How a Retiree Should Weigh Selling a Structured Settlement

Structured settlement payments of $1,500 a month feel safe—until a buyer offers cash. See the real cost, court approval, and keep-or-sell math.

In This Article

You hold a guaranteed check — should you trade it for cash?

A structured settlement paying $1,500 a month is one of the steadiest income streams a retiree can own. The real question is whether trading it for a single lump sum ever works in your favor.

That question rarely arrives calmly. A medical bill, a failing roof, a stack of credit card statements, or a glossy mailer promising “fast cash for your payments” pushes it to the front of the kitchen table overnight.

Here is the answer most sites selling these deals will not lead with. Selling is sometimes the right move and often a costly one, and the line between the two is math you can run yourself before anyone visits your home.

This guide covers what your payments are truly worth, how a sale works, what lands in your bank account after the discount, and when keeping the income clearly wins. You can also see how the stream fits your wider plan with a retirement income calculator.

Read it before you sign. The protections built into this process exist for your benefit — and they only work if you use them.

ℹ️ Disclaimer: This article explains the sale of structured settlement payments — a regulated insurance and financial transaction — for educational purposes only. Discount rates, tax treatment, court-approval rules, and benefit impacts vary by state, by contract, and by individual circumstances as of 2026. Before selling any portion of a structured settlement, consult a licensed financial professional, a tax advisor, and where court approval or public benefits are involved, an attorney.

What a structured settlement actually pays you

Your settlement is a promise from a life insurance company to pay you on a fixed schedule, often for decades or for life.

Guaranteed, insurer-backed income

These payments are backed by an annuity the at-fault party purchased to fund your award. That structure is why the income is so dependable: it does not fluctuate with the stock market, and it cannot be spent in a weak moment.

For a retiree, that reliability is the entire point. A guaranteed $1,500 every month is harder to replace than most people assume, especially once you factor in how inflation quietly erodes fixed dollars over a long retirement — something you can model with an inflation impact tool.

The trade-off is rigidity. The schedule that made sense the year your case settled may not match the life — or the budget — you have now, which you can map in a household budgeting tool.

Why the payments are usually tax-free

Payments from a personal physical injury settlement generally arrive free of federal income tax. That advantage often makes the income worth more, dollar for dollar, than taxable money of the same size.

📊 Data Point: Payments from a personal physical injury structured settlement are excluded from gross income under Internal Revenue Code Section 104(a)(2). — Source: Internal Revenue Service, 2026.

The tax treatment depends on what your award was meant to replace, which the IRS explains in its overview of how settlement proceeds are taxed. Awards for lost wages or punitive damages can be treated very differently from injury compensation.

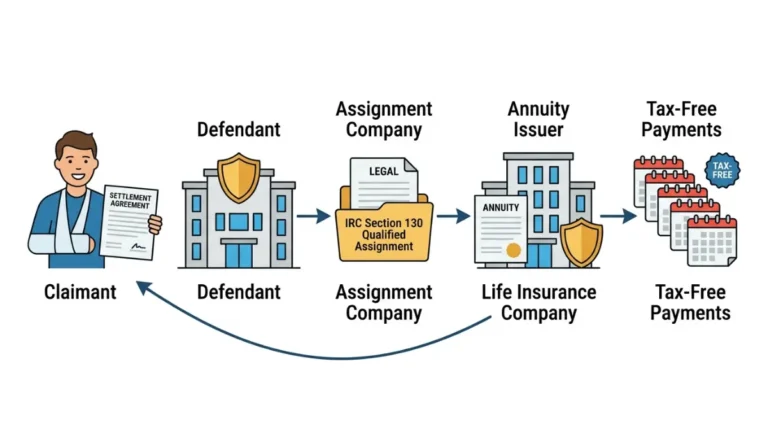

How selling a structured settlement actually works

Selling means transferring your future payments to a buyer in the secondary market in exchange for cash today.

Full sale versus partial sale

A full sale hands over every remaining payment. A partial sale lets you sell a set number of payments — or a slice of each monthly check — and keep the rest of your guaranteed income intact.

