Treasury Bill (T-Bill): What It Is, Current Rates & How to Buy in 2026

Treasury Bill rates range from 3.63% to 4.15% in February 2026. Discover what T-Bills are, how the discount works, and how to start buying with just $100.

In This Article

Quick Answer: A Treasury bill (T-bill) is a short-term U.S. government debt security that matures in 4 weeks to 1 year. You buy it below face value and receive the full amount at maturity — the difference is your return. As of February 2026, T-bill yields range from 3.63% to ~4.15% depending on the term you choose.

What Is a Treasury Bill?

A Treasury bill — also called a T-bill — is a short-term debt security issued by the U.S. Department of the Treasury to fund government operations. Unlike stocks or bonds, T-bills don’t pay regular interest. Instead, you buy them at a discount below face value, and at maturity, the government pays you the full face value.

The difference between what you paid and what you receive is your profit. It’s simple, safe, and backed by the full faith and credit of the U.S. government — making it one of the lowest-risk investments available to American investors today.

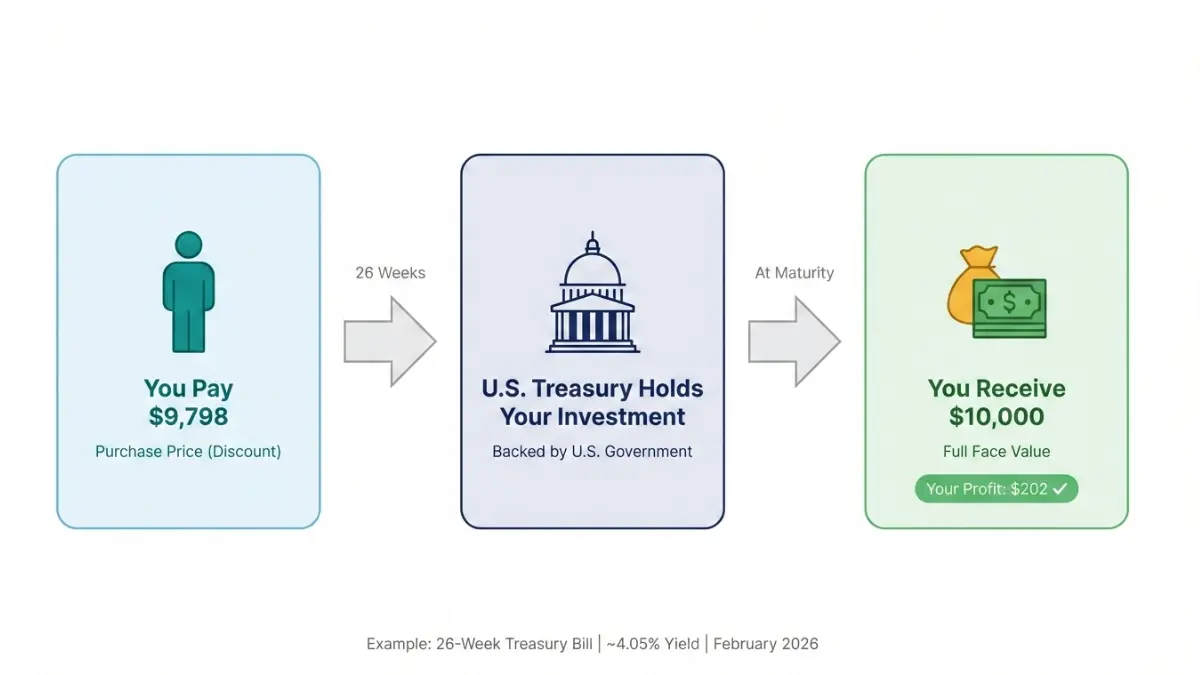

Real Dollar Example:

- You buy a 26-week T-bill with a $10,000 face value

- You pay approximately $9,798 today

- In 26 weeks, you receive $10,000

- Your gain: $202 — no stock market risk, no volatility

Key T-Bill Facts at a Glance

- Minimum purchase: $100 (in $100 increments)

