What Actually Funds Your Structured Settlement Annuity

Structured settlement annuity payments are funded by a life insurer under IRC 130 — but selling without court approval triggers a 40% federal tax.

In This Article

What a structured settlement annuity actually is — and why an insurance company is involved

If your attorney told you that your settlement will be paid as a structured settlement annuity, you are now dealing with a life insurance contract — not a payment plan from the defendant.

That single distinction determines who actually guarantees your money, why the IRS treats your payments as tax-free, and what options remain if your financial needs change years from now.

The two questions every new recipient asks first

Two questions arrive in every new-recipient conversation I’ve had over 28 years in capital markets.

First: who is legally responsible for paying me — and what happens if that entity fails?

Second: are these payments genuinely tax-free, or is there an IRS exposure I need to understand before I sign?

Both questions have precise, statutory answers.

Why this article covers the insurance mechanics — not just the legal definition

Most settlement explanations describe structured payments as money arriving over time.

That framing skips the insurance mechanism that guarantees those payments, the two IRC sections that create the tax exemption, and the present-value analysis that tells you whether the offer you received is financially fair.

This article covers all three.

ℹ️ Disclaimer: This article discusses structured settlement annuities, which are insurance products governed by state insurance law, IRC Sections 104, 130, and 5891, and state structured settlement protection acts. The content is educational only and does not constitute legal, tax, or insurance advice. Before accepting, modifying, negotiating, or transferring any structured settlement annuity, consult a licensed structured settlement consultant (CSSC), a Certified Financial Planner (CFP), and/or a licensed attorney. All figures are illustrative; verify current terms with a qualified professional.

What a structured settlement annuity is — and who the parties are

A structured settlement annuity is a periodic payment stream, funded by a licensed life insurance company, that satisfies a personal injury or wrongful death claim in lieu of a lump-sum payment — and whose payments are excluded from the recipient’s gross income under IRC Section 104(a)(2).

That definition raises the question most recipients never think to ask: why is a life insurance company involved at all?

How a structured settlement differs from a commercial annuity

A commercial annuity is a retail product funded with your own money — you pay the insurer, and the insurer pays you back over time.

A structured settlement annuity is funded by the defendant’s money, issued under a court-recognized settlement agreement, and structured through the IRC Section 130 qualified assignment framework that grants the tax-free status commercial annuities cannot access.

The life insurance calculator provides useful context for understanding the economics of insurance-funded income payments — a helpful baseline as you evaluate the long-term financial weight of your payment schedule.

