The Real Tax Rules for Wrongful Death Structured Settlements

A wrongful death structured settlement guarantees family income for decades — but punitive damages and COLA terms determine the real payout value.

In This Article

What families need to know about wrongful death settlement payments

When a wrongful death lawsuit ends in a settlement, the total compensation figure is almost never delivered as a single payment.

A wrongful death structured settlement is a configured financial instrument — funded by an annuity contract and governed by federal tax law — that converts the award into a stream of periodic payments over months, years, or a lifetime.

Why the payment structure matters as much as the total award

The total settlement figure captures attention at the negotiating table.

The payment structure — duration, inflation protection, beneficiary designation — determines how much the family actually receives and what that income is worth after a decade of price erosion.

What this guide covers — and who should read it before signing

This guide is written for families who have received a settlement offer and need to understand the financial instrument before agreeing to its terms.

Before evaluating any offer, understanding how structured settlements work as a financial product is the most consequential preparation step available — and the one most families skip entirely.

ℹ️ Disclaimer: The structured settlement and annuity information in this article is provided for educational purposes only. Wrongful death structured settlements are regulated insurance and financial instruments; tax treatment under IRC §104(a)(2), payment terms, and consumer protections vary by case-specific facts, state law, and the provisions of each individual settlement agreement. Consult a licensed financial advisor, a CPA with settlement experience, and independent legal counsel before accepting, modifying, or selling any wrongful death structured settlement.

What a wrongful death structured settlement actually is

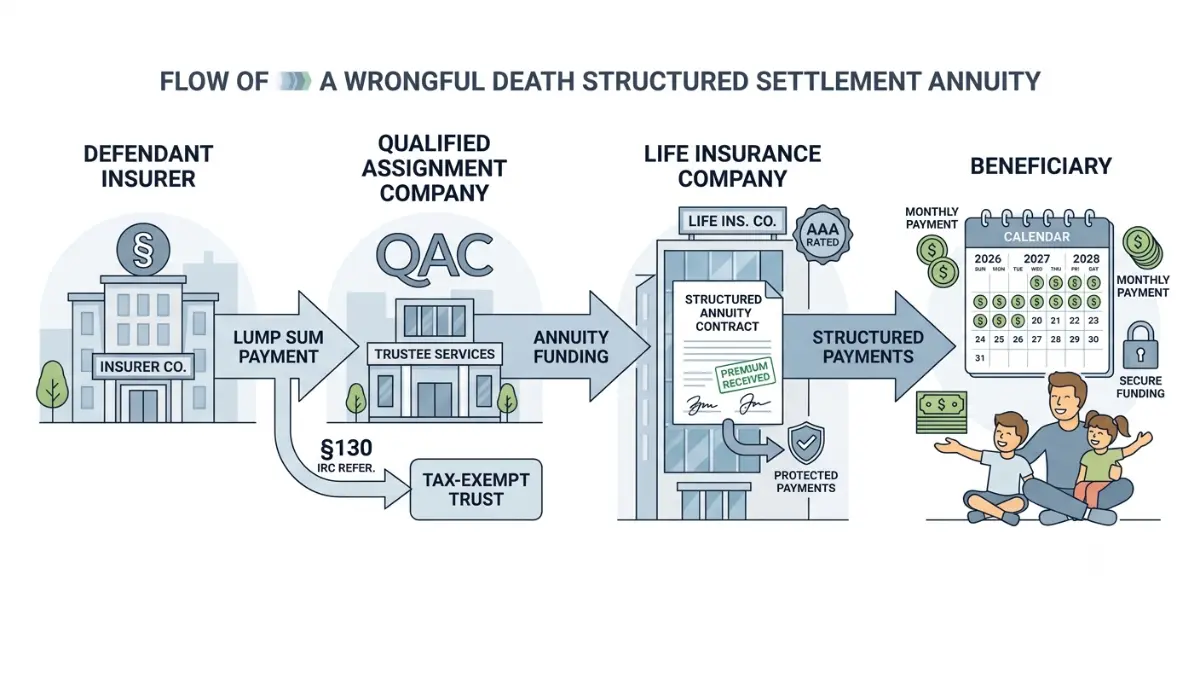

A wrongful death structured settlement is a legally binding financial arrangement in which the defendant’s insurer funds periodic payments to the surviving beneficiary through an annuity contract issued by a licensed life insurance company — rather than writing a single check.

