How Annuities Work, and Whether One Is Worth It

How annuities work comes down to two phases and their cost. The honest version: payouts, the 10% penalty before 59½, and the fees that erode returns.

In This Article

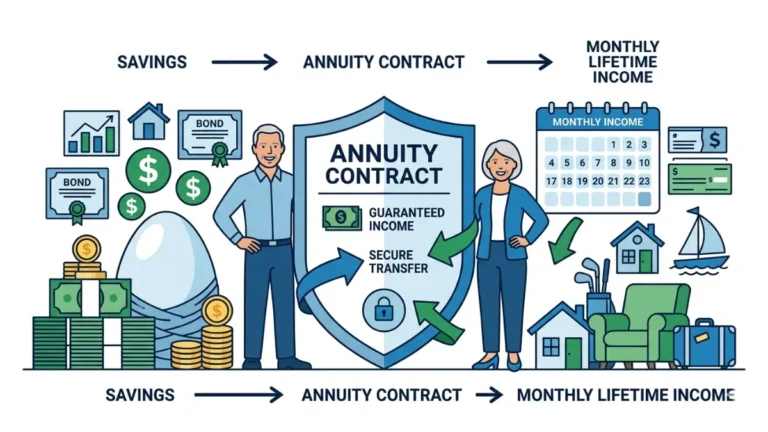

An annuity is a contract with an insurance company: you hand over money now, and it pays you back later — often as guaranteed income you can’t outlive. That single sentence hides a lot of moving parts, which is why the product trips up so many people standing at the edge of retirement.

This guide walks the whole path from premium to payout, and it’s written by people who don’t sell annuities.

If you just rolled over a 401(k) and an advisor floated an annuity, start with the two phases below, then the cost section. If you’re weighing an annuity against a CD or a bond, jump to what they cost and what they pay. If your worry is being locked in or losing money, the risks section is for you. And if you only need the tax rules — the 10% penalty, RMDs, what the IRS takes — that part stands on its own.

Wherever you start, every figure here is tied to a named source you can check yourself.

ℹ️ Financial Disclaimer: This article is general financial education, not personalized advice. Annuities involve investment, tax, insurance, and sometimes credit considerations, and the right choice depends on facts specific to you. Before buying, surrendering, or withdrawing from an annuity, consult a fee-only fiduciary advisor about whether it fits your plan and a CPA or tax attorney about the tax consequences — and read the contract in full. Rates and payouts shown are market snapshots and are not guaranteed until a policy is issued.

How an annuity works: the two phases

An annuity works in two phases: an accumulation phase, when your money grows, and a payout phase, when it turns into income. You fund it with a premium — either one lump sum or a series of payments — and the insurer holds and grows that money until you’re ready to draw on it.

🔍 How It Works: Think of an annuity in two stages. First you put money in and it grows without yearly taxes (accumulation); then you flip a switch and the insurer pays you back as income (payout). Some annuities skip straight to the payout stage — you hand over a lump sum and income starts within about a month.

The accumulation phase (paying in and growing)

During accumulation, your balance grows tax-deferred — you owe no income tax on the gains until you take money out. Depending on the type of annuity, that growth comes from a fixed interest rate, a market index, or underlying investment funds. The longer money compounds untouched, the more the deferral matters; you can estimate how tax-deferred growth builds over time to see the effect.

The payout phase (turning it into income)

When you’re ready, you switch on income — a step called annuitization — and the insurer sends regular payments for a set number of years or for life. You can also take withdrawals instead of fully annuitizing, though how each dollar is taxed depends on whether the contract is qualified or non-qualified, which the tax section covers. For the wider overview of income options and real costs, see our guide to what an annuity is and what it really costs.

The main types of annuities (and how each one works)

The main types of annuities differ by how your money grows and how much risk you carry. Here’s the short version, with what you trade away in each:

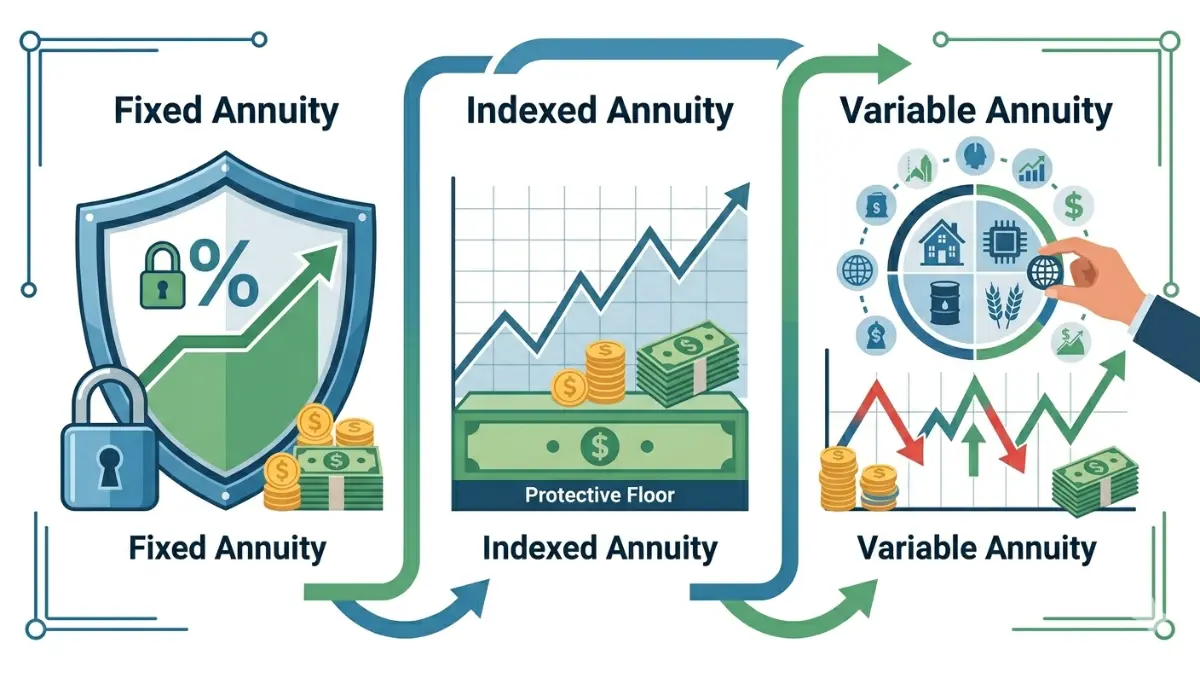

- Fixed / MYGA: a guaranteed interest rate for a set term — the simplest and most predictable, but the rate is capped and your money is committed.

- Fixed index: interest tied to a market index (like the S&P 500) with a 0% floor, so a market drop won’t cut your principal — but gains are limited by a cap or participation rate.

- Variable: your money goes into investment subaccounts; the highest growth potential, real risk of loss, and the highest fees.

- Immediate vs. deferred: an immediate annuity starts paying within about a month of a lump-sum purchase, while a deferred annuity grows first and pays later.

Variable and registered index-linked annuities are securities — regulated by the SEC and FINRA, not just state insurance departments — so they come with a prospectus and extra disclosures, as the SEC’s investor guidance on variable annuities explains. A deeper feature-by-feature breakdown sits in our closer look at annuity types.

✅ Action Step: No single type is “best” — suitability depends on your time horizon, income needs, and risk tolerance. Before committing, ask a fee-only fiduciary advisor: “Given my goals and how soon I’ll need this money, which type fits — and what does it cost me all-in versus a simpler alternative?”

What annuities cost — and what they pay

Annuities carry two kinds of cost: charges to get out early, and ongoing fees while you’re in. What they pay back depends on the type, your age, and current interest rates.

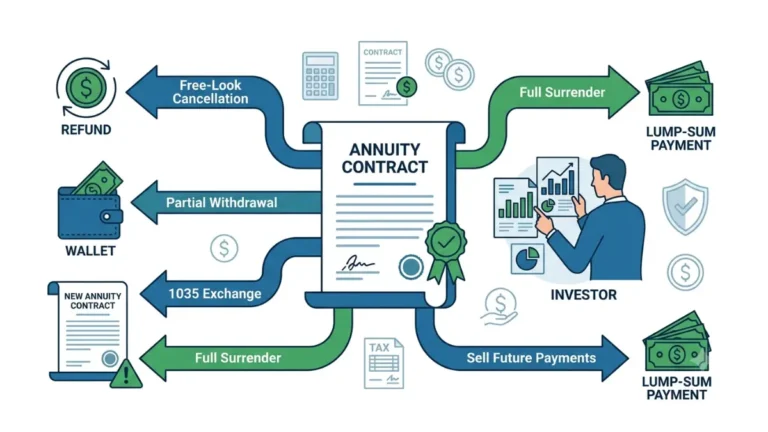

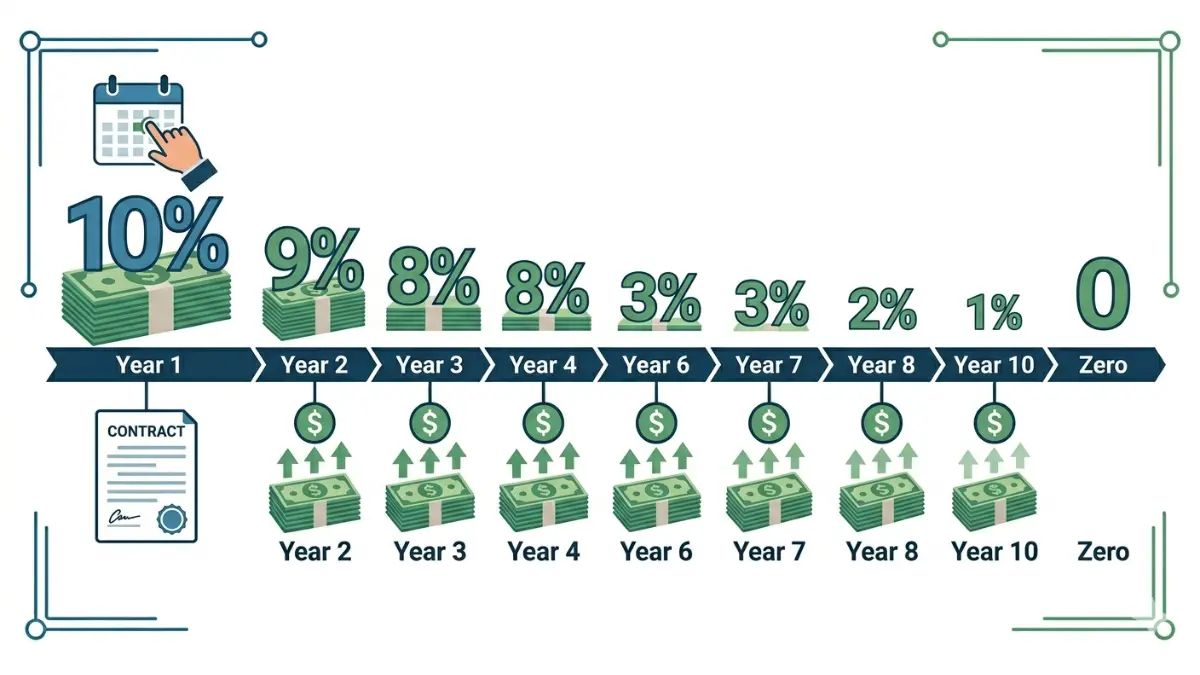

Surrender charges and the surrender period

A surrender charge is a fee for taking out more than your contract allows during an early window called the surrender period. Industry schedules commonly start around 6–10% in year one and decline to zero over roughly three to ten years, and most contracts let you withdraw about 10% of value each year penalty-free. Variable annuities can have surrender periods of eight years or more.