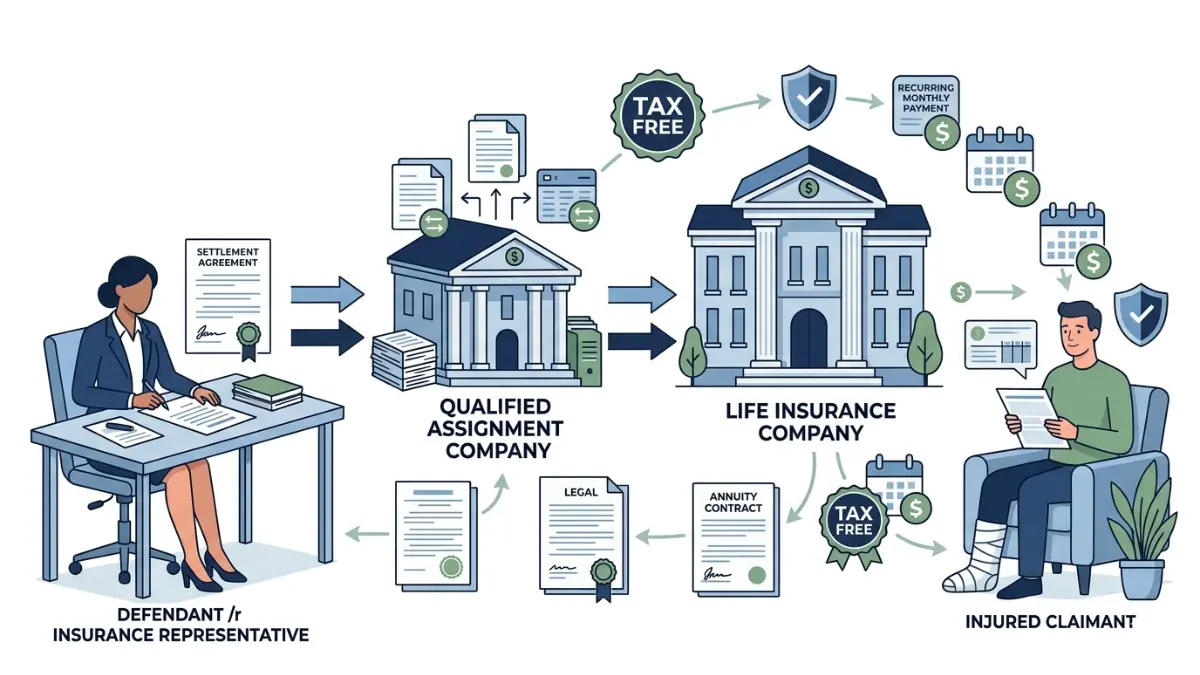

The four parties in every structured settlement — and what each one does

Four distinct parties are involved in every structured settlement annuity — and collapsing any two of them into one entity is the single most common misunderstanding I see in client meetings.

- The defendant — the liable party, who agrees to the settlement and funds the initial premium.

- The qualified assignment company — the legal entity that accepts the defendant’s payment obligation under IRC Section 130, becoming the new obligor.

- The life insurance company — the annuity issuer, which receives the premium from the assignment company and sends every periodic payment directly to you.

- You, the claimant — the irrevocable payee whose rights to receive payments cannot be accelerated, reassigned, or borrowed against.

💡 Expert Note (CFA): The assignment company and the life insurer are two separate legal and financial entities — a distinction that matters enormously for evaluating your payment security. The assignment company transfers the legal obligation; the insurer funds the economic one. When assessing the safety of your payments, check the life insurer’s AM Best or S&P credit rating. The assignment company’s creditworthiness is secondary.

