How Workers Comp Structured Settlements Differ From Injury Cases

Workers comp structured settlement annuity rates shifted $13,400 in value in 2026 — and most injured workers never check the pricing date before signing.

In This Article

What injured workers need to know before signing

Your employer’s insurer just handed you a settlement offer. That document is asking you to make a permanent, irrevocable financial decision — often while you are still in recovery.

Workers comp structured settlements are not the same financial product as personal injury structured settlements. The tax rules differ, the negotiation leverage differs, and the legal framework differs in ways that directly affect your long-term financial outcome.

Why most workers comp settlement guides get this wrong

Most content on this topic is written by attorneys focused on the claims process. The financial mechanics — how annuity pricing works, how the 2026 interest rate environment changes the real value of your payments, how the IRC treats workers comp differently from a tort award — are almost never addressed with precision.

The one distinction that changes your financial outcome

The difference between IRC §104(a)(1) and §104(a)(2) can determine whether a portion of your settlement carries a taxable component. Start with what structured settlements cost and how they pay — this article then layers the workers comp-specific rules that change everything.

ℹ️ Disclaimer: The workers compensation and structured settlement content in this article is for educational purposes only. Workers comp structured settlements are state-regulated insurance products, and payment terms, tax treatment, state board approval requirements, and payment modification rights vary materially by state and by the specific facts of each claim. The tax exclusion analysis reflects IRC §104(a)(1) and IRS Publication 4345 as of 2026. Consult a licensed workers comp attorney and an NSSTA-registered structured settlement consultant before accepting, rejecting, or modifying any settlement offer.

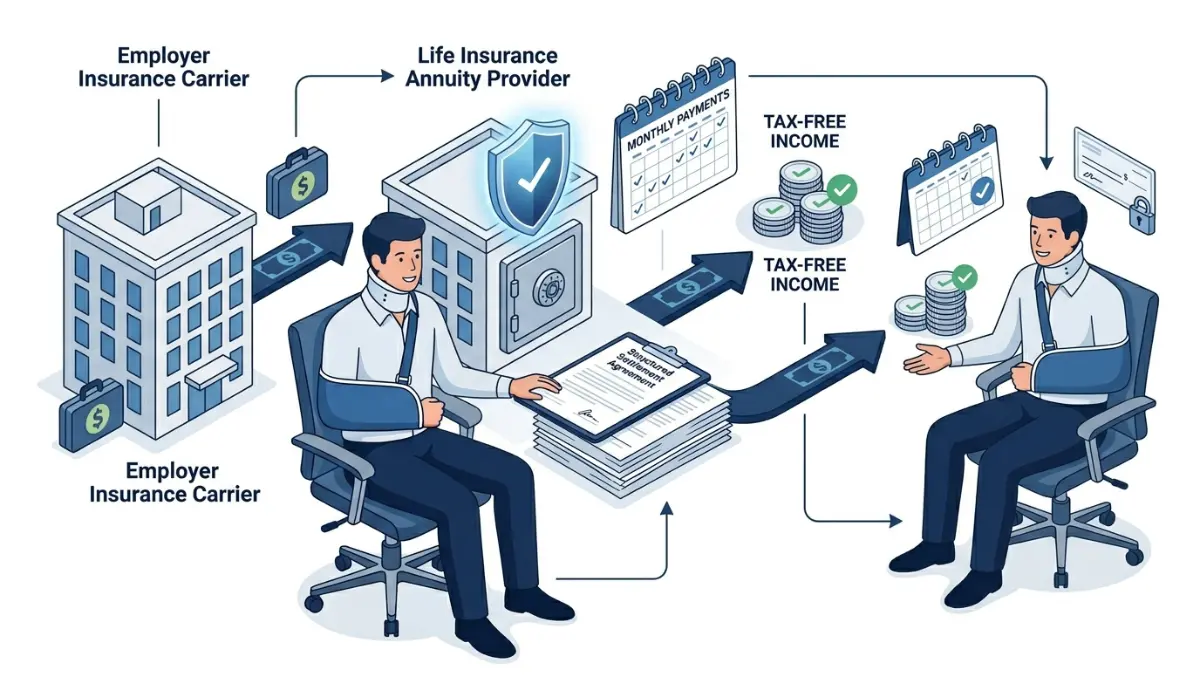

How a workers comp structured settlement actually works

A workers comp structured settlement is a legally binding agreement in which an injured worker accepts periodic payments — funded through a life insurance annuity purchased by the employer’s carrier — in exchange for releasing all future workers comp claims. The insurer does not pay you directly over time; it purchases a qualified annuity from a life insurance company, which then makes payments on a negotiated schedule.

📊 Data Point: The Bureau of Labor Statistics Injuries, Illnesses, and Fatalities program tracks occupational injury cases resulting in permanent impairment — serious claims in this category are a primary driver of structured settlement negotiations between injured workers and employers’ carriers. Source: BLS Injuries, Illnesses, and Fatalities Program, 2026.

Who funds the payments and how long they last

The employer’s insurance carrier purchases the annuity. Common payment structures run 10 years, 20 years, or for the claimant’s lifetime.

Lifetime structures carry a different pricing logic than fixed-term agreements — a distinction that matters when evaluating any offer on the table. Understanding how annuities work as financial instruments builds the vocabulary you need to assess what you are actually being offered.

How the annuity is priced and what that means for your payout

The annuity rate is not fixed by the gross settlement dollar amount alone. It is driven by prevailing long-term interest rates at the time the insurer purchases the contract.

A one-percentage-point difference in that pricing rate on a 20-year payment stream can change your effective settlement value by more than $40,000.

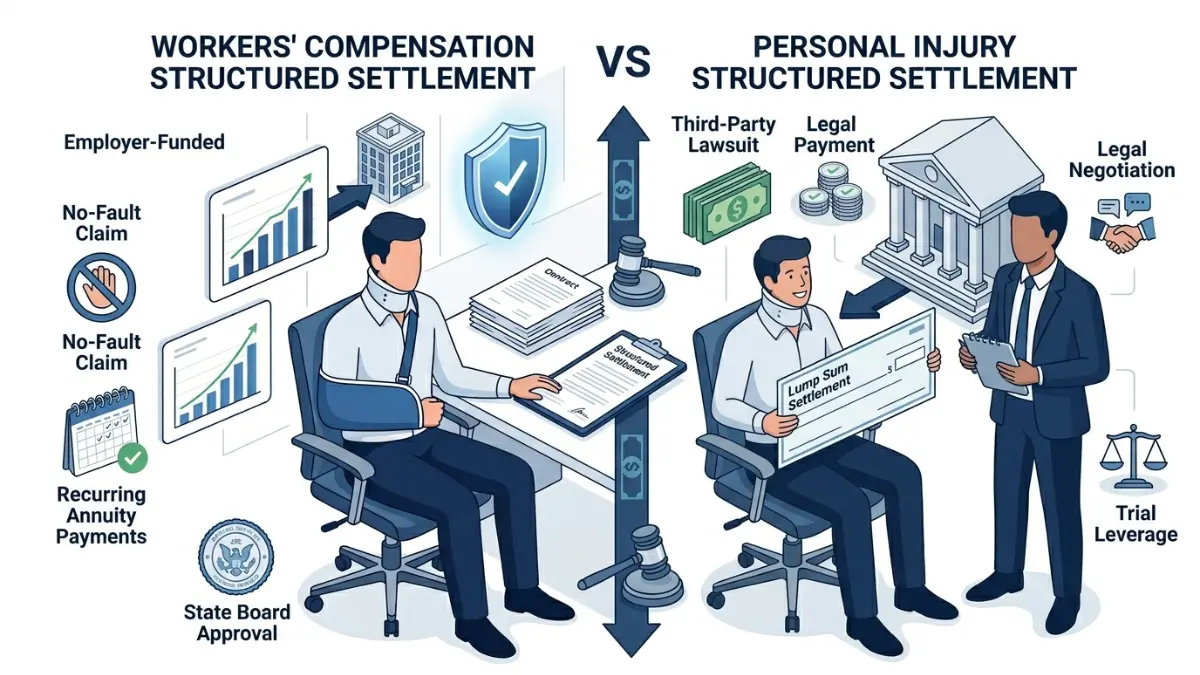

Workers comp vs. personal injury: six differences that matter

A personal injury structured settlement and a workers comp structured settlement share a name. They do not share a legal or financial foundation. The table below captures the six dimensions most likely to affect your financial outcome.

| Dimension | Workers Comp Settlement | Personal Injury Settlement |

|---|---|---|

| Tax exclusion basis | IRC §104(a)(1) — statutory, categorical | IRC §104(a)(2) — physical injury proof required |

| Negotiation leverage | Limited — no-fault system, no trial threat | Greater — liability dispute creates pressure |

| State board approval | Required in most states | Court approval of structured terms only |

| Ability to sell payments | Restricted or prohibited in most states | Allowed with court approval in most states |

| COLA provisions | Available — varies by state statute | Negotiable by agreement |

| Benefit offset risk | Yes — SSDI offsets may apply | No automatic offset |

Source: State workers compensation statutes; IRS IRC §104; 2026.

Tax treatment: the IRC §104 distinction most people miss

Under IRC §104(a)(1), workers comp payments are excluded from federal gross income categorically — without requiring proof that the payment is “on account of personal physical injury.” That is the standard governing the §104(a)(2) tort exclusion, and the two are not interchangeable.

Mixed settlements that include wages, non-physical damages, or components outside the workers comp statute may carry taxable elements. Use the income tax calculator to model the net impact of any taxable component on your actual recovery.

Negotiation rights, state approval, and the ability to sell

Workers comp is a no-fault system. There is no liability dispute, which eliminates the trial-threat leverage personal injury plaintiffs use to drive higher settlements. Knowing what the state board approval process requires before negotiations begin is a structural advantage most claimants do not have.

If you later need liquidity, selling workers comp structured settlement payments is far more restricted than factoring a personal injury award — prohibited outright in many states. That restriction is a variable that belongs in your evaluation before the ink dries.

💡 Expert Note (CFA): The no-fault limitation is the most consistently underestimated factor I see in workers comp settlement negotiations. A personal injury plaintiff can credibly threaten trial; a workers comp claimant cannot. That asymmetry shapes every offer the insurer makes — and every counteroffer you have standing to make. Knowing it before entering negotiation is a meaningful financial advantage.

Lump sum or structured payments: how to decide

The right choice between a lump sum and structured periodic payments depends on three financial variables — not on what the employer’s insurer calls standard practice, and not on a general rule.

The three variables that determine which option pays more

- Present value at current annuity rates. Calculate the lump-sum equivalent of the offered periodic payment stream at the 2026 benchmark annuity rate. Use the investment calculator to model what a lump sum would generate if invested at current market yields — then compare the two numbers directly.

- Your capacity to manage a lump sum without depleting it. A $300,000 lump sum invested at 5.0% annually generates approximately $15,000 per year. That requires disciplined investment management and a plan for rising medical costs — if that discipline is uncertain, structured payments protect against premature depletion.

- Your state’s COLA provisions and benefit-offset rules. Fixed periodic payments lose real value over 15 to 20 years as prices rise. Use the inflation calculator to model the real purchasing power of any fixed payment schedule before committing to it.

💡 Expert Note (CFA): In 28 years of client advisory work, the most common and most costly mistake I have seen is accepting a structured settlement without first calculating the present value of the payment stream at the current annuity rate — then comparing it directly to the lump sum offer. Insurers price structured settlements to their advantage. The present-value calculation reveals the gap. I have seen differences of more than $60,000 between the present value of the periodic payments and the lump sum figure the insurer initially offered.

When structured payments are the right financial choice

Structured payments make sense when the injury involves permanent disability, when lifetime medical cost exposure is uncertain, or when the claimant’s financial history suggests a lump sum would be quickly depleted. Read the complete lump sum vs. structured settlement analysis before arriving at any conclusion.

