What Is a Bond? The Investing Secret That Pays You

Bonds pay you steady fixed interest while keeping your money safer than stocks. Discover all bond types, 2026 yields & how to buy your first bond today.

In This Article

What Is a Bond? The Answer in 60 Words

A bond is a loan you give to a government or corporation in exchange for fixed interest payments. You receive regular coupon payments throughout the bond’s life, and get your original investment — the principal — returned when the bond matures. Bonds are the core of fixed-income investing and one of the most reliable ways to generate steady income from your portfolio.

📊 February 2026 Market Signal: The 10-year U.S. Treasury bond yield hit 4.12% on February 13, 2026. The Fed held its benchmark rate at 3.50–3.75% on January 28, 2026. Bond ETFs pulled in over $330 billion in 2025 — roughly one-third of all ETF inflows that year. This is the bond moment investors have been waiting for.

What You’ll Learn in This Guide:

- Exactly how bonds pay you (with a real $10,000 example)

- All 8 bond types, their risks, and 2026 yields

- Bonds vs. stocks vs. CDs — the definitive comparison

- A 5-step beginner’s action plan to start investing today

- 11 expert-answered FAQs covering every common question

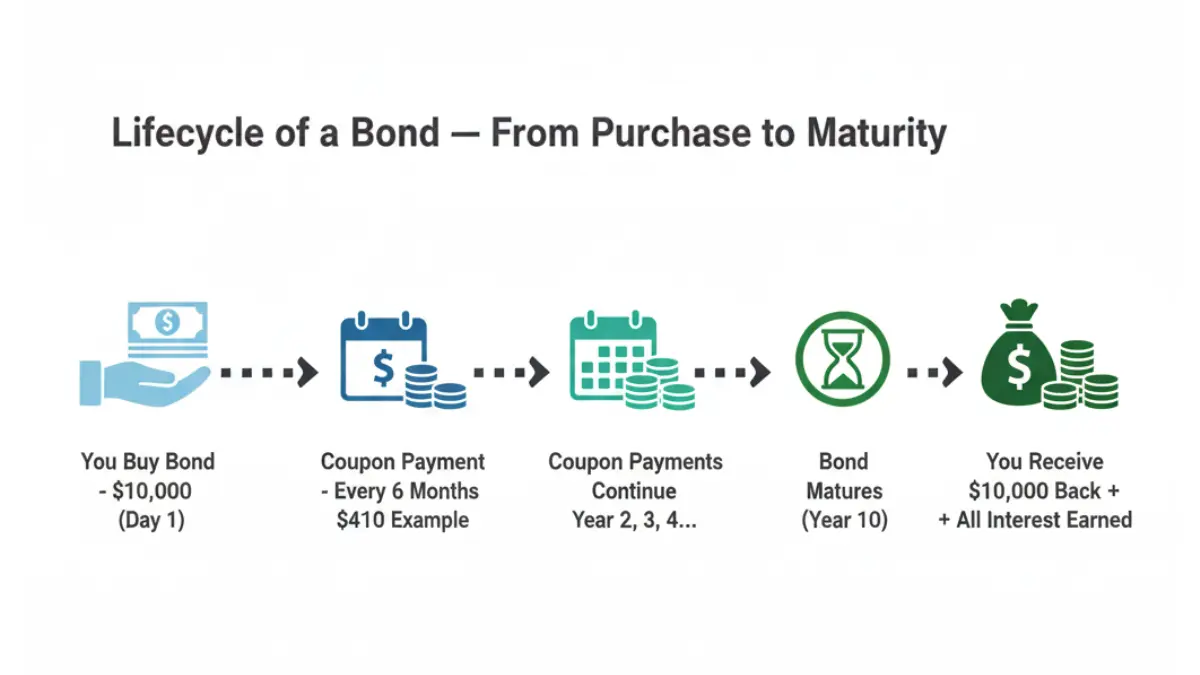

How Does a Bond Actually Pay You? Step-by-Step

Understanding how bonds work is simpler than most finance sites make it. Here’s the clean breakdown.

The Bond Lifecycle

Step 1 — You lend money: You buy a bond at its face value (typically $1,000).

Step 2 — You earn coupon payments: The issuer pays you fixed interest — usually every 6 months — called a “coupon.”

Step 3 — Bond matures: At the end of the term, the issuer repays your full principal. You’ve earned income the entire time it was outstanding.

Real $10,000 Example — What You Actually Earn

| Bond Type | Amount Invested | Coupon Rate | Annual Income | Term | Total Income Earned |

|---|---|---|---|---|---|

| Treasury Bond | $10,000 | 4.1% | $410/yr | 10 years | $4,100 |

| Corporate Bond | $10,000 | 5.5% | $550/yr | 5 years | $2,750 |

| Municipal Bond | $10,000 | 3.6% (tax-free) | $360/yr | 7 years | $2,520 |

| High-Yield Bond | $10,000 | 7.5% | $750/yr | 5 years | $3,750 |

These are income-only figures. You also receive your $10,000 principal back at maturity in each case.

Key Bond Terms — Decoded

- Par Value (Face Value): The amount you lend, and receive back at maturity. Usually $1,000.

- Coupon Rate: The annual interest rate the issuer agrees to pay you.

- Maturity Date: When the issuer repays your principal. Terms range from 1 to 30 years.

- Bond Yield: The return you actually earn, accounting for the price you paid. Bond prices and yields move in opposite directions.

- Credit Rating: A grade from agencies like Moody’s or S&P showing how likely the issuer is to repay you.

💡 What This Means For You: If you’re currently using a savings account paying under 2%, a 10-year Treasury bond at 4.1% nearly doubles your income — with government-backed safety.

According to the U.S. Securities and Exchange Commission’s Investor.gov, bonds provide investors with predictable income, capital preservation, and a counterbalance to volatile stock holdings.

8 Types of Bonds — Which One Is Right for You in 2026?

Not all bonds are equal. Understanding the differences determines how much you earn — and how much risk you take.

The 2026 Bond Type Comparison Table

| Bond Type | Issuer | Risk Level | 2026 Yield Range | Tax Advantage | Best For |

|---|---|---|---|---|---|

| Treasury Bond | U.S. Government | ⭐ Very Low | 4.1%–4.8% | State/local tax-exempt | Safety-first investors |

| Treasury Note | U.S. Government | ⭐ Very Low | 3.9%–4.3% | State/local tax-exempt | Short-to-mid term income |

| Municipal Bond | State/Local Gov | 🟢 Low | 3.4%–4.2% | Federal tax-free | High-income earners |

| Corporate Bond | Corporations | 🟡 Medium | 4.5%–6.5% | None | Income seekers |

| High-Yield Bond | Low-rated corps | 🔴 High | 7%–9%+ | None | Risk-tolerant investors |

| I-Bond (Savings) | U.S. Treasury | ⭐ Very Low | 4.03% (Nov 2025–Apr 2026) | Federal tax-deferred | Inflation protection |

| TIPS | U.S. Treasury | ⭐ Very Low | ~2% real yield | State/local tax-exempt | Inflation hedgers |

| Bond ETF | Fund basket | 🟢 Low–Med | Varies (3%–7%) | Depends on holdings | Beginners |

The 4 Most Important Bond Types — Quick Deep Dives

🏛️ Treasury Bonds Treasury bonds are issued by the U.S. government and backed by its full faith and credit. The 30-year T-bond yields around 4.79% as of February 12, 2026. You can buy them for as little as $100 directly through TreasuryDirect.gov, the official U.S. government platform — with zero broker fees.

🏢 Corporate Bonds Corporations issue bonds to fund expansion, acquisitions, or operations. Investment-grade corporate bonds (rated BBB or higher) currently yield 4.5%–6.5%. They carry more risk than Treasuries, but pay meaningfully higher coupons. Before investing, always verify the bond’s credit rating through Moody’s or S&P.

🏙️ Municipal Bonds Municipal bonds — “munis” — are issued by states, cities, and local governments. Their defining advantage: interest is typically exempt from federal income tax, and often state and local taxes too. For investors in high tax brackets, the after-tax yield on munis frequently beats corporate bonds. A muni paying 3.6% tax-free can equal a corporate bond paying 5%+ for a taxpayer in the 32% bracket.

