How Medicaid Counts Your Structured Settlement in 2026

Structured settlement Medicaid rules work against you the moment a lump sum arrives — CMS’s 2026 $2,000 asset limit can suspend coverage that same day.

In This Article

Why your structured settlement and Medicaid are on a collision course

A $90,000 lump sum deposited on a Thursday can end your Medicaid coverage by Friday.

That is not a hypothetical.

It is the financial reality for thousands of structured settlement recipients every year — people who accepted a factoring company’s buyout offer without understanding what happens to their Medicaid eligibility the moment those funds arrive in their account.

The offer that could cost you your health coverage

Factoring companies profit by purchasing your future payment stream at a steep discount to its present value.

What they rarely disclose — because they have no financial incentive to — is that the lump sum they offer may instantly push your total assets above the threshold that keeps you enrolled in Medicaid.

What this article will tell you that most sites won’t

This article breaks down exactly how Medicaid counts settlement proceeds in 2026, what the income and asset thresholds are by program type, and which legal tools can protect your benefits before you sign anything.

You will leave with a step-by-step disqualification sequence, a protection strategy comparison table, and the single most important action to take before responding to any buyout offer.

ℹ️ Disclaimer: The structured settlement and Medicaid information in this article is intended for educational purposes only. The sale of structured settlement payment rights is a regulated financial transaction subject to your state’s Structured Settlement Protection Act and requires court approval in 49 states as of 2026. Medicaid eligibility rules — including income thresholds, asset limits, look-back periods, and estate recovery provisions — are administered by the Centers for Medicare & Medicaid Services and vary by state and program type. Before making any decision to sell or transfer structured settlement payment rights, consult a licensed special needs attorney and a licensed financial advisor with experience in Medicaid benefit planning.

How Medicaid counts money — and why it treats your settlement differently

Under Medicaid’s means-tested benefits framework, the classification of your money — income or asset — determines whether your benefits survive contact with a structured settlement.

This distinction is not subtle. The financial consequences are not either.

The difference between income and assets under Medicaid rules

Countable income is money received in a calendar month, measured against your program’s monthly income limit.

Countable assets — also called resources — are what Medicaid measures to determine whether your total holdings, on any given day, exceed the program’s resource limit.

💡 Expert Note (CFA): The most consequential mistake I see clients make is assuming the IRS exclusion for personal physical injury settlement payments — available under IRC Section 104(a)(2) — also shields them from Medicaid’s means test. It does not. The IRS and Medicaid operate under entirely separate legal frameworks. Settlement income excluded from your federal tax return can still be counted as a Medicaid resource the moment it enters your account. The IRS provides additional guidance on disability-related tax rules in Publication 907 for persons with disabilities — read it alongside your Medicaid program rules, not instead of them.

Where a structured settlement lands in Medicaid’s classification system

| Settlement Type | Medicaid Classification | Counted When | Test Applied |

|---|---|---|---|

| Ongoing periodic payments (personal injury) | Income — most programs | Month received | Monthly income threshold |

| Lump sum from selling settlement | Countable asset | Day funds received | Resource limit |

| Settlement held in qualifying special needs trust | Excluded resource | Not counted | N/A |

Ongoing periodic payments from a structured settlement are excluded from MAGI-based Medicaid’s income calculation — but may count as unearned income under SSI-linked Medicaid in the month they are received.

Use the Social Security income estimator to model your SSI-linked benefit picture if both programs apply to you — SSI-linked Medicaid enforces the strictest income and asset rules of any program type.

The 2026 income and asset thresholds that determine your Medicaid risk

The threshold that determines your Medicaid eligibility is specific, measurable, and in most states, unchanged for more than three decades.

Knowing exactly where it sits — before you negotiate with a factoring company — is what separates a protected decision from an irreversible one.

Standard Medicaid vs. LTSS Medicaid: two different income tests

MAGI-based Medicaid (ACA expansion) applies an income-only test with no asset limit.

LTSS Medicaid — which covers long-term services and supports including nursing home care — applies both an income test and a $2,000 resource limit, with a 60-month look-back period for asset transfers.

