How to Sell Structured Settlement Payments — The Right 6 Steps

Structured settlement discount rates run 9%–18% in 2026. Court approval is required in 49 states — see the process and your net proceeds before signing.

In This Article

What It Really Means to Sell Your Structured Settlement

Selling your structured settlement is legally possible — but the process is more regulated and more expensive than most factoring company advertisements disclose upfront.

Before deciding, run your numbers through a budget calculator to confirm whether your financial need is immediate, recurring, or better addressed through an alternative source of funds.

Why Factoring Companies Make It Sound Simpler Than It Is

A factoring company profits by purchasing your future annuity payments at a steep discount, then collecting the full payment value over time.

The wider that discount gap, the more profitable the transaction is for the buyer — which is why most marketing materials emphasize convenience over cost.

What This Guide Will Tell You That Most Don’t

In nearly three decades advising clients on capital markets decisions, I have reviewed structured settlement transfer offers where the true cost — once the discount rate was properly calculated — exceeded 20% of the total payment stream value.

This guide provides what buyer-affiliated content rarely does: a complete 6-step process, real discount rate calculations, mandatory legal requirements, and an honest framework for deciding whether selling is the right financial move for your situation.

ℹ️ Disclaimer: The structured settlement transfer information in this article is intended for educational purposes. Structured settlement sales are legally regulated transactions subject to mandatory state court approval under the Structured Settlement Protection Act, enacted in 49 states as of 2026. Discount rates, processing timelines, and net proceeds vary by factoring company and jurisdiction. Consult a licensed independent attorney and a fee-only financial advisor before signing any transfer agreement.

How a Structured Settlement Sale Actually Works

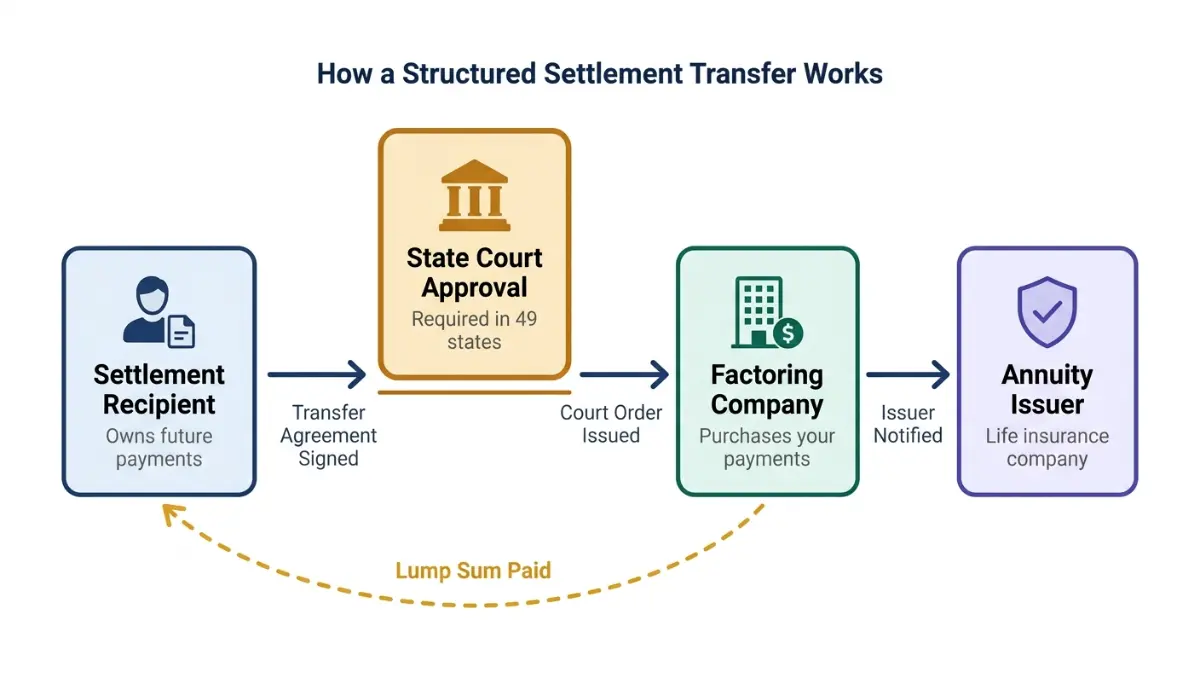

A structured settlement transfer is not a simple cash-out — it is a legally regulated three-party transaction with a specific chain of approval.