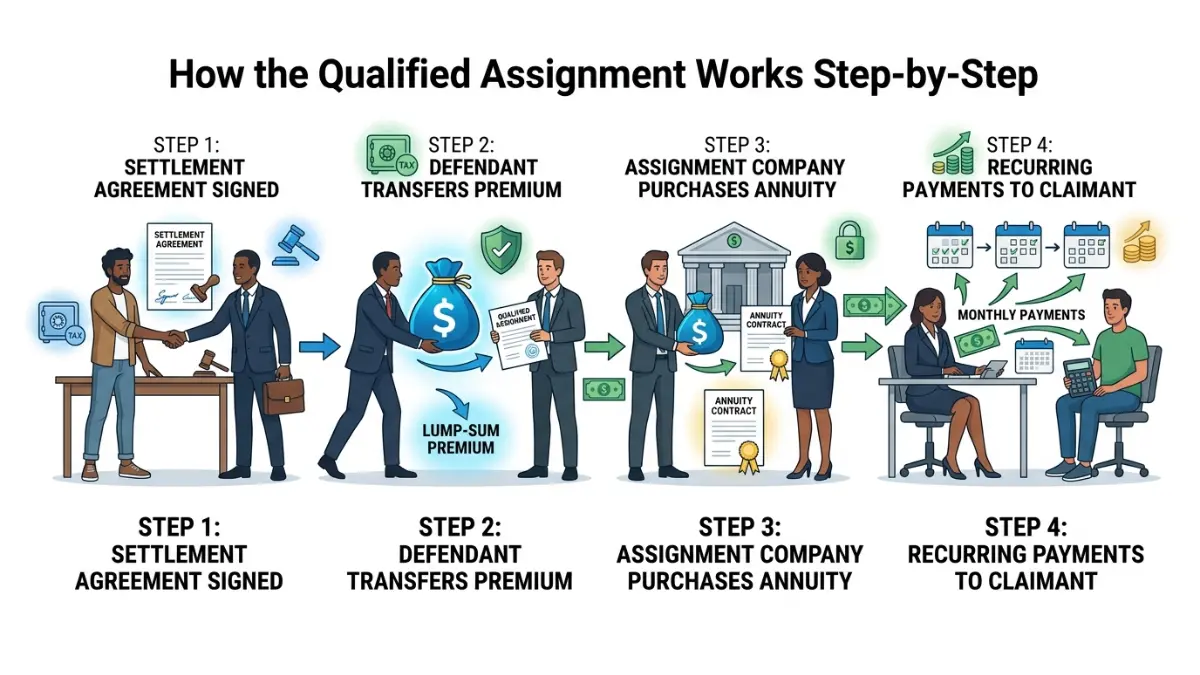

How the qualified assignment works — the step-by-step funding sequence

The qualified assignment is the legal mechanism that transforms a defendant’s payment obligation into a guaranteed life insurance contract — and it is the single most important process in the entire structured settlement.

Understanding it tells you exactly why your payments are safe, why they qualify for tax-free status, and what the document in front of you actually obligates.

Step 1 through Step 4 — the four-stage assignment sequence

The funding of a structured settlement annuity follows a precise four-stage sequence, each stage governed by federal statute:

- Settlement agreement is executed. You and the defendant agree to resolve the claim through periodic payments. The payment schedule — amounts, dates, and duration — is fixed in the settlement document and cannot be unilaterally changed.

- Defendant funds the assignment company. The defendant transfers a single cash premium to a qualified assignment company, simultaneously transferring both the legal obligation to pay and the economic cost of funding those future payments.

- Assignment company purchases the annuity contract. The assignment company uses that premium to purchase an irrevocable annuity contract from a rated, state-licensed life insurance company. The insurer contractually commits to every payment on the schedule.

- Life insurer pays you directly. The life insurance company sends each periodic payment directly to you on the agreed dates — independently of the defendant and independently of the assignment company — for the full term of the agreement.

Why the assignment company and the insurer are two different entities

The assignment company is a legal vehicle whose job is to absorb the defendant’s obligation and deploy the premium to an insurer.

The life insurer is the economic engine whose job is to invest that premium against long-term reserves and meet every payment — which is why this two-entity structure is a safety feature, not unnecessary complexity.

What “qualified” means under IRC Section 130 — and why it matters for your taxes

For your payments to be excluded from income under IRC Section 104(a)(2), the assignment must satisfy four requirements under IRC Section 130: the payments must compensate for physical personal injury, the amounts and timing must be fixed and determinable, the rights must be payable only to you or your named beneficiary, and the obligation must be assumed from the original obligor.

📊 Data Point: IRC Section 130 was enacted specifically to provide the tax-exempt framework for structured settlement assignments. As of 2026, it remains the sole statutory mechanism by which a defendant can transfer payment obligations while preserving the claimant’s full income exclusion under IRC Section 104(a)(2) — confirmed by the IRS in its guidance on settlements and judgments.

How structured settlement annuity payments are priced and calculated

The premium a life insurer charges for a structured settlement annuity equals the present value of all future payments, discounted at the insurer’s internal pricing rate — a calculation driven by the claimant’s life expectancy, the payment schedule design, and prevailing long-term interest rates.

That figure is rarely discussed openly in settlement negotiations, which is exactly why recipients should understand how it works before signing.

Present value and the discount rate — what drives the lump-sum equivalent

Present value is the amount of money today that, invested at the assumed rate, would generate exactly the scheduled future payments.

A higher discount rate lowers the present value — meaning the insurer needs to invest less today to fund the same future stream.

📊 Data Point: In 2026, life insurers pricing structured settlement annuities typically apply internal discount rates between 3.5% and 5.5%, calibrated to long-term Treasury yields and investment-grade corporate bond spreads — Source: National Structured Settlement Trade Association (NSSTA), Q1 2026 industry pricing benchmarks.

The investment calculator lets you run the present-value equivalent of any structured payment stream at any assumed rate — a direct cross-check against the offer you received.

The ROI calculator can compare the implied return of your payment schedule against what a lump-sum alternative might realistically generate in a diversified portfolio.

How rated age and mortality adjustment affect your payment amount

Rated age is a medical underwriting adjustment that insurers apply to claimants whose documented health impairments reduce their life expectancy below actuarial norms.

If an underwriter determines your health profile matches that of a person 10 years older, the insurer prices the annuity using that older rated age — which reduces the premium required and can either lower the defendant’s cost or increase the monthly payment available to you.

💡 Expert Note (CFA): The rated-age adjustment is the single most underexplored pricing factor in structured settlements — and almost no claimant is informed about it before signing. If you have any documented health condition, insist that a licensed structured settlement consultant (CSSC) obtain a rated-age evaluation from the insurer before the payment schedule is finalized. I’ve seen this adjustment increase a monthly payment by 15%–25%.

The inflation calculator shows how a fixed monthly payment loses purchasing power over a 20- or 30-year period at historical inflation rates — critical context for any life-contingent annuity schedule.

The FINRA guidance on annuity suitability is relevant whenever a structured settlement broker recommends a specific insurer — suitability standards apply even in the settlement context, and recipients should ask whether the recommended carrier is the most competitively priced option available.

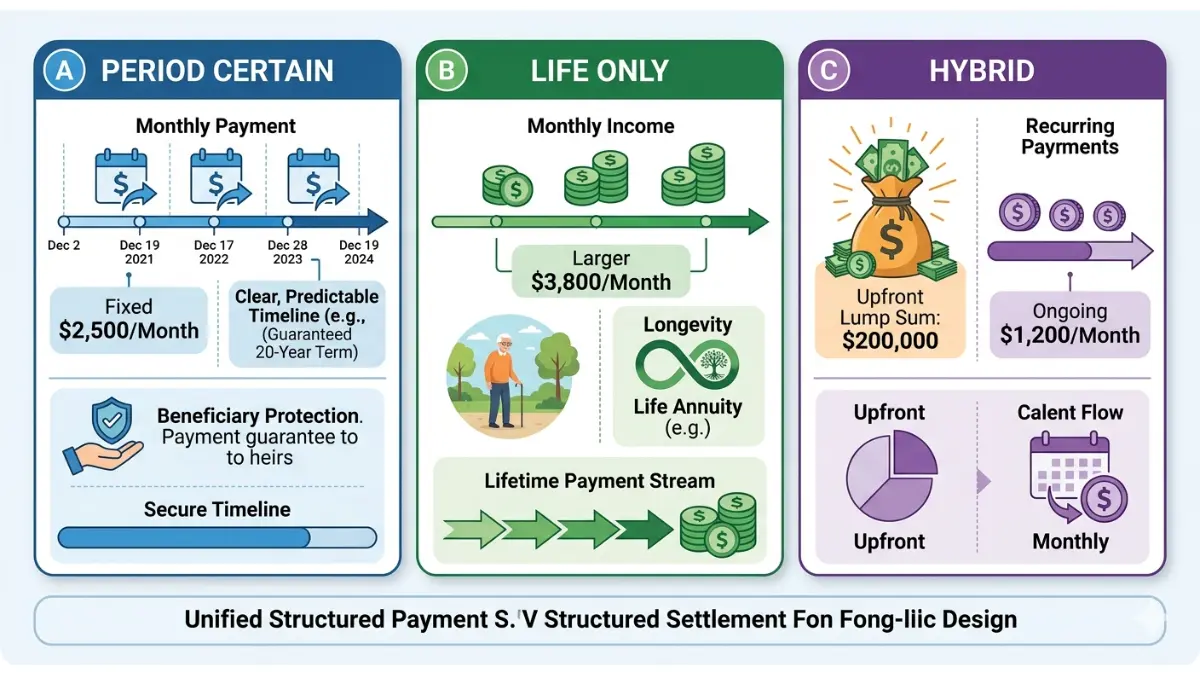

A 2026 structured settlement pricing example — $500,000 settlement, three schedules

| Payment Schedule | Monthly Amount | Duration | Nominal Total | Est. Premium at 4.5% | Best For |

|---|---|---|---|---|---|

| A — Period Certain | $2,500 | 20 years | $600,000 | ~$385,000 | Predictability; beneficiary protection |

| B — Life Only | $3,100 | Claimant’s life | Varies | ~$375,000 | Maximum monthly income; no residual |

| C — Hybrid | $1,800/mo + $150K upfront | 15 years | ~$474,000 + $150K | ~$490,000 | Immediate liquidity need plus ongoing income |

Source: Illustrative 2026 model. Actual premiums vary by insurer, claimant health, and rate environment.

Why structured settlement annuity payments are tax-free — what the IRS actually says

Structured settlement annuity payments are tax-free for a reason grounded in statute — not in how your attorney describes them or how the settlement agreement is worded.

Understanding the exact statutory basis protects you from the most common — and most expensive — misconception recipients carry into the IRS filing season.

IRC Section 104(a)(2) — the physical injury exclusion explained

Under IRC Section 104(a)(2), amounts received as compensation for physical personal injury or physical sickness are excluded from the recipient’s gross income — regardless of the payment amount or duration.

That exclusion applies to every periodic payment in a properly structured settlement annuity, covering both the principal and the growth component built into the annuity contract.

📊 Data Point: IRS Publication 4345, “Settlements — Taxability” (2026) confirms that periodic payments received as damages for physical personal injury are fully excludable under IRC Section 104(a)(2), provided the structured settlement annuity was established through a qualified assignment under IRC Section 130.

The income tax calculator helps estimate your total 2026 income tax liability — useful when a settlement includes both tax-free components and any taxable amounts that need to be reported.

What IRC Section 130 adds — why the qualified assignment preserves the exemption

The qualified assignment under IRC Section 130 is not just a transfer mechanism — it is the step that makes the tax exclusion durable at the annuity level.

Without a qualified assignment, payments from an insurance company to a claimant could be characterized as annuity income subject to the normal taxation rules for commercial annuities — partially taxable as the payment exceeds the cost basis.

The take-home pay calculator provides a useful snapshot of your net monthly income picture when structured settlement payments are layered alongside wages or other taxable income sources.

The exceptions — when structured settlement payments can become taxable

Three categories of settlement proceeds do not qualify for the IRC 104(a)(2) exclusion and will generate a tax obligation if received as part of your structured payment stream:

- Punitive damages — taxable as ordinary income under IRC Section 104(a)(2)’s explicit exclusion of non-compensatory damages.

- Pre-judgment interest — taxable as interest income, regardless of how the interest is characterized in the settlement agreement.

- Emotional distress damages without a physical injury origin — taxable if the distress claim is not tied to a documented physical injury or sickness.

⚠️ Warning: Mixed settlements — those combining compensatory physical injury damages with punitive awards, back pay, or unrelated emotional distress claims — require a CPA or tax attorney to allocate the taxable and non-taxable portions before the payment schedule is finalized. Errors in this allocation have triggered IRS notices and accuracy-related penalties. Allocate in writing, on paper, before signing.

The capital gains tax calculator is relevant if you negotiate any portion of your settlement as a lump sum and invest those proceeds — gains on subsequent investment growth are fully taxable.

Lump sum, structured payments, or selling — how to evaluate each option

The right choice between accepting structured settlement payments, negotiating a lump sum, or selling future payments to a factoring company is not a matter of preference — it is a present-value calculation with real, quantifiable dollar consequences.

Each path has a different cost structure, and only one of them is reversible.