The agreement specifies the full payment schedule: amount, frequency, duration, escalation provisions, and beneficiary designation.

How the annuity mechanism works — who issues it and who guarantees it

The payment obligation does not stay with the defendant or their insurer indefinitely.

Under IRC §130, the defendant’s insurer typically transfers that obligation — via a qualified assignment — to a specialized assignment company, which purchases an annuity from a licensed life insurer to fund every future payment.

💡 Expert Note (CFA): Once the qualified assignment is executed, the life insurance company — not the defendant, not their carrier — becomes the guarantor of every payment. Life insurers issuing structured settlement annuities are regulated under state insurance law and typically carry state guaranty fund protections. Before signing, confirm the financial strength rating of the specific annuity issuer named in the contract. For a foundational explanation of how annuities function as long-term payment instruments, that resource covers the core mechanics in accessible terms.

The difference between the settlement award and the structured settlement contract

The settlement award is the total compensation both parties agreed to.

The structured settlement contract is the separate annuity document that determines when and how that award is paid — it deserves independent financial review before signature, the same way any multi-decade insurance contract would.

Families should also evaluate which structured settlement companies have the strongest payment reliability records when assessing the insurer named in their specific offer.

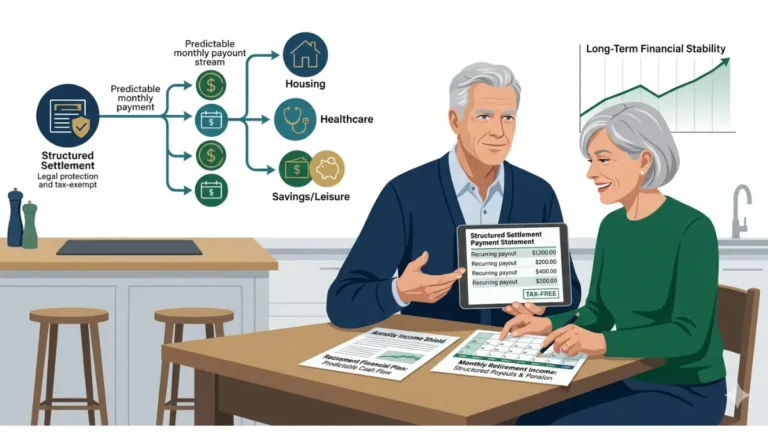

How wrongful death settlement payment schedules are structured

Wrongful death structured settlements can be configured to pay over several time frames, depending on the beneficiary’s age, financial needs, and negotiated terms — and the schedule is not set by the insurer alone.

Every element described below is negotiable before the contract is signed.

Payment duration options: fixed period, lifetime, and hybrid structures

The three primary structures available in a wrongful death structured settlement are:

- Fixed-period payments: Payments run for a defined term — commonly 10, 20, or 30 years — regardless of whether the beneficiary is alive for the full period. If the beneficiary dies early, remaining payments continue to a named heir or estate.

- Lifetime annuity payments: Payments continue for the beneficiary’s life, priced actuarially on age and life expectancy at settlement. A guaranteed minimum period — typically 10 or 20 years — is commonly negotiated to protect the estate if the beneficiary dies early in the payout window.

- Hybrid structures: An upfront lump-sum front load covers immediate expenses, followed by smaller periodic payments — used when near-term housing, medical, or education costs require immediate liquidity.

For context on how life insurers price these payout options, the SEC’s investor education resource on annuities explains the underlying pricing mechanics from a regulatory standpoint.

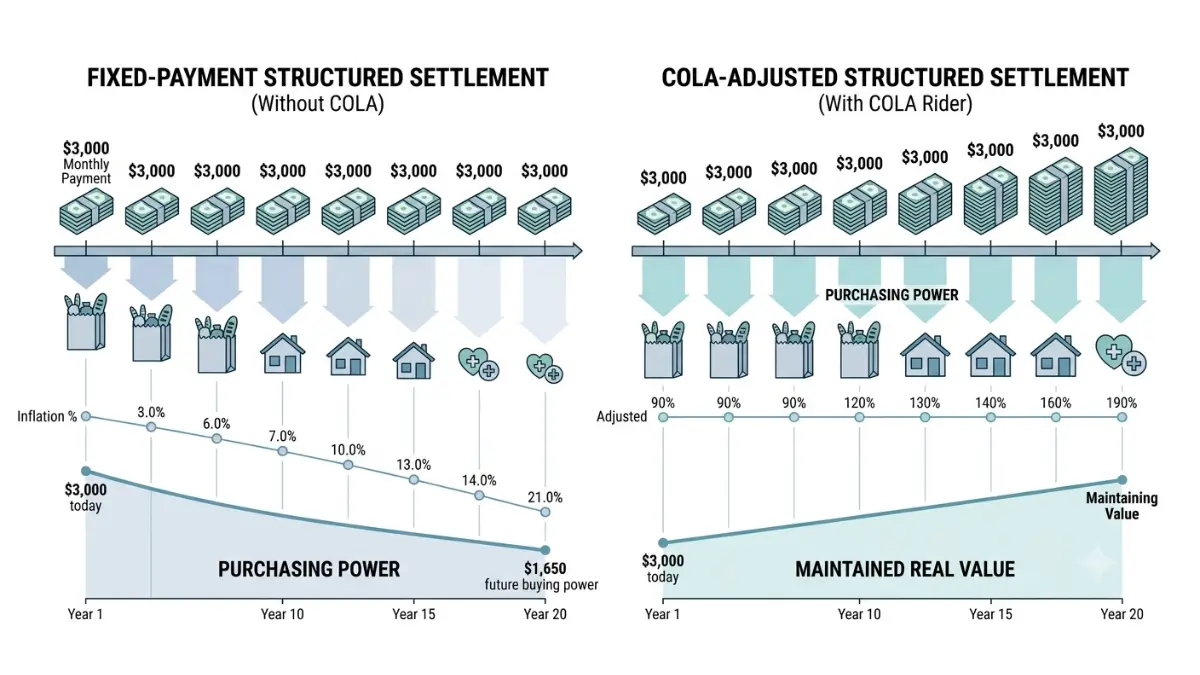

COLA riders and purchasing power over long payout windows

A cost-of-living adjustment (COLA) rider increases each structured settlement payment by a fixed annual percentage — typically 1%–3% — to offset the compounding effect of inflation over long payout windows.

A flat $3,000 monthly payment in 2026 carries the purchasing power of approximately $2,035 per month by 2046 at 3% annual inflation — a reduction of nearly one-third over 20 years.

💡 Expert Note (CFA): COLA riders are consistently underrepresented in initial settlement offers — not because they’re unavailable, but because they increase the annuity premium the insurer must pay. Families accepting a 20- or 30-year structured settlement without asking about a COLA rider are locking in a permanent, compounding reduction in real income. Run your specific payment amount through the inflation calculator to see exactly what flat payments are worth in purchasing power at your settlement’s duration.

Special considerations when minor children are among the beneficiaries

When minor children are named beneficiaries, most states require court approval of the settlement structure to ensure the payment terms serve the minor’s long-term interests.

Payments for minors are commonly deferred until adulthood, placed in trust, or configured to fund educational milestones at specific ages.

Are wrongful death structured settlement payments tax-free?

Under IRC §104(a)(2), compensation received on account of physical injury or death is generally excluded from federal gross income — meaning most wrongful death structured settlement payments are not subject to income tax.

This exclusion covers both the compensatory principal and the investment earnings the annuity generates over time, provided the settlement qualifies under the statute.

IRC §104 and the physical injury exclusion — what it covers and what it does not

The exclusion applies to compensatory damages — payments that replace lost income, cover medical costs, or compensate the family for loss of support and companionship attributable to the death.

It does not apply to punitive damages, which are awarded to punish the defendant and are explicitly taxable as ordinary income under the same statute.

📊 Data Point: IRS Publication 4345 — Settlements — Taxability (2026 edition) — governs federal tax treatment of structured settlement proceeds and defines the distinction between compensatory and punitive components. Source: IRS Publication 4345, Internal Revenue Service, 2026.

For the complete 2026 statutory framework covering which structured settlement payments are taxable under current IRS rules, that article covers both the exclusion and its exceptions in full detail.

The punitive damages exception — the tax liability most families don’t anticipate

When a wrongful death judgment includes both compensatory damages and punitive damages, only the compensatory portion qualifies for the IRC §104(a)(2) exclusion.

The punitive component is taxable as ordinary income in each year a payment that includes a punitive allocation is received — creating a recurring tax event across the entire settlement duration.

⚠️ Warning: A $200,000 punitive damages component distributed across 20 annual structured settlement payments generates a taxable income event every year. Families who are unaware of this distinction sometimes face unexpected tax bills beginning in year one of their payout. Use the income tax calculator to model the annual tax cost of a punitive allocation at your household income level before signing. For additional IRS guidance on compensation for injuries and physical conditions, the IRS topic covering injury and sickness exclusions explains the underlying statutory framework. (URL requires live verification.)

💡 Expert Note (CFA): The punitive damages tax carve-out is the single most costly misunderstanding I encounter in wrongful death settlement reviews. Ask your plaintiff attorney for a written breakdown of the compensatory versus punitive allocation in the settlement — and have an independent CPA review that allocation before you sign. The IRS does not accept “the attorney said it was all tax-free” as a defense against underreported income.