Understanding who the parties are and what is actually being sold protects you from the most common misunderstandings that factoring companies rely on.

The Three Parties in Every Structured Settlement Transfer

Every structured settlement sale involves three distinct parties with different interests.

- The settlement recipient (you): The legal owner of the right to receive future periodic payments, who is seeking a lump-sum advance on those payments.

- The factoring company: A private financial firm that purchases your payment rights at a discounted present value and assumes the right to receive your future payments.

- The annuity issuer: The life insurance company that holds the original annuity policy and continues making payments — now to the factoring company — after the transfer is completed and court-approved.

What You Are Selling (and What You Are Not)

You are selling the right to receive future periodic payments, not the annuity policy itself.

The original annuity contract remains held by the issuing insurance company, meaning the factoring company takes on counterparty risk with a regulated insurer — not with you directly — after the transfer is finalized.

💡 Expert Note (CFA): A critical distinction most buyers never explain: federal law under 26 U.S.C. §5891 imposes a 40% excise tax on factoring companies that complete structured settlement transfers without court approval. This is why every reputable buyer files a court petition — and why any company that promises to skip the court process is either misleading you or operating illegally.

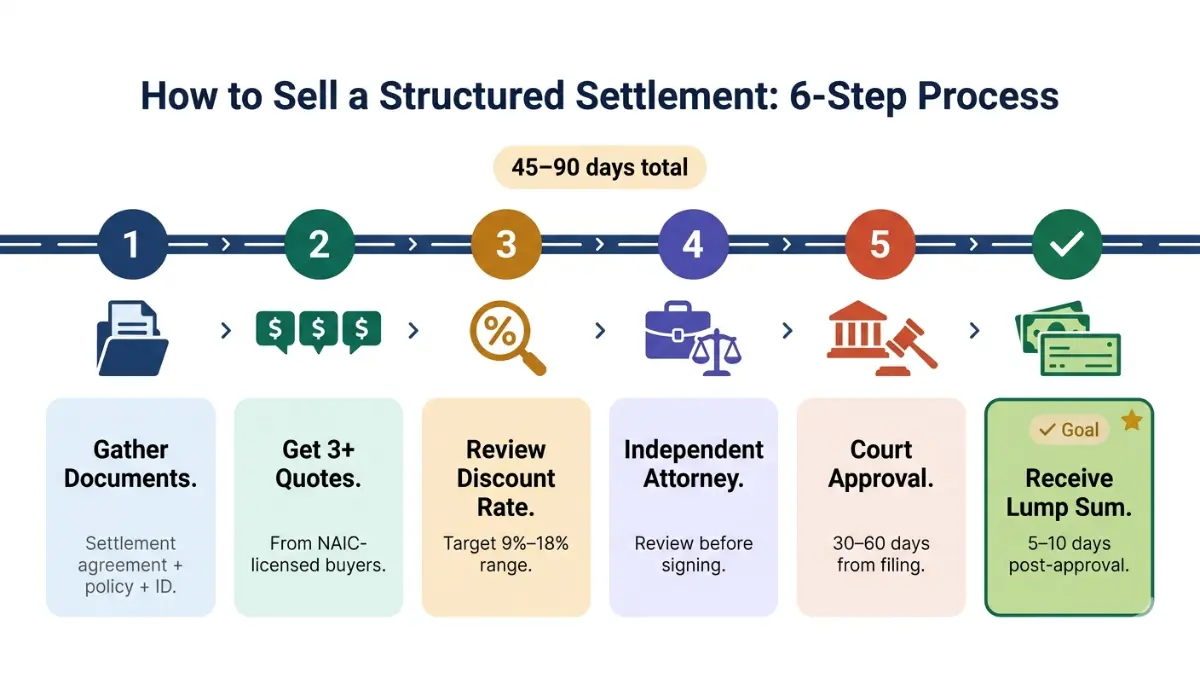

How to Sell Your Structured Settlement in 6 Steps

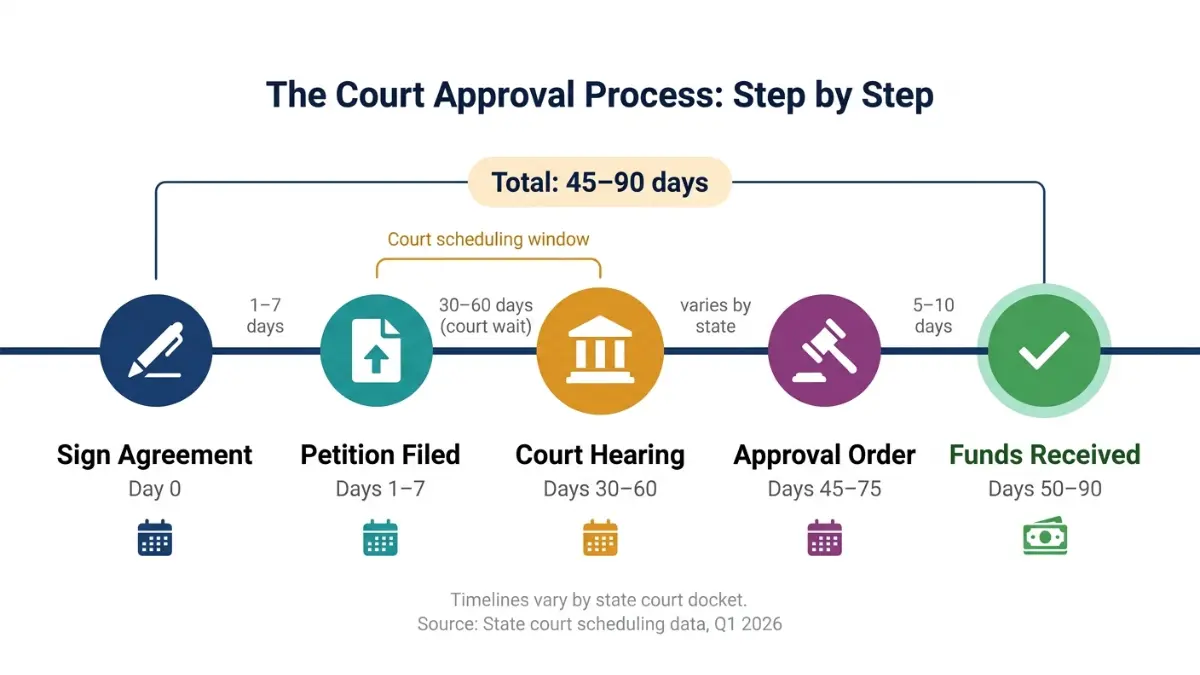

To sell your structured settlement payments, complete these six steps in order — the process typically takes 45 to 90 days from initial contact to lump-sum disbursement.

Partial sales are permitted in most states: you may sell a specific number of future payments rather than your entire remaining stream.

Step 1: Gather Your Settlement Documents