- Terms available: 4, 6, 8, 13, 17, 26, and 52 weeks

- Backed by: U.S. federal government

- Interest paid: At maturity only (not periodically)

- State/local taxes: Exempt

- Federal taxes: Applicable in the year the bill matures

- Where to buy: TreasuryDirect.gov or through any major brokerage

Treasury Bill vs. Treasury Note vs. Treasury Bond

| Security | Maturity | Interest Payments | Minimum |

|---|---|---|---|

| Treasury Bill (T-Bill) | 4 weeks – 1 year | At maturity (discount) | $100 |

| Treasury Note (T-Note) | 2 – 10 years | Every 6 months | $100 |

| Treasury Bond (T-Bond) | 20 – 30 years | Every 6 months | $100 |

The key difference is time horizon. T-bills are ideal for short-term savings goals where you need your money back within a year. If you’re thinking about longer-term fixed-income strategy, our guide on what is a bond covers the full spectrum of U.S. debt securities.

💡 Expert Insight: “Treasury bills are the only investment where the U.S. government acts as your direct counterparty — there is no institution, no bank, and no middleman between you and repayment.” — Dr. James Hartley, CFA

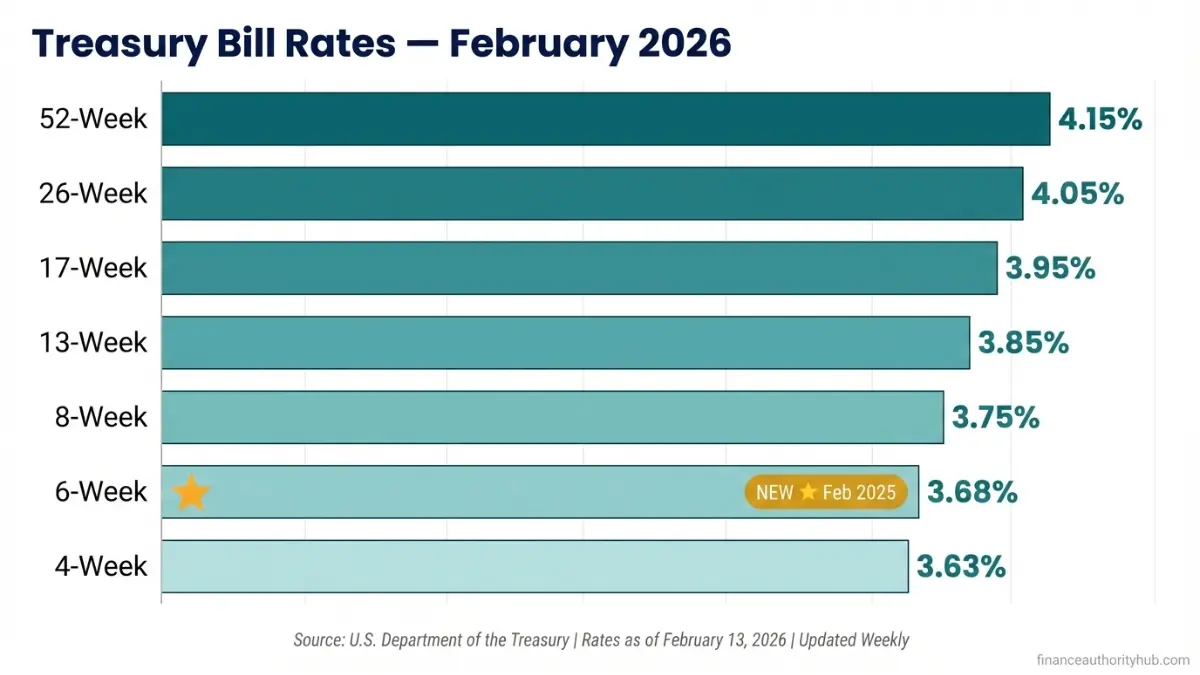

Current Treasury Bill Rates — February 2026

T-bill yields have remained attractive in early 2026, with the Federal Reserve maintaining its target rate at 3.50%–3.75% following a series of rate cuts from 2023 highs. The 4-week T-bill yield stood at approximately 3.70% as of February 13, 2026 — still well above pre-2022 levels and significantly higher than the national average savings account rate.