⚡ High-Yield Bonds High-yield bonds (formerly called “junk bonds”) are issued by companies with lower credit ratings. They pay 7–9%+ in 2026 — but carry real default risk. These bonds are not for beginners. Only suitable for investors who can tolerate losses and understand credit analysis. If you’re exploring higher-yield strategies, also read our guide on derivatives and risk-adjusted returns.

📊 Expert Insight: “In 2026’s rate environment, intermediate-term investment-grade bonds offer the most compelling risk-reward balance for individual investors. Treasury bonds provide income stability, while corporate bonds offer meaningful yield pickup for those who understand credit quality.” — FinanceAuthorityHub.com Senior Investment Analyst, CFA

Bonds vs. Stocks vs. CDs — The 2026 Comparison That Settles the Debate

One of the most common investor questions: should I own bonds instead of stocks or CDs? The honest answer: it depends on your goal, timeline, and risk tolerance.

Side-by-Side: Bonds vs. Stocks vs. CDs in 2026

| Factor | Bonds | Stocks | CDs |

|---|---|---|---|

| Average Return | 4%–9% | ~10% (long-term historical) | 4.5%–5.2% |

| Risk Level | Low–Medium | High | Very Low |

| Income Type | Fixed coupon payments | Dividends + capital gains | Fixed interest |

| Liquidity | Moderate (secondary market) | High (daily trading) | Low (penalty if early exit) |

| Government Protected | Gov bonds: Yes | No | Yes (FDIC up to $250K) |

| Best Environment | Rising rates → falling prices; stable rates → best income | Bull markets, long horizons | Stable or falling rate periods |

| Inflation Protection | TIPS only | Partial via earnings growth | None |

The 5 Bond Risks Every Investor Must Know

Understanding risk is as important as chasing yield. These are the five you cannot ignore:

- Interest Rate Risk: When interest rates rise, existing bond prices fall. This is the most common risk for bond holders. Shorter-term bonds are less affected.

- Credit/Default Risk: If the bond issuer can’t make payments, you may lose income — or principal. Always check credit ratings before buying.

- Inflation Risk: If inflation runs higher than your coupon rate, your real purchasing power shrinks. TIPS bonds solve this problem.

- Liquidity Risk: Some bonds — especially corporate or municipal — can be hard to sell quickly without accepting a discount.

- Call Risk: Some bonds let issuers “call” (repay early) before maturity, cutting off your income stream if rates fall.

💡 What This Means For You: A balanced investor portfolio typically holds both stocks and bonds. According to Vanguard’s Portfolio Allocation Models, adding bonds can reduce portfolio volatility significantly during stock market downturns. If you’re managing mortgage debt alongside investments, use our mortgage calculator to see how your debt obligations affect how much capital you can allocate to bonds.

Understanding how bond income interacts with your broader tax picture is critical — especially if you’re evaluating capital gains tax in 2026 when selling bonds before maturity.