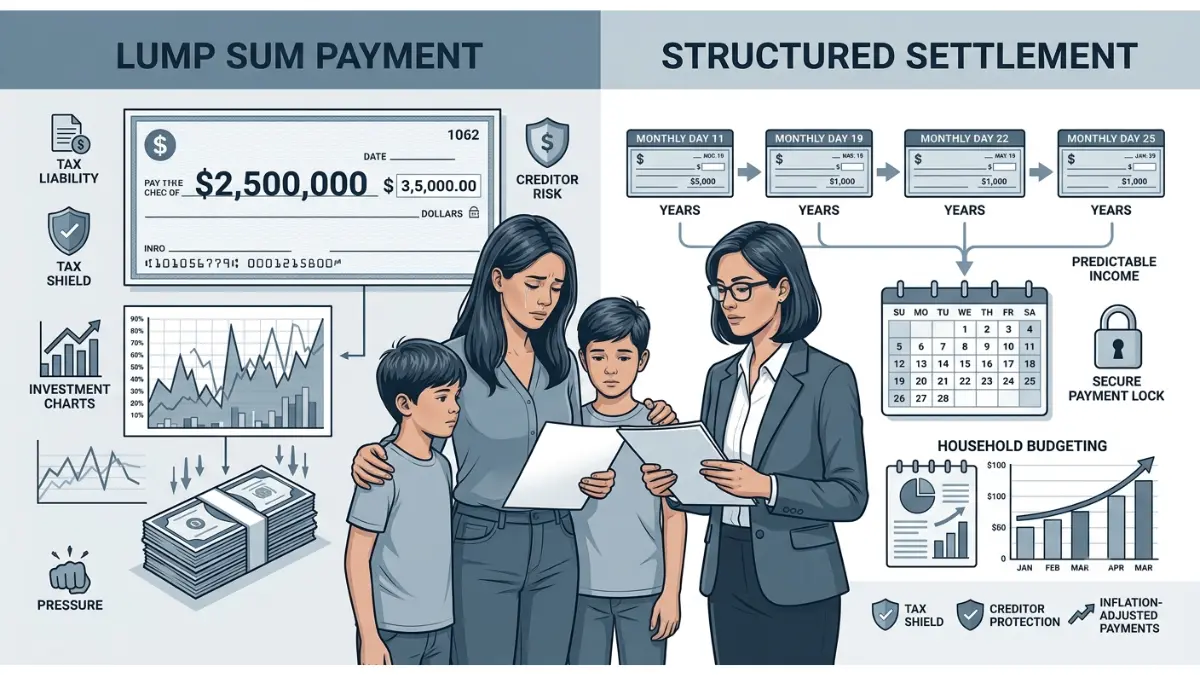

Lump sum vs. structured settlement: which is right for your family?

The choice between a lump sum and a wrongful death structured settlement is not a question of which option is universally superior — it is a diagnostic question about a specific family’s tax situation, investment discipline, income needs, and creditor exposure.

Both can be the right answer.

| Factor | Lump Sum | Structured Settlement | Key Consideration |

|---|---|---|---|

| Federal tax treatment | Investment returns taxable annually | Payments generally excluded under §104 | Structured settlement advantage for most tax brackets |

| Investment risk | Recipient manages full portfolio risk | Life insurer bears investment risk | Lump sum requires active management discipline |

| Creditor protection | Subject to creditors once received | Protected in most states under state law | Structured settlement advantage where creditor exposure exists |

| Inflation protection | Depends entirely on investment returns | Available via negotiated COLA rider | COLA rider negotiation critical for 20+ year payout windows |

| Flexibility | Full access to funds at any time | Payments fixed; selling requires court approval | Lump sum advantage for households needing liquidity |

When a structured settlement is the stronger financial choice

A structured settlement consistently outperforms a lump sum when the beneficiary lacks professional investment management experience, has creditor exposure, needs guaranteed long-term income replacement, or faces a high marginal tax rate on reinvested returns.

Understanding why the structured settlement discount rate affects the real value of any offer is critical context before making this comparison — it determines what the total payment stream is worth in today’s dollars.

When a lump sum may serve the family better

A lump sum may be more appropriate when the beneficiary has demonstrated investment management capability, has tax-advantaged account capacity to shelter reinvested returns, and has minimal creditor exposure.

The investment calculator models what a lump sum grows to at different assumed return rates over the same horizon as the structured payment stream — making the after-tax comparison concrete rather than theoretical.

How to negotiate wrongful death structured settlement terms before signing

The insurer’s initial proposal is a starting point.

Before signing, request: a COLA rider scenario, a guaranteed minimum payment period, a hybrid front-load option, and the compensatory versus punitive allocation in writing — then have the full package reviewed by a fee-only financial advisor with no commission interest in the outcome.

💡 Expert Note (CFA): The comparison most families never run — but should — is the after-tax, after-inflation return on a lump sum versus a COLA-adjusted structured settlement over 20 years. I’ve run this model dozens of times. At the 22%–32% federal tax bracket, the structured settlement wins more often than most families expect because reinvested lump-sum returns are taxed annually while structured settlement payments are not. For a side-by-side analysis with 2026 figures, lump sum vs. structured settlement: which pays more over time covers both scenarios in specific dollar terms.