When to push for a lump sum instead

A lump sum typically produces more total wealth when the claimant is younger than 55, has a clear investment strategy, and can achieve returns that exceed the structured settlement discount rate. Review how structured settlement discount rates are calculated to understand precisely how the insurer priced the offer in front of you.

⚠️ Warning: Workers comp structured settlements are permanent in most states. Once approved by the state workers comp board, the payment terms cannot be renegotiated or modified without significant legal barriers. Obtain an independent present-value analysis from an NSSTA-registered consultant and a full attorney review before signing anything. Consult a licensed workers comp attorney and a licensed financial professional before making this decision.

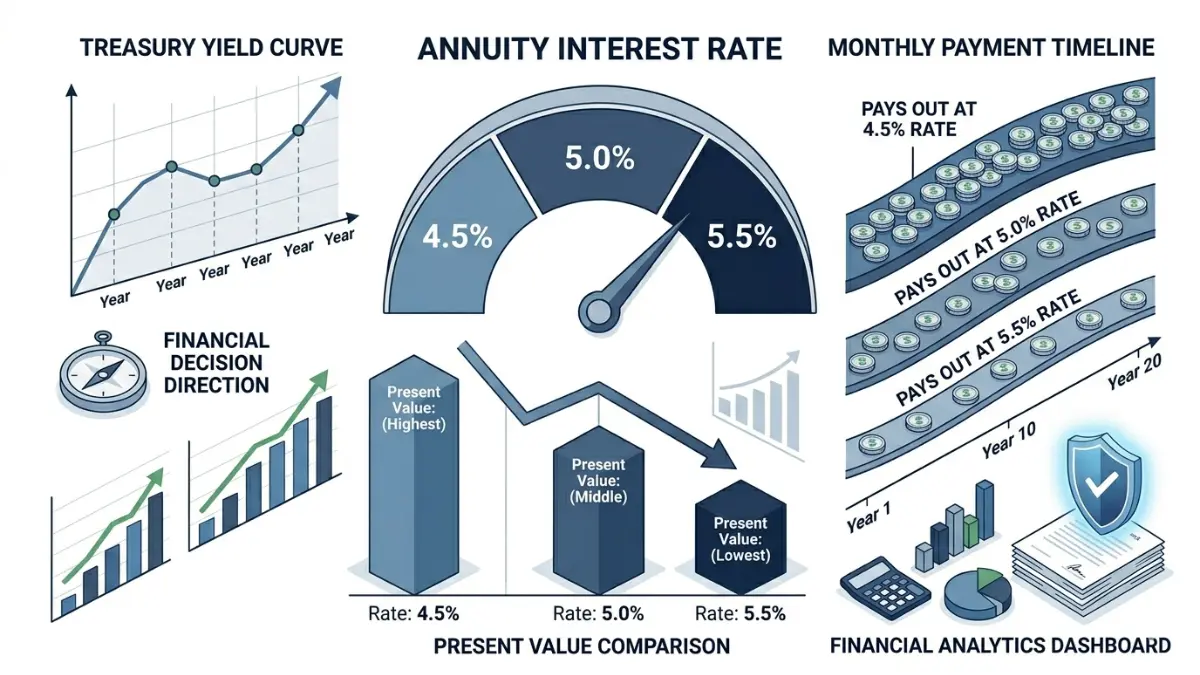

How 2026 annuity rates shape your settlement value

Annuity pricing in a workers comp structured settlement is not arbitrary. It tracks the 20-year U.S. Treasury constant maturity yield at the time the insurer prices the contract — the same rate-sensitivity that governs the present value of any long-duration fixed-income position.

What drives annuity pricing in a workers comp settlement

Life insurance companies price structured settlement annuities as a spread above long-term Treasury benchmarks. In the 2026 rate environment, benchmark rates for 20-year workers comp structured settlement annuities have ranged approximately 4.5% to 5.5%.

Understanding how annuities are regulated and priced as financial products at the federal level clarifies why the annuity pricing date in a settlement agreement is a financially material number — not a procedural formality.

📊 Data Point: The Federal Reserve’s Statistical Release H.15 tracks the 20-year constant maturity Treasury yield daily — the primary benchmark used by life insurance companies pricing workers comp structured settlement annuities. Source: Federal Reserve Statistical Release H.15, 2026.

A 2026 rate scenario: how a 50-basis-point difference changes your payout

The table below shows the present value of $2,000 per month over 20 years at three annuity pricing rates within the 2026 benchmark range.

| Annuity Rate | PV of $2,000/Month × 20 Years | Difference vs. 4.5% |

|---|---|---|

| 4.5% | $316,400 | — |

| 5.0% | $303,000 | −$13,400 |

| 5.5% | $290,400 | −$26,000 |

Calculated using standard present-value formula for monthly annuity payments. Rates are illustrative of the 2026 structured settlement pricing environment. Verify actual annuity pricing with a licensed structured settlement consultant.

💡 Expert Note (CFA): A 50-basis-point rate difference — less than half a percentage point — reduces the present value of a 20-year $2,000/month stream by more than $13,000. I apply the same duration analysis to evaluate structured settlement offers that I use to measure interest-rate sensitivity in a fixed-income portfolio. The mechanism is identical. The annuity pricing date is a negotiating variable, not a formality.

Tax rules and state approval: what the law requires

Under IRC §104(a)(1), periodic payments received under a workers compensation statute are excluded from federal gross income — categorically, and without the physical injury proof requirement that governs the §104(a)(2) tort exclusion.

The federal tax exclusion under IRC §104(a)(1)

The exclusion applies to every installment in a workers comp structured settlement funded under a qualifying state statute. Mixed settlements that include wages, non-physical damages, or components outside the workers comp framework may contain taxable elements — making the characterization of each settlement component financially significant.

IRS Publication 4345 is the authoritative source on the taxability of settlement proceeds. The IRS guidance on nontaxable income categories confirms the statutory basis of the workers comp exclusion and the boundaries of its application.

📊 Data Point: IRS Publication 4345 (2026) confirms that amounts received as workers compensation for occupational sickness or injury are fully excludable from gross income under IRC §104(a)(1) — with no physical injury requirement. Source: IRS Publication 4345, 2026.

State approval requirements and restrictions on selling your payments

Most states require workers comp board approval before a structured settlement becomes binding. That approval protects claimants from coercive settlement tactics — but it also makes the agreement very difficult to modify after the fact.

Factoring workers comp settlement payments is far more restricted than factoring personal injury awards — prohibited in many states. Before relying on future payment liquidity, verify your state’s specific statute and review the full tax treatment of structured settlement payments as part of your pre-signing analysis.

💡 Expert Note (CFA): A CPA on one client engagement incorrectly applied §104(a)(2) rules to a workers comp structured settlement, generating a false taxable income estimate that nearly triggered a $18,000 unnecessary tax provision. The §104(a)(1) exclusion is statutory and categorical. Verify the correct code section with a licensed tax professional before any tax planning is attempted around a settlement.

Your next step before signing any settlement offer

The same discipline that governs evaluating a 20-year bond position applies to your workers comp structured settlement offer. No permanent financial agreement should be signed without first calculating the present value of the payment stream at the current annuity rate.

Three steps before you accept or reject a settlement offer

- Calculate the present value. Use the current benchmark annuity rate to calculate the lump-sum equivalent of the periodic payments. Compare that number directly to any lump sum offer — the gap reveals whether the structured option is priced fairly.

- Get a workers comp attorney review. State board approval requirements, benefit offsets, and COLA provisions vary by jurisdiction. An attorney reviews the legal structure of the agreement before you commit to its terms.

- Request an independent broker valuation. An NSSTA-registered structured settlement consultant provides a present-value analysis independent of the insurer. Compare the leading structured settlement companies and consultants before engaging one.

Where to find independent financial and legal guidance

For the full claim-to-settlement timeline, the workers compensation overview covers every stage from initial claim through final settlement approval.

✅ Pro Tip: Request the annuity pricing date in writing before signing any agreement. That date sets the interest rate at which your payment stream was valued. A pricing date from months earlier can cost thousands of dollars if rates have moved since the insurer first calculated the offer.

