator — Ensure your savings cover your retirement years alongside your insurance plan

- 401(k) Calculator — Maximize employer-matched retirement contributions

- Debt Consolidation Calculator — Reduce your DIME debt line item by consolidating high-interest balances

- Savings Calculator — Grow the “existing resources” side of your coverage gap equation

- Life Insurance Rates, Types & Guide — Full expert guide to choosing the right policy after using this calculator

⚠️ Disclaimer: This article and life insurance calculator are for educational and informational purposes only and do not constitute financial, insurance, legal, or tax advice. All coverage estimates are illustrative and based on general financial planning frameworks. Individual results will vary based on personal circumstances, health history, insurer underwriting, and state regulations. Please consult a licensed insurance professional, certified financial planner (CFP), or qualified financial advisor for advice tailored to your specific situation before purchasing any insurance product.

Reviewed by the financeauthorityhub.com Expert Panel | Last updated: March 2026 | Primary sources: SSA.gov Survivor Benefits, IRS Life Insurance & Disability Proceeds, CDC National Vital Statistics, NAIC Consumer Information

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.