How Your Structured Settlement Stays Outside Self-Employment Tax

Structured settlement money never counts toward the $184,500 Social Security wage base or your self-employment tax—see why, and what still gets taxed.

In This Article

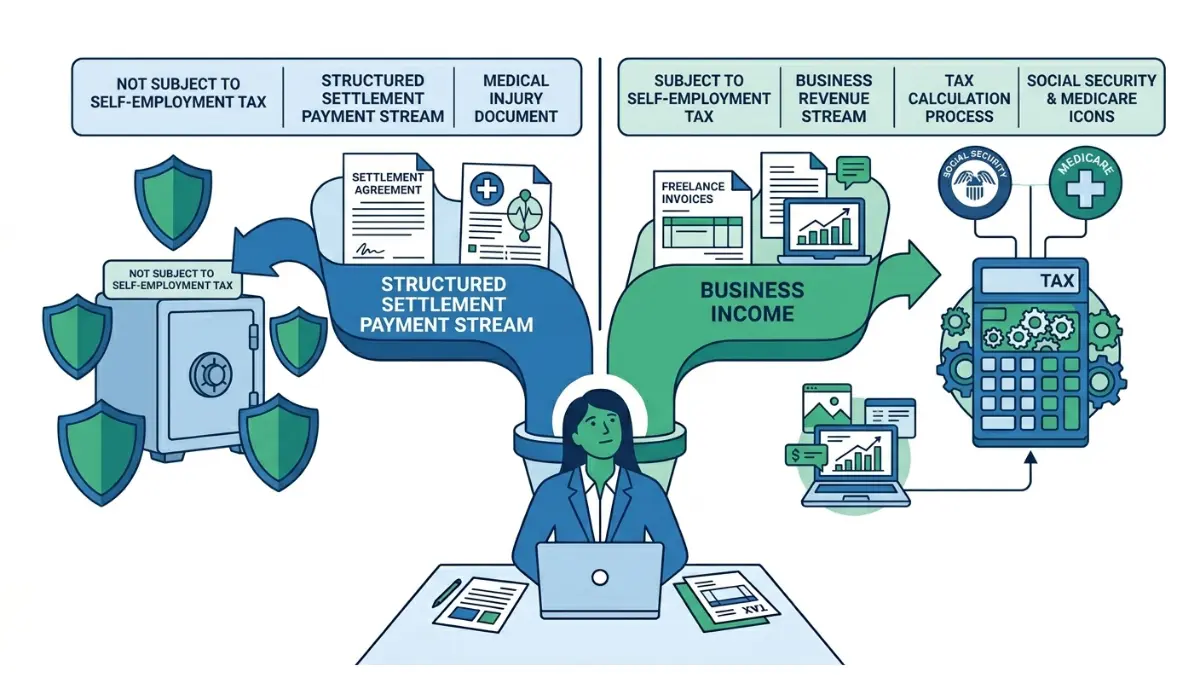

Running your own business while receiving settlement checks creates one nagging fear: does that money get swept into your self-employment tax bill? For most recipients, the answer brings real relief.

A structured settlement paid for a personal physical injury is excluded from your income under federal law, and that exclusion does not change because you are self-employed. Your settlement sits in one bucket, fully protected. Your business profit sