How an annuity works, what it pays, and the real costs

Is an annuity worth it? The answer is in the fees — near zero on a fixed annuity, over 3% a year on a variable one. Here’s how to decide.

In This Article

An annuity is one of the few financial products that can promise you a paycheck for life — and also one of the easiest to buy wrong. The word covers everything from a simple, CD-like savings contract to a complex, fee-layered investment with a salesperson attached. Understanding which is which, before you sign, is the difference between a guarantee that protects you and a contract that quietly costs you tens of thousands of dollars.

Where you are right now shapes what you most need from this page:

- If you’re sitting on a maturing CD or a cash lump sum and chasing a better, safe yield, start with the rates and the real-cost sections — the math between a fixed annuity and a CD is currently meaningful.

- If you’re five to ten years from retirement and afraid of outliving your money, the income and decision sections are written for you.

- If a salesperson or “advisor” has already pitched you a specific annuity, read the costs and the safety sections first, then bring the question list to your next meeting.

- If you’re just trying to understand the word before anyone sells you anything, the next two sections give you the plain definition and the full menu of types.

This guide explains how annuities work, what they pay, the rates available as of June 2026, the fees you actually carry, how they’re taxed, and the honest case for and against buying one. Every rate, limit, and fee here is tied to a named authority and dated, because a wrong number on a page like this costs real people real money.

ℹ️ Financial Disclaimer: This article covers investing (variable annuities are securities), insurance product selection (fixed, indexed, and income annuities are insurance contracts), federal tax treatment (tax deferral, ordinary-income taxation, the 10% early-withdrawal penalty, and RMD/QLAC rules), and retirement-income planning.

The rates, tax figures, contract terms, and product comparisons here reflect current data from the cited authorities and are for educational purposes only — not personalized financial, tax, insurance, or legal advice. Your right choice depends on your age, income, other assets, tax bracket, health, and goals. Consult a fiduciary financial advisor (CFP® or fee-only RIA), a CPA or tax attorney, and a licensed insurance professional before acting on anything in this article.

How an annuity actually works

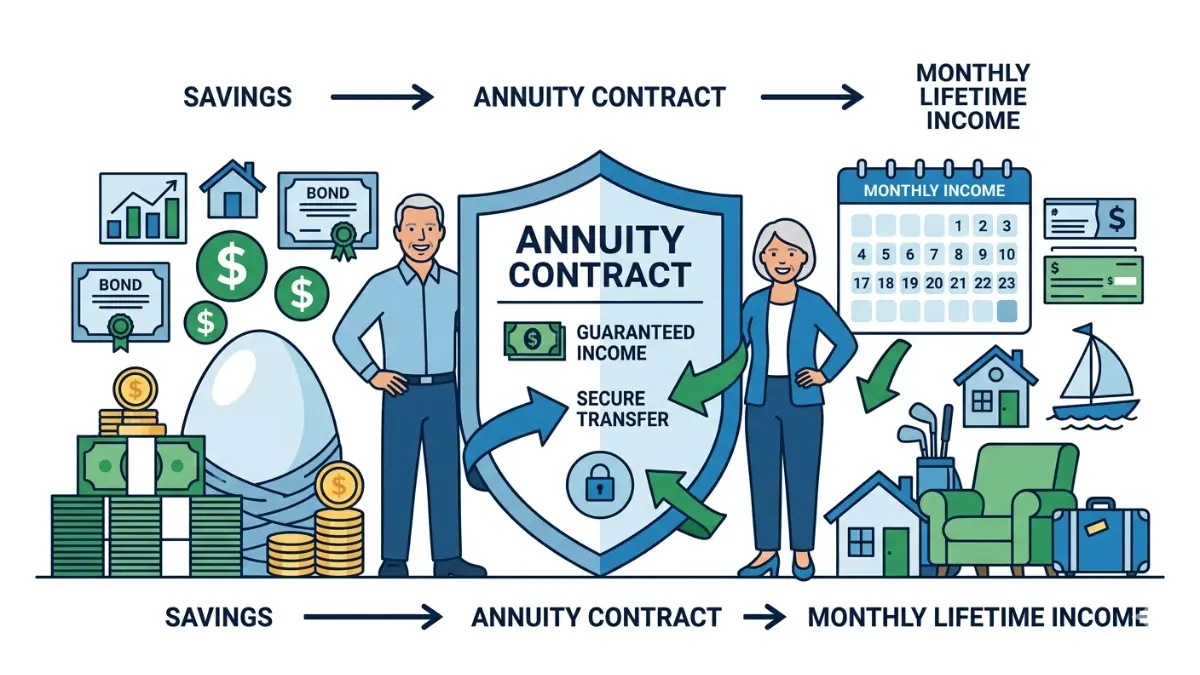

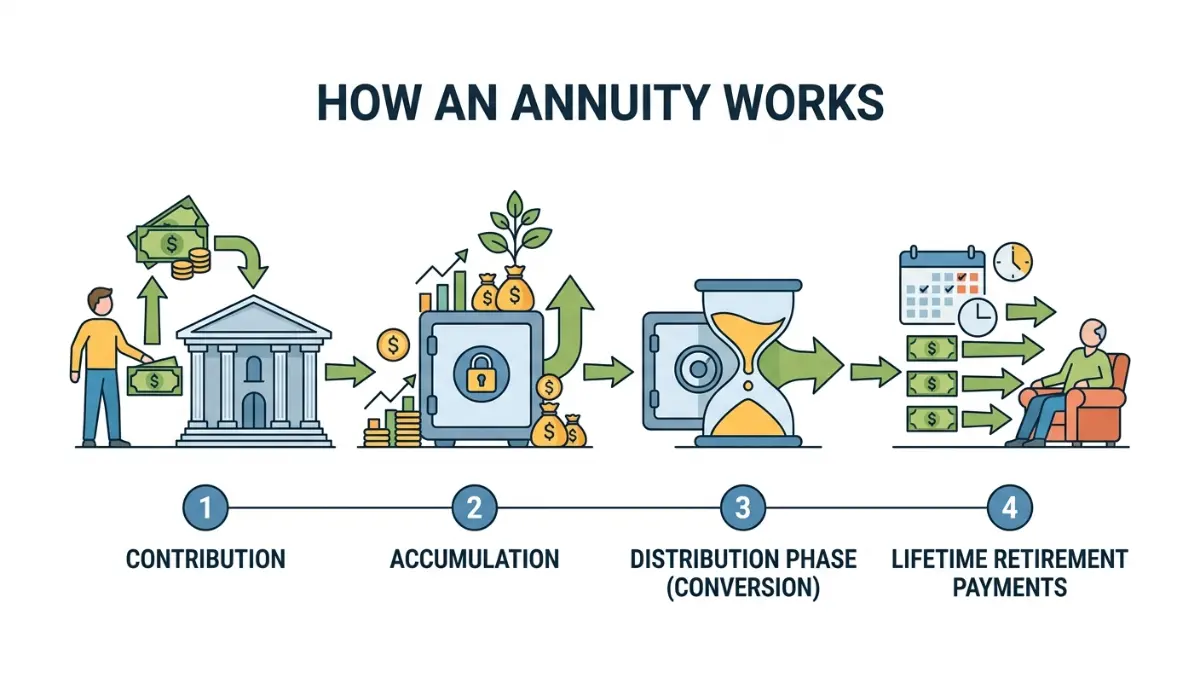

An annuity is a contract you make with an insurance company, not a deposit at a bank. You hand the insurer money — either a single lump sum or a series of payments — and in return the company promises to pay you back later, either as a stream of income for a set number of years or for the rest of your life. That promise to convert your savings into guaranteed income is the one thing an annuity does that almost no other product can.