Locate your original settlement agreement, annuity policy number, current payment schedule, government-issued photo ID, and any prior court orders related to the settlement.

Missing documents extend your timeline by weeks — contact your annuity issuer directly if you cannot locate your policy number.

Step 2: Get Competing Quotes From at Least Three Factoring Companies

Contact a minimum of three NAIC-licensed structured settlement buyers and request written quotes within the same week so payment valuations are comparable.

Never accept a first offer — industry data confirms that competing quotes routinely differ by 3 to 6 percentage points on the discount rate, representing thousands of dollars on a six-figure payment stream.

Step 3: Review Each Offer’s Discount Rate and Net Proceeds

Ask each company to provide its implied annual discount rate in writing alongside the offered lump sum, processing fees, and the total dollar amount you will surrender.

Do not compare lump sums alone — a $5,000 difference in offered amounts can conceal a discount rate spread of 5% or more.

Step 4: Hire an Independent Attorney to Review the Transfer Agreement

Before signing any transfer agreement, retain an attorney who does not represent the factoring company and who has experience with structured settlement law in your state.

In my experience reviewing these agreements with clients, the discount rate calculation methodology and early-termination clauses are the most consistently misunderstood sections — and the most consequential.

✅ Pro Tip: Ask your attorney to confirm that the transfer agreement matches the written quote you received. Factoring companies occasionally modify fee terms between the quote and the contract stage.

Step 5: File the Court Petition and Attend the Approval Hearing

The factoring company files a petition in your state court, which schedules a hearing to review whether the transfer is in your best interest as the payee — a legal standard that includes evaluating your financial need, your awareness of the discount rate cost, and whether lower-cost alternatives were considered.

Court hearings are typically scheduled 30 to 60 days after petition filing, depending on your state’s docket.