Workers comp structured settlement: frequently asked questions

1. What is a workers comp structured settlement?

A workers comp structured settlement is a legally binding agreement in which an injured worker accepts periodic payments, funded by a life insurance annuity the employer’s carrier purchases, in exchange for releasing all future workers comp claims. Payment terms are negotiated before state board approval. Consult a licensed workers comp attorney before signing any agreement.

2. How does a workers comp structured settlement differ from a lump sum?

A workers comp structured settlement delivers guaranteed periodic income — monthly, annually, or for life — while a lump sum transfers the full settlement value at once. Whether structured payments produce more total value depends on the 2026 annuity pricing rate and your personal investment capacity. Consult a licensed financial professional before deciding between the two.

3. Are workers comp structured settlements taxable in 2026?

Workers comp structured settlement payments are excluded from federal gross income under IRC §104(a)(1). This statutory exclusion is categorical and does not require physical injury proof. Mixed settlements with wage components or non-physical damages may contain taxable elements. Consult a licensed CPA or tax attorney for analysis specific to your settlement structure.

4. Can I negotiate a workers comp structured settlement?

Yes — payment frequency, duration, COLA adjustments, and lump sum components in a workers comp structured settlement are all negotiable before state board approval. Workers comp is a no-fault system, so leverage is more limited than in personal injury cases. An NSSTA-registered consultant and a workers comp attorney together strengthen your negotiating position.

5. How long do workers comp structured settlement payments typically last?

Workers comp structured settlement payment terms commonly run 10 to 30 years, or for the claimant’s lifetime in permanent total disability cases. Lifetime structures carry higher long-term protection against outliving the benefit but are priced differently than fixed-term agreements. The term is negotiated as part of the overall settlement package before state board approval.

6. What happens to my workers comp structured settlement if I die?

Most workers comp structured settlement agreements include a guaranteed payment period. If the claimant dies before the period ends, remaining payments pass to a named beneficiary. Lifetime-only structures with no guaranteed period cease at death. Confirm the specific guaranteed-period terms of any offer with a licensed workers comp attorney before signing.

7. Can I sell my workers comp structured settlement payments?

Selling workers comp structured settlement payments — known as factoring — is significantly more restricted than selling personal injury payments. Many states prohibit it outright under workers comp statutes. Where permitted, board or court approval is required. Verify your state’s specific factoring statute before relying on any anticipated future liquidity from your settlement.

8. How is a personal injury structured settlement different from workers comp?

A personal injury structured settlement is governed by IRC §104(a)(2) and requires physical injury proof for the tax exclusion. A workers comp structured settlement uses the §104(a)(1) categorical exclusion, is subject to state board approval, may carry SSDI offset risk, and offers significantly more restricted factoring rights than a personal injury award.

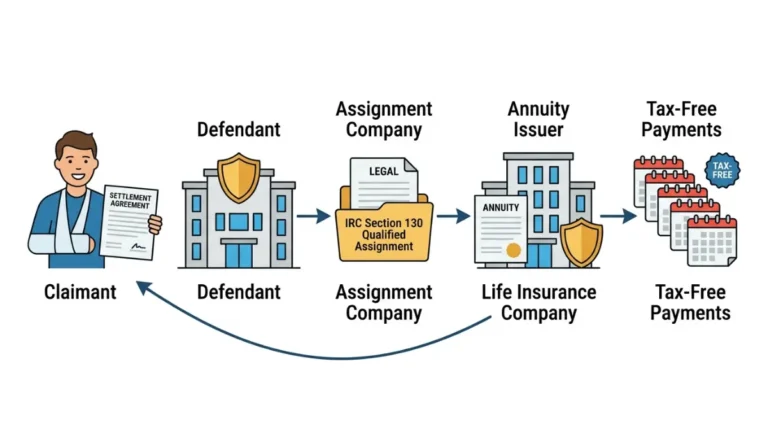

9. Who actually pays for a workers comp structured settlement?

The employer’s workers comp insurance carrier funds the workers comp structured settlement by purchasing a qualified annuity from a life insurance company. That life insurer — not the employer, not the carrier — makes the actual periodic payments. The carrier transfers the obligation through a qualified assignment under IRC §130, releasing itself from long-term payment liability.