Live T-Bill Rate Table — All 7 Maturities (February 2026)

| T-Bill Term | Days | Approx. Yield | Auction Day | Best For |

|---|---|---|---|---|

| 4-Week | 28 | ~3.63–3.70% | Thursdays | Maximum liquidity |

| 6-Week ⭐ | 42 | ~3.68% | Tuesdays | New option (Feb 2025) |

| 8-Week | 56 | ~3.75% | Thursdays | Short-term buffer |

| 13-Week | 91 | ~3.85% | Mondays | Most popular starter |

| 17-Week | 119 | ~3.95% | Wednesdays | Mid-range balance |

| 26-Week | 182 | ~4.05% | Mondays | Best yield/flexibility ratio |

| 52-Week | 365 | ~4.15% | Monthly | Highest short-term yield |

Source: U.S. Treasury — Daily Treasury Bill Rates, February 2026. Rates change with each weekly auction.

⭐ NEW in 2025: The 6-week T-bill was introduced as a benchmark security on February 18, 2025 — a brand-new maturity option that most financial websites have not yet updated their guides to include.

What This Means For You

- Need money in under 2 months? → 4-week or 6-week T-bill

- Building a savings buffer? → 13-week is the most popular, most liquid choice

- Want the highest short-term government yield? → 26-week or 52-week T-bill

- Living in a high-tax state? → See Section 5 for the tax math that changes everything

For real-time rate comparisons against savings accounts and CDs, check our roundup of banks paying 5% APY to see exactly how T-bills stack up against the best HYSA options today.

How Treasury Bills Work — Mechanics & Risk

Understanding the discount mechanism is the key to understanding T-bills. Treasury bills are typically issued at a discount from the par amount. For example, if you buy a $1,000 bill at a price per $100 of $99.986111, you would pay $999.86. When the bill matures, you are paid the full face value of $1,000 — your interest is the face value minus the purchase price.

This is why T-bills are called zero-coupon instruments. No monthly checks, no quarterly dividends — just a clean, one-time payout at the end of the term.

How T-Bill Auctions Work

The U.S. Treasury sells T-bills through a weekly auction process. Every American investor can participate. There are two ways to bid:

| Bid Type | Who It’s For | Guarantee | Maximum |

|---|---|---|---|

| Noncompetitive | Individual investors | ✅ Guaranteed fill | $10 million |

| Competitive | Institutions, experienced traders | ❌ No guarantee | 35% of offering |

With a noncompetitive bid, you agree to accept the discount rate determined at auction, and you are guaranteed to receive the full amount you want. This is the recommended approach for 95% of retail investors — you’re guaranteed your T-bill at whatever rate the market sets that week.

Can You Lose Money on a Treasury Bill?

If held to maturity: No. The U.S. government guarantees full face value repayment. Treasury bills represented approximately 22% of all outstanding marketable Treasury debt as of October 2025 — the sheer scale of this market reflects its systemic reliability.

If sold early: Yes, theoretically. T-bills trade on the secondary market, and their price can dip if interest rates rise after you buy. However, because T-bill maturities are so short (under 1 year), this risk is extremely limited compared to longer-duration bonds.

🛡️ Key Takeaway: T-bills are not FDIC-insured — but they are backed directly by the U.S. government, which has never defaulted on its short-term debt obligations. Most financial experts consider this safer than any FDIC-insured product.

How to Buy Treasury Bills in 2026 — 3 Methods

You have three clear options for buying T-bills in 2026. Each suits a different type of investor.