Step 6: Complete the Transfer and Receive Your Lump Sum

After the judge issues a court approval order, the factoring company notifies the annuity issuer, who updates its payment records.

The lump-sum disbursement typically arrives within 5 to 10 business days of the approval order.

📊 Data Point: According to the CFPB’s consumer guidance on structured settlement transfers, sellers have the legal right to cancel a transfer agreement before the court issues its approval order. Confirm your cancellation window in writing before signing.

How to Evaluate Structured Settlement Offers and Choose a Buyer

The single most important skill in this process is reading a factoring company’s offer for what it actually costs — not what the marketed lump sum appears to be.

Run your own debt-to-income ratio calculation before accepting any offer to confirm you understand the financial gap you are trying to close and whether a partial sale might cover it.

What to Look For in a Transfer Agreement Before You Sign

Four contract elements determine whether an offer is acceptable or exploitative.

- The stated annual discount rate: Must appear in the agreement as a named percentage, not buried in a fee schedule.

- Total fees and processing costs: Must be itemized, not listed as a single undifferentiated amount.

- Your cancellation rights: You retain the right to withdraw before the court issues its approval order — the agreement must specify your cancellation window.

- The annuity issuer notification clause: Confirms that the issuing insurance company will be formally notified and will continue making payments to the factoring company post-transfer.

Red Flags That Signal a Predatory Structured Settlement Buyer

Walk away from any factoring company that does any of the following.

- Declines to provide the implied annual discount rate in writing before you sign

- Promises court approval in fewer than 30 days (not legally credible in any state)

- Discourages you from consulting an independent attorney

- Presents a verbal offer that differs from the written agreement

- Charges undisclosed fees after the transfer agreement is signed

💡 Expert Note (CFA): One of the most costly mistakes I’ve seen clients make is accepting a lump-sum offer framed in nominal dollar terms without ever calculating the implied discount rate. An offer of $82,000 on a $100,000 remaining payment stream sounds like a modest haircut. At certain payment schedules, that same offer implies a 22% effective annual discount rate — well above the 2026 market range of 9% to 18%.

Your Right to Shop Competing Offers (and Why Most Buyers Don’t Mention It)

No federal law or state SSPA requires you to accept the first offer you receive, and no factoring company can legally penalize you for requesting competing quotes.

The structured settlement factoring market is competitive — three written quotes is the minimum standard a fee-only financial advisor would recommend before any transfer agreement is signed.

📊 Data Point: The CFPB’s 2026 consumer financial protection guidance confirms that settlement recipients retain full rights to compare offers, seek independent counsel, and withdraw from a transfer agreement prior to court approval. Source: Consumer Financial Protection Bureau, Q1 2026.

What a Structured Settlement Sale Will Actually Cost You

The discount rate on a structured settlement sale is the annualized percentage a factoring company applies to reduce the present value of your future payments to their offered lump sum — and in 2026, that rate ranges from 9% to 18% among reputable buyers, according to National Structured Settlement Trade Association transaction data.

This is the number that determines your true cost.

How the Discount Rate Determines Your Net Proceeds

The factoring company calculates the present value of your future payment stream using its offered discount rate, then pays you that present value as a lump sum.

The higher the discount rate, the lower the lump sum you receive — and unlike a loan, this loss is permanent and irrevocable once the court approves the transfer.

Use an APR calculator to convert the factoring company’s discount rate into an annualized equivalent — this allows a direct cost comparison against personal loan APRs, which typically run 8% to 28% for creditworthy borrowers in Q1 2026.

You can also use a percentage calculator to verify the discount rate math on any offer before you sign.

The Real Cost at 9%, 12%, 15%, and 18%: A Worked Calculation

The table below shows illustrative lump-sum outcomes on a $100,000 total remaining payment stream at different discount rates. Actual net proceeds depend on payment timing, duration, and factoring company methodology — use these figures as a comparison benchmark, not a precise quote.