Option 1 — Accept the structured settlement: when the annuity wins

A structured settlement annuity delivers full present value, tax-free income, and counterparty protection that no lump sum alternative replicates.

For a recipient who needs long-term income stability — particularly one who is managing a permanent injury, disability, or chronic condition — the guaranteed payment stream eliminates the risk of outliving the proceeds or making a poor investment decision with a large sum.

The retirement calculator can model how structured annuity payments integrate with your Social Security benefit and other retirement income sources across a 20- or 30-year horizon.

Option 2 — Negotiate a lump sum: what you actually give up

A lump sum offers immediate liquidity — but defendants and their insurers calculate the lump-sum offer at a discount to the structured payout’s present value, and that discount always favors the defendant.

The compound interest calculator lets you model what a specific lump-sum amount could realistically grow to over the settlement period — a direct comparison against the nominal total of the structured schedule.

💡 Expert Note (CFA): In nearly three decades of advising clients on fixed-income instruments and settlement income planning, the most persistent misconception I encounter is that a lump sum is simply “the same money paid earlier.” It is not. The defendant’s insurer has calculated the offer to be profitable for them at the current rate environment. At a 4.5% internal pricing rate, a defendant offering $380,000 today is telling you the structured payment stream is worth $500,000+ over time. Run the present-value calculation before responding to any lump-sum counter-offer. The savings calculator can show the accumulation scenario if you invest the lump sum at realistic 2026 return assumptions.

Option 3 — Sell future payments: the IRC 5891 excise tax and what factoring really costs

Selling future structured settlement annuity payments to a factoring company is legal — but it is the most financially costly option on this list, and it is irreversible.

⚠️ Warning: Any transfer of structured settlement payment rights that is not approved by a state court is subject to a 40% federal excise tax under IRC Section 5891 — a penalty designed to deter unauthorized sales. In 2026, factoring companies typically apply discount rates of 9%–18% to purchased payment streams, meaning a $100,000 payment due in 10 years may be purchased for as little as $32,000–$42,000.

Before contacting any factoring company, review the CFPB’s consumer guidance on structured settlement transfers, which explains the disclosures you are legally owed before any offer is presented.

The SEC’s investor alert on structured settlement factoring also warns consumers about third-party investment schemes that use purchased settlement rights — a red flag for any seller to understand before signing a transfer agreement.

✅ Pro Tip: Before engaging any factoring company, ask a licensed CSSC or independent CFP to calculate the implied discount rate on the offer in writing. Federal law requires factoring companies to disclose the effective discount rate — if a company resists providing that figure, end the conversation.

The Social Security calculator can help you model total retirement income — useful context when evaluating whether selling payments creates a long-term income gap that cannot be recovered.