The partial route is the option most retirees overlook and the one buyer-funded ads rarely emphasize. Selling only enough payments to cover a specific need often beats surrendering the whole stream.

The court-approval step you cannot skip

Every legitimate sale runs through a courtroom. A judge reviews the deal under your state’s Structured Settlement Protection Act and must decide it serves your interest before any money moves.

The typical process — application, mandatory written disclosures, a waiting period, and a hearing — runs roughly 45 to 90 days. That timeline is a feature, not a flaw: it gives you room to reconsider an offer made under pressure.

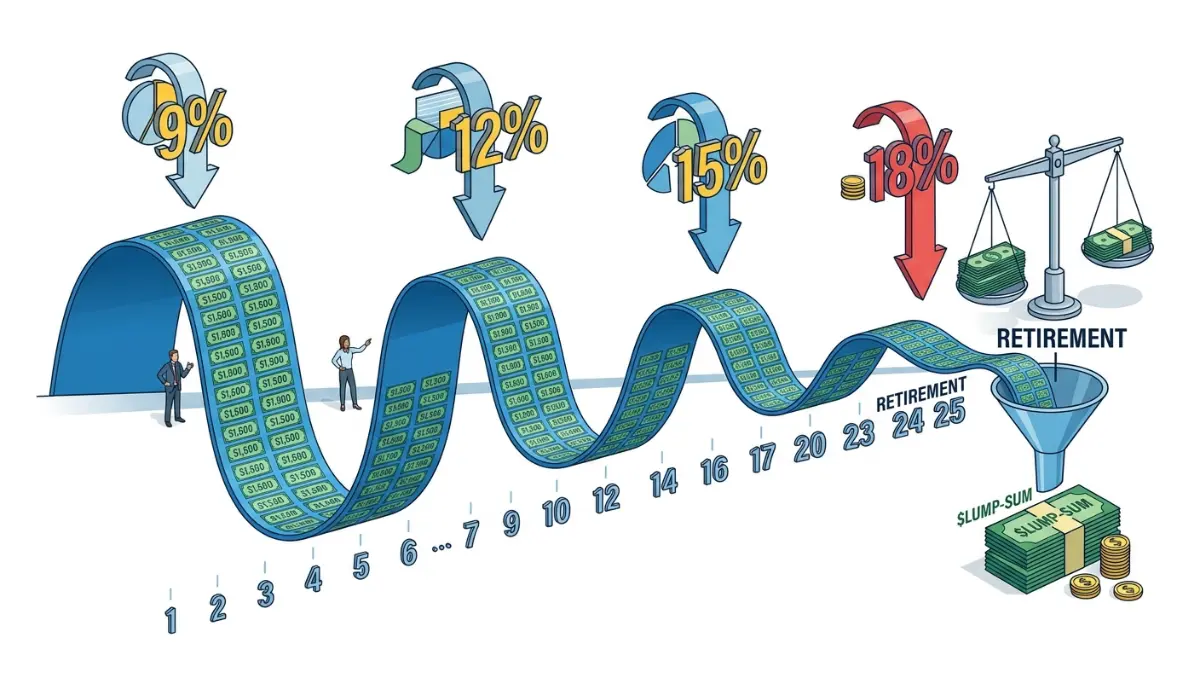

How much cash will you really get for $1,500 a month?

Expect noticeably less than the total of the payments you give up — that gap is the price of getting your money early.

Buyers apply a discount rate to your future payments, and industry data in 2026 puts that rate roughly between 9% and 18%. On a stream worth $100,000 on paper, sellers commonly net somewhere between $82,000 and $91,000, with the rest kept by the buyer.

| Discount rate | Cash you receive | Total you give up | Key consideration |

|---|---|---|---|

| 9% | ~$91,000 | ~$9,000 | Most competitive offers land here |

| 12% | ~$87,000 | ~$13,000 | Common mid-range quote |

| 15% | ~$84,000 | ~$16,000 | Shop and compare before signing |

| 18% | ~$82,000 | ~$18,000 | High end of the typical range |

Illustrative figures on a $100,000 face value, based on industry-reported discount rates. Your actual quote depends on payment timing and the buyer; verify current terms directly.

