What Structured Settlement Scams Actually Cost in 2026

Structured settlement scams cost recipients $40,200 on a single deal when discount rates exceed the 2026 NSSTA fair-market threshold of 11.4%.

In This Article

Why structured settlement scam offers are surging in 2026

Structured settlement scams did not invent themselves in 2026. They scaled.

📊 Data Point: The CFPB recorded more than 3,400 structured settlement transfer complaints in 2026 — a 23% increase over the prior reporting period. Source: Consumer Financial Protection Bureau, Q1 2026 Annual Complaint Report.

The contact no longer comes only by phone. Predatory factoring companies now reach settlement recipients through text campaigns, social media ads, and data-broker-driven email — timed to hit during identifiable financial stress events.

In 28 years of reviewing structured financial products on behalf of clients, I have seen factoring agreements carrying effective APRs above 22% — delivered with fabricated 48-hour deadlines as the opening tactic.

This article gives you nine specific red flags with 2026 benchmarks you can apply to the offer already in your hand. Reading what structured settlements pay and cost is the baseline — this article is the protection layer on top of it.

ℹ️ Disclaimer: The information in this article addresses the transfer and sale of structured settlement payment rights, a financial and legal transaction governed by state Structured Settlement Protection Acts (SSPAs) and subject to mandatory court approval in most U.S. jurisdictions. All rates and regulatory thresholds are current as of 2026 and subject to change. Consult a licensed financial professional (CFA or CFP) and a licensed attorney with structured settlement experience before executing any transfer agreement.

