Inside a Personal Injury Structured Settlement Negotiation

Personal injury structured settlement talks involve five parties and one irreversible signature. Know who’s across the table before you negotiate.

In This Article

What to expect when your settlement talks turn to “structuring”

Your case is close to settling, your attorney mentioned “structuring” the money, and a negotiation is coming. This guide maps who sits across the table and what you can still change.

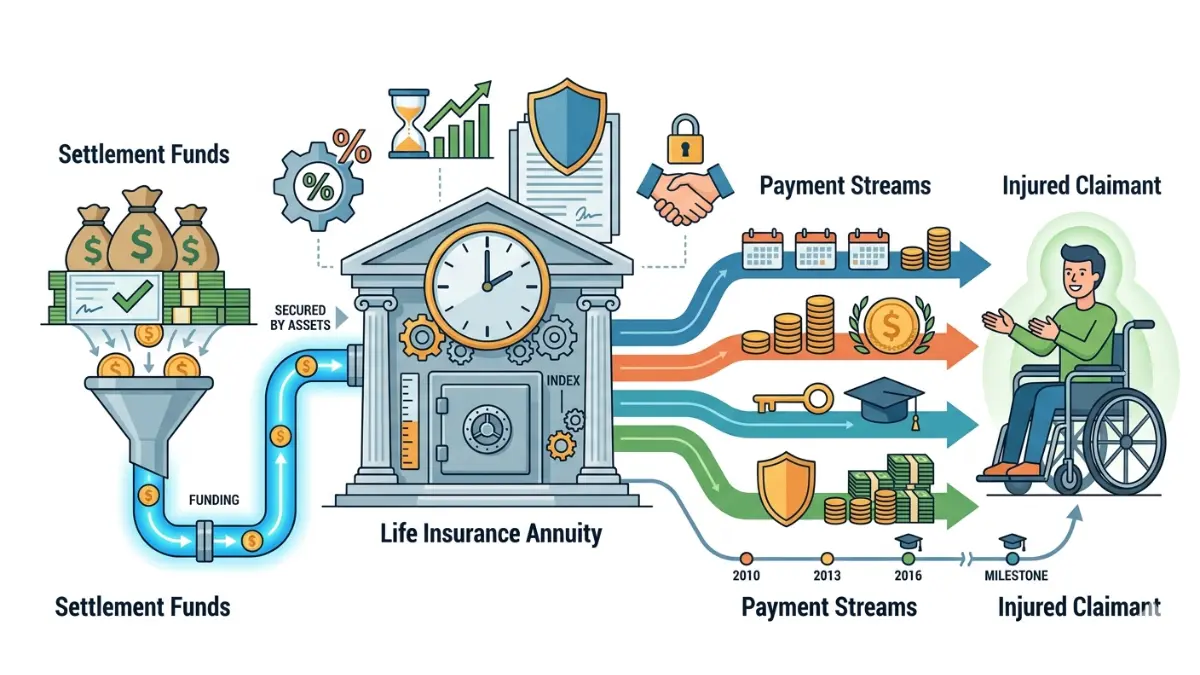

A personal injury structured settlement converts your award into a stream of periodic payments funded by an insurance annuity, instead of one lump check. The design of that stream is negotiable now — and effectively frozen the moment you sign.

That single fact is worth more than anything else here. Most people walk in not knowing it.

Finance Authority Hub does not buy, broker, or sell settlement payments, so the aim below is to close the information gap that insurers and brokers quietly rely on.

You will learn the tax-free mechanics, the five people in the room, the levers you can still pull, and the real cost of changing your mind later.

ℹ️ Disclaimer: This article covers personal injury structured settlements, which involve insurance annuities, federal and state tax law, and court-supervised legal agreements. Payout rates, tax treatment, and state Structured Settlement Protection Act rules vary by insurer, jurisdiction, and your individual circumstances in 2026. Consult a licensed attorney, a CPA, and a credentialed financial professional such as a CFP before accepting, designing, or selling any structured settlement.