Conflating these two programs is the most common structural error on competitor sites — and the confusion leads readers to the wrong answer at exactly the wrong moment.

| Medicaid Program | Income Test Basis | 2026 Income Limit (Individual) | Asset/Resource Limit | Look-Back Period |

|---|---|---|---|---|

| ACA Expansion (MAGI-based) | Modified Adjusted Gross Income | ~$21,600/year (138% of 2026 FPL) | None | None |

| SSI-Linked Medicaid | SSI eligibility rules | ~$991/month (2026 SSI federal benefit rate) | $2,000 | None |

| LTSS / Long-Term Care Medicaid | State-determined | State-specific | $2,000 (most states) | 60 months |

Source: Centers for Medicare & Medicaid Services, 2026. State-specific thresholds vary — verify directly with your state Medicaid agency before any financial decision.

📊 Data Point: The individual resource limit of $2,000 for SSI-linked and LTSS Medicaid has been the federal standard since 1989, per CMS policy guidance. As of 2026, most states continue to apply this threshold without adjustment. Source: Centers for Medicare & Medicaid Services, 2026.

The $2,000 line: how Medicaid’s resource limit works in 2026

The $2,000 resource limit means any lump sum — including proceeds from selling a structured settlement — that pushes total countable assets above $2,000 triggers Medicaid disqualification on the day those funds are received.

There is no grace period.

Use the income tax calculator to calculate your after-tax net proceeds from any proposed settlement sale — then compare that figure against the $2,000 threshold using the paycheck calculator to map your monthly income position against your program’s 2026 limit.

The salary calculator is useful if your structured settlement payments are replacing lost wages — understanding your annualized income picture clarifies which Medicaid program type most likely applies to you.

💡 Expert Note (CFA): The IRS publishes clear guidance on the taxability of personal injury settlements in Publication 4345. Run that analysis in full — then separately run your state Medicaid agency’s countability rules. These are two parallel calculations that require two different professional reviews, and conflating them is what costs recipients their benefits.