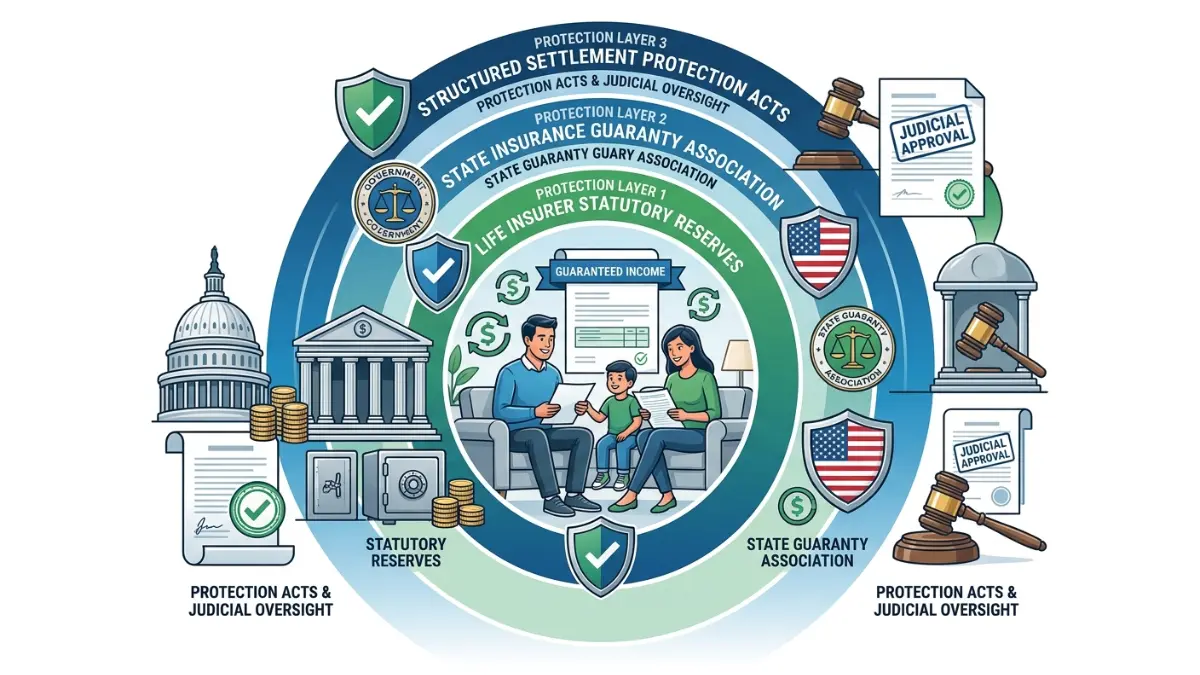

What to do next — protecting your structured settlement from the start

Your structured settlement annuity is not simply an arrangement between you and the defendant — it is a legally protected, insurance-backed financial instrument with three independent safety layers that most recipients never have explained to them.

Knowing those layers before you sign — not after — is what separates a confident settlement decision from one you revisit for years.

The three protections every structured settlement recipient should verify

Three independent safeguards protect every properly structured settlement annuity:

- The life insurer’s statutory reserves — state regulators require licensed life insurers to maintain capital reserves against long-term annuity obligations; verify the insurer’s AM Best rating is A- or higher before the annuity is issued.

- Your state’s insurance guaranty association — if the life insurer becomes insolvent, your state guaranty association provides a backstop; as of 2026, coverage for life annuity contracts ranges from $250,000 to $500,000 per covered contract depending on the state.

- State structured settlement protection acts — all 50 states have enacted laws requiring a court to approve any transfer of your payment rights before it is enforceable, protecting you from unauthorized or predatory sales.

📊 Data Point: As of January 2026, every U.S. state has enacted a structured settlement protection act (SSPA) requiring court approval for payment transfers — Source: National Structured Settlement Trade Association (NSSTA), 2026 State Law Compendium.

Your next step — and who to call before you sign anything

The first call after receiving a structured settlement offer is not to a factoring company — it is to a licensed structured settlement consultant (CSSC) or an independent CFP who does not earn a commission from the insurance company funding the annuity.

That professional can model every payment schedule, calculate the present-value differential between structured and lump-sum offers, verify the rated-age adjustment, and confirm the insurer’s financial strength rating — all before you sign.

The budget calculator can help you map your monthly income needs against proposed payment schedules before your consultation, so you arrive with real numbers instead of estimates.

Frequently asked questions about structured settlement annuities

The 11 questions below address the most consequential knowledge gaps for anyone receiving, evaluating, or considering changes to a structured settlement offer. Every answer reflects 2026 law and current market conditions. For guidance specific to your settlement agreement, consult a licensed structured settlement consultant (CSSC) or independent CFP before signing any document.

1. What is a structured settlement annuity?

A structured settlement annuity is a periodic payment stream funded by a licensed life insurance company that satisfies a personal injury or wrongful death claim in lieu of a lump-sum judgment. Under IRC Section 104(a)(2), those payments are fully excluded from the recipient’s gross income — making a structured settlement annuity one of the few financial instruments that generates completely tax-free income regardless of payment size.