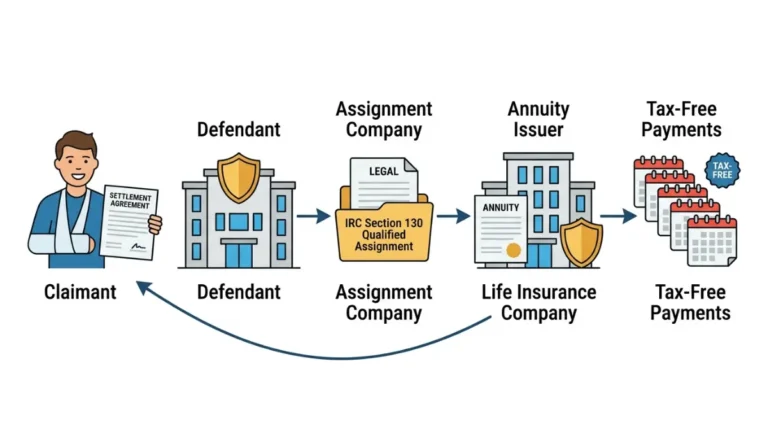

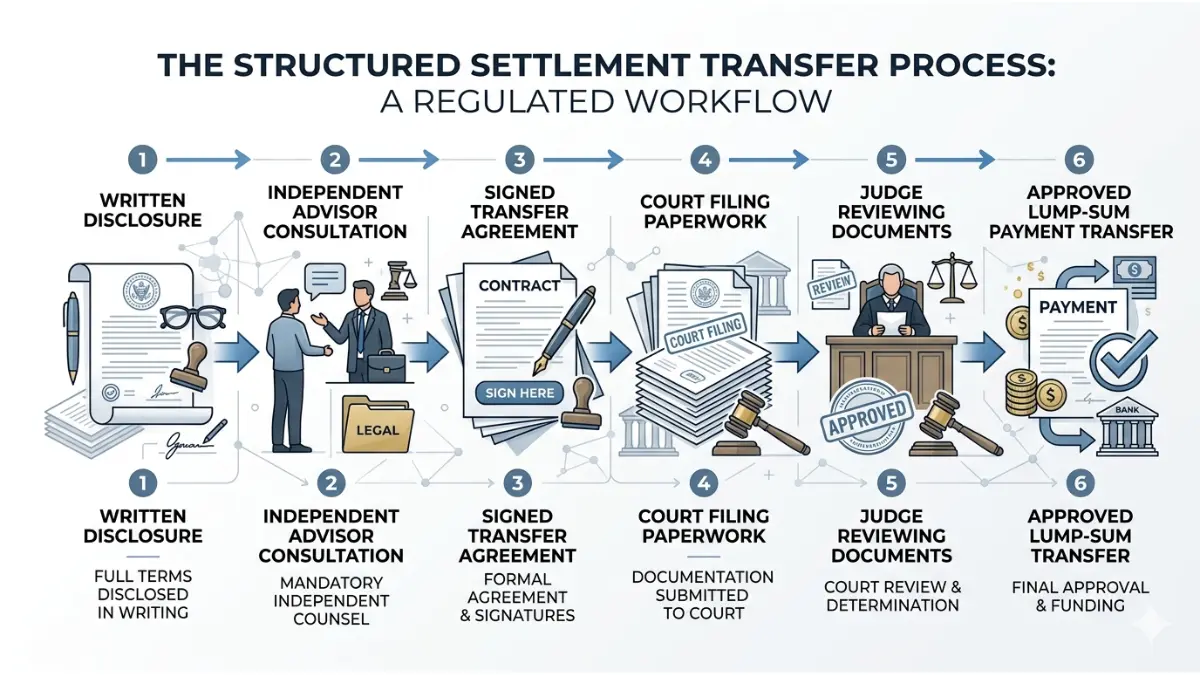

How a structured settlement buyout actually works — and where fraud enters

A structured settlement buyout follows a defined legal sequence. Knowing the legitimate process is the only way to recognize when a buyer is deviating from it.

The six steps of a legitimate structured settlement transfer

- The buyer provides a written disclosure statement — including the exact discount rate, lump sum, and total payment value — before any agreement is signed.

- The recipient is offered an independent professional advice (IPA) referral to a licensed professional unconnected to the buyer.

- Both parties execute a transfer agreement.

- The buyer files a transfer petition with the applicable court.

- A judge reviews the transfer under the “best interest” standard.

- Court approval is granted before any payment changes hands.

📊 Data Point: As of 2026, 49 states have enacted Structured Settlement Protection Acts (SSPAs) requiring court approval for all structured settlement transfers. Source: NSSTA, 2026 State Law Summary.

Where predatory companies deviate from each step

Predatory buyers compress, skip, or obscure every step above. They present contracts that bury the discount rate. They discourage IPA referrals. They describe court approval as “automatic” or “already arranged.”

Use the inflation calculator to see how the real value of your future payments changes over your remaining term — that figure alone explains why preserving those payments matters. The CFPB’s structured settlement consumer guidance specifies what disclosures a factoring company must provide before any agreement is signed.

The 9 red flags in a structured settlement buyout offer

Nine red flags signal predatory intent in a structured settlement buyout offer:

Red flags 1–4: pressure tactics, upfront fees, and rate concealment

1. An expiring offer with a specific deadline. Legitimate buyers do not manufacture urgency. Any 24-, 48-, or 72-hour deadline is a pressure tactic — not a market constraint.

2. Refusal to disclose the effective APR. Every SSPA-compliant buyer must disclose the discount rate in writing before signing. A buyer providing only a lump-sum figure is concealing the true cost. Use the APR calculator to find the effective annual rate on any buyout offer before reading any other contract term.

3. Any upfront fee requested before a court petition is filed. No compliant transfer requires payment from the recipient before court approval. Any such fee — processing, application, or escrow — is disqualifying.

4. Discount rate presented only as a percentage of total payments. Framing an offer as “90 cents on the dollar” hides the effective APR, which may be far higher when adjusted for payment timeline.

Red flags 5–9: legal evasion, licensing gaps, and document fraud

5. Any claim that court approval is optional or pre-arranged. In 49 states, a judge must review every structured settlement transfer. No exceptions exist for urgency or buyer preference.

6. The buyer cannot produce a state license number. All factoring companies operating legally in 2026 must hold active state licensing. A legitimate buyer provides this number immediately on request.

7. No written disclosure statement offered before signing. SSPA law in most states requires written disclosure at least 3 business days before agreement execution. Absence is a statutory violation.