🔍 How It Works: Say a contract has a 7% first-year surrender charge and you pull out $50,000 above your penalty-free amount. The fee is 7% × $50,000 = $3,500, deducted from what you receive. The charge typically drops about one point a year until it reaches zero.

Ongoing fees and what it pays

Variable annuities stack fees — mortality and expense charges, administrative fees, underlying fund expenses, and rider costs — that can run roughly 2–3%+ a year and quietly erode returns; fixed annuities and MYGAs typically carry no explicit annual fee. As a mid-2026 market snapshot, an immediate annuity rate for a 65-year-old buying $100,000 of life-only income produced rough payouts in the low-$600s a month for a man and the high-$500s to low-$600s for a woman, per industry rate surveys — figures that vary by carrier and state and aren’t locked until the policy is issued. You can compare a fixed annuity’s rate against current CD rates to see how the guarantee stacks up.

⚠️ Costly Mistake: A “7% payout rate” is not 7% interest. Much of each immediate-annuity payment is simply your own principal handed back to you. Comparing an annuity’s payout rate to a CD’s interest rate makes the annuity look far more generous than it actually is.

For how each fee works, FINRA’s overview of annuity fees and types is a neutral reference, and you can weigh the payout against how bonds work as a fixed-income option.

How annuity income is taxed (and the rules that bite)

You can generally withdraw from an annuity without the IRS’s early-withdrawal penalty once you reach age 59½; before that, the taxable portion usually faces an extra 10% tax on top of income tax, per the IRS rules on pensions and annuities. How much of a withdrawal is taxable comes down to one distinction.

Qualified vs. non-qualified — and why it changes your taxes

A qualified annuity is funded with pre-tax money (like IRA or 401(k) dollars), so every dollar withdrawn is taxed as ordinary income. A non-qualified annuity is funded with after-tax money, so only the earnings are taxed — and the IRS treats earnings as coming out first. The same pre-tax logic governs how qualified retirement accounts like IRAs and 401(k)s are taxed.

The 59½ rule, the 10% penalty, and RMDs

The 10% penalty has exceptions — including death, disability, and a series of substantially equal periodic payments. Separately, money in qualified annuities is subject to required minimum distributions: under SECURE 2.0, RMDs generally begin at age 73 for people born 1951–1959 (rising to 75 for those born in 1960 or later), per IRS Publication 590-B. You can estimate your retirement income and when RMDs start ahead of time.

✅ Action Step: Whether your annuity is qualified or non-qualified changes your tax bill significantly. Before taking a withdrawal, ask a CPA: “Given my contract type and age, how will this distribution be taxed, and will the 10% penalty apply to any of it?”