The moment you sell — exactly how Medicaid disqualification happens

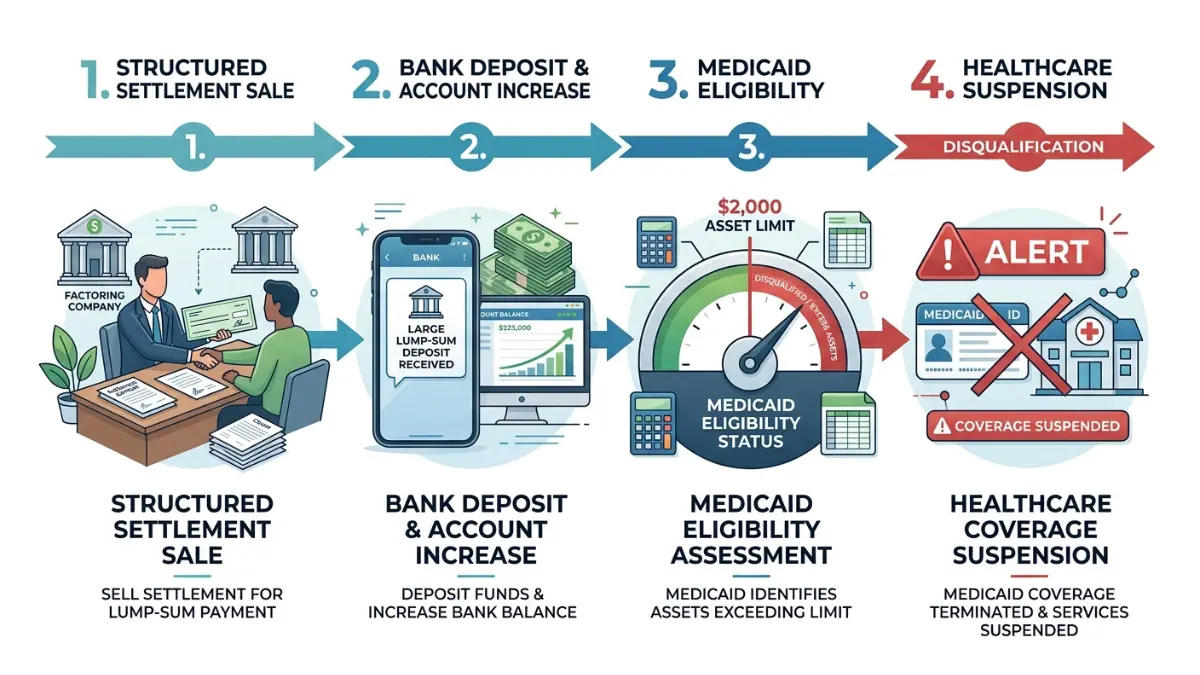

Medicaid disqualification after selling a structured settlement follows a precise, documented sequence.

Understanding it before the factoring company’s offer expires is the financial difference between a protected transaction and an irreversible loss of healthcare coverage.

Day one: how a lump sum becomes a Medicaid-ending asset

A structured settlement factoring transaction works like this: the factoring company deposits a discounted lump sum today in exchange for your future payment rights.

The instant those funds arrive in any account you own — checking, savings, or otherwise — they become a countable asset for Medicaid purposes.

⚠️ Warning: If the lump sum, combined with your existing countable assets, exceeds $2,000 on any single day, Medicaid can suspend your coverage immediately. This disqualification does not wait for your next eligibility review — it can take effect the same day funds are received, with no cure window under standard or SSI-linked Medicaid.

Use the take-home pay calculator to determine your actual net receipt after any applicable withholding, then compare that figure directly against your program’s current $2,000 resource threshold.

How long you could lose coverage — and what determines the penalty period

For LTSS Medicaid, the consequence is not just disqualification — it is a calculated penalty period that can run for months or years.

The penalty period is determined by dividing the total transferred asset value by your state’s average monthly nursing home cost — a calculation the factoring company will never volunteer.

💡 Expert Note (CFA): A client came to me after accepting a $92,000 structured settlement buyout offer. Their state’s average monthly nursing home cost was $8,400. The resulting LTSS Medicaid penalty period was 10.95 months — nearly 11 months during which Medicaid paid nothing toward their long-term care. The factoring company’s representative had described the transaction as straightforward. No one on the other side of the table had modeled the penalty calculation.

📊 Data Point: The look-back period for LTSS Medicaid is 60 months (five years) under federal law at 42 U.S.C. § 1396p. Any transfer of a structured settlement for less than fair market value within this window before applying for LTSS Medicaid can trigger a penalty period. Source: Centers for Medicare & Medicaid Services, 2026.

How to keep Medicaid when you have a structured settlement

Three legal tools allow structured settlement recipients to maintain Medicaid eligibility.

None requires giving up the settlement money. All require professional oversight to execute without error.

First-party special needs trust: the most powerful Medicaid protection tool

A first-party special needs trust — also called a self-settled (d)(4)(A) trust — holds settlement funds in a structure that Medicaid does not count as a resource.

The trust must be irrevocable, established for the benefit of an individual with a disability under age 65, and must include a Medicaid payback provision.

💡 Expert Note (CFA): The Medicaid payback provision is the detail most blogs on this topic omit — and it is the most financially consequential provision in the entire trust structure. Upon the beneficiary’s death, the state must be reimbursed for all Medicaid benefits paid during the beneficiary’s lifetime before any remaining trust assets pass to other heirs. Clients who understand this before the trust is established can plan around it — including modeling whether a life insurance policy naming non-Medicaid beneficiaries makes sense alongside the trust to offset the payback obligation.

Consult a licensed special needs attorney to draft the trust — a structural drafting error can cause the trust to be counted as a Medicaid resource retroactively, triggering disqualification after the fact.

Use the compound interest calculator to project trust asset growth if the settlement funds will be invested inside the trust vehicle over a multi-year horizon.

ABLE accounts: the 2026 contribution limit and who qualifies

An ABLE account allows individuals with qualifying disabilities to contribute up to $19,000 in 2026 — the IRS annual contribution limit tied to the gift tax exclusion — without those funds counting against Medicaid’s resource limit.

One hard eligibility requirement applies: disability onset must have occurred before age 26.