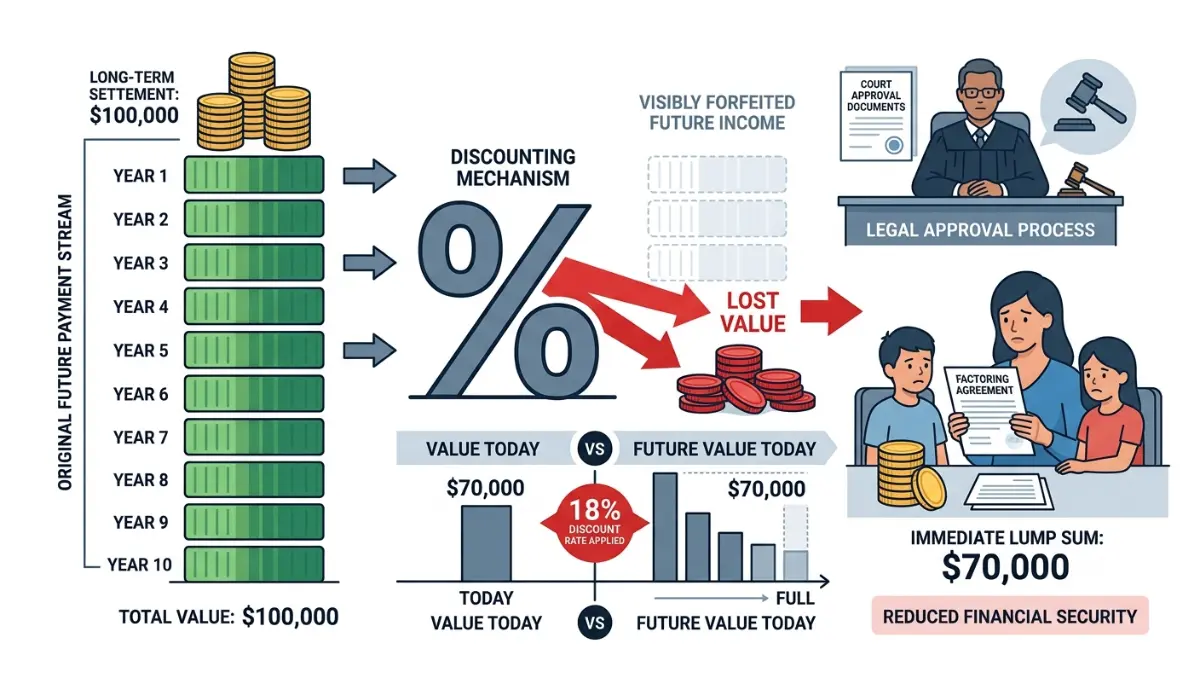

Can you sell wrongful death structured settlement payments?

Selling structured settlement payments to a factoring company in exchange for a lump sum is legally permitted in all 50 states — but requires court approval before any transfer can occur.

This option exists specifically as a last resort, and the permanent financial cost of using it is larger than most families realize before they begin the process.

How the structured settlement factoring process works — and why courts must approve it

Under structured settlement protection acts (SSPAs) enacted in all 50 states, a factoring company cannot purchase future payments without a judge reviewing the transaction and finding it is in the seller’s best interest.

The court approval requirement provides a procedural check — but it does not guarantee the financial terms are favorable, only that a legal standard was met.

For a full walkthrough of what to expect from filing through hearing, how the court approval process works for structured settlement transfers covers every step in detail.

The real cost of selling payments early — what families actually receive

A factoring company calculates its purchase offer by applying a discount rate — typically 9%–18% in the 2026 secondary market — to determine the present value of the payment stream.

At a 12% discount rate, a family selling $100,000 in future payments receives approximately $68,000–$74,000 today, permanently forfeiting the remaining $26,000–$32,000.

⚠️ Warning: Factoring companies are legally required to disclose the effective discount rate in writing before court. Have that disclosure independently reviewed before signing any transfer agreement. The full cost breakdown of selling structured settlement payments and what to expect when selling your payment stream both cover the financial tradeoffs with real-dollar calculations. For consumer rights context throughout the process, the CFPB’s consumer guidance on structured settlement transfers provides independent information on your rights before any agreement is signed.