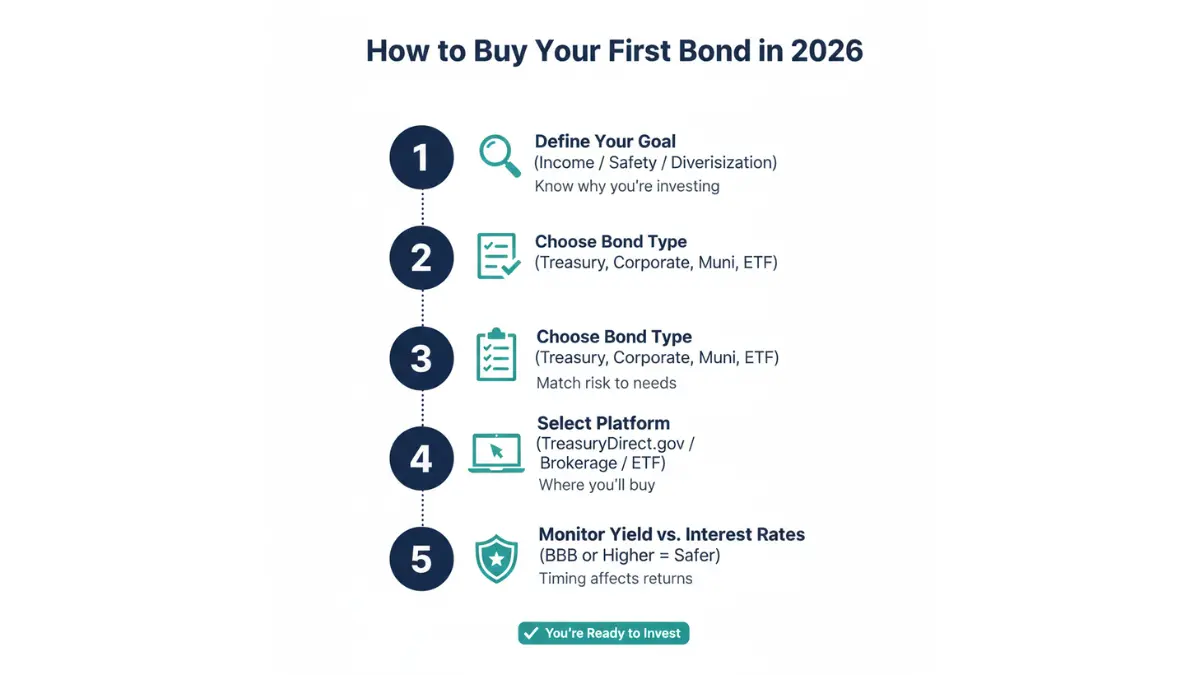

How to Buy Bonds in 2026 — Your 5-Step Beginner’s Playbook

No jargon. No fluff. Just the exact steps a first-time bond investor needs to take today.

Step 1: Define Your Goal

Ask yourself: Am I investing for income, safety, or portfolio diversification? Your answer determines which bond type fits your needs.

- Income focus → Corporate bonds or high-yield bonds

- Safety first → Treasury bonds or municipal bonds

- Inflation protection → TIPS or I-Bonds

- Balanced diversification → Bond ETF (lowest barrier to entry)

Step 2: Choose Your Bond Type

Use the comparison table in Section 3. If you’re unsure, a Bond ETF like Vanguard’s BND or iShares AGG gives you instant exposure to thousands of bonds with a single purchase, starting under $100.

Step 3: Pick Your Buying Method

| Method | Best For | Minimum | Fee |

|---|---|---|---|

| TreasuryDirect.gov | Treasury bonds + I-Bonds | $100–$25 | $0 (free) |

| Brokerage Account | Corporate + municipal bonds | Varies ($1,000+) | Low commission |

| Bond ETF | Beginners, diversification | Price of 1 share (~$75–$100) | Low expense ratio |

| Bond Mutual Fund | Long-term, managed approach | Often $500–$3,000 | Annual management fee |

You can purchase U.S. Treasury bonds directly with zero broker fees through TreasuryDirect.gov, the official U.S. government platform — the single safest and cheapest option for government bonds.

Step 4: Check the Bond’s Credit Rating

| Rating (S&P) | Rating (Moody’s) | Meaning | Risk Level |

|---|---|---|---|

| AAA | Aaa | Highest quality | Very Low |

| AA | Aa | High quality | Very Low |

| A | A | Strong | Low |

| BBB | Baa | Investment grade floor | Low–Medium |

| BB and below | Ba and below | High-yield / Junk | High |

Rule of thumb: For most individual investors, stick to bonds rated BBB or higher. Below BBB = high-yield territory, with meaningfully higher default probability.

Step 5: Monitor Your Bond Portfolio

- Watch the Fed’s rate decisions — these directly impact your bond prices

- Review your bond’s duration (how sensitive it is to interest rate changes)

- Rebalance annually if your stock-to-bond ratio drifts significantly

- For investors nearing retirement, gradually increasing bond allocation reduces risk

💡 Should You Buy Bonds in February 2026?