8. Discouragement of your consulting an attorney or financial advisor. A compliant buyer is required to offer IPA access — not undermine it. Any buyer who pushes back on your seeking counsel benefits when you remain uninformed.

9. A turnaround promised in under two weeks. A legitimate transfer takes 45–90 days in 2026. A sub-two-week close almost certainly bypasses required legal process.

⚠️ Warning: Red Flag 5 — a claimed exemption from court approval — is the most legally dangerous claim in this list. Stop the conversation and file a CFPB report before responding further.

💡 Expert Note (CFA): Red Flag 2 costs recipients the most money. Buyers advertising “90 cents on the dollar” frequently imply effective APRs of 18%–24% when adjusted for payment duration. Calculate the annualized rate before reading any other contract term. The SEC’s investor alert on structured settlement fraud documents these rate concealment patterns directly.

How to evaluate a structured settlement offer before you sign

Four steps to evaluate any structured settlement offer before responding:

The four-step offer evaluation process

Step 1 — Verify buyer licensing. Request the state-specific license number and cross-reference it against your state insurance commissioner’s database before sharing any documentation.

Step 2 — Calculate the implied discount rate. Divide the offered lump sum by total remaining payment value. A result below 0.83 (83 cents on the dollar) indicates an elevated-rate offer — request written justification before proceeding.

Step 3 — Request all SSPA-required disclosures. The written disclosure statement must be provided at least 3 business days before signing in most states. No document — no deal.

Step 4 — Consult a licensed financial professional. A CFP or CFA can calculate the true present value of your stream, verify the discount rate against 2026 benchmarks, and identify alternatives that address your cash need without a permanent transfer.

💡 Expert Note (CFA): Before any client of mine proceeded past Step 2, I required a full present-value analysis. In more than half of those cases, it revealed an alternative — a personal loan, partial sale, or hardship arrangement — that solved the immediate need without permanently transferring the full stream.

When to walk away — and what to do immediately after

Walk away if the buyer fails any step above or pressures you to skip consultation. Compare options using a structured settlement vs. lump sum analysis before deciding. Run the savings calculator to project what keeping your payments is worth and the income tax calculator to estimate any lump-sum tax exposure before Step 4.