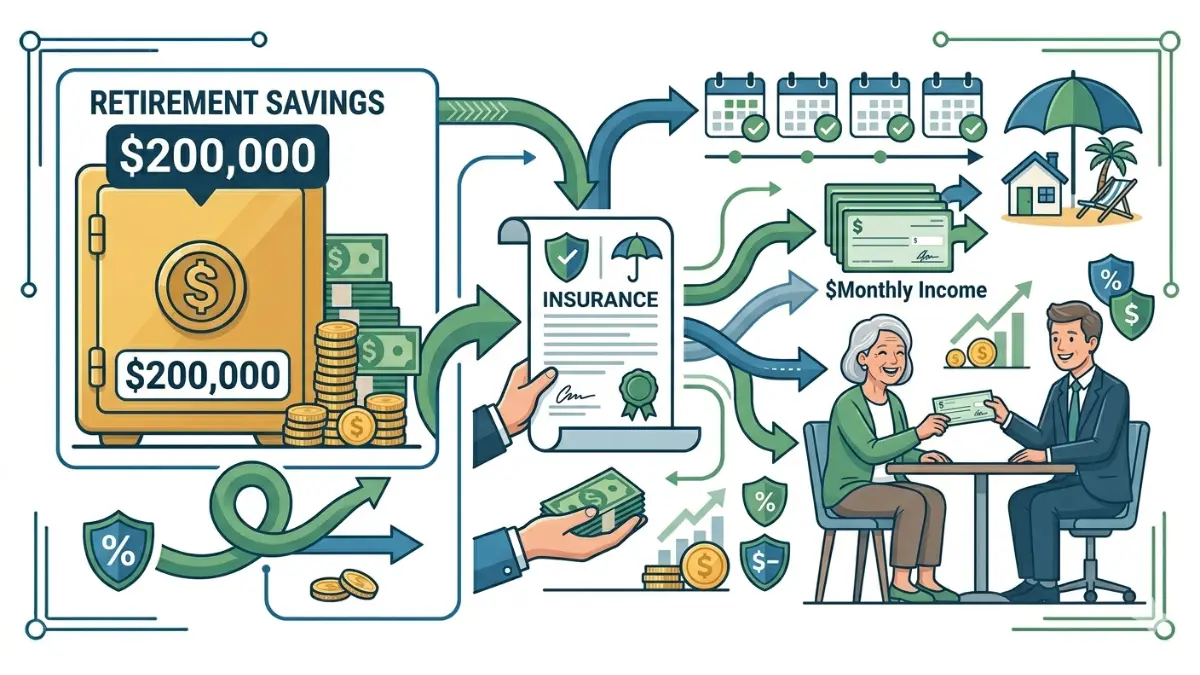

A real example: from a $200,000 premium to a monthly check

Here is how one premium becomes income, with the tax math shown. The numbers are illustrative — not a quote — but the method is the IRS’s own.

The setup and the monthly payout

Picture a 65-year-old who puts $200,000 of after-tax savings — a non-qualified contract — into an immediate, life-only annuity. At mid-2026 payout rates, that might generate roughly $1,200 a month for life. Because the money was already taxed once, only part of each payment is taxable now.

How the IRS splits each payment (the exclusion ratio)

For a non-qualified commercial annuity, the IRS uses its General Rule to set an exclusion ratio — the share of each payment that’s a tax-free return of your own principal.

🔍 How It Works: The exclusion ratio is your investment divided by the total income you’re expected to receive. With $200,000 paid in and an expected return of about $288,000 ($1,200 × 12 months × roughly 20 years of IRS-table life expectancy), the ratio is about 69% ($200,000 ÷ $288,000). So roughly 69% of each $1,200 payment — close to $833 — comes back tax-free, and the remaining ~$367 is taxable.

When the payments become fully taxable

That ~$833 stays tax-free only until you’ve recovered your full $200,000 — here, after about 240 payments, around age 85. After that, 100% of each payment is taxable as ordinary income, as IRS Publication 575 explains. If you die before recovering your full cost, the unrecovered amount can be claimed as a deduction on your final return.

Risks, mistakes, and what an annuity does not guarantee

Annuities reduce some risks — like outliving your savings — but they carry others worth naming plainly.

Can you lose money in an annuity?

Yes. Variable annuities can lose value when markets fall, index annuities can credit 0% in a bad year, and fees reduce what you keep. A fixed payment also loses purchasing power to inflation unless you add a costly inflation rider — you can see how inflation erodes a fixed amount over time.

Are annuities FDIC insured?

No — annuities are not FDIC insured. They are backed by the issuing insurer’s claims-paying ability and, as a backstop, by your state’s guaranty association.

📊 Data Point: Most states protect at least $250,000 in present value of annuity benefits per owner, per insurer, if an insurer fails — Source: NAIC Life & Health Insurance Guaranty Association Model Act (#520). Coverage is per owner, not per contract, and some states protect more; check your own state’s guaranty association.

The most common buyer mistakes

The big ones: surrendering early and eating the charge, buying complexity (and fees) you don’t need, and locking up money you’ll need for emergencies. Annuitizing trades liquidity for income — the same lump-sum-versus-stream decision covered in our lump sum vs. payment stream guide.