Your next steps before accepting a wrongful death settlement

Three actions taken before signing determine what a family receives for the next decade or more.

Request the compensatory and punitive allocation in writing. Ask your plaintiff attorney to produce a written breakdown of which settlement components are compensatory and which are punitive — then have a CPA with settlement experience review that allocation before any agreement is signed.

Ask for three payment structure scenarios. Request a flat-payment scenario, a COLA-adjusted scenario, and a hybrid front-load scenario from the settlement broker side by side — so the comparison is real and not theoretical.

Retain a fee-only financial advisor before you sign, not after. A financial advisor with no commission stake in which option you choose can model the after-tax, after-inflation comparison between the structured settlement offer and a lump-sum alternative using your actual household numbers.

Understanding what the court approval process protects if you later need to transfer payments is also part of accepting a structured settlement with full information about your future options.

The families who receive the most from a wrongful death structured settlement are the ones who treated the financial instrument with the same scrutiny they would apply to any other multi-decade contract.

Frequently asked questions about wrongful death structured settlements

1. What is a wrongful death structured settlement?

A wrongful death structured settlement is a financial arrangement in which periodic payments — funded through a licensed life insurance annuity — are paid to surviving family members in place of a single lump sum. Payments are guaranteed by a life insurer through a qualified assignment under IRC §130. Consult a licensed financial professional before accepting any settlement terms.

2. How are wrongful death settlement payments calculated?

Payments are based on the total agreed compensation, the beneficiary’s age and life expectancy, the desired payment duration, and prevailing annuity pricing at settlement. A settlement broker models multiple payment scenarios for comparison. Because calculations depend on 2026 annuity market rates, consult a licensed financial professional to evaluate the specific terms in your offer.

3. Are wrongful death structured settlement payments tax-free?

Compensatory damages in a wrongful death structured settlement are generally excluded from federal gross income under IRC §104(a)(2). Punitive damages within the same award, however, are taxable at ordinary income rates. A CPA with settlement experience should review the full compensatory-versus-punitive allocation in your case before the agreement is finalized.

4. How long does a wrongful death structured settlement last?

A wrongful death structured settlement can run for a fixed period — commonly 10, 20, or 30 years — or for the beneficiary’s lifetime. Lifetime annuities often include a guaranteed minimum payment period to protect the estate if the beneficiary dies early. Duration is negotiable before signing and should reflect the family’s long-term income replacement needs.

5. Can you sell wrongful death structured settlement payments?

Payments can be sold to a factoring company for a lump sum, but court approval is required in all 50 states under structured settlement protection acts. The sale price typically represents 60%–90% of total future payment value after the factoring discount rate is applied. Consult a licensed financial professional before entering any structured settlement transfer agreement.

6. What is the difference between a lump sum and a wrongful death structured settlement?

A lump sum provides immediate access to the full award but places investment risk and tax liability on the recipient. A wrongful death structured settlement provides guaranteed periodic payments backed by a life insurer, with creditor protection in most states and no active investment management required. The superior choice depends on the recipient’s tax situation, discipline, and income needs.

7. Who pays a wrongful death structured settlement?

The defendant’s liability insurer initially funds the settlement. Through a qualified assignment under IRC §130, the payment obligation transfers to a specialized assignment company, which purchases an annuity from a licensed life insurer. The life insurer then pays the beneficiary directly on schedule. The defendant is legally released from future payment responsibility once the assignment is executed.

8. What happens to structured settlement payments if the beneficiary dies?

The outcome depends on the settlement contract terms. Many agreements include a guaranteed minimum payment period — meaning payments continue to a named heir or the estate for the remainder of the guaranteed term. Death benefit provisions must be negotiated and written into the contract before signing. Consult a licensed financial professional about beneficiary designation options specific to your situation.