Buying Method Comparison

| Method | Best For | Minimum | Fees | Liquidity |

|---|---|---|---|---|

| TreasuryDirect.gov | Direct investors, fee-haters | $100 | Free | Hold 45 days min. |

| Brokerage Account | Portfolio integration | ~$1,000 | Usually free | Secondary market |

| T-Bill ETFs (TBIL, XBIL) | Hands-off, maximum flexibility | 1 share (~$50–100) | Expense ratio | Daily |

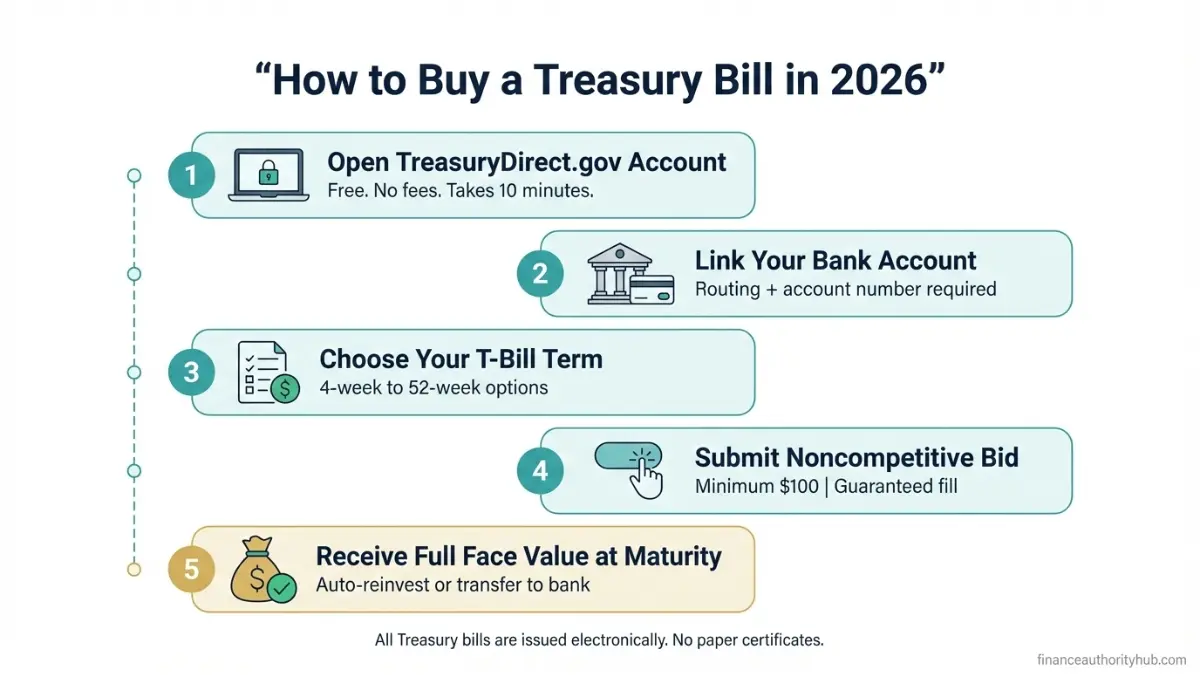

Method 1: Buy Direct via TreasuryDirect.gov (Recommended for Most Investors)

This is the free, direct route — no intermediary, no fees. TreasuryDirect is the official U.S. government application where you can buy and hold Treasury marketable securities. All Treasury marketable securities require a minimum bid of $100, and you may bid in increments of $100.

Step-by-Step TreasuryDirect Buying Guide:

- Go to TreasuryDirect.gov and click “Open an Account”

- Complete identity verification (Social Security Number, bank details required)

- Log in → click “BuyDirect” in your account dashboard

- Select “Bills” from the security type menu

- Choose your T-bill term (4-week, 13-week, 26-week, etc.)

- Enter purchase amount (minimum $100)

- Select “Noncompetitive” bid — this guarantees your purchase

- Choose maturity instruction: “Reinvest” (auto-roll into next auction) or “Transfer to Bank”

- Submit your order before the auction closing time (typically 11:30 AM ET on auction day)

- On auction day, you can see results after 5 PM Eastern time in your TreasuryDirect account

Pro Tip: Set up automatic reinvestment when buying. Every time your T-bill matures, it rolls into a new one automatically — no manual action needed. This is the T-bill ladder in its simplest form.

Method 2: Buy Through a Brokerage

Available at Fidelity, Charles Schwab, Vanguard, and most major brokers. Search “Treasury Bills” in the fixed-income or bonds section. You can also access the secondary market through brokers — meaning you can buy T-bills any business day, not just on weekly auction dates.