📊 Data Point: The Consumer Financial Protection Bureau cautions that people who sell future settlement payments can receive far less cash than the settlement is actually worth. — Source: Consumer Financial Protection Bureau, 2026.

The smartest move is to translate any quoted rate into plain dollars given up, then compare that cost to what the cash would earn or save you. A compound interest calculator shows the long-run cost of losing the payments, and a return-on-investment tool frames the same gap as the profit the buyer earns on money you already own.

💡 Expert Note (CFA): In nearly three decades advising clients, the costliest mistake I see with these offers is judging them by the headline cash, not the dollars surrendered. When a retiree sells $100,000 of payments for $84,000, that $16,000 is a guaranteed return the buyer collects on your asset — I make clients write both numbers down, side by side, before anyone signs.

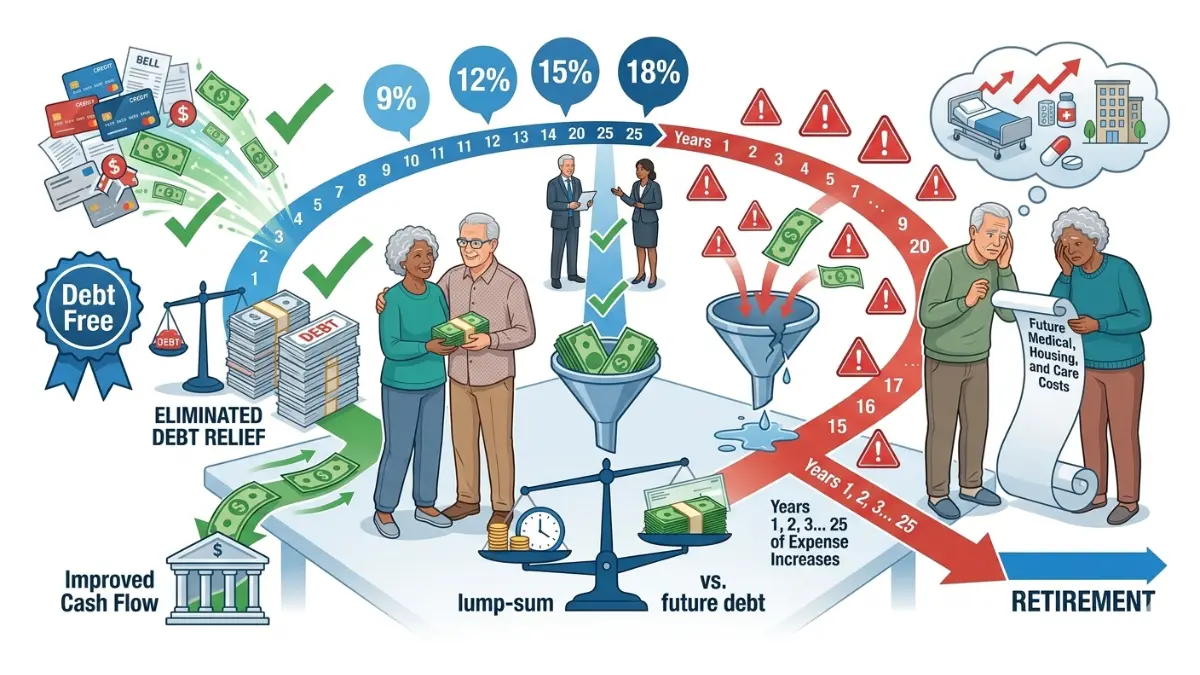

When selling makes sense — and when it doesn’t

Sell only when the cash solves a problem the payments cannot, and never to replace income you cannot rebuild.

The income you would have to replace

Start with one number: the monthly payment you would lose. For a retiree on a fixed budget, surrendering $1,500 a month to clear a one-time bill can trade a permanent income hole for a temporary fix.

Selling tends to make sense in a narrow set of cases. Wiping out high-interest debt is the strongest one, since a debt consolidation tool and a credit card payoff tool can show that card balances at 22% to 29% APR cost far more than the discount on a structured settlement.