The person who receives the payments is the annuitant. The insurer is the counterparty carrying the promise. According to the IRS, an annuity is simply a contract that requires payments for more than one full year to the person entitled to receive them.

🔍 How It Works: Most annuities run in two phases. During the accumulation phase, your money sits with the insurer and grows — at a fixed rate, a market-linked rate, or based on investments you choose, depending on the type. During the distribution phase, the contract pays you: either you take withdrawals, or you “annuitize,” which converts the balance into scheduled income payments. Some annuities skip straight to the distribution phase and start paying within a year (immediate annuities); others defer it for years or decades (deferred annuities).

The mechanism underneath all of this is risk transfer. When you buy a lifetime annuity, you are paying the insurer to take on the risk that you live longer than your money would otherwise last — what the industry calls longevity risk. The insurer pools thousands of contracts; some annuitants die early, some live long, and the averages let the company guarantee income it could not promise to any one person.

That transfer is the genuine value of an annuity, and also the source of its cost and its limits. You give up some control and some liquidity, and in exchange you move a risk off your own shoulders. Whether that trade is worth it is the real question this guide builds toward — and the answer is different for a 45-year-old still accumulating than for a 68-year-old who wants a private pension.

One point that surprises many buyers: an annuity is not FDIC-insured. A bank CD is backed by the federal government up to the deposit-insurance limit; an annuity is backed only by the issuing insurance company’s ability to pay its claims, with a state-level safety net behind it. That distinction matters enough that it has its own section later in this guide.

⚠️ Costly Mistake: Treating “annuity” as one product. A multi-year fixed annuity and a variable annuity with income riders are as different as a savings account and a brokerage account — different risks, wildly different fees, different tax edges. Buying one because you read something good about the other is how people end up in contracts that don’t fit.

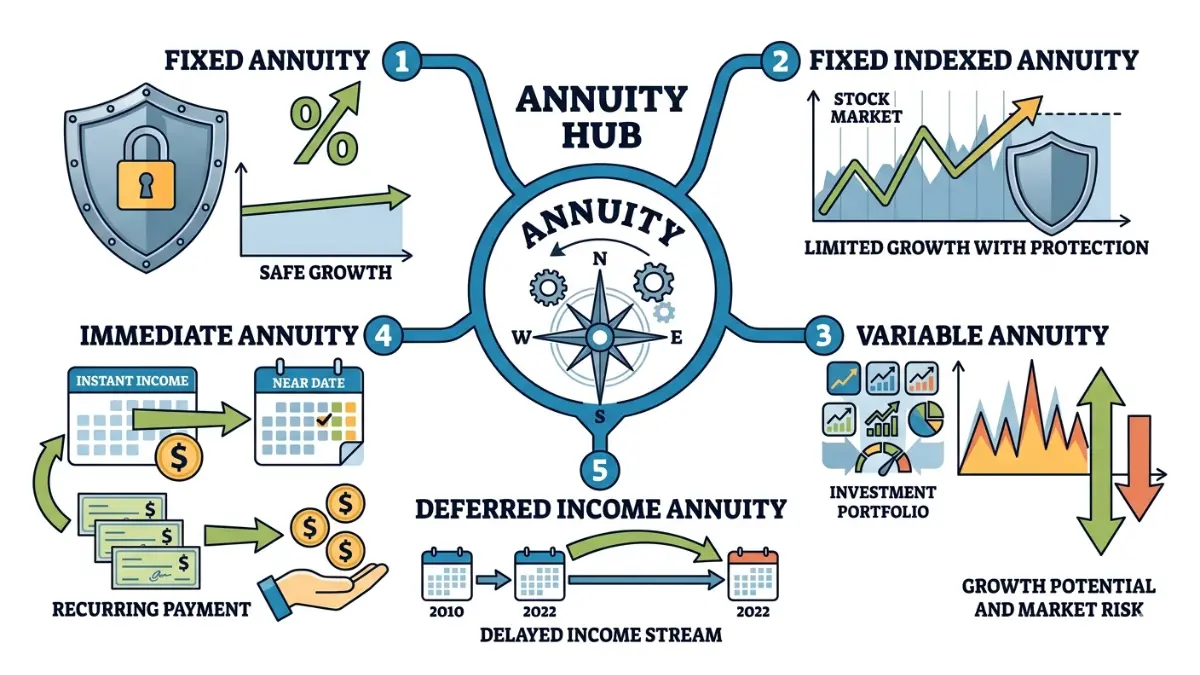

The main types of annuities, explained simply

The word “annuity” hides at least five distinct products, and the differences decide your risk, your return, your fees, and your liquidity. Sorting them is the single most useful thing you can do before talking to anyone selling one. The clearest way to organize them is by how your money grows and by when the income starts.

By how your money grows, there are three families:

- Fixed annuities pay a guaranteed interest rate set by the insurer, much like a CD. The most common version is the multi-year guaranteed annuity (MYGA), which locks a fixed rate for a chosen term, typically 2 to 10 years. Your principal is protected and the rate cannot change during the term. These are the simplest annuities and usually carry no explicit annual fees.

- Fixed-indexed annuities (FIAs) tie your interest to a market index, such as the S&P 500, while protecting your principal from market losses. You don’t get the index’s full return; instead, gains are limited by a cap, a participation rate, or a spread (explained just below). In a down year, your credited interest is 0% — you don’t lose principal to market declines, but you also don’t gain.

- Variable annuities invest your money in mutual-fund-like sub-accounts that you select. Your account value rises and falls with those investments, so you can lose money, including principal. Variable annuities are legally securities, regulated by the SEC and FINRA in addition to state insurance regulators, and they carry the highest fees of any annuity type.

By when the income starts, the same products split again:

- Immediate annuities, usually a single premium immediate annuity (SPIA), take a lump sum and begin paying income within about a year. These are the purest “turn savings into a paycheck” tool.

- Deferred annuities, including the deferred income annuity (DIA), delay payments to a future date you choose, letting the money grow first.

A newer category, the registered index-linked annuity (RILA), sits between indexed and variable: it offers more upside than a typical FIA but, unlike an FIA, exposes you to some market loss in exchange. RILAs are securities and are more complex; they deserve their own analysis rather than a first annuity purchase made under sales pressure.

🔍 How It Works: Inside a fixed-indexed annuity, three “limiting features” decide how much of the index’s gain you actually receive. A cap sets a ceiling — if your cap is 6% and the index rises 8%, you’re credited 6%. A participation rate credits a percentage of the gain — a 90% participation rate on a 10% index gain credits 9%. A spread subtracts a fixed amount first — a 3% spread on an 8% index gain credits 5%.