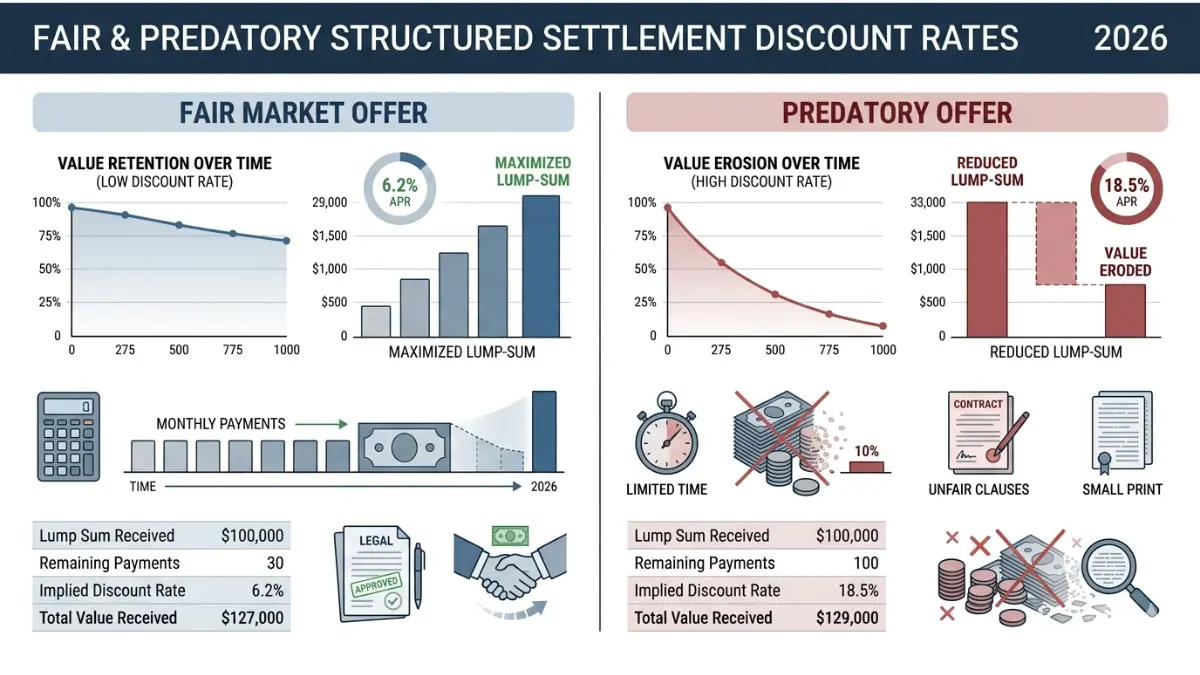

What a fair structured settlement discount rate looks like in 2026

A fair structured settlement discount rate in 2026 falls between 9% and 15% for most transaction sizes, depending on remaining payment duration and state of residence.

2026 discount rate benchmarks: fair, elevated, and predatory ranges

| Settlement Size | Fair Rate Range | Elevated (Negotiate) | Predatory Threshold |

|---|---|---|---|

| Under $50,000 | 9%–13% | 14%–17% | 18%+ |

| $50,000–$150,000 | 9%–12% | 13%–16% | 17%+ |

| $150,000–$400,000 | 8%–11% | 12%–15% | 16%+ |

| Over $400,000 | 7%–10% | 11%–14% | 15%+ |

Source: NSSTA 2026 Market Rate Survey; CFPB consumer guidance. Verify directly with NSSTA before any transaction.

📊 Data Point: The median effective discount rate on completed structured settlement transfers tracked by NSSTA in 2026 was 11.4%. Offers above 17% fall outside fair-market range for most settlement sizes. Source: NSSTA, 2026 Annual Industry Report.

What an 8-point rate difference costs you in real dollars

Consider a settlement paying $2,000 per month for 10 years — $240,000 total remaining value.

At a 10% effective annual discount rate, the fair lump-sum value is approximately $151,300.

At 18%, that offer drops to approximately $111,100 — a gap of $40,200 on a single transaction.

Use the investment calculator to model your payment stream’s present value with your specific figures. The table above is your benchmark — read how discount rates affect your structured settlement payout and what selling your structured settlement payments actually costs for the complete picture.

How to verify your buyer and know your legal rights before signing

Three regulatory databases confirm or disqualify a structured settlement buyer in 2026.

The three databases that confirm or disqualify a buyer

| Step | Database | What to Search | Red Flag If Missing |

|---|---|---|---|

| 1 | State Insurance Commissioner | Buyer’s company name | No active license on file |

| 2 | FINRA BrokerCheck | Buyer’s company name | No registration, or prior disciplinary actions |

| 3 | SEC EDGAR | Buyer’s company name | No registration found |

Run all three checks before sharing any documentation. Verify through FINRA’s BrokerCheck database and the SEC’s EDGAR company database — both are free and take under five minutes.

Your rights under the Structured Settlement Protection Act

The Structured Settlement Protection Act grants you the right to a written disclosure before signing, the right to independent professional advice, the right to court review under the “best interest” standard, and the right to rescind during the statutory cooling-off period.

⚠️ Warning: Any buyer who discourages your reading the SSPA disclosure or consulting your own professional is violating state law in most jurisdictions. That behavior alone is sufficient reason to disengage.

Read the court approval process for structured settlement transfers and review how to evaluate structured settlement companies before engaging any factoring firm.

Three steps to take before you respond to any buyout offer

You now have the framework: nine red flags with 2026 benchmarks, a four-step evaluation process, and a three-database verification workflow.

Your action plan starts before you reply

Step 1 — Run the 9-red-flag checklist against the offer. Any single disqualifying flag is sufficient reason to pause.