- Fed held rates at 3.50–3.75% on January 28, 2026

- 10-year Treasury: 4.12% (February 13, 2026)

- 30-year Treasury: 4.79% (February 12, 2026)

- Markets currently pricing 2 rate cuts in 2026 (June + September)

Expert verdict: With two rate cuts expected this year, bond prices are likely to rise as rates fall. Buying now — before cuts arrive — locks in today’s higher yields and creates potential for capital appreciation. This is the same principle that makes bonds attractive ahead of rate-cutting cycles.

If you’re building a broader retirement strategy, see our guide on retirement planning in your 30s and how bonds fit into a long-term wealth-building plan. For those exploring equity income alongside bonds, our index funds vs. mutual funds breakdown is worth reading alongside this guide.

11 Expert-Answered FAQs About Bonds

Q1: What is a bond in simple terms?

A bond is a loan you give to a government or company. In return, they pay you fixed interest on a schedule, then return your original money when the loan term ends.

Q2: How does a bond make money for me?

Bonds pay you in two ways: (1) regular coupon payments throughout the bond’s life, and (2) the return of your principal at maturity. If you sell before maturity and prices have risen, you may also earn a capital gain.

Q3: Are bonds safer than stocks?

Generally yes. Bonds provide fixed, contractual payments and rank ahead of stockholders in the event of bankruptcy. However, bond prices can still fall if interest rates rise, and high-yield bonds carry real default risk.

Q4: What is a bond yield?

Bond yield is the return you earn on a bond. It’s calculated by dividing the annual coupon payment by the bond’s current price. When bond prices rise, yields fall — and vice versa. The 10-year Treasury yielded 4.12% on February 13, 2026.

Q5: What happens when a bond matures?

When a bond matures, the issuer repays you the full face value (par value) — typically $1,000 per bond. You keep all the interest you earned throughout the term. Nothing additional happens; the investment simply ends.

Q6: What is the minimum amount to invest in bonds?

– U.S. Treasury bonds: $100 via TreasuryDirect.gov

– I-Bonds (savings bonds): $25 via TreasuryDirect.gov

– Corporate/municipal bonds: Typically $1,000 minimum

– Bond ETFs: As low as the price of one share (~$75–$100)

Q7: Are bonds a good investment in 2026?

Yes — particularly for income-focused and risk-conscious investors. With Treasury yields at 4.1%–4.8% and two rate cuts expected, bonds offer both income and potential price appreciation. This environment closely mirrors the conditions preceding the strong bond rallies of 2019 and 2024.

Q8: What is the difference between a bond and a stock?

A stock makes you a part-owner of a company. A bond makes you a creditor — you lend money and receive fixed interest. Stocks offer higher potential returns but more volatility. Bonds offer lower, predictable returns with significantly less risk. Most financial advisors recommend holding both.

Q9: What is a junk bond?

A junk bond (officially “high-yield bond”) is issued by a company with a credit rating below BBB (S&P) or Baa (Moody’s). They pay higher yields (7–9%+ in 2026) to compensate for higher default risk. Not recommended for conservative or beginner investors.

Q10: How do rising interest rates affect bond prices?

When interest rates rise, existing bond prices fall — because newly issued bonds offer better rates, making older bonds less attractive. When rates fall, existing bond prices rise. This is the most important relationship to understand in bond investing.

Q11: Can I lose money investing in bonds?

Yes. You can lose money if: (1) you sell before maturity when prices have dropped due to rising rates, (2) the bond issuer defaults on payments, or (3) inflation outpaces your bond’s coupon rate. U.S. government bonds are considered near-zero default risk — but not zero price risk if sold early.

📋 Disclaimer: This article is for educational purposes only and does not constitute financial advice or a recommendation to buy or sell any investment. Bond investing involves risk, including potential loss of principal. Past performance does not guarantee future results. Interest rates and yields are subject to change. Always consult a qualified, licensed financial advisor before making investment decisions. Data cited reflects market conditions as of February 13, 2026.

Explore more on financeauthorityhub.com: How to Start Investing with $100 · What Is Compound Interest · 401(k) vs IRA — Which to Max First · Roth IRA 2026 Complete Guide

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.