A single contract can use more than one of these at once, which can stack the limits and lower your real return well below the index. These features are set by the insurer and can change at each contract anniversary, so the rate that looked attractive at purchase is not guaranteed for the life of the contract.

Here is how the families compare on the attributes that actually drive a decision:

| Annuity type | How it grows | Can you lose principal? | Typical explicit fees | Best for |

|---|---|---|---|---|

| Fixed / MYGA | Guaranteed fixed rate for a set term | No (barring insurer failure) | Usually none | Safe, CD-like growth; near-term savers |

| Fixed-indexed (FIA) | Market-linked, capped; 0% floor | No to market loss | Low; rider fees if added | Conservative growth with downside protection |

| Variable | Chosen sub-accounts (market) | Yes | Highest (2%–3%+ all-in) | Tax-deferred investing plus optional guarantees |

| Immediate (SPIA) | N/A — pays income now | N/A — irrevocable | Built into payout | Turning a lump sum into lifetime income |

| Deferred income (DIA) | Grows, then pays later | Depends on type | Varies | Locking in future lifetime income |

Sources: product structures and securities status per Investor.gov (SEC) and FINRA; FIA crediting mechanics and fee ranges per insurer disclosures and industry data cited in the Real Costs and Rates sections below. Fee figures are detailed and sourced in the Real Costs section.

💡 Expert Note: SEC and FINRA guidance both stress that the type of annuity determines how it is regulated and how it can lose value. Because variable annuities are securities, anyone selling them must hold a securities license, and you can verify that license on FINRA BrokerCheck. A fixed or indexed annuity, by contrast, is sold under an insurance license and overseen by your state insurance commissioner. Knowing which product you’re being offered tells you which regulator stands behind it.

Current annuity rates and how they’re set

The most concrete reason annuities are getting attention in 2026 is rates: fixed annuity yields are near their highest levels in roughly 15 years, and they currently beat comparable CDs by a meaningful margin. But “annuity rates” means different things for different products, so the numbers below are organized by type, dated, and sourced.

For fixed annuities, the headline figure is the MYGA rate. As of June 2026, the best 5-year MYGA rate available was about 6.30%, while the strongest A-rated carriers were offering roughly 5.00% to 5.75%, depending on term and deposit size. Higher rates generally come from lower-rated insurers, which is a trade-off in safety, not a free lunch.

📊 Data Point: As of June 2026, the best 5-year fixed annuity (MYGA) rate was approximately 6.30%, with top A-rated carriers near 5.65%; the single highest fixed annuity rate in the market was about 6.50% on a 7-year contract from an A-rated insurer — roughly 1.6 percentage points above a comparable CD. (Source: aggregated carrier rate data, AnnuityRateWatch-sourced trackers, June 2026. Rates change daily and vary by state — verify the live rate on the day you buy.)

The comparison that drives most fixed-annuity decisions is MYGA versus CD. As of June 2026, a best-in-market 5-year MYGA near 6.30% compared with a top 5-year CD around 4.20% — a difference of roughly 2.10 percentage points per year, plus the annuity’s tax-deferral advantage (a CD’s interest is taxed every year; a MYGA’s is not until you withdraw). The trade-off is liquidity: a MYGA ties your money up for the term, with surrender charges for early access, and the 10% federal penalty can apply if you withdraw gains before age 59½.

🔍 How It Works: Annuity rates are not set in a vacuum — they track the broader interest-rate environment, especially the 10-year Treasury yield, which in turn reflects the Federal Reserve’s policy rate. When the Fed holds rates higher, insurers can invest your premium at higher yields and pass some of that through as higher annuity rates. As of its April 2026 meeting, the Federal Reserve held its federal funds target range at 3.50%–3.75%, with the next meeting scheduled for June 16–17, 2026. Industry analysts expect annuity rates to edge lower only gradually as the Fed eases, which is why locking a multi-year rate now can be attractive — but a rate decision after this article’s review date could change that picture.

For fixed-indexed annuities, there is no single guaranteed rate. Instead your return depends on the index plus the cap, participation rate, or spread in your specific contract, and on the insurer’s renewal behavior at each anniversary. That makes a quoted FIA “rate” far less comparable than a MYGA rate, and far more dependent on the contract’s fine print.

For variable annuities, the “rate” is your sub-account performance, which can be negative. There is no guaranteed accumulation rate unless you add an income rider — and that guarantee applies to a separate “benefit base” used to calculate income, not necessarily to your actual cash value.

One protection worth checking on any fixed or indexed annuity is the minimum guaranteed interest rate (MGIR) — the floor your rate can never fall below, even after the initial term renews. Many contracts set this floor at just 1.00%, though a few stronger contracts guarantee meaningfully higher minimums. When you compare offers, the renewal rate and the MGIR matter as much as the flashy first-term rate.

You can see how a MYGA stacks up against a certificate of deposit in our MYGA versus CD comparison.

⚠️ Costly Mistake: Comparing only the first-term “teaser” rate. A 6.30% rate that renews at the insurer’s discretion to a 1.00% floor is a different product from one with a 2.55% guaranteed minimum. Ask for the renewal-rate history and the MGIR in writing before you judge any fixed or indexed annuity by its headline number.