10. What are the main advantages of a workers comp structured settlement?

A workers comp structured settlement provides guaranteed tax-free income under IRC §104(a)(1), eliminates investment risk for claimants who cannot manage a lump sum, and protects against premature depletion of settlement funds. States with COLA provisions allow periodic payments to partially retain real purchasing power over a 15- to 20-year payment horizon.

11. How much is a typical workers comp structured settlement worth?

Workers comp structured settlement values range from under $50,000 for short-term injuries to more than $1 million for permanent total disability cases with lifetime medical cost exposure. The gross value reflects injury severity, projected wage loss, and future medical costs. Consult an NSSTA-registered structured settlement consultant for a valuation specific to your claim.

12. Do I need a lawyer to obtain a workers comp structured settlement?

An attorney is strongly advisable before agreeing to any workers comp structured settlement — even where not legally required. State board approval processes, benefit offset rules, and negotiation strategy require legal expertise. An NSSTA-registered consultant handles the financial present-value analysis. Together, these two professionals cover the full decision landscape before signing.

13. What is a qualified assignment in a structured settlement?

A qualified assignment, governed by IRC §130, is the mechanism by which an insurance carrier transfers its workers comp structured settlement payment obligation to a third-party assignee and life insurance annuity issuer. This releases the carrier from long-term payment liability. The injured worker’s payments continue unchanged — issued by the assignee’s annuity rather than the original carrier.

14. How do 2026 annuity rates affect the value of my settlement?

Workers comp structured settlement annuities are priced against long-term Treasury benchmarks. In 2026, benchmark rates for 20-year structures have ranged approximately 4.5%–5.5%. A 50-basis-point rate difference changes the present value of a $2,000/month 20-year stream by approximately $13,400. Consult a licensed structured settlement consultant for a rate-specific present-value analysis of your offer.

15. Is a workers comp structured settlement better than a lump sum?

No universal answer applies to a workers comp structured settlement vs. lump sum decision. Structured payments provide guaranteed tax-free income and depletion protection. A lump sum offers flexibility and investment upside but requires discipline. The right choice depends on your age, health, investment capacity, and state’s COLA and offset rules. Consult a licensed financial professional.

16. Which state laws govern workers comp structured settlements?

Each state’s workers compensation statute governs workers comp structured settlement payment terms, modification rights, and board approval requirements — there is no uniform federal framework for these provisions. The IRC §104(a)(1) federal tax exclusion applies uniformly across states. Verify your specific state’s board approval process and factoring restrictions with a licensed workers comp attorney.

17. Can my employer force me to accept a structured settlement in workers comp?

No employer can legally compel acceptance of a workers comp structured settlement without the claimant’s agreement. However, the employer’s insurer controls the terms of any offer, and in no-fault workers comp systems the claimant has limited leverage to demand a lump sum. A licensed workers comp attorney can clarify your rights and strengthen your position before any deadline.

ℹ️ Disclaimer: The workers compensation and structured settlement information in this article is for educational purposes only. Workers comp structured settlements are state-regulated insurance products — funded through life insurance annuities issued under state workers compensation statutes — and terms, tax treatment, board approval requirements, and payment modification rights vary materially by state and claim. The tax exclusion analysis reflects IRC §104(a)(1) and IRS Publication 4345 as of 2026.

Annuity rate figures in this article represent illustrative 2026 benchmark ranges and do not constitute a quote, offer, or guarantee from any insurer or structured settlement provider. Before accepting, rejecting, or modifying any workers compensation settlement offer, consult a licensed workers comp attorney and an NSSTA-registered structured settlement consultant in your state. Michael R. Thompson, CFA, and FinanceAuthorityHub.com do not provide legal, insurance, or settlement brokerage services and are not affiliated with any structured settlement provider or workers compensation carrier.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.