What a personal injury structured settlement actually is

A personal injury structured settlement is a legal agreement that pays your compensation as scheduled payments over time, funded by a life insurance annuity, with those payments excluded from federal income tax under Internal Revenue Code Section 104(a)(2).

That tax treatment is the entire reason these exist.

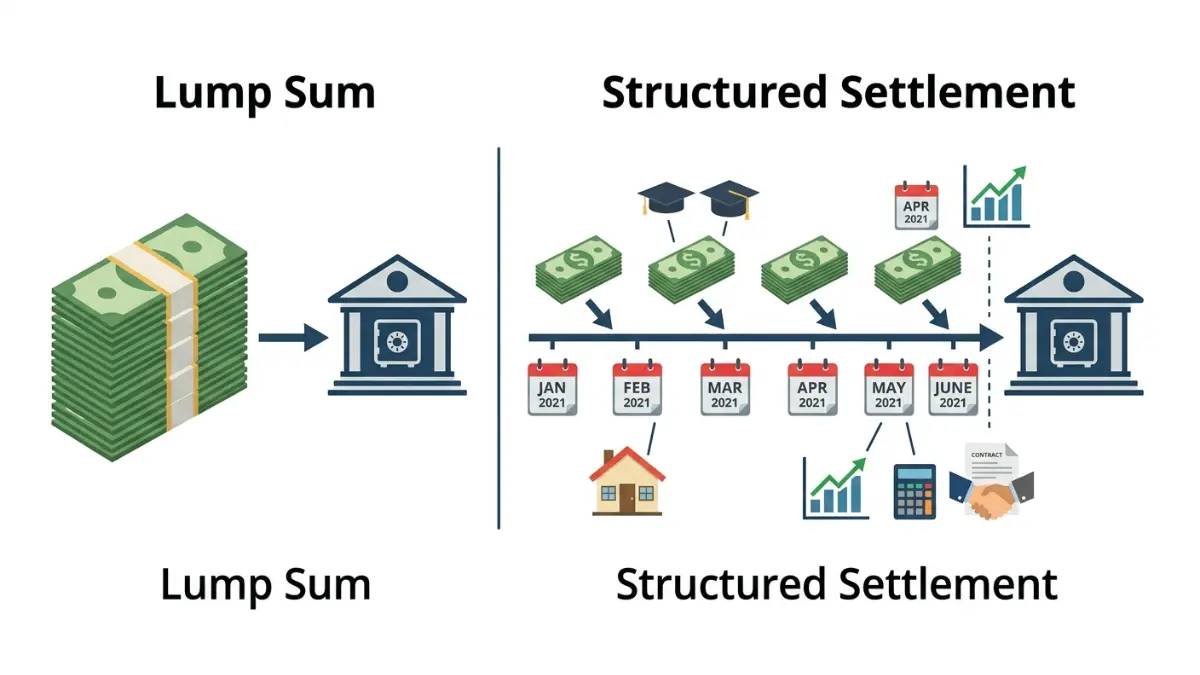

Periodic payments versus a single lump sum

A lump sum hands you everything at once. A structure spreads it across months, years, or a lifetime, with future guaranteed payments sized to medical needs, lost income, or a child’s college years.

You can also combine both. A partial lump sum at signing covers immediate bills, while the remainder funds a long-term income stream.

Why the payments are tax-free — and the one big exception

Damages received for personal physical injury or sickness are excluded from gross income, whether paid as a lump sum or as periodic payments. The growth inside the funding annuity is excluded too, which is the quiet edge over a taxable account.

📊 Data Point: Compensatory damages for personal physical injury or sickness are excluded from federal gross income under Internal Revenue Code Section 104(a)(2) — a treatment broadened by the Periodic Payment Settlement Act of 1982. — Source: Internal Revenue Service, 2026.

The exception is where people get hurt. Punitive damages and any awarded interest are taxable, even when the underlying case involved a physical injury.

💡 Expert Note (CFA): In reviewing settlement allocations over the years, the costliest mistake I see is treating an entire award as tax-free. When an agreement folds punitive damages or interest into the “injury” total without breaking them out, that taxable slice can quietly follow you onto a future tax return.

If part of your award is taxable, size the bite before you sign — one pass to estimate what you would owe on the taxable portion keeps the surprise off next April’s return.

The IRS spells out which parts of a settlement it can actually tax. To weigh a tax-free stream against investing a lump sum yourself, the math of tax-free compounding over decades is where the difference appears.

Who is at the table — and how the talks unfold

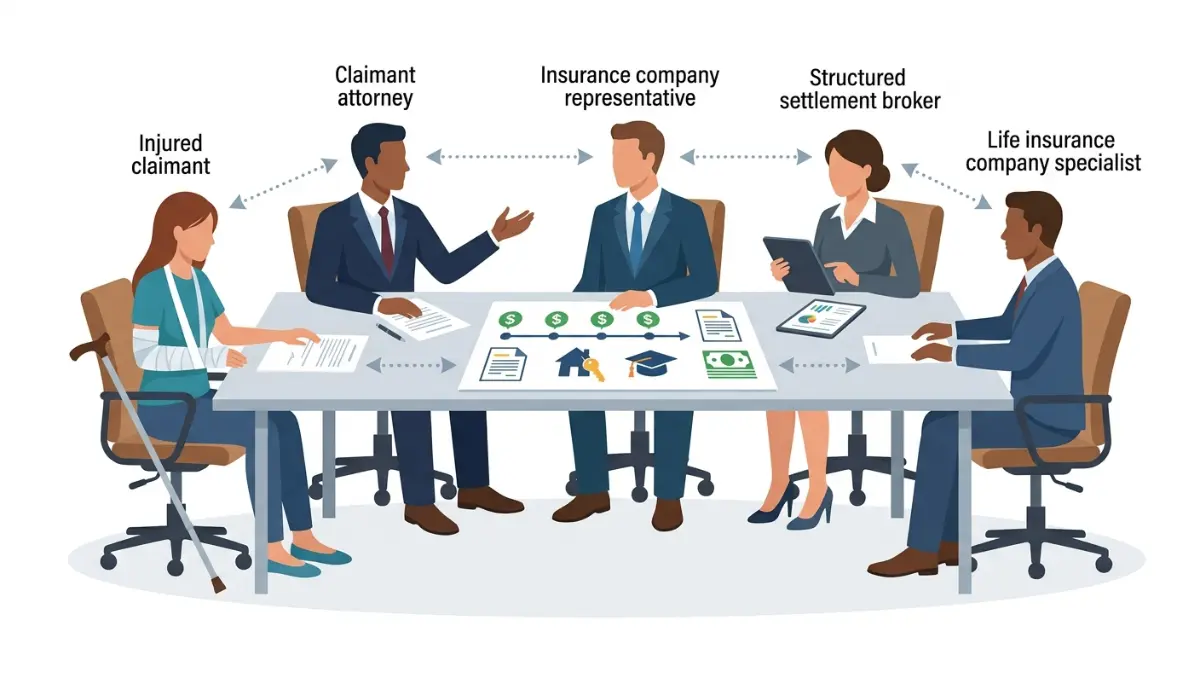

A structured settlement negotiation typically involves five parties, and knowing each one’s incentive is the difference between negotiating and being negotiated.

The five people in the room

- You, the claimant — the injured person whose future the payments are meant to protect.

- Your attorney — represents your legal interests and reviews every term before you sign.

- The defendant or, usually, their insurer — the party paying, motivated to close the case efficiently.

- The structured settlement broker — designs the annuity and payment schedule, often one for each side.

- The life insurance company — issues the annuity that funds your future payments.

A qualified assignment under Internal Revenue Code Section 130 lets the payment obligation move to an assignment company, which buys the annuity. That mechanism is what preserves the tax treatment.

Who pays the structured settlement broker?

The broker is generally paid a commission built into the annuity by the life insurer — not billed to you out of pocket. That does not make the broker your adversary, but it does mean their compensation is tied to the product being placed.

✅ Pro Tip: Within 48 hours of your next call with counsel, ask one question: “Is a plaintiff-side broker or settlement planner involved, or only the defense’s?” A planner working for you can model payment designs against your specific needs rather than the insurer’s convenience.

The order the conversation usually follows

Talks generally move from total dollar figure, to how much is taken as cash versus structured, to the payment schedule’s shape and start date. The schedule is the part most people leave on autopilot — and it is the part you can most influence.

Lump sum, structure, or both — what is still negotiable

Yes — the payment design is negotiable before you sign and effectively fixed afterward. That window is short, so treat the schedule as the real negotiation, not an afterthought.

The choice is rarely all-or-nothing. A hybrid settlement with a partial lump sum plus a structured remainder resolves the false binary for many claimants.

| Approach | Best for | Key consideration |

|---|---|---|

| Full lump sum | Confident money managers, large immediate needs | Growth is taxable; spending risk is on you |

| Full structure | Long-horizon income, dependents, spending concerns | Tax-free, but locked once signed |

| Hybrid (cash + structure) | Immediate bills plus long-term security | Lets you clear debt now and protect the rest |

Approach descriptions are general and educational; the right mix depends on your circumstances in 2026.

When a lump sum makes more sense

A lump sum fits a borrower who must clear high-interest debt immediately or who manages money with discipline. If you intend to invest it, remember the growth is taxable — running the numbers through a projection of long-term investment growth and then the tax owed on those gains shows the real after-tax result.

When a structure makes more sense

A structure fits anyone who values predictable, tax-free income or who worries about spending a large sum quickly. Mapping the monthly figure against your real expenses with a working monthly budget makes the trade-off concrete.

💡 Expert Note (CFA): For a claimant facing decades of reduced earning capacity, I have watched guaranteed tax-free monthly income outperform a lump sum that felt larger on paper. The lump sum gets spent, lent, or invested badly under emotional pressure; the structure simply keeps paying.

How the payments are funded — and what sets the amount

Your payments are funded by a life insurance annuity, and the amount turns on three things: the premium, the current interest-rate environment, and your assigned rated age.

How an annuity funds your payments

The assignment company uses settlement money to buy an annuity from a highly rated life insurer. That insurer then sends you the scheduled payments — monthly, annually, or on any timetable you negotiated.

Because payout rates move with interest rates, the same premium buys different income at different times. Treat any quoted figure as current-only and confirm it the week you sign.

What a rated age is — and why it can raise your payments

A rated age is an age the insurer assigns based on documented health conditions that shorten life expectancy. A higher rated age means a shorter expected payout period, which raises the monthly amount on life-contingent payments.

📊 Data Point: Payments from a qualified structured settlement annuity retain their tax-free status under Internal Revenue Code Section 104(a)(2) regardless of how long the payout period runs. — Source: Internal Revenue Service, 2026.

Life-contingent versus period-certain payouts

Life-contingent payments last as long as you live and stop at death. Period-certain payments run for a set number of years and continue to your beneficiaries if you pass early — a distinction that matters enormously if you have dependents.

Fixed payments also lose purchasing power over time, so check what a level payment is worth years out with an inflation-adjustment estimate.

If the structure is meant to carry you into later life, compare it against a broader retirement-income projection or your existing workplace retirement savings.

And a simple savings build-up shows what setting aside part of each payment could do.

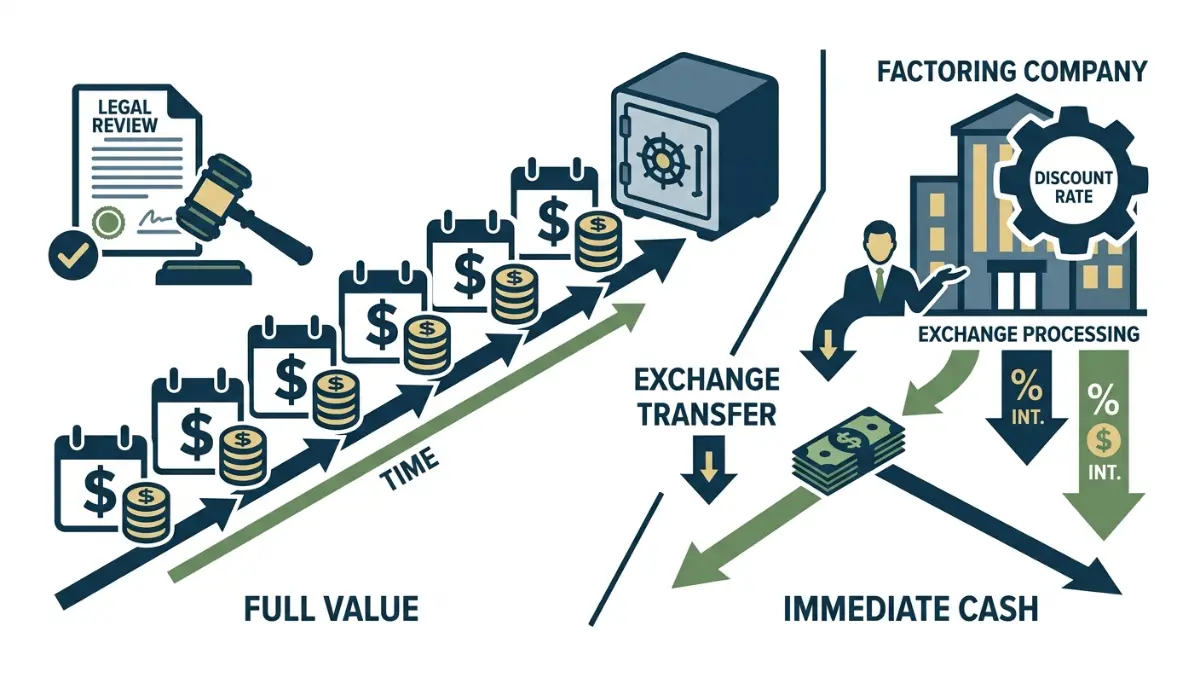

What you cannot undo — and the cost of cashing out later

A structured settlement is built to be permanent, and selling payments later is expensive and court-supervised. Understanding that now prevents an irreversible mistake at the table.

Why the design is effectively permanent

Once the annuity is purchased and the agreement signed, you cannot renegotiate the schedule. There is no “edit” button — only a difficult, discounted secondary market.

⚠️ Warning: Do not agree to a payment schedule you do not fully understand on the assumption you can fix it later. After signing, your only route to a different amount is selling future payments to a factoring company, almost always for far less than they are worth.

Selling payments later: court approval and discount rates

If you sell, a factoring company buys your future payments at a discount and a judge must approve the transfer under your state’s Structured Settlement Protection Act, applying a best-interest standard. You receive a lump sum well below the payments’ face value.

📊 Data Point: Selling structured settlement payments without court approval under an applicable state statute triggers a 40% federal excise tax on the factoring company under Internal Revenue Code Section 5891. — Source: Internal Revenue Service / Internal Revenue Code, 2026.

Consumer regulators warn this market favors the buyer. The CFPB cautions that “cash now” companies often pay far less than a settlement is worth, and a joint SEC and FINRA alert on selling income streams urges caution before any transfer.