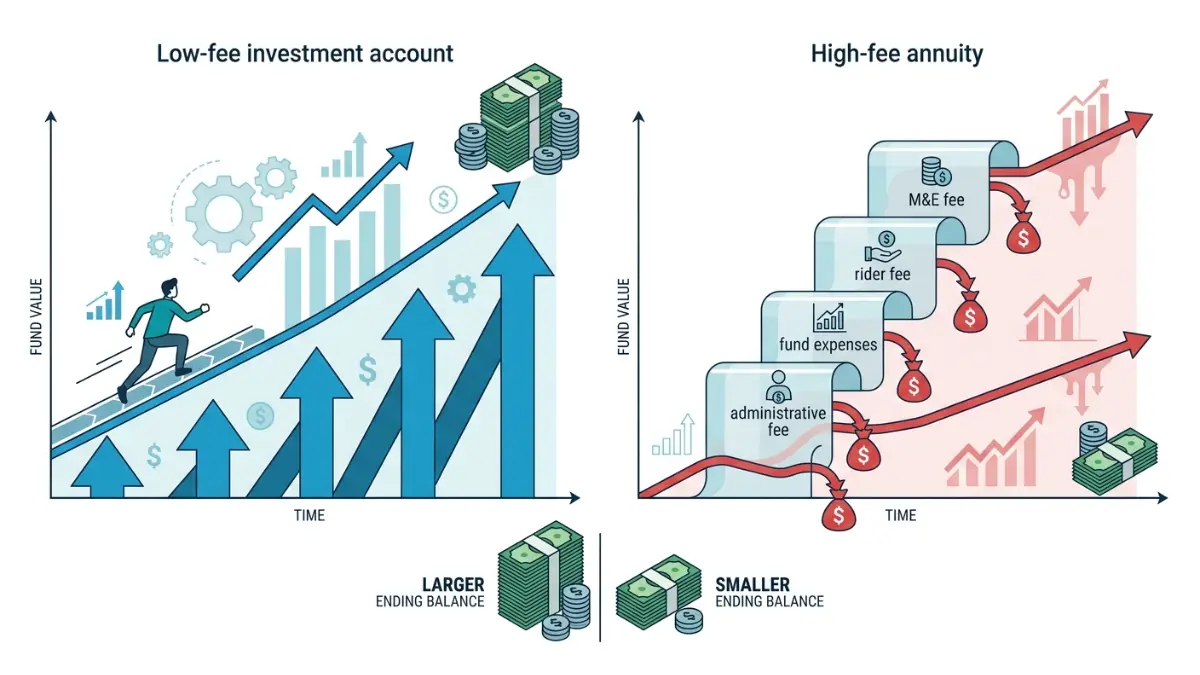

The real cost of an annuity: fees you actually pay

This is the section the sales presentation usually skips, and it is the heart of this guide. The honest cost of an annuity ranges from effectively zero to more than 3% of your money every year, and on a long-held contract that gap compounds into a five-figure difference. The rule of thumb: the simpler the annuity, the lower the cost — and the more guarantees and investment features layered on, the more you pay.

Fixed and MYGA annuities are usually the cheapest. They typically carry no explicit annual fee; the insurer earns its margin on the spread between what it pays you and what it earns investing your premium. The main “cost” is illiquidity — the surrender charge for leaving early — not an ongoing fee.

Variable annuities are the most expensive, because their fees are layered — several charges apply to the same money at once. The major layers, with ranges drawn from SEC, Investor.gov, and insurer disclosures, are:

- Mortality and expense (M&E) risk charge: the base contract fee, typically about 1.00%–1.50% per year (1.25% is a common figure). You pay it for the contract’s insurance guarantees whether or not you ever use them.

- Administrative fees: recordkeeping and maintenance, often around 0.15% per year, sometimes a flat dollar charge.

- Underlying fund (sub-account) expenses: the cost of the investments themselves, commonly around 0.60%–1.00% per year, though some run higher.

- Rider charges: optional guarantees added on top. A guaranteed lifetime withdrawal benefit (GLWB) averages roughly 1.0% per year; an enhanced death benefit roughly 0.5% per year. Individual riders commonly range from 0.25% to 1.50%.

📊 Data Point: Industry data puts the typical all-in cost of a variable annuity at roughly 2.0%–3.0% per year, with the recent industry average near 2.0%–2.3%. A single feature-rich contract can reach about 3.15% per year — for example, a 1.25% M&E charge plus a 0.90% fund expense plus a 1.0% income rider. SEC EDGAR prospectus filings confirm that living-benefit rider fees alone can run from roughly 1.40% up to a contractual maximum of 2.25%. (Sources: SEC/Investor.gov fee guidance; SEC EDGAR variable-annuity prospectus filings; industry fee surveys, 2025–2026.)

Then there are surrender charges, which apply to most deferred annuities — fixed, indexed, and variable alike — if you withdraw more than the allowed amount during the surrender period. According to the SEC’s investor guidance on variable annuities, a typical schedule starts at a 7% charge in the first year and declines about 1 percentage point each year, lasting six to ten years, with a new surrender period beginning for each new premium payment. Most contracts let you withdraw about 10% of the value each year without a surrender charge.

🔍 How It Works: Surrender charges are calculated on the amount you withdraw above the free-withdrawal allowance. Say you put $100,000 into a contract with a 7% first-year surrender charge and a 10% annual free withdrawal, and in year one you need $50,000. The first $10,000 (10% of value) comes out free; the remaining $40,000 is hit with the 7% charge — $2,800 — leaving you that much short. The charge shrinks each year and eventually disappears, which is why annuities are built for money you genuinely won’t need for the length of the surrender term.

Now the original calculation that no product pitch will show you — what these fees actually cost over a decade.

The Real 10-Year Cost of a $100,000 Annuity. Assume $100,000 invested for 10 years, earning a constant 6% gross annual return before fees. (That return is an illustration only; it is not guaranteed, and real variable sub-account returns vary and can be negative.) The only variable below is the annual fee drag:

| Annual fee level | What it represents | Net return | Value after 10 years | Cost of fees vs. low-cost |

|---|---|---|---|---|

| 0.20% | Low-cost index fund (taxable or IRA) | 5.80% | ~$175,800 | — |

| 2.30% | Industry-average variable annuity | 3.70% | ~$143,800 | ~$32,000 |

| 3.15% | Variable annuity + fund + income rider | 2.85% | ~$132,500 | ~$43,300 |

Illustration by FinanceAuthorityHub using fee ranges sourced above; assumes a constant 6% gross return for comparison only. Excludes surrender charges and taxes. Not a projection of any specific product. Verify your contract’s actual fees in its prospectus.

The point is not that variable annuities are always wrong — it is that the fee difference is real, large, and compounding, so the guarantees you’re buying have to be worth roughly $32,000–$43,000 of forgone growth on a $100,000 contract over ten years. For some people — those who genuinely need guaranteed lifetime income and will use the rider — that trade can be worth it. For someone simply seeking tax-deferred growth, a lower-cost path often leaves far more money on the table than the pitch implies.

✅ Action Step: Before buying any annuity with ongoing fees, ask a fee-only fiduciary advisor (CFP® or RIA, verifiable on FINRA BrokerCheck) this exact question: “Add up every annual charge on this contract — M&E, administrative, fund expenses, and each rider — and show me the total percentage and the dollar cost over the years I expect to hold it, next to a lower-cost alternative that meets the same goal.” If the seller won’t itemize it, that is your answer.

💡 Expert Note: FINRA guidance warns specifically about “bonus” or “premium” credits used to entice annuity exchanges — an extra 1%–5% added to your contract value. The catch is that contracts offering bonuses often carry higher ongoing fees or longer surrender periods that can outweigh the bonus, and you may have to repay the bonus in certain cases. A credit on the front end is not free money; price the whole contract.

You can stress-test the fee drag on your own numbers and time horizon with our compound interest and investment growth calculator, adjusting the annual fee to see the difference for yourself.

How much does an annuity pay?

The income an annuity pays depends on four things: how much you put in, your age when payments start, the payout option you choose, and the interest-rate environment when you buy. For an income annuity, both older age and higher rates mean larger monthly checks, because the insurer expects to make payments over fewer years. The figures below are real, dated quotes — but they move with rates and differ by carrier, so treat them as a current snapshot, not a promise.

How much does a $100,000 annuity pay per month?

The clearest starting point is the single premium immediate annuity (SPIA), which turns a lump sum into income that begins within about 30 days. As of mid-2026, a $100,000 life-only SPIA bought at age 65 paid roughly $620–$670 per month for a man and about $575–$640 for a woman, the difference reflecting longer female life expectancy. A joint payout covering two spouses lowers the monthly amount — to roughly $536 for a couple both aged 65 — because the insurer expects to pay across two lifetimes.

📊 Data Point: Based on immediate-annuity quotes for a $100,000 premium as of April–June 2026, a 65-year-old can expect approximately $575–$670 per month for life on a single life-only SPIA, varying by gender and carrier; a joint-life payout for a couple both aged 65 starts near $536 per month. (Source: aggregated SPIA quote data from A-rated carriers, April–June 2026. Quotes vary by carrier, state, and date, and are not guaranteed until a policy is issued.)