Frequently asked questions about how annuities work

1. How do annuities work in simple terms?

An annuity is a contract with an insurance company that works in two phases. You pay in — a lump sum or installments — and the money grows tax-deferred during the accumulation phase. Then you switch on income, and the insurer pays you regular amounts for a set period or for life.

2. How much does a $100,000 annuity pay per month?

It depends on your age, sex, payout option, and current rates. As a mid-2026 snapshot, a 65-year-old buying $100,000 of life-only income saw roughly the low-$600s a month (men) or high-$500s to low-$600s (women). These vary by carrier and aren’t guaranteed until issue; confirm current quotes with a licensed agent.

3. What are the main types of annuities?

The main types are fixed (including multi-year guaranteed, or MYGA), fixed index, and variable — and any of these can be immediate or deferred. Fixed offers a guaranteed rate, index ties gains to a market benchmark with a floor, and variable invests in subaccounts with higher risk and higher fees.

4. Are annuities a good investment?

It depends on what you need them for. An annuity can be worth it if guaranteed lifetime income matters more to you than liquidity and growth; it is a poor fit if you’ll need the money soon or want low fees. Discuss the trade-off with a fee-only fiduciary advisor before deciding.

5. How are annuities taxed?

Earnings are taxed as ordinary income, not at capital-gains rates. A qualified annuity (pre-tax money) is fully taxable on withdrawal, while a non-qualified annuity (after-tax money) taxes only the earnings, which come out first. Confirm your situation with a CPA, since the contract type changes the result.

6. Can you lose money in an annuity?

Yes. Variable annuities can lose value in down markets, index annuities can credit 0% in a bad year, and fees reduce your returns. Surrendering early also triggers charges, and a fixed payment can lose purchasing power to inflation. For product-specific risk, consult a fiduciary advisor before buying.

7. What is the surrender period on an annuity?

The surrender period is the early window — commonly three to ten years — when withdrawing more than your penalty-free amount triggers a surrender charge. Charges often start around 6–10% and decline to zero over that period. Most contracts allow about 10% of value to be withdrawn each year without a charge.

8. When can you withdraw from an annuity without the 10% penalty?

Generally at age 59½. Withdrawing the taxable portion before then usually adds an extra 10% IRS tax, with exceptions such as death, disability, or substantially equal periodic payments. Any surrender charge from the insurer is separate from this IRS penalty. Ask a CPA whether an exception applies to you.

9. Are annuities FDIC insured?

No. Annuities are not FDIC insured; they are backed by the issuing insurer’s claims-paying ability. As a backstop, state guaranty associations typically protect at least $250,000 in annuity value per owner, per insurer, though limits vary by state. Checking the insurer’s financial-strength rating is a sensible precaution.

10. What’s the difference between a qualified and non-qualified annuity?

A qualified annuity is funded with pre-tax dollars (like IRA or 401(k) money), so the entire withdrawal is taxable. A non-qualified annuity uses after-tax dollars, so only the earnings portion is taxed. The distinction also affects required minimum distributions, so confirm the tax impact with a CPA.

11. Do you pay RMDs on an annuity?

Qualified annuities follow required minimum distribution rules: under SECURE 2.0, withdrawals generally must begin at age 73 (rising to 75 for those born in 1960 or later). Non-qualified annuities generally have no lifetime RMDs. Because the penalty for missing an RMD is steep, confirm your timing with a CPA.

The bottom line on how annuities work

An annuity is a trade: you give up some control and simplicity in exchange for guaranteed income you can’t outlive. That trade is right for some retirees and wrong for others, and the deciding factors are your need for liquidity, your tolerance for fees, and how much guaranteed income you already have from Social Security and any pension.

Before you sign anything, get the full surrender schedule and all-in costs in writing, run your own numbers, and talk the fit through with a fee-only fiduciary advisor and a CPA. To see where an annuity might sit alongside the rest of your plan, review retirement savings benchmarks by age.

Grab our “10 Questions to Ask Before You Buy an Annuity” checklist before that conversation.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.