Before ever selling, compare it against alternatives — the true return you would forfeit by discounting your own payments, and whether consolidating existing debt solves the cash crunch without giving up tax-free income.

What happens if the insurer fails

Annuities are backed by state guaranty associations if an insurer becomes insolvent, though coverage limits differ by state. This is why brokers place these annuities with the most financially secure life insurers, and why you can ask which insurer is being used and why.

Walk into the talks prepared, not pressured

The most valuable thing you can carry into the room is the knowledge that the schedule is yours to shape now and locked forever after. Slow the conversation down at exactly that point.

Ask who the broker works for, whether a partial lump sum fits your immediate needs, and how the payout type protects your dependents. Then have a licensed attorney and an independent financial professional review the draft before you sign anything — regulators flag real risks in these income-stream products once an outside party is involved.

Your future income is being designed in a single meeting. Treat it with the same care you would a 30-year decision — because that is what it is.

Frequently asked questions

1. What is a personal injury structured settlement?

A personal injury structured settlement is an agreement that pays your injury compensation as scheduled payments funded by an insurance annuity, rather than one lump sum. The periodic payments are excluded from federal income tax, and the schedule is designed during settlement to match your future financial needs.

2. How does a structured settlement negotiation work?

A structured settlement negotiation moves from the total dollar amount, to how much is taken as cash versus structured, to the schedule’s shape and start date. Your attorney, the defendant’s insurer, and a structured settlement broker shape the design, which becomes fixed once you sign the agreement.

3. Who pays the structured settlement broker?

The structured settlement broker is generally paid a commission built into the annuity by the life insurance company, not billed directly to you. Because that pay is tied to placing the product, ask whether a broker or settlement planner is also working specifically on your side of the negotiation.

4. Lump sum or structured settlement — which is better?

Neither is universally better. A lump sum suits disciplined money managers and urgent debts, while a structured settlement suits predictable tax-free income and long-term security. Many people choose a hybrid, taking a partial lump sum for immediate bills and structuring the rest to protect future income.

5. Are personal injury structured settlement payments tax-free?

Yes. Payments from a personal injury structured settlement for physical injury or sickness are excluded from federal income tax under Internal Revenue Code Section 104(a)(2), including the annuity’s growth. Punitive damages and awarded interest remain taxable, even when the case involved a physical injury.

6. What is a rated age in a structured settlement?

A rated age is an age an insurer assigns based on documented health conditions that reduce life expectancy. In a structured settlement, a higher rated age shortens the expected payout period, which raises the monthly amount on life-contingent payments designed to last for your lifetime.

7. Can I change a structured settlement after I sign it?

No. Once a structured settlement is signed and the annuity is purchased, the payment schedule cannot be renegotiated. Your only route to a different amount is selling future payments on the secondary market, which requires court approval and pays far less than the payments’ full value.

8. How are structured settlement payments funded?

Structured settlement payments are funded by a life insurance annuity. Settlement money is used to buy the annuity through a qualified assignment, and the issuing insurer then sends your scheduled payments. The amount depends on the premium, current interest rates, and your assigned rated age.

9. Can I sell my structured settlement payments later?

Yes, but selling structured settlement payments is costly. A factoring company buys them at a discount, a judge must approve the transfer under your state’s Structured Settlement Protection Act, and you receive a lump sum well below face value. Unapproved transfers carry a 40% federal excise tax.

10. What happens if the insurance company fails?

If the life insurer funding your structured settlement becomes insolvent, state guaranty associations provide a backstop, though coverage limits vary by state. This is why structured settlement annuities are placed with highly rated insurers, and why you can ask which insurer funds your payments and why.

11. Do I need my own advisor for a structured settlement?

For a high-stakes, irreversible structured settlement, an independent review is worth it. A licensed attorney protects your legal interests, while a credentialed financial professional can model payment designs against your real needs — separate from the broker whose pay is tied to placing the annuity.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.