Two levers change these numbers. Buying older raises the monthly check — a 70-year-old receives more than a 65-year-old for the same premium. And deferring the start date with a deferred income annuity (DIA) lets the premium grow first, producing a larger payment later. You can see how an income annuity fits alongside Social Security and your other savings using our retirement and 401(k) calculator.

What a payout rate is — and why it is not an interest rate

The figure a seller quotes — say, a “7% payout” — is a payout rate, not an interest rate, and confusing the two is one of the most common annuity misunderstandings. A payout rate is the annual income per dollar of premium, and it blends two things: the interest the insurer earns and a return of your own principal.

🔍 How It Works: A 7% payout rate on a $100,000 SPIA means about $7,000 per year, or roughly $583 per month — but that is not 7% growth on your money. Part of each payment is the insurer returning your own principal; part is interest. The reason an income annuity can pay more per year than a typical “safe withdrawal” strategy is the mortality credit: the insurer pools thousands of contracts, and because some annuitants die earlier than expected, the pool can pay survivors more than their own money alone would support. That pooling is the real engine of lifetime income — and the reason the headline payout figure is not a “return” you could compare to a stock or bond.

Payout options and what your heirs receive

Every income annuity asks you to choose how long, and to whom, it pays. A single life option pays the most each month but stops at your death. A joint life option pays as long as either you or your spouse is alive, for a lower monthly amount. A period-certain feature guarantees payments for a set number of years even if you die early, and a return-of-premium feature ensures your beneficiaries receive at least what you paid in — each protection trims your monthly income.

⚠️ Costly Mistake: Choosing a life-only payout by default without weighing what happens at death. Life-only pays the highest monthly income, but if you die early, payments simply stop and your heirs receive nothing. A period-certain or joint option protects your family at the cost of a lower check — a trade-off to decide deliberately, after seeing both numbers.

✅ Action Step: Before annuitizing any savings, ask a fee-only fiduciary advisor (CFP® or RIA) two specific questions: “How much of my savings should I convert to guaranteed income to cover only my essential, non-negotiable expenses?” and “Show me the monthly income for life-only, joint, and period-certain options side by side, so I can see exactly what each protection costs me.” Annuitizing too much can leave you cash-poor and inflexible; annuitizing too little can leave essentials exposed.

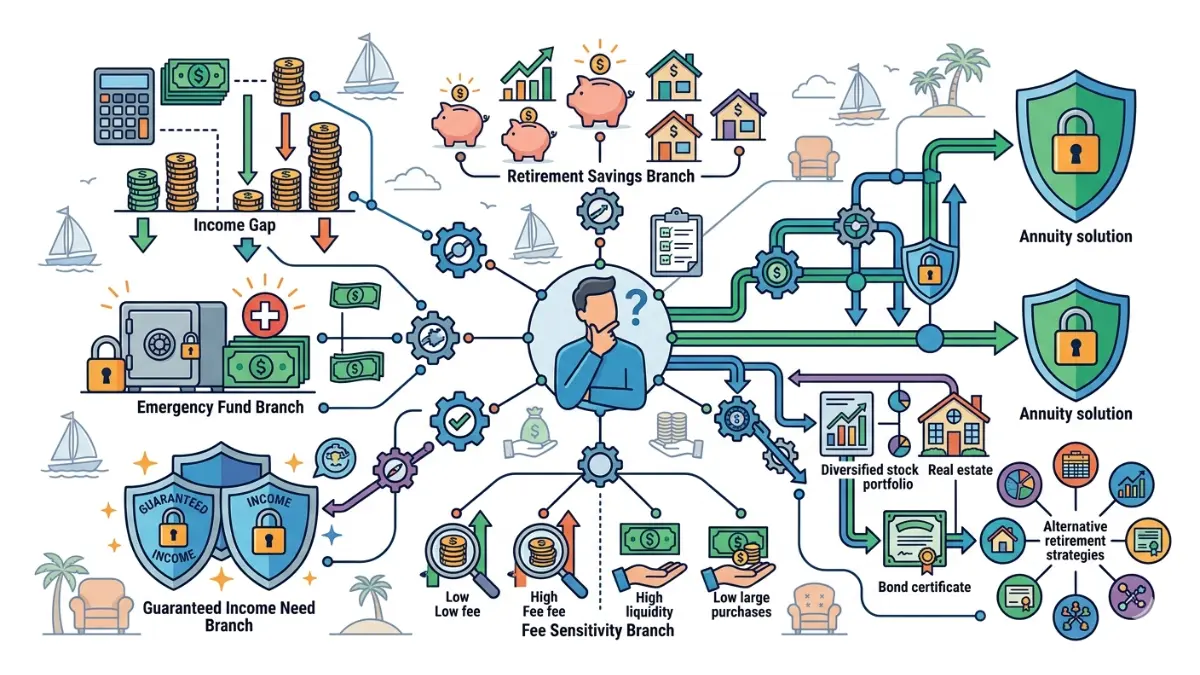

Should you buy an annuity?

This is the question the rest of the guide has been building toward, and the honest answer is that an annuity is the right tool for some people and the wrong one for many. It is not a scam, and it is not a miracle — it is insurance against outliving your money, with a cost attached. The goal here is to give you a clear way to decide, not to push you toward or away from a sale.

When an annuity tends to make sense

An annuity is most defensible when you have essential retirement expenses — housing, food, healthcare, insurance — that are not already covered by Social Security or a pension, and you want those covered for life regardless of how markets behave. It also fits people who are genuinely anxious about outliving their savings and would behave better, and sleep better, with a guaranteed paycheck than with a portfolio they might panic-sell. For these buyers, converting a portion of savings into income can be the difference between a secure retirement and a fearful one.

When an annuity is probably the wrong tool

An annuity is usually the wrong choice if you have not yet filled lower-cost, tax-advantaged accounts like a 401(k) or IRA, if you lack liquid emergency savings outside the contract, or if you are being sold a high-fee variable product mainly for “tax-deferred growth” you could get more cheaply elsewhere. It is also a poor fit if you may need the lump sum during the surrender period, or if the income you would give up to fees and surrender flexibility outweighs the guarantee you would gain. A guarantee you are overpaying for, or one that locks up money you will need, is not protection — it is a cost.

🔍 How It Works — The 6-Gate Annuity Decision Framework. Work through these six questions in order, ideally with a fiduciary, before buying any annuity. They are educational gates, not advice about your specific situation:

- The income-gap gate: After Social Security and any pension, do you have essential expenses that are not covered for life? If no, you may not need guaranteed income at all.

- The lower-cost-accounts gate: Have you already maxed out 401(k), IRA, and HSA space? Tax-deferred growth inside those is usually cheaper than inside an annuity.

- The liquidity gate: Do you have separate emergency savings you will not touch for the length of the surrender period (often 6–10 years)? Check this with our emergency fund calculator before locking money up.

- The simplicity-and-cost gate: Is the product simple and low-cost (a MYGA or a no-frills income annuity), or are you paying 2%–3%+ a year for features you may never use?