This method is ideal if you already have a brokerage account and want T-bills alongside your other investments. If you’re still comparing savings vehicles for your financial plan, use our home affordability calculator to see how redirecting short-term savings into T-bills affects your path to homeownership.

Method 3: T-Bill ETFs

For investors who want daily liquidity without managing individual auctions, T-bill ETFs are an excellent alternative. Popular options include TBIL (3-month) and XBIL (6-month). These trade like stocks, have expense ratios under 0.20%, and provide instant T-bill exposure.

Downside: You lose the state-tax exemption benefit that individual T-bills provide (see Section 5).

T-Bill vs. CD vs. HYSA vs. Money Market — 2026 Full Comparison + The Tax Edge

This is the section no competitor covers properly. Here’s the complete picture for 2026.

Side-by-Side Rate and Feature Comparison

| Feature | Treasury Bill | Top CD (1-Year) | High-Yield Savings | Money Market Fund |

|---|---|---|---|---|

| Feb 2026 Yield | ~3.63–4.15% | ~4.0–4.5% (best) | ~3.5–4.2% | ~4.0–4.3% |

| Federal Tax | ✅ Yes | ✅ Yes | ✅ Yes | ✅ Yes |

| State & Local Tax | ❌ Exempt | ✅ Taxable | ✅ Taxable | ⚠️ Partial |

| FDIC Insured | ❌ (Gov. backed) | ✅ Yes | ✅ Yes | ❌ No |

| Early Withdrawal | Secondary market | Penalty applies | Anytime | Anytime |

| Minimum | $100 | $500–$1,000 | $0–$1 | $1–$1,000 |

| Rate Lock | Fixed at auction | Fixed for CD term | Variable | Variable |

The Hidden Tax Advantage Most Investors Miss

Here’s where T-bills quietly beat higher-yielding alternatives for millions of Americans. All interest from Treasury securities, including T-bills, is exempt from state and local taxes — in a high-tax state like New York, this effectively bumps the tax-equivalent yield by approximately 0.25 percentage points.

That means a T-bill’s true after-tax yield is higher than its stated rate for anyone paying state income tax. Here’s the math:

Tax-Equivalent Yield Table (26-Week T-Bill at ~4.05%, February 2026)

| State | State Income Tax Rate | T-Bill Yield | Tax-Equiv. Yield | CD Rate Needed to Match |

|---|---|---|---|---|

| California | 9.30% | 4.05% | 4.47% | 4.47% CD |

| New York | 6.85% | 4.05% | 4.35% | 4.35% CD |

| Illinois | 4.95% | 4.05% | 4.26% | 4.26% CD |

| Florida/Texas | 0% | 4.05% | 4.05% | 4.05% CD |

💡 What This Means For You: If you’re in California, you’d need a CD paying 4.47% to match a T-bill paying 4.05% after taxes. Most CDs don’t offer that. T-bills win — quietly and legally.

If you’re managing your tax picture across multiple income streams, our 2026 tax brackets guide shows exactly how T-bill income interacts with your marginal rate and federal deductions.