Step 2 — Verify the buyer’s licensing across all three databases before sharing documentation.

Step 3 — Consult a licensed financial professional. The court process protects you — but only if you reach it.

✅ Pro Tip: Request all buyer communications in writing. A legitimate company agrees immediately. A predatory one pushes back — that response is its own disqualifying signal.

The recipients who avoid the worst outcomes share one characteristic: they slowed down when the buyer manufactured urgency. Understand how structured settlement payments are taxed as part of your complete evaluation. If you believe you have encountered a structured settlement scam, file a report at consumerfinance.gov/complaint — it routes directly to state and federal enforcement agencies.

Structured settlement scams: answers to your most important questions

1. What is a structured settlement buyout?

A structured settlement buyout is a transaction in which a factoring company purchases your right to receive future periodic payments in exchange for an immediate lump sum. The lump sum is always less than the total payment value — the difference is the buyer’s profit, expressed as a discount rate applied to your remaining payment stream.

2. Can a scam actually cause you to lose your structured settlement?

Yes. Fraudulent structured settlement buyers have intercepted payment streams using improperly executed assignment documents. Without completed court approval under your state’s SSPA, a transfer is legally void in most states — but recovering misdirected funds typically requires costly, time-consuming litigation.

3. What discount rate is too high for a structured settlement in 2026?

A structured settlement discount rate above 17% is elevated for most settlement sizes in 2026; above 20%, it falls into predatory territory by NSSTA benchmarks. For settlements over $150,000, fair-market rates typically run 8%–12%. Rates above those thresholds warrant written justification and independent professional review before any further negotiation.

4. How do I know if a structured settlement buyer is legitimate?

A legitimate structured settlement buyer provides a written disclosure statement, files a court transfer petition, offers an IPA referral, and can confirm active state licensing immediately. Cross-reference the company through your state insurance commissioner, FINRA BrokerCheck, and SEC EDGAR before providing any personal or financial documentation.

5. Are structured settlement buyers required to have a license?

Yes. Structured settlement factoring companies must hold active state licenses in jurisdictions where they solicit in 2026. Operating without a license violates both state consumer protection law and SSPA compliance requirements. Ask for the license number before sharing documentation — a legitimate buyer provides it without hesitation.

6. What is the Structured Settlement Protection Act?

The Structured Settlement Protection Act (SSPA) is a state statute — enacted in 49 states — requiring court approval before a structured settlement can be transferred. A judge applies a “best interest” standard to verify the transfer serves the recipient’s needs. It is the primary legal protection settlement recipients have against predatory buyers.

7. Can a factoring company take your payments without court approval?

No. In 49 states, a structured settlement transfer without court approval under the applicable SSPA is legally invalid in most circumstances. Any buyer claiming court approval is unnecessary is either misinformed or misrepresenting the legal requirements. Verify your state’s specific SSPA requirements independently before proceeding.

8. How long does a legitimate structured settlement transfer take in 2026?

A compliant structured settlement transfer takes 45–90 days in 2026, from signed agreement to court-approved completion. The timeline includes statutory disclosure periods, court filing, hearing scheduling, and order issuance. Any buyer promising completion in under two weeks is almost certainly bypassing one or more legally required steps.

9. What fees should you expect when selling a structured settlement?

In 2026, compliant structured settlement buyers embed all costs within the discount rate — no separate upfront fee is charged before court approval. Any buyer requesting a processing fee, application fee, or escrow deposit before a court petition is filed is operating outside SSPA compliance standards.

10. Should you consult a financial advisor before selling a structured settlement?

Yes. A licensed CFA or CFP can calculate the present value of your structured settlement stream, verify whether the offered discount rate falls within 2026 fair-market ranges, and identify alternative solutions that may address your immediate need without permanently transferring your income stream.

11. How do you report a structured settlement scam?

File a complaint through the CFPB’s online portal — it routes reports to state and federal regulators. Also notify your state attorney general’s consumer protection division and your state insurance commissioner. Document all buyer communications — emails, texts, contract drafts, and verbal claims about court approval — before filing.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.