- The use-the-guarantee gate: Will you actually use the guarantee you are paying for — the lifetime income or the rider — or are you buying a benefit base you will never draw on?

- The safety gate: Is the insurer highly rated, and is your amount within your state guaranty association’s coverage limit? (More on this in the safety section.)

If you cannot answer “yes” — or “this clearly fits me” — to gates 1, 3, 4, and 5, slow down before signing.

⚠️ Costly Mistake: Putting most or all of your savings into an annuity. Even when an annuity fits, it is meant to cover essential income, not to be your whole plan. Keeping liquid, accessible money outside the contract is what lets you handle a medical bill, a roof, or an opportunity without triggering surrender charges.

For a deeper look at the trade-offs for different situations, see our analysis of whether an annuity is worth it.

Because choosing and sizing an annuity involves product selection and retirement-income sequencing, this is a decision to validate with a credentialed professional rather than a sales representative whose pay depends on the sale.

How annuities are taxed

The tax rules are where annuities surprise people most, in both good ways and bad. The headline benefit is tax-deferred growth; the headline catch is that withdrawals are taxed as ordinary income, and early ones can carry a penalty. Getting this right changes how much of your money you actually keep, so confirm the specifics with a CPA before you act.

Tax-deferred growth and ordinary-income taxation

Money inside an annuity grows without annual taxation — you owe nothing on the interest or gains until you take money out. Unlike a 401(k) or IRA, a non-qualified annuity (funded with after-tax dollars) has no IRS contribution or income limits, which is part of its appeal for high earners who have maxed other accounts. The trade-off arrives at withdrawal: annuity gains are taxed as ordinary income, not at the lower long-term capital-gains rates that apply to most stock investments. The IRS explains the tax treatment of pension and annuity income in its annuities and pension income guidance, Publication 575.

⚠️ Costly Mistake: Assuming annuity growth is taxed like a brokerage account. For a non-qualified annuity, withdrawals come out gains-first (last-in, first-out), so your earliest withdrawals are fully taxable as ordinary income — there is no favorable capital-gains rate, and no step-up that lets you cherry-pick principal first. For some investors in high brackets, this turns a “tax advantage” into a higher lifetime tax bill than a low-turnover index fund would have generated.

The 10% early-withdrawal penalty before 59½

Like other retirement vehicles, annuities discourage early access. If you withdraw taxable gains before age 59½, the IRS generally adds a 10% penalty on top of the ordinary income tax — the same threshold that applies to IRAs and 401(k)s. This is one reason annuities are built for long horizons, and why putting money you might need sooner into one is a costly mismatch.

Qualified vs. non-qualified — and the exclusion ratio

How an annuity is taxed depends on the money that funded it. A qualified annuity is bought with pre-tax retirement money (an IRA or 401(k) rollover), so every dollar of income is taxed as ordinary income. A non-qualified annuity is bought with after-tax money, so only the earnings portion of each payment is taxable; the rest is a tax-free return of your own principal, calculated using the exclusion ratio.

🔍 How It Works: Suppose a 65-year-old buys a $200,000 SPIA with after-tax savings, and the IRS assigns a 20-year (240-month) life expectancy. Dividing the premium by the expected payments — $200,000 ÷ 240 — gives about $833 of each monthly payment as a tax-free return of your own principal; only the amount above that is taxable as ordinary income. Once you outlive the 20-year expectancy, you have fully recovered your principal, so 100% of every later payment becomes taxable. The exclusion ratio is why a non-qualified income annuity can be surprisingly tax-efficient in the early years.

RMDs, and how a QLAC can delay them

If your annuity sits inside a traditional IRA or 401(k), it is subject to required minimum distributions (RMDs), which currently begin at age 73. One specialized product, the qualified longevity annuity contract (QLAC), lets you carve money out of RMD calculations and defer income to as late as age 85.

📊 Data Point: For 2026, you can place up to $210,000 (a per-person lifetime limit) of qualified retirement money into a QLAC, and that amount is excluded from your RMD calculations until income begins. The SECURE 2.0 Act removed the prior 25%-of-balance cap and set the flat, inflation-indexed limit. A QLAC’s income can be deferred to as late as age 85, and the contract can be rescinded within 90 days of purchase without losing its qualified status. (Source: IRS 2026 retirement-plan cost-of-living adjustments; SECURE 2.0 Act provisions; Treasury QLAC regulations.)

You can read more about how withdrawals are forced and timed in our guide to how required minimum distributions work.

The 1035 exchange: switching annuities tax-free

If you already own an annuity that no longer fits — too expensive, a weak rate, a downgraded insurer — you are not stuck. Section 1035 of the tax code lets you exchange one non-qualified annuity for another without triggering tax on the gains, so a move from a 3%-a-year variable annuity to a no-fee MYGA can preserve every dollar of accumulated, tax-deferred growth.

⚠️ Costly Mistake: Cashing out the old annuity yourself to “reinvest” it. If you take the money personally — even briefly — you take constructive receipt, the gains become taxable, and the 10% penalty may apply if you are under 59½. A proper 1035 exchange moves funds insurer-to-insurer; for partial exchanges, the IRS also expects no withdrawals from either contract for 180 days. And the exchange avoids taxes, not surrender charges — your old contract’s surrender fee can still apply, so check it first.

Because qualified-account rules, the exclusion ratio, penalty exceptions, and 1035 mechanics all turn on details specific to your accounts and state, this section is general education, not tax advice. Confirm your numbers with a CPA or tax attorney before acting, and ask specifically: “Given how this annuity was funded and my age, exactly how will each withdrawal be taxed, and will any penalty apply?”

Risks, mistakes, and is your money safe?

Annuities carry real protections and real risks, and an honest page has to name both. The biggest misconceptions are that annuities are federally insured (they are not) and that they are entirely safe (their safety depends on the insurer and on limits you should check). Here is what actually stands behind the guarantee, and where the genuine dangers lie.

Is an annuity safe? Insurer strength and state guaranty associations

An annuity’s guarantee is only as strong as the insurance company behind it, because — unlike a bank CD — an annuity is not FDIC-insured. The first line of safety is the insurer’s own financial strength, which independent agencies such as AM Best rate; most professionals suggest sticking to carriers rated A- or higher for long-term guarantees. Behind the insurer sits a second line: your state guaranty association, which protects policyholders if an insurer fails.

📊 Data Point: State guaranty associations typically cover annuity contracts up to about $250,000 in present value per person, per insurer, though limits vary by state and some are higher. A practical implication: if you plan to place more than that coverage amount in annuities, splitting it across two insurers from different parent companies keeps more of your money within the safety net. (Source: state guaranty association coverage standards; coverage amounts vary by state — confirm your state’s limit.)

💡 Expert Note: SEC and FINRA materials emphasize verifying both the product and the person before buying. You can confirm an insurer’s strength through its AM Best rating, and — for any variable annuity, which is a security — you can check the seller’s license and disciplinary history on FINRA BrokerCheck. Two minutes of verification is cheap insurance against a bad contract or a bad actor.