📊 Data Point: The 2026 industry discount rate range of 9%–18% reflects current NSSTA transaction data. Rates above 18% are at the high end and above 20% are considered predatory by consumer advocacy organizations. Source: National Structured Settlement Trade Association (nssta.com), Q1 2026.

| Discount Rate | Lump Sum Offered | Dollar Loss | % of Stream Surrendered | Key Consideration |

|---|---|---|---|---|

| 9% | $91,000 | $9,000 | 9% | Lowest cost — rare; negotiate aggressively to approach this |

| 12% | $88,000 | $12,000 | 12% | Below market average — strong offer worth accepting if urgent |

| 15% | $85,000 | $15,000 | 15% | Near 2026 market average — acceptable if no lower-cost option exists |

| 18% | $82,000 | $18,000 | 18% | High end of market range — request competing quotes before accepting |

| 22%+ | $78,000 | $22,000+ | 22%+ | Predatory threshold — decline and reshop with at least two other buyers |

Source: Illustrative figures based on NSSTA 2026 transaction range. Verify your specific offer using the implied discount rate formula: Discount Rate = (Total Future Payments − Lump Sum) ÷ Total Future Payments.

An inflation calculator can show you the real purchasing-power value of your future payment stream today, which often reveals that the lump-sum offer is even less competitive than the nominal discount rate suggests.

For context on what keeping your payments and investing them could return over the same period, an investment calculator provides a useful comparison benchmark.

When Selling Makes Financial Sense — and When It Doesn’t

Selling a structured settlement is financially rational when three conditions are simultaneously true: the immediate financial need exceeds the cost of the discount rate, no lower-cost financing alternative is available, and the lump sum will address a non-recurring crisis rather than fund ongoing expenses.

Selling is financially irrational when the proceeds will be used for discretionary spending, when a personal loan at market rates would cost less than the discount rate, or when only a portion of the payment stream would satisfy the need — in which case, a partial sale preserves more of your long-term income.

Court Approval: The Legal Step Every Structured Settlement Sale Requires

Court approval is not optional. In 49 states, any structured settlement transfer that is completed without a judge’s approval order triggers a 40% federal excise tax under 26 U.S.C. §5891 — a cost that effectively voids the economic rationale of the transaction entirely.

The single state without an SSPA as of 2026 is Vermont; all other states require a state court judge to review and approve every transfer before funds can be disbursed.

What the Structured Settlement Protection Act Requires From You

Under the applicable state Structured Settlement Protection Act, the factoring company — not you — bears responsibility for filing the court petition, paying court costs, and scheduling the hearing.

Your obligation is to appear at the hearing, provide documentation of your financial need if requested by the court, and confirm that you understand the discount rate and have received independent legal advice.

💡 Expert Note (CFA): Courts apply a “best interest of the payee” standard — meaning the judge evaluates your financial circumstances, your awareness of the true cost, and whether alternatives were considered. I advise clients to document their financial need in writing before the hearing. A judge who sees that a client carefully evaluated alternatives and understands the discount rate math is far more likely to approve the transfer without delay.

The IRS clarifies in IRS Publication 4345 that original structured settlement payments received on schedule are generally income tax-exempt — but consult a CPA on how a lump-sum transfer may affect your specific tax situation, particularly if your settlement includes punitive damages.

Use an income tax calculator to model the potential tax impact of receiving a large lump sum in a single tax year, and a capital gains tax calculator if any portion of your settlement proceeds involve investment returns.

What Judges Look For Before Approving a Transfer

Judges applying the best-interest standard typically evaluate four factors.

- Financial need: Is there a documented, legitimate reason for needing a lump sum now — medical debt, housing emergency, debt resolution — rather than a preference for convenience?

- Cost awareness: Does the seller understand the implied discount rate and the total dollar amount surrendered?

- Alternatives considered: Did the seller evaluate lower-cost financing options before reaching this transaction?

- Independent legal counsel: Was the seller represented by an attorney independent of the factoring company?

State-by-State: How Long Court Approval Takes

Court approval timelines vary significantly by state docket conditions. The figures below reflect 2026 average windows from petition filing to judge’s order.

| State | Average Court Approval Window |

|---|---|

| California | 60–90 days |

| Texas | 45–75 days |

| Florida | 45–60 days |

| New York | 60–90 days |

| Illinois | 45–75 days |

| Ohio | 30–60 days |

Source: State court scheduling data, Q1 2026. Timelines subject to docket conditions.

Risks to Know Before You Sell — and Alternatives Worth Considering First

The most important risk in any structured settlement sale is one that most guides mention last and most readers underestimate: the transfer is irrevocable after court approval.

Once the judge signs the order and the annuity issuer updates its records, no court will unwind the transaction — and no factoring company will buy those payments back at what you surrendered them for.

Five Risks Every Structured Settlement Seller Should Understand

Consider each of these before signing any transfer agreement.