Five questions before you sign

It tends to be a mistake when the payments fund daily living, when the cash covers ordinary spending, or when a smaller solution exists. Weigh the lost stream against your Social Security benefit estimate and against what the proceeds might earn in a diversified investment growth tool before deciding.

✅ Pro Tip: Before requesting a single quote, write down the exact dollar amount you need and the specific bill it covers. Then ask whether selling only enough payments to cover that amount — rather than the entire stream — gets you there.

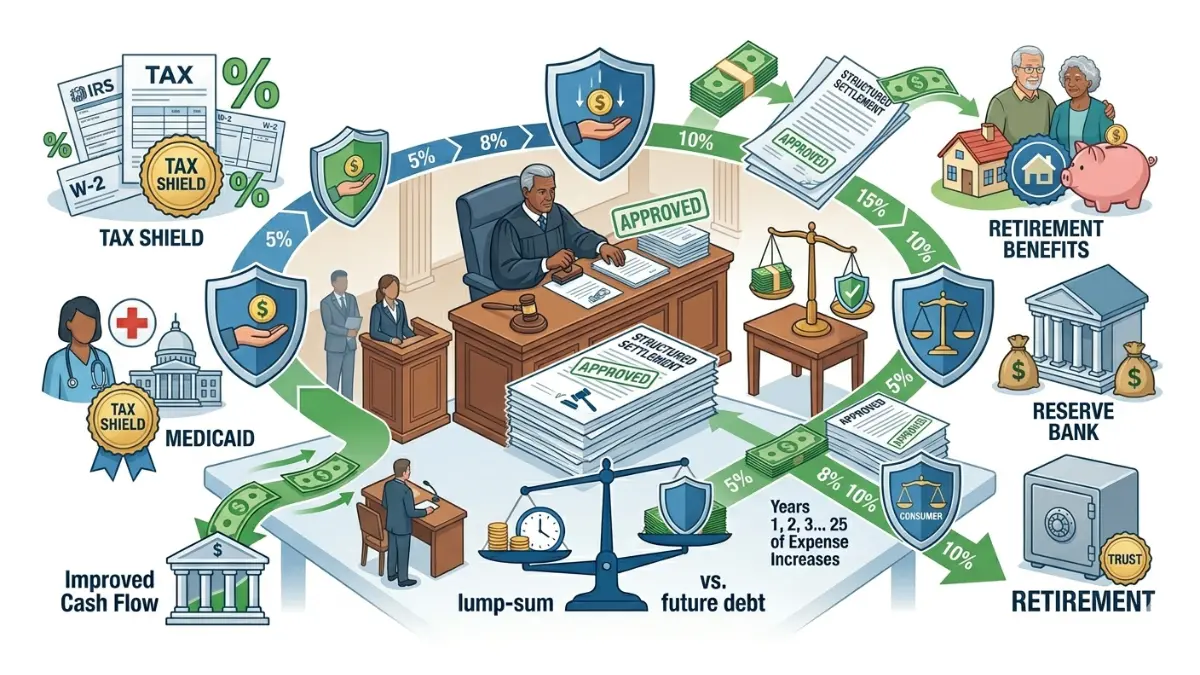

Court approval, taxes, and benefit risks to know first

A judge stands between you and a bad deal — and a few hidden risks can cost more than the discount rate.

Yes, court approval is mandatory almost everywhere. A judge must review the transfer and find it in your best interest before the sale is final, which is your strongest built-in protection against a predatory offer.

📊 Data Point: Nearly every state — 49 states plus the District of Columbia — requires a judge to approve a structured settlement transfer and find it in the seller’s best interest. — Source: state Structured Settlement Protection Acts; Consumer Financial Protection Bureau, 2026.

There is also a powerful tax rule working in your favor. A federal excise tax pushes buyers to seek court approval, because skipping it is financially ruinous for them.

📊 Data Point: Federal law imposes a 40% excise tax on the factoring discount when a structured settlement is sold without an advance court-approved qualified order. — Source: Internal Revenue Service, IRC Section 5891, 2026.