9. How is a wrongful death structured settlement funded?

After settlement, the defendant’s insurer pays a lump-sum premium to a qualified assignment company. That company purchases an annuity from a licensed life insurer, which invests the premium and makes scheduled payments to the beneficiary. The life insurer — not the defendant — becomes the direct payment source for the full duration of the structured settlement.

10. What is a qualified assignment in a structured settlement?

A qualified assignment under IRC §130 transfers the defendant’s payment obligation to a third-party assignment company, which purchases an annuity to fund all future payments. This legally releases the defendant from ongoing liability. The assignment company’s financial strength and the annuity issuer’s credit rating are factors a licensed financial advisor can help you evaluate before signing.

11. Can a wrongful death structured settlement be modified after it’s signed?

Once executed, the payment schedule is generally fixed by the annuity contract and cannot be modified. This permanence makes pre-signing negotiation critical — including COLA provisions, payment duration, and beneficiary designations. Consult a licensed financial professional to model multiple payment scenarios before committing to any structure, as post-signing changes are rarely available.

12. Do minor children receive wrongful death structured settlement payments differently?

When minor children are beneficiaries, most states require court approval to confirm the payment structure serves the minor’s best interests. Payments may be deferred until adulthood, placed in trust, or structured to fund education at specific ages. Independent legal counsel familiar with minor settlement law is recommended before finalizing any wrongful death structured settlement that includes children as beneficiaries.

13. What is a structured settlement protection act?

A structured settlement protection act (SSPA) is state legislation requiring court approval before a recipient can sell future payments to a factoring company. All 50 states have enacted SSPAs as of 2026. The court must find the transaction is in the recipient’s best interest — providing a legal check against pressure to sell future income at steep discounts under financial duress.

14. How do I negotiate a wrongful death structured settlement?

Negotiation begins before final figures are agreed to. Request a minimum of three payment scenarios from the settlement broker, ask specifically about COLA riders, guaranteed payment periods, and beneficiary designations, and have the full package reviewed by a fee-only financial advisor who is unaffiliated with any party to the case before any agreement is signed.

15. What is the average wrongful death structured settlement amount?

Amounts vary significantly by case. In 2026, wrongful death settlements range from under $500,000 to several million dollars, depending on the deceased’s age, income, and dependency factors. Payment streams are typically sized to replace projected lifetime income loss. A licensed financial professional can help evaluate whether a specific offer reflects the full measurable economic loss in your case.

16. Can wrongful death settlement payments be taken by creditors?

In most states, structured settlement periodic payments are protected from creditors under state law — a meaningful advantage over a lump sum, which is generally subject to creditor claims once deposited. Creditor protection provisions vary by state. A licensed financial professional familiar with your state’s laws can explain how that protection applies to your specific settlement and household situation.

17. What fees are involved in a wrongful death structured settlement?

The plaintiff attorney typically receives a contingency fee of 25%–40% of the gross award before the settlement is funded. Structured settlement brokers are compensated by the annuity issuer, not by the family directly. Factoring fees apply only if payments are later sold, typically reducing future payment value by 10%–40% depending on the discount rate and payment timeline applied.

ℹ️ Disclaimer: The structured settlement and annuity information in this article is provided for educational purposes only. Wrongful death structured settlements are regulated insurance and financial instruments; tax treatment under IRC §104(a)(2), payment terms, and consumer protections vary by case-specific facts, state law, and the provisions of each individual settlement agreement. The IRC §104(a)(2) exclusion applies only under conditions that must be verified for each case — particularly where a judgment includes punitive damages, interest, or non-physical-injury components that may be taxable.

Nothing in this article constitutes financial, legal, or tax advice. Michael R. Thompson, CFA, and FinanceAuthorityHub.com do not provide legal or tax services and are not affiliated with any structured settlement annuity issuer, factoring company, or settlement broker. Consult a licensed financial advisor, a CPA with settlement experience, and independent legal counsel before accepting, modifying, or selling any structured settlement.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.