📊 Data Point: The 2026 ABLE account annual contribution limit is $19,000 per beneficiary, per IRS guidance on ABLE accounts. Funds contributed above this limit may be counted as a Medicaid resource in the month of contribution. Source: Internal Revenue Service, 2026. Verify current limits before contributing.

Use the savings calculator to project ABLE account growth over five to ten years, and the investment calculator if your ABLE account will hold market-based assets with variable growth rates.

Structured spend-down: a strategy with a narrow window

A Medicaid spend-down involves spending excess lump sum assets on Medicaid-exempt categories — medical equipment, home modifications, prepaid funeral arrangements, certain education expenses — within the same calendar month the funds are received.

This strategy is legal. It is also unforgiving of timing errors.

✅ Pro Tip: Before any factoring transaction closes, contact your state Medicaid agency and request a written list of exempt spend-down categories for your specific program type. This list varies by state and determines exactly what purchases will not trigger disqualification. Obtain this list in writing before funds arrive.

Map your compliant monthly spend plan against the lump sum amount using the budget calculator — and execute the full plan before the last day of the calendar month in which the funds arrive.

The legal process every structured settlement sale must go through

Selling a structured settlement is not a private financial transaction.

It is a court-supervised proceeding — and the court holds both the authority and the obligation to determine whether the sale serves your best interests before it can proceed.

Why a judge must approve your structured settlement sale

The Structured Settlement Protection Act — enacted in some form in 49 states as of 2026 — requires that any transfer of structured settlement payment rights receive a court order before the transaction closes.

The court must find the sale is in the payee’s best interest, a determination that explicitly includes evaluating the impact on government benefit eligibility.

⚠️ Warning: Court approval does not protect your Medicaid. A judge can approve a transaction as legally compliant while Medicaid disqualification still takes effect the day the lump sum is deposited. Raising your Medicaid situation at the court hearing — with written documentation from your state Medicaid agency and a written benefit impact analysis from a licensed financial advisor — is your right and your responsibility.

The CFPB provides consumer rights guidance covering disclosure requirements that apply when selling a structured settlement, including mandatory waiting periods factoring companies must honor before any transaction can proceed.

Medicaid estate recovery: can the state claim your settlement after you die?

Medicaid estate recovery — required by federal law under 42 U.S.C. § 1396p — directs states to seek reimbursement from a deceased LTSS Medicaid beneficiary’s estate for long-term care benefits paid during their lifetime.

If structured settlement proceeds — or a trust holding them — are considered part of your estate under your state’s law, the state may file a reimbursement claim after your death.

Recovery scope varies significantly by state, and the interaction between trust payback provisions and estate recovery rules requires state-specific legal analysis.

Use the life insurance calculator to model whether a policy naming non-Medicaid beneficiaries makes financial sense alongside a special needs trust — particularly if estate recovery exposure is a concern in your state’s program.

Your next step before signing anything

The lump sum offer on the table has an expiration date.

The Medicaid disqualification it can trigger does not.

The three questions to answer before you accept any buyout offer

Answer these three questions before responding to any factoring company:

- Which Medicaid program type are you enrolled in — MAGI-based, SSI-linked, or LTSS? Contact your state Medicaid agency and get your 2026 resource limit and income limit in writing before you respond to any offer.

- Has a licensed special needs attorney reviewed the transaction for benefit impact? Not a general practice attorney — a disability planning specialist who knows your state’s current Medicaid rules.

- Can the entire lump sum be protected — through a first-party special needs trust, ABLE account, or spend-down plan — so that no portion of the funds appears in your countable resource total on the day they are received?

Use the retirement calculator to model the long-term value of keeping your structured settlement payment stream versus accepting the factoring company’s discounted lump sum — in many cases, the present value of the full payment stream significantly exceeds the offer on the table.

A licensed financial advisor who specializes in benefit-protected finances can run this comparison against your actual numbers before any decision is made.

Structured settlement and Medicaid: your questions answered

1. Does a structured settlement affect Medicaid eligibility?

A structured settlement affects Medicaid eligibility differently depending on your program type. MAGI-based Medicaid (ACA expansion) generally excludes periodic payments from its income test. SSI-linked and LTSS Medicaid apply both income and asset tests that may count settlement payments or a lump sum. Before any financial decision, consult a licensed special needs attorney or financial advisor with Medicaid benefit experience.