You can read the federal rule directly on the IRS page describing the excise tax on settlement factoring transactions, and the consumer agency’s cautions for people selling future payments are worth reading in full.

⚠️ Warning: A lump sum can disqualify you from Medicaid, SSI, or other means-tested benefits by pushing you over the asset limit. If you receive any needs-based benefit, confirm the impact before you sell — lost coverage can cost far more than the cash you collect.

The lump sum can also create taxable income depending on what you do with it, so estimate the effect with an income tax estimator before counting on the full amount.

Structured settlement and lump sum: common retiree questions

1. How much cash will I get for $1,500 a month?

Your lump sum depends on how many payments you sell and the discount rate the buyer applies. At an industry-typical 9% to 18% rate, a structured settlement stream worth $100,000 on paper often nets roughly $82,000 to $91,000. Selling fewer payments raises the share you keep.

2. Is selling a structured settlement a good idea for a retiree?

Selling a structured settlement is rarely wise for a retiree whose monthly payments cover living costs, because that income is hard to replace. It can make sense when the lump sum eliminates high-interest debt or funds a genuine one-time need you cannot meet another way.

3. How is the lump sum calculated?

Buyers calculate your lump sum using present value: they total the future payments, then subtract a discount rate for the time value of money and their profit. A higher discount rate, or payments due far in the future, shrinks the structured settlement cash you actually receive.

4. Do I pay taxes on the lump sum?

Payments from a personal physical injury structured settlement are generally tax-free under federal law, and a court-approved sale usually preserves that tax-free treatment on the lump sum. Non-injury settlements can be taxed differently, so the classification of your original award determines the final result.

5. Can I sell only part of my payments?

Yes. A partial sale lets you sell a set number of future payments, or a portion of each monthly check, while keeping the rest of your structured settlement. Retirees often choose this route to raise a lump sum without surrendering all of their guaranteed monthly income.

6. Who has to approve the sale?

A judge must approve almost every structured settlement sale. In 49 states and the District of Columbia, a court reviews the deal and must find the lump sum transfer is in your best interest before any money changes hands, which blocks the most predatory offers from closing.

7. Will selling affect my Medicaid or SSI?

It can. A large lump sum from a structured settlement counts as a resource that may push you over the asset limits for Medicaid, SSI, or other means-tested benefits. Receiving and holding the cash the wrong way can interrupt coverage you depend on.

8. What discount rate is fair?

A competitive structured settlement discount rate in 2026 generally sits toward the lower end of the 9% to 18% industry range. Always convert the quoted rate into the actual dollars you surrender, because two offers with similar rates can differ by thousands on the same lump sum.

9. How long does the sale take?

Selling a structured settlement typically takes about 45 to 90 days because of the required court hearing. The timeline covers your application, written disclosures, a waiting period, and a judge’s review before the lump sum is released, so it is never a same-week source of cash.

10. Can I change my mind after signing?

Often, yes. Most state Structured Settlement Protection Acts give you a cancellation window after signing and before the court approves the lump sum, so you can back out of a structured settlement sale. The exact number of days varies by state, so read your contract’s cancellation clause closely.

11. What are the alternatives to selling?

Before selling a structured settlement, weigh lower-cost options: a personal loan, a home equity line, paying off only the highest-interest debt, or selling just a few payments rather than the whole stream. Each can raise a lump sum while protecting more of your guaranteed monthly income.

The bottom line: protect the income first

Keep the payments unless both the math and an independent advisor point clearly toward selling.

For most retirees, a guaranteed $1,500 a month is worth more than the discounted cash a buyer will offer for it. When a real need exists, a partial sale usually beats a full one, and a court’s best-interest review is a safeguard worth leaning on.

If you do receive a lump sum, give it a job before you spend a dollar. Park it somewhere safe first — a high-yield savings tool or a certificate of deposit calculator can show what idle cash earns while you plan, and FINRA’s guidance on handling a sudden sum of money lays out sensible first steps.

Run the numbers, sleep on the offer, and bring in a fiduciary who is not paid on the transaction before you sign anything.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.