- Irrevocability: The income stream you sell is permanently gone — not deferred, not recoverable at any price after court approval.

- Above-market discount rates: A rate above 18% costs you more than a personal loan would in most 2026 credit environments.

- Loss of income stability: Structured settlement payments are guaranteed by a rated insurance company — the lump sum is not.

- Tax exposure: Depending on your settlement type, a lump-sum receipt may have income tax implications that periodic payments did not.

- Predatory buyer tactics: High-pressure sales tactics, undisclosed fees, and verbal offers that differ from written contracts are documented patterns in this industry.

Lower-Cost Alternatives to Selling Your Structured Settlement

Before committing to a sale, compare the discount rate cost against these alternatives.

- Personal loan: A loan calculator can show you the total interest cost of a personal loan at current 2026 APRs — for borrowers with good credit, this is often cheaper than the discount rate.

- Debt consolidation: A debt consolidation calculator compares consolidation costs against your current obligations — relevant if debt is the trigger for the lump-sum need.

- HELOC or home equity loan: If you own property, a home equity calculator shows your available equity — HELOC rates in Q1 2026 average 8.9% to 10.4% for qualified borrowers, significantly below most factoring discount rates.

- Partial structured settlement sale: Selling 12 to 24 months of payments rather than the full remaining stream preserves your long-term income while addressing a near-term cash need.

- Emergency savings: A savings calculator helps determine how quickly you could accumulate the needed funds without surrendering any payment rights.

The CFA’s Honest Assessment: Is Selling Right for You?

Selling a structured settlement makes financial sense when your immediate, documented need exceeds the cost of the discount rate and no lower-cost alternative is available within your required timeline.

It is the wrong decision when the proceeds fund discretionary spending, when you have not obtained competing quotes, or when you have not had an independent attorney confirm the transfer agreement terms.

⚠️ Warning: Before signing a transfer agreement, consult an independent attorney who does not represent the factoring company. The clients I’ve seen regret this decision most were those who acted under time pressure without independent legal review — and no amount of post-signing regret reverses a court-approved structured settlement transfer.

Frequently Asked Questions About Selling Structured Settlement Payments

1. How do you sell structured settlement payments?

To sell structured settlement payments, gather your settlement documents, get competing quotes from at least three factoring companies, review each offer’s discount rate and net proceeds, hire an independent attorney to review the transfer agreement, file the court petition, and receive your lump sum 5 to 10 days after court approval. The full process takes 45 to 90 days.

2. How long does it take to sell a structured settlement?

Selling a structured settlement typically takes 45 to 90 days from initial contact to lump-sum disbursement. The court petition and approval hearing account for the majority of the timeline — most state courts schedule hearings 30 to 60 days after the petition is filed. Incomplete documentation or high court docket volume can extend the process.

3. What is the discount rate for structured settlement sales?

The structured settlement discount rate is the annualized percentage a factoring company uses to calculate the present value of your future payments, then pays you as a lump sum. In 2026, reputable buyers offer rates between 9% and 18%, according to NSSTA transaction data. Rates above 18% are at the high end and should trigger additional competing quotes.

4. Do I need court approval to sell my structured settlement?

Yes. In 49 states, court approval is required for every structured settlement transfer under the applicable Structured Settlement Protection Act. A state court judge applies a “best interest of the payee” standard before issuing an approval order. Transfers completed without court approval trigger a 40% federal excise tax under 26 U.S.C. §5891.

5. How much money will I lose selling my structured settlement?

The amount lost depends on the discount rate applied and the timing of your payments. On a $100,000 total remaining payment stream, a 12% discount rate costs approximately $12,000, while an 18% rate costs approximately $18,000. Rates above 20% are considered predatory by consumer advocacy organizations. Always request the implied annual discount rate in writing before signing.

6. Is it a good idea to sell your structured settlement?

Selling a structured settlement is financially rational only when your documented need exceeds the discount rate cost, no lower-cost financing alternative is available, and the lump sum addresses a non-recurring crisis. It is the wrong decision when proceeds fund discretionary spending, when a personal loan would cost less, or when a partial sale would satisfy the need.

7. What companies buy structured settlements?

The largest structured settlement buyers in the U.S. include JG Wentworth, Peachtree Financial Solutions, DRB Capital, and Seneca One Finance. Before selecting a buyer, confirm that the company is NAIC-licensed, discloses its discount rate in writing, and does not discourage you from seeking independent legal counsel. Always obtain competing quotes from at least three buyers.