The liquidity and inflation risks

Beyond insurer failure, two everyday risks matter more for most buyers. The first is liquidity: during the surrender period, getting your money out early triggers surrender charges, so an annuity is the wrong home for funds you may need. The second is inflation: a fixed monthly payment that looks comfortable at 65 buys noticeably less at 80, and adding a cost-of-living rider to offset that lowers your starting income.

⚠️ Costly Mistake: Ignoring inflation on a fixed lifetime payout. A level $625 monthly check does not rise with prices, so its real purchasing power erodes every year. If inflation protection matters to you, price a cost-of-living adjustment rider — but go in knowing it reduces your initial payment, sometimes substantially.

Common annuity mistakes to avoid

Most annuity regret traces back to a short list of avoidable errors. The most frequent are buying chiefly for a “bonus” credit without pricing the higher fees that often accompany it, overlooking the layered fees on a variable contract, annuitizing all of your savings instead of just an income floor, skipping the insurer’s rating, and not reading the surrender schedule before signing. Each is preventable with questions and a day’s patience.

You can see where an annuity should sit within your broader finances using our net worth calculator before committing a large share of your assets.

Your free-look period: the safety valve after you sign

Even after you buy, the law gives you a window to change your mind. Most states require a free-look period, generally lasting 10 to 30 days from when you receive the contract, during which you can cancel for a full refund. It exists precisely so you can have the contract reviewed by someone who does not earn a commission on it.

✅ Action Step: Use the free-look period deliberately. The day your contract arrives, mark the free-look deadline on your calendar, then take the document to a fee-only fiduciary advisor or a CPA and ask: “Does this contract actually do what I was told, and do the fees and surrender terms match the pitch?” If the answer is no, cancel within the window and get your money back.

How to buy an annuity without overpaying

If you have decided an annuity fits, the buying process is where you either get a fair deal or quietly overpay for years. The good news: the steps that protect you are simple, free, and take a few days of patience rather than any special expertise. Work through them in order before you sign anything.

Step 1: Define the job before you shop

Decide what you actually want the annuity to do, because that single choice rules out most products. If you want safe, CD-like growth on money you won’t touch for several years, you are shopping for a MYGA and should ignore variable products entirely. If you want guaranteed lifetime income starting now, you are shopping for an income annuity (a SPIA or DIA), and the comparison is mostly about the monthly payout per dollar.

Step 2: Compare quotes and check the insurer’s rating

Annuity pricing varies meaningfully between carriers, so get quotes from several A-rated insurers rather than buying the first one pitched. For a fixed annuity, compare the guaranteed rate and the minimum guaranteed rate at renewal; for an income annuity, compare the monthly payout for the identical age, premium, and payout option. Then check the insurer’s AM Best financial-strength rating, because the guarantee is only as good as the company behind it.

💡 Expert Note: FINRA’s investor materials stress checking both the product and the person selling it. For any variable annuity — a security — you can review the seller’s license and any disciplinary record on FINRA BrokerCheck, and you can read FINRA’s guidance on annuity exchanges and what to watch for. A reputable seller will welcome the verification; resistance is a warning sign.

Step 3: Read the full fee table and the surrender schedule

Before signing, get every cost in writing, not just the headline rate. For a variable or rider-laden contract, that means the mortality and expense charge, administrative fees, fund expenses, and each rider — totaled as one annual percentage and a dollar figure over your expected holding period. Then read the surrender-charge schedule so you know exactly how long your money is locked and what early access would cost.

⚠️ Costly Mistake: Letting “the rate sounds good” end the conversation. A strong rate paired with a 1% income rider you’ll never use, a 0.90% fund fee, and a 1.25% M&E charge is a contract bleeding more than 3% a year — enough, as the cost section showed, to cost tens of thousands over a decade. The fee table, not the rate, tells you what you’re really buying.

Step 4: Use the free-look period to confirm before you fully commit

Even after you sign, your free-look period gives you 10 to 30 days (depending on your state) to cancel for a full refund. Treat it as a built-in second opinion: have a fee-only professional read the issued contract against what you were promised. If anything fails to match, cancel within the window.

✅ Action Step: Before you buy, have a fee-only fiduciary advisor (CFP® or RIA, verifiable on FINRA BrokerCheck) or a CPA review the specific contract and ask: “Does this product do the job I need at the lowest total cost available, and is there a simpler or cheaper way to get the same guarantee?” Paying a few hundred dollars for one hour of conflict-free review can save you many thousands across the life of the contract.

The 12 questions to ask before you buy any annuity. Bring these to any annuity conversation — the answers separate a fair contract from an expensive one:

- What type of annuity is this — fixed, indexed, variable, or income — and which regulator oversees it?

- What is the guaranteed rate or payout, and what is the minimum guaranteed rate after any initial term?

- List every annual fee — M&E, administrative, fund, and each rider — as a total percentage and a dollar cost over the years I expect to hold it.

- What is the full surrender-charge schedule, and how much can I withdraw each year without a charge?

- Is there a bonus or premium credit, and what higher fees or longer surrender period come attached to it?

- What is the insurer’s AM Best (or comparable) financial-strength rating?

- Is my amount within my state guaranty association’s coverage limit?

- What payout options exist — single life, joint, period-certain, return-of-premium — and what does each pay per month?

- Given how I’m funding this, exactly how will withdrawals and income be taxed, and will any penalty apply?

- What does my family receive if I die before income begins, and after it begins?

- Is there inflation protection available, and how much monthly income does it cost me?

- How are you paid on this product, and can I verify your license on FINRA BrokerCheck?

✅ Action Step: Download our free, printable “12 Questions to Ask Before You Buy Any Annuity” checklist and take it to your next meeting. It turns a sales presentation into an interview you control — and gives you a written record of every answer to review during your free-look period.

Frequently asked questions about annuities

1. What is an annuity in simple terms?

An annuity is a contract with an insurance company: you give it money — a lump sum or a series of payments — and it promises to pay you back later, either for a set number of years or for life. Its defining purpose is turning savings into guaranteed income you cannot outlive. Annuities are insurance products, not bank deposits, and are not FDIC-insured. Speak with a fiduciary advisor before buying.

2. How does an annuity work?

Most annuities have two phases. During the accumulation phase your money grows — at a fixed rate, a market-linked rate, or based on investments you pick. During the distribution phase, the contract pays you, either through withdrawals or by “annuitizing” the balance into scheduled income. Immediate annuities skip ahead and begin paying within about a year. Because the right structure depends on your goals, consult a financial professional first.

3. What are the main types of annuities?

There are fixed annuities (including MYGAs, which guarantee a set rate like a CD), fixed-indexed annuities (market-linked with a 0% floor), and variable annuities (invested in sub-accounts, with market risk and the highest fees). By timing, there are immediate annuities that pay now and deferred annuities that pay later. Each carries different risk, cost, and liquidity, so match the type to your goal with professional guidance.

4. What is the difference between a fixed and a variable annuity?

A fixed annuity pays a guaranteed interest rate and protects your principal, much like a CD, and is overseen by state insurance regulators. A variable annuity invests in market sub-accounts, so its value can fall, and it is a security regulated by the SEC and FINRA — with all-in fees commonly running 2% to 3% or more per year. The right choice depends on your risk tolerance; consult a licensed professional.