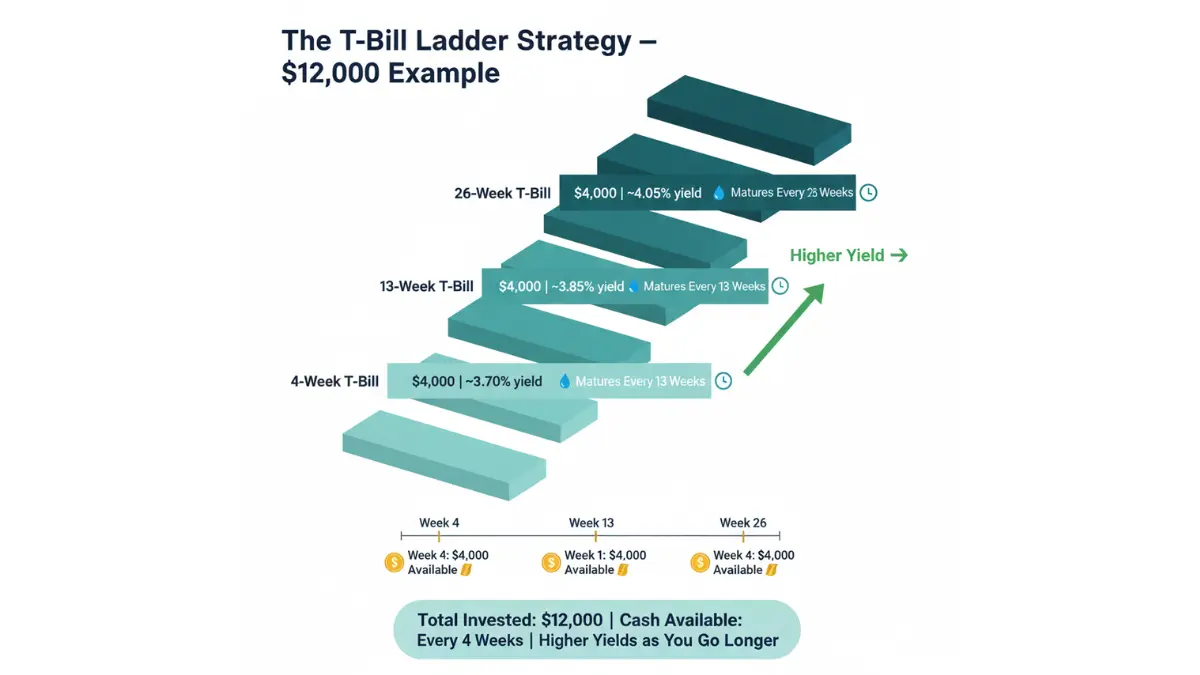

The T-Bill Ladder Strategy — Earn More, Stay Flexible

A T-bill ladder is one of the most powerful yet underused personal finance strategies. No competitor in the top 10 explains it with a real example. Here’s how it works:

$12,000 T-Bill Ladder Example (3-Step):

| Step | Amount | T-Bill Term | Yield | Money Available |

|---|---|---|---|---|

| 1 | $4,000 | 4-week | ~3.70% | Every 4 weeks |

| 2 | $4,000 | 13-week | ~3.85% | Every 13 weeks |

| 3 | $4,000 | 26-week | ~4.05% | Every 26 weeks |

Result: You always have T-bills maturing, giving you regular access to cash — while the longer-dated portion earns higher yields. When each T-bill matures, you reinvest it into the next available term. Over time, you capture the best available rates while maintaining flexibility.

This strategy pairs naturally with a broader short-term savings plan. If you’re building toward a larger financial goal, use our 52-week savings plan alongside a T-bill ladder to maximize both discipline and return.

To understand how T-bill income fits into your overall investment approach, our guide on compound interest fundamentals shows how even modest short-term yields compound into meaningful gains when reinvested consistently.

Is a Treasury Bill a Good Investment in 2026?

The direct answer: Yes — for the right investor and the right goal.

T-bills are not wealth-building instruments. They will not outperform the S&P 500 over a decade. But for short-term capital preservation with better-than-savings returns and a meaningful tax advantage, they are exceptional in the current 2026 rate environment.

Pros and Cons — At a Glance

| ✅ Pros | ❌ Cons |

|---|---|

| Backed by U.S. government (virtually zero default risk) | Returns lower than equities long-term |

| State & local tax-exempt for all U.S. investors | Not FDIC insured (still very safe) |

| Yields significantly above pre-2022 levels | Requires TreasuryDirect account or broker setup |

| Start investing with just $100 | Rate drops if Fed cuts again |

| 7 maturity options for maximum flexibility | Not suitable for long-term retirement growth |

| Weekly auctions — easy to access anytime | 45-day holding period on TreasuryDirect |

| Ideal for T-bill laddering strategy | T-bill ETFs lose state tax exemption |

Who Should Use T-Bills in 2026?