2. How does a structured settlement annuity work?

A structured settlement annuity is funded through a qualified assignment under IRC Section 130. The defendant pays a premium to a qualified assignment company, which purchases an annuity from a licensed life insurer. That insurer sends periodic payments directly to the claimant on the agreed schedule for the full term. Consult a licensed structured settlement consultant (CSSC) before accepting any payment schedule.

3. Are structured settlement annuity payments taxable?

Structured settlement annuity payments are excluded from gross income under IRC Section 104(a)(2) when they compensate for physical personal injury — confirmed by IRS Publication 4345. Punitive damages and pre-judgment interest included in the same settlement are taxable as ordinary income or interest. For any mixed-damage settlement, consult a CPA or tax attorney before signing to avoid an unexpected IRS liability.

4. Who actually funds and pays a structured settlement annuity?

The defendant funds a structured settlement annuity at settlement by transferring a one-time cash premium to a qualified assignment company. That company purchases an annuity contract from a licensed life insurer, which then sends each periodic payment directly to the claimant. The life insurer — not the defendant and not the assignment company — is the entity that funds every payment for the full term.

5. Can you cash out or sell a structured settlement annuity?

Future structured settlement annuity payments can be sold to a factoring company, but state court approval is legally required in all 50 states under structured settlement protection acts. Unauthorized transfers trigger a 40% federal excise tax under IRC Section 5891. In 2026, factoring companies apply discount rates of 9%–18%, deeply reducing payment present value. Speak with a structured settlement attorney before any transfer agreement is signed.

6. What is a qualified assignment in a structured settlement?

A qualified assignment is the legal mechanism under IRC Section 130 that transfers the defendant’s payment obligation to a third-party assignment company, which then funds a life insurance annuity. The assignment is what makes structured settlement annuity payments eligible for the IRC Section 104 income exclusion. Without a properly structured qualified assignment, the tax-free status of periodic payments may not be preserved at the annuity level.

7. How safe is a structured settlement annuity?

A structured settlement annuity is protected by three layers: the life insurer’s statutory reserves, your state’s insurance guaranty association (covering $250,000–$500,000 per life annuity contract in most states as of 2026), and state court-approval requirements that prevent unauthorized payment transfers. Verify the insurer’s AM Best rating of A- or higher and your state’s specific guaranty fund limit with a licensed insurance professional before signing.

8. What is the difference between a structured settlement and an annuity?

A structured settlement is a legal agreement to resolve a claim — the annuity is the insurance contract that funds it. A structured settlement annuity qualifies for the IRC Section 104 income exclusion under the IRC Section 130 qualified assignment framework, which commercial annuities cannot access. The tax treatment, payment restrictions, and regulatory protections governing a structured settlement annuity are entirely distinct from those of a retail insurance product.

9. How much does a structured settlement annuity cost the defendant?

The defendant’s cost equals the premium paid to the assignment company, which equals the present value of all future payments at the insurer’s internal pricing rate. In 2026, illustrative premiums for a $500,000 aggregate structured settlement range from approximately $375,000 to $490,000 depending on the payment schedule design and the claimant’s rated age. A certified structured settlement consultant (CSSC) can model the exact premium for any specific payment schedule.

10. What are structured settlement protection acts?

Structured settlement protection acts are state laws — enacted in all 50 states as of 2026 — that require a judge to approve any transfer of structured settlement annuity payment rights before that transfer is legally enforceable. The court must find the transfer is in the recipient’s best financial and personal interest. These laws exist to protect recipients from being pressured into selling future payments at deeply discounted factoring rates. Consult a licensed attorney before any transfer proceeding.

11. Should I take a lump sum or a structured settlement annuity?

The right choice depends on your long-term income needs, your capacity to manage and invest a large sum responsibly, and the present-value gap between the two offers — which defendants always calculate in their favor. In 2026, factoring companies discount structured settlement annuity payment streams at 9%–18%, showing the true cost of liquidity. A Certified Financial Planner (CFP) or licensed CSSC can model both options with real numbers before you decide.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.