8. Can you sell part of your structured settlement?

Yes. A partial structured settlement sale allows you to sell a specific number of future payments — for example, the next 24 monthly payments — while retaining the remainder of your payment stream. Partial sales require the same court approval process as full transfers and are available in most states. This option often satisfies a near-term cash need at lower total cost.

9. Are structured settlement sales taxable?

Original structured settlement payments are generally income tax-exempt under IRS Publication 4345 when they arise from physical injury or illness claims. However, a lump-sum transfer may have tax implications depending on your settlement type, the year you receive the funds, and your existing income. Consult a CPA before completing a transfer to confirm your specific tax treatment.

10. What is the Structured Settlement Protection Act?

The Structured Settlement Protection Act is state legislation — enacted in 49 states as of 2026 — that requires every structured settlement transfer to be reviewed and approved by a state court judge before the transfer is finalized. The act protects settlement recipients by requiring disclosure of the discount rate, net proceeds, and the right to seek independent legal advice before signing.

11. Can you sell a structured settlement from a workers’ compensation claim?

Workers’ compensation structured settlements are subject to additional state-specific restrictions that vary significantly. In many states, workers’ comp settlement transfers face stricter court review standards or require approval from a workers’ compensation board in addition to the standard court petition. Consult a licensed attorney in your state before pursuing a factoring transaction on a workers’ comp settlement.

12. What happens after a judge approves my structured settlement sale?

After court approval, the factoring company formally notifies the annuity issuer — the life insurance company holding the original policy — that payment rights have been transferred. The issuer updates its payment records, and the factoring company disburses your lump sum, typically within 5 to 10 business days of the approval order. Your original payment stream then routes to the factoring company.

13. What documents do I need to sell my structured settlement?

To initiate a structured settlement sale, you typically need your original settlement agreement, the annuity policy number or policy document, your current payment schedule, government-issued photo ID, and documentation of any prior court orders related to the settlement. Missing documents are the most common cause of timeline delays — contact your annuity issuer proactively if any document cannot be located.

14. Can I back out of selling my structured settlement?

Yes — before court approval is issued, you retain the right to cancel the transfer agreement. Most state SSPAs preserve this right through the date of the approval order. After the judge signs the order and the annuity issuer is notified, the transfer is legally finalized and cannot be reversed. Confirm your specific cancellation window in writing before signing any agreement.

15. What is the difference between selling and borrowing against a structured settlement?

Selling a structured settlement permanently transfers your right to future payments to a factoring company in exchange for a lump sum — it is irrevocable after court approval. Borrowing against a structured settlement, where permitted, is a loan secured by future payments that must be repaid with interest. Selling eliminates the income stream entirely; borrowing preserves it if repaid on schedule.

16. How do I choose the best structured settlement buyer?

To choose the best structured settlement buyer, compare the implied annual discount rate — not just the offered lump sum — from at least three NAIC-licensed companies. Confirm that each buyer discloses all fees in writing, supports your right to independent legal counsel, and does not pressure you to sign before comparing offers. A lower discount rate and transparent fee disclosure are the two most reliable quality signals.

17. What are the alternatives to selling a structured settlement?

Alternatives to a structured settlement sale include personal loans (often cheaper than the discount rate for creditworthy borrowers), home equity lines of credit (averaging 8.9% to 10.4% APR in Q1 2026), partial structured settlement sales that preserve the majority of your income stream, debt consolidation, and liquidating emergency savings. Evaluate each option’s true cost before committing to an irrevocable transfer.

Your Next Step: Sell Smarter or Reconsider First

The clients I’ve seen navigate this process most successfully shared one discipline: they got competing quotes, had an independent attorney review the agreement before signing, and understood the discount rate math before they sat down in the courtroom.

A structured settlement sale cannot be undone after court approval.

Three Actions to Take Before You Contact Any Factoring Company

- Calculate your financial gap using your actual income, obligations, and the specific lump sum needed — not a ballpark.

- Get at least three written quotes from NAIC-licensed buyers, each with the implied annual discount rate stated explicitly.

- Retain an independent attorney before signing any transfer agreement — one whose fee is paid by you, not the factoring company.

The CFPB’s consumer guidance on structured settlement transfers is a free starting point for understanding your legal rights throughout this process.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.