✅ T-bills are ideal for:

- Emergency fund overflow (money beyond your 3–6 month cash reserve)

- Short-term savings goals within 1 year (vacation, down payment runway, tax payment reserves)

- Conservative investors who want government-guaranteed returns

- High-tax-state residents where the tax exemption provides a real yield boost

- Retirees preserving capital with better-than-savings returns

- Anyone parking cash while waiting for better investment opportunities

❌ T-bills are NOT ideal for:

- Long-term wealth building (use index funds, Roth IRA, or 401(k) instead)

- Investors who need daily liquidity without a secondary market (use HYSA instead)

- Income investors who need regular payments (use Treasury Notes or bonds)

If you’re approaching retirement and want to understand where T-bills fit into a broader fixed-income allocation, our retirement savings by age guide and 401(k) vs IRA comparison map out exactly how short-term instruments complement long-term accounts.

Expert Panel Verdict: “In early 2026, Treasury bills offer one of the best risk-adjusted returns available for capital with a sub-12-month horizon. The state tax exemption is particularly powerful for investors in California, New York, and Illinois. Anyone sitting on idle cash above their emergency fund should seriously consider a T-bill ladder.” — Dr. James Hartley, CFA, financeauthorityhub.com Financial Expert Panel

Treasury Bill FAQs — Quick Answers

1. What is a Treasury bill in simple terms?

A T-bill is a short-term loan you give to the U.S. government. You pay less than face value today, and the government repays you the full amount in 4 weeks to 1 year. Your profit is the difference.

2. What are current Treasury bill rates in February 2026?

Rates currently range from approximately 3.63% (4-week) to ~4.15% (52-week). Rates change with each weekly auction and follow the Federal Reserve’s rate direction.

3. What is the minimum amount to invest in a Treasury bill?

The minimum purchase is $100, and bills are sold in $100 increments. You can buy directly at TreasuryDirect.gov with no fees.

4. How do I buy a Treasury bill?

The easiest method is through TreasuryDirect.gov — create a free account, link your bank, choose your term, and submit a noncompetitive bid. You can also buy through Fidelity, Schwab, or Vanguard.

5. Are Treasury bills tax-free?

Partially. T-bill interest is exempt from all state and local income taxes but is subject to federal income tax in the year the bill matures. This gives T-bills a meaningful advantage over CDs and savings accounts in high-tax states.

6. Can you lose money on a Treasury bill?

Not if held to maturity. The U.S. government guarantees full face value repayment. If you sell early on the secondary market before maturity, the price could be slightly lower than face value depending on interest rate movements.

7. What is the difference between a T-bill and a T-bond?

T-bills mature in 1 year or less and pay no periodic interest. T-bonds mature in 20–30 years and pay interest every 6 months. T-bills carry far less interest rate risk. See our what is a bond guide for a full breakdown.

8. What is a 6-week Treasury bill? ⭐

The 6-week T-bill was introduced as a benchmark Treasury security on February 18, 2025, auctioned every Tuesday. It fills the gap between the 4-week and 8-week options and currently yields approximately 3.68%. Most financial websites have not yet updated to include this new option.

9. What is a T-bill ladder?

A T-bill ladder means buying T-bills across multiple maturities (e.g., 4-week, 13-week, and 26-week) simultaneously. As each bill matures, you reinvest it. This gives you regular access to cash while capturing higher yields on longer-dated bills.

10. Are Treasury bills better than a high-yield savings account in 2026?

For high-tax-state residents: usually yes, once you factor in the state-tax exemption. For states with no income tax (Texas, Florida), the after-tax yields are closer. Compare using the tax-equivalent yield table in Section 5 above.

11. How often are Treasury bill auctions held?

The 4-week, 6-week, 8-week, 13-week, 17-week, and 26-week bills are auctioned every week. The 52-week bill is auctioned every four weeks. Auction results are published at TreasuryDirect.gov the same day, after 5 PM ET.

Disclaimer

This article is for educational and informational purposes only and does not constitute financial, investment, or tax advice. Treasury bill rates change with every weekly auction. All yield data reflects approximate secondary market rates as of February 2026 and may have changed by the time you read this. Always verify current rates at TreasuryDirect.gov and consult a licensed financial advisor or tax professional before making investment decisions. Past yields do not guarantee future returns.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.