2. Are structured settlement payments counted as income for Medicaid?

Ongoing structured settlement payments from a personal physical injury settlement are generally excluded from MAGI-based Medicaid income under IRC Section 104(a)(2). For SSI-linked Medicaid, periodic payments may count as unearned income in the month received — tested against the 2026 SSI federal benefit rate of approximately $991 per month. Consult a licensed special needs attorney or financial advisor for your program-specific rules.

3. Can I sell my structured settlement if I’m currently on Medicaid?

Selling a structured settlement while on Medicaid is legally permitted — but the lump sum you receive may trigger immediate disqualification. If countable assets exceed $2,000 on the day funds arrive, Medicaid can suspend coverage that same day. A special needs trust, ABLE account, or spend-down plan may protect eligibility. Consult a licensed special needs attorney before signing any factoring agreement.

4. What happens to my Medicaid the day I receive a lump sum settlement?

The lump sum is classified as a countable asset on the day it is deposited. If that deposit pushes total resources above the 2026 Medicaid resource limit of $2,000 for SSI-linked and LTSS programs, coverage can be suspended immediately. For LTSS Medicaid, a penalty period is also calculated and applied. Consult a licensed special needs attorney or financial advisor before making any decision.

5. Is there a look-back period for structured settlements and Medicaid?

A 60-month look-back period applies to LTSS Medicaid only — not to standard MAGI-based Medicaid. Selling a structured settlement for less than fair market value within this 60-month window before applying for LTSS Medicaid can trigger a calculated penalty period. The penalty length is determined by dividing the transfer amount by your state’s average monthly nursing home cost. Consult a licensed special needs attorney before taking action.

6. What is the Medicaid asset limit in 2026?

For SSI-linked and LTSS Medicaid, the 2026 individual resource limit is $2,000 in countable assets in most states — a federal standard unchanged since 1989. MAGI-based Medicaid has no asset limit; only income is tested. Some states have enacted higher limits. Verify your state’s 2026 specific threshold directly with your state Medicaid agency before any financial transaction.

7. Can a special needs trust protect my Medicaid eligibility?

A first-party special needs trust holds settlement funds in a structure Medicaid does not count as a resource. It must be irrevocable, established for a beneficiary with a disability under age 65, and must contain a Medicaid payback provision. Improperly drafted trusts can be counted as resources retroactively. An attorney specializing in special needs planning must review and draft any trust document to ensure compliance.

8. Do I need court approval to sell my structured settlement?

Yes. Under the Structured Settlement Protection Act, enacted in 49 states as of 2026, any transfer of structured settlement payment rights requires a court order finding the sale is in your best interest. Medicaid benefit impact is a valid best-interest factor you can raise at the hearing. Court approval alone does not protect your Medicaid coverage. Consult a licensed special needs attorney before proceeding.

9. What is a structured settlement factoring transaction?

A structured settlement factoring transaction is the sale of future payment rights to a third-party buyer — a factoring company — in exchange for a lump sum at a discount to the full present value of the payment stream. The factoring company profits on that discount. The transaction requires court approval in most states and creates immediate asset implications for Medicaid eligibility on the day funds are received.

10. Can Medicaid recover money from my structured settlement after I die?

Federal law requires states to pursue reimbursement from a deceased Medicaid beneficiary’s estate for long-term care benefits paid. If structured settlement proceeds — or a trust holding them — are considered part of your estate under your state’s law, the state may file a recovery claim after your death. Recovery scope varies significantly by state. Consult a licensed special needs attorney to understand your state-specific estate recovery exposure.

11. What should I do before selling my structured settlement if I have Medicaid?

Before selling a structured settlement while on Medicaid: confirm your program type and 2026 resource limit in writing from your state Medicaid agency; retain a licensed special needs attorney to assess the transaction’s benefit impact before any agreement is signed; and do not accept the lump sum until a financial advisor has modeled the full asset position against your current Medicaid threshold.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.