What to Do When You Receive a Structured Settlement Offer

Received a structured settlement offer? A CFA explains the tax-free rules and the one move to make before you sign.

In This Article

What it means to receive a structured settlement offer

A number is now on the table, and you have to decide what to do with it.

When you receive a structured settlement offer, one of two situations is usually unfolding. Either an insurer is proposing to resolve your injury claim through payments spread over years, or a factoring company is offering cash today for periodic payments you already collect.

Both versions feel urgent. Both reward patience far more than speed.

In my 28 years advising clients, the conversations that end badly almost always share one trait. The person signed within days of the first call.

The good news is that you have more time, more leverage, and more legal protection than the offer letter suggests. A judge has to bless most of these deals, and the tax rules are friendlier than most people fear.

This guide gives you a neutral, step-by-step plan for responding — whether you are weighing a new lump sum versus payments, or deciding whether to cash out a settlement you already hold. Nobody here earns a cent based on which choice you make.

ℹ️ Disclaimer: This article covers investing, financial-planning, and tax matters related to structured settlements for educational purposes only. Tax treatment, discount rates, and court-approval rules vary by state, by the nature of your underlying claim, and by market conditions in 2026. Before accepting, keeping, or selling any structured settlement, consult a fiduciary financial advisor, a licensed tax professional (CPA or enrolled agent), and a licensed attorney in your state.

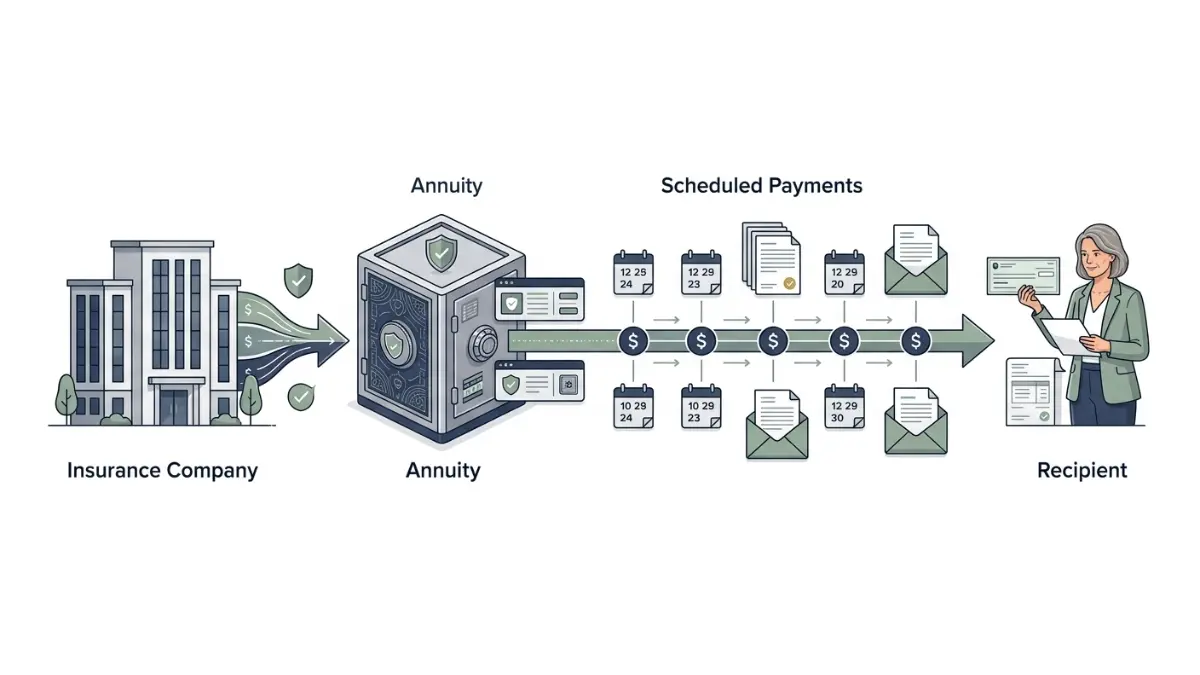

What a structured settlement offer really is

A structured settlement is a stream of guaranteed payments funded by an annuity an insurer buys to resolve a claim.

The single most reassuring fact comes first.

📊 Data Point: Damages received for personal physical injury or sickness are excluded from gross income under IRC Section 104(a)(2) — and that exclusion applies whether you take a lump sum or periodic payments. Source: Internal Revenue Service, Tax Implications of Settlements and Judgments (current as of 2026).

Is a structured settlement lump sum taxable?

A structured settlement lump sum for physical injury is generally tax-free, and converting future payments to a lump sum does not change that status.

The exclusion has limits worth knowing. Portions tied to punitive damages, lost wages in non-injury cases, or emotional distress without a physical cause can be taxable.

That distinction is where readers lose money. You can use an income tax estimator for any non-injury portion of an award to see what, if anything, is exposed.

The IRS lays out the full framework in its own guidance on how lawsuit and settlement money is taxed.

Annuity, payee, and present value — the words on your offer

You are the payee — the person entitled to receive the payments.

Behind the offer sits a qualified assignment and an annuity that funds each check. The number that matters most is present value: what your future payments are worth in today’s dollars.

Understanding how money grows or shrinks in value over time is the foundation for judging any offer you receive.

What to do when you receive a structured settlement offer

When you receive a structured settlement offer, work through these steps before you sign anything:

- Get the full offer in writing — request every term, the total payout, and the timeline on paper, not over the phone.

- Identify the offer type — confirm whether this resolves a claim or buys existing payments you already receive.

- Confirm the tax status — verify which portions fall under the injury exclusion and which do not.

- Benchmark the present value — calculate what your future payments are worth today before comparing any cash offer.

- Never accept on the first call — a same-day signature is the most expensive mistake in this market.

- Get independent professional advice — from an advisor with no financial stake in your decision.

- Collect competing offers — if you are selling, multiple quotes routinely change the number materially.

- Understand court approval — most sales require a judge to find the deal in your best interest.

- Check your rescission rights — many states give you a window to cancel after signing.

- Consult a fiduciary — before the final signature, not after.

✅ Pro Tip: Within 48 hours, ask the offering party for the discount rate and the total dollars you give up, in writing. A company that won’t put both on paper has told you something important.

The single most valuable habit here is documentation. Before signing any agreement, treat it the way you would a mortgage — read every line, and benchmark it against a payoff timeline for high-interest balances if debt is what’s driving the decision.

💡 Expert Note (CFA): In my experience, clients who insist on step five — never signing on the first call — keep an average of thousands of dollars more than those who feel rushed. The pressure to decide today is a sales tactic, not a deadline.

Lump sum or structured payments — how to decide

The right answer depends on your need, your time horizon, and your temperament — not on which number looks bigger.

Guaranteed periodic payments win when you value stability, face a long horizon, or worry about spending a large sum too quickly. A lump sum wins when you have a specific, documented need or a higher-return use for the money — and the discipline to follow through.

There is a hidden cost to fixed payments, though. Inflation quietly erodes them, and you can see what a fixed payment will actually buy years from now to weigh that against the certainty.

| Factor | Structured payments | Lump sum | Best for |

|---|---|---|---|

| Income certainty | High — guaranteed schedule | Depends on how you invest | Risk-averse recipients |

| Inflation risk | Higher on fixed amounts | Manageable if invested | Long horizons favor flexibility |

| Spending discipline | Built in | Requires self-control | Those wary of overspending |

| Liquidity for a real need | Limited | Immediate | Documented, urgent needs |

Illustrative framework, not a recommendation; outcomes vary by individual circumstances.

If you lean toward a lump sum, model it honestly. Run the numbers on what a lump sum could earn if invested, how guaranteed income fits a long-term retirement plan, and a fixed return on a certificate of deposit for a safe baseline.

A lump sum exchanged for an annuity is, in effect, the mirror image of buying one — the trade-offs that come with paying for guaranteed lifetime income apply in reverse.