5. What is a MYGA?

A multi-year guaranteed annuity (MYGA) is the simplest fixed annuity: you deposit a lump sum and the insurer guarantees a fixed interest rate for a set term, typically 2 to 10 years. Your principal is protected, the rate cannot change during the term, and there are usually no annual fees. The main trade-off is illiquidity during the surrender period. Confirm tax treatment with a CPA before buying.

6. How much does a $100,000 annuity pay per month?

As of April–June 2026, a $100,000 life-only immediate annuity bought at age 65 paid roughly $575 to $670 per month for life, varying by gender and carrier; a joint payout for a couple both 65 started near $536 per month. Older buyers receive more, because payments are expected over fewer years. Quotes vary by carrier, state, and date. Ask a fiduciary advisor how much income to annuitize.

7. What are current annuity rates?

As of June 2026, the best 5-year fixed annuity (MYGA) rates reached about 6.30%, with top A-rated carriers near 5.65% and the single highest fixed rate around 6.50% on a 7-year contract. That compared with roughly 4.20% on a top 5-year CD. Annuity rates change daily and vary by state, so verify the live rate on your purchase date, and consult a professional.

8. How much does an annuity cost?

Fixed and MYGA annuities usually carry no explicit annual fee. Variable annuities are the most expensive, with all-in costs commonly running 2% to 3% or more per year — combining a mortality and expense charge (about 1.00%–1.50%), administrative fees (about 0.15%), fund expenses, and optional rider charges (often 0.25%–1.50%). A feature-rich contract can reach about 3.15% annually. Review the full fee table with a fiduciary before buying.

9. What is a surrender charge?

A surrender charge is a fee for withdrawing more than the allowed amount from a deferred annuity during its surrender period. A typical schedule starts at 7% in the first year and declines about 1 percentage point annually over six to ten years; most contracts let you withdraw about 10% of value each year charge-free. Read the full schedule before signing, and consult a professional about your liquidity needs.

10. Are annuities a good investment?

An annuity is insurance against outliving your money, not a growth investment, so “good” depends on your situation. It can make sense if you have essential expenses not covered by Social Security or a pension and want lifetime income. It is often the wrong choice if you have not maxed lower-cost retirement accounts or need liquidity. Work through the decision with a fee-only fiduciary advisor.

11. How are annuities taxed?

Annuity earnings grow tax-deferred and are taxed as ordinary income — not at capital-gains rates — when withdrawn. A qualified annuity (funded with pre-tax money) is fully taxable on withdrawal; a non-qualified annuity (after-tax money) taxes only the earnings portion, using the exclusion ratio. Withdrawals follow a gains-first order for non-qualified contracts. Because the rules turn on your specifics, confirm with a CPA or tax attorney.

12. Are annuity withdrawals taxed before age 59½?

Yes. If you withdraw taxable gains from an annuity before age 59½, the IRS generally adds a 10% early-withdrawal penalty on top of ordinary income tax — the same threshold that applies to IRAs and 401(k)s. This is a key reason annuities suit long time horizons rather than money you may need sooner. Ask a CPA whether any penalty exceptions apply to your situation.

13. What is a QLAC?

A qualified longevity annuity contract (QLAC) is a deferred income annuity bought with qualified retirement money that delays required minimum distributions and starts income as late as age 85. For 2026, you can place up to $210,000 (a per-person lifetime limit) into a QLAC, and that amount is excluded from RMD calculations until income begins. It can be rescinded within 90 days of purchase. Consult a CPA or fiduciary before using one.

14. Do annuities have required minimum distributions?

An annuity held inside a traditional IRA or 401(k) is subject to required minimum distributions, which currently begin at age 73. A non-qualified annuity (funded with after-tax money) has no RMDs. A QLAC can exclude up to $210,000 of qualified money from RMD calculations until income starts, as late as age 85. Because RMD rules are detailed and penalties are steep, confirm your obligations with a CPA.

15. Can you lose money in an annuity?

Yes, depending on the type. A variable annuity can lose value because your money is invested in market sub-accounts. A fixed or fixed-indexed annuity protects your principal from market losses, though an indexed annuity can credit 0% in a down year. All annuities also carry insurer-failure risk, since they are not FDIC-insured — backed instead by the insurer and your state guaranty association. Discuss safety with a professional.

16. Is a fixed annuity better than a CD?

It depends on your priorities. As of June 2026, top fixed annuities (MYGAs) paid meaningfully more than CDs — roughly 6.30% versus about 4.20% on five-year terms — and annuity interest grows tax-deferred, while CD interest is taxed yearly. The trade-offs are that annuities are less liquid, carry surrender charges, are not FDIC-insured, and can incur a 10% penalty on gains before age 59½. Consult a professional about which fits.

17. How do I buy an annuity safely?

Define what you need the annuity to do, get quotes from several A-rated insurers, and verify the insurer’s financial-strength rating. Read the full fee table and surrender schedule before signing, and for a variable annuity, check the seller’s license on FINRA BrokerCheck. After buying, use your 10-to-30-day free-look period to have a fee-only professional confirm the contract matches the pitch before you commit.

18. What happens to an annuity when you die?

It depends on the payout option. A life-only income annuity stops paying at your death, leaving nothing to heirs. A joint, period-certain, or return-of-premium option continues payments to a spouse or beneficiary, in exchange for a lower monthly amount. A deferred annuity still in its accumulation phase generally passes its value to your named beneficiary. Choose the option deliberately, and review beneficiary details with a financial professional.

What to do before your next money decision

If you’ve read this far, you are doing the single most valuable thing an annuity buyer can do: understanding the product before anyone sells it to you. Whether you’re protecting a maturing CD, building a private pension, or simply trying to decode a pitch you’ve already received, you now know the questions that separate a contract that protects you from one that costs you.

Annuities are neither the villain nor the hero some make them out to be. They are a tool — powerful for someone who needs guaranteed income and is genuinely worried about outliving their savings, and an expensive mismatch for someone who needs growth, liquidity, or lower-cost alternatives they haven’t yet used. The difference is almost always in the fit, the fees, and the fine print.

To go deeper on the decisions ahead, see whether an annuity is worth it for your situation, how a MYGA compares with a CD for safe savings, and the full breakdown of fixed versus variable annuities. And before any meeting, download our “12 Questions to Ask Before You Buy Any Annuity” checklist so the conversation runs on your terms.

The most important step before your next move is one conversation: sit down with a fee-only fiduciary advisor (CFP® or RIA) or a CPA — someone who is not paid a commission on the product — and ask, “Is this annuity the lowest-cost way to meet my actual goal, and what am I giving up to get its guarantee?” That single, conflict-free answer is worth more than any rate quote.

Every figure in this guide is tied to a named, current authority — the Federal Reserve, the IRS, the SEC, Investor.gov, and FINRA — and dated, because a wrong number on a page like this costs real people real money. Rates and quotes are verified as of June 2026 and should be reconfirmed on the day you buy; the high-stakes tax, product-selection, and income sections are written as education and are reviewed before publication by our editorial team against the cited sources.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.