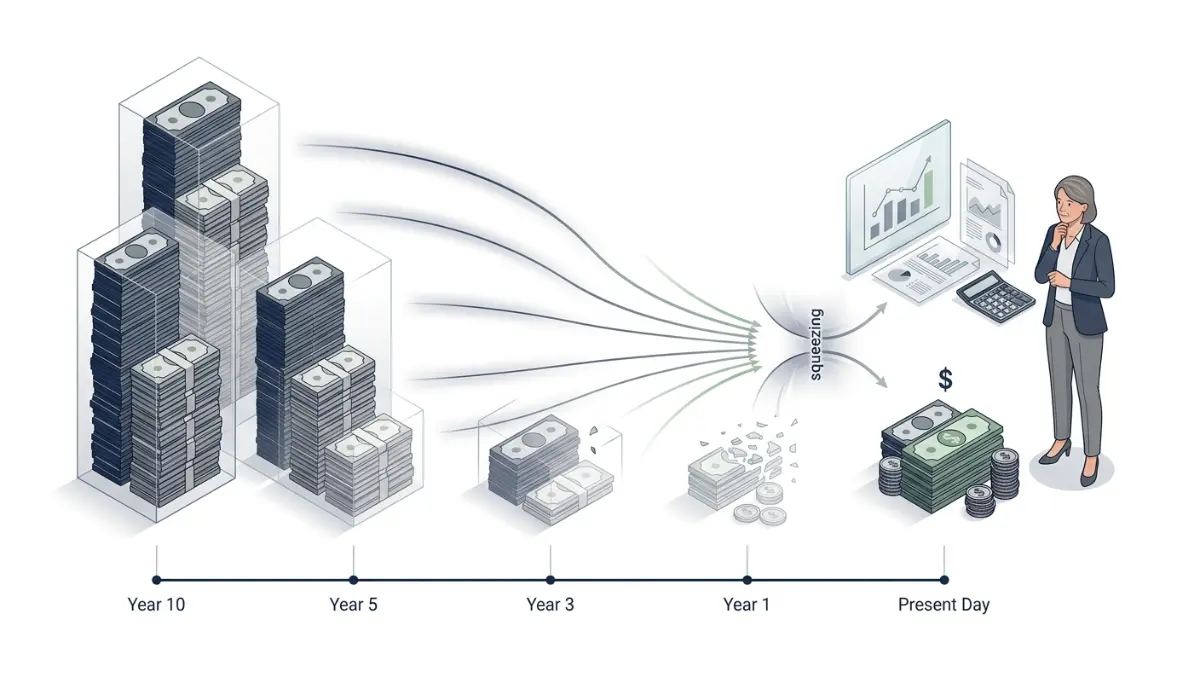

How much you really lose by selling future payments

Selling future payments always means accepting less than they are worth — and sometimes far less.

What a discount rate is — and what a fair one looks like

A discount rate is the percentage a buyer applies to shrink your future payments into a smaller lump sum today.

The higher the rate, the more of your money the buyer keeps. Secondary-market rates in 2026 commonly run in the low-to-mid double digits, though they vary widely by state and payment type — so treat any quote as a starting point and verify current rates directly with the buyer in writing.

A small change in that rate moves real dollars. Before you accept, compare the return on different uses of the money so you can see the trade clearly.

Red flags: how buyers underpay

The clearest warning comes from a federal case, not a hypothetical.

📊 Data Point: In the CFPB’s enforcement action against structured-settlement buyer Access Funding, the lump sums offered to consumers were roughly 30% of the present value of their future payments. Source: Consumer Financial Protection Bureau, Access Funding enforcement action (prior-year federal case, cited as documented precedent).

That is a 70% haircut on guaranteed money.

⚠️ Warning: A buyer who pressures you to sign quickly, steers you to “their” advisor, or refuses to disclose the discount rate in writing is showing you the deal’s true character. Walk away and get a competing quote.

If a genuine debt emergency is driving the sale, weigh alternatives first — sometimes consolidating high-interest balances instead preserves the income stream you would otherwise destroy. The CFPB documents how these deals harmed real families in its action against a buyer that underpaid sellers.

Your legal protections before you sign anything

You have more legal protection here than almost any other consumer financial decision — use it.

Why a judge must approve any sale

Court approval is mandatory: every U.S. sale of structured settlement payments must be approved by a judge under state and federal law.

State Structured Settlement Protection Acts add written disclosures, waiting periods, and the right to independent advice. The judge applies a best-interest standard, which means a rushed or lopsided deal can be — and is — rejected.

The 40% excise tax and the protections it backs

There is a powerful enforcement mechanism behind the court requirement.

📊 Data Point: A 40% excise tax applies to the factoring discount on any structured settlement transfer that is not approved in advance by a qualified court order, under IRC Section 5891. Source: Internal Revenue Service, About Form 8876 (current as of 2026).

That tax is precisely why no legitimate buyer will skip the courtroom.

💡 Expert Note (CFA): The best-interest hearing is your leverage, not your obstacle. Judges routinely ask why you need the money and whether you understand you’re receiving less than face value — so walk in with documented needs and a present-value figure of your own.

For high-stakes or irreversible terms, have a licensed attorney review the petition before the hearing. The full mechanics of the excise tax and the court-order exception are spelled out in the IRS’s rules on the tax that applies to non-approved sales.

Structured settlement offer FAQs

Quick answers to the questions readers ask most after an offer lands.

1. What does receiving a structured settlement offer mean?

When you receive a structured settlement offer, someone is either proposing to resolve your claim with payments over time, or offering cash now to buy payments you already receive. Both deserve scrutiny, written terms, and independent review before you respond, because the first number presented is rarely the best available.

2. Should I take a lump sum or structured payments?

Deciding between a lump sum or structured payments depends on your needs, time horizon, and discipline. Guaranteed payments protect against overspending and longevity risk, while a lump sum suits a documented need or higher-return use. There is no universal answer — only the answer that fits your actual financial situation and goals.

3. How much do I lose if I sell my structured settlement?

How much you lose selling a structured settlement depends on the discount rate applied. Buyers pay less than present value, and in one federal enforcement case lump sums were roughly 30% of true value. Competing quotes and a present-value benchmark are your best defense against an excessive loss.

4. Are structured settlement payments taxable?

Structured settlement payments for personal physical injury are generally tax-free under IRC Section 104(a)(2), and that status survives conversion to a lump sum. Exceptions exist for punitive damages, certain lost wages, and emotional distress without a physical cause, which can be taxable depending on how the settlement was structured.

5. Do I need a lawyer to respond to a structured settlement offer?

You are not always required to hire a lawyer to respond to a structured settlement offer, but for any sale you should. Court approval involves a best-interest hearing, and independent legal review protects you from one-sided terms. Many states require independent professional advice before a transfer can proceed.

6. How long does it take to sell a structured settlement?

Selling a structured settlement typically takes several weeks to a few months because court approval is required. The timeline includes written disclosures, a mandatory waiting period, a best-interest hearing, and funding after the judge signs. Timelines vary by state, so confirm your local waiting-period rules before counting on a date.

7. Can I sell only part of my structured settlement?

Yes, you can often sell only part of your structured settlement payments. A partial sale preserves future income, demonstrates financial responsibility to a judge, and frequently improves your odds of court approval. Selling only what you genuinely need is usually the more defensible and financially sound path forward.

8. What is a fair discount rate in 2026?

A fair discount rate in 2026 is the lowest one competing buyers will offer for your specific payment stream, since rates vary widely by state and term. Always request the rate in writing, gather multiple quotes, and judge offers by net dollars received rather than the rate alone.

9. Can I change my mind after accepting an offer?

You may be able to change your mind after accepting a structured settlement offer, because many states grant rescission rights for a set window after signing. Court approval also stands between signing and funding, giving you another chance to withdraw. Confirm your state’s specific cancellation rules immediately after signing anything.

10. What is the 40% excise tax on structured settlement sales?

The 40% excise tax on structured settlement sales applies to the factoring discount when a transfer is not approved in advance by a qualified court order, under IRC Section 5891. It effectively forces buyers through the courts, which is exactly why every legitimate transfer goes before a judge.

11. Who should I talk to before signing a structured settlement offer?

Before signing a structured settlement offer, talk to a fiduciary financial advisor, a licensed tax professional, and an attorney in your state. Each addresses a different risk — value, taxes, and legal terms. Independent advice with no stake in your decision is the strongest protection you have against a costly deal.

Your next move with the offer in hand

The offer is not a deadline — it is the opening of a process you control.

Before you sign, do two things. Benchmark what your payments are truly worth in today’s dollars, and speak with someone who earns nothing from your choice.

💡 Expert Note (CFA): The single piece of advice I give every client holding an offer is the same — slow down and get a second number. The cost of waiting a week is almost always smaller than the cost of signing too soon.

Once the money is settled, put a plan around it. A simple plan for the money once it arrives turns a one-time event into lasting stability.

You have the protections, the leverage, and now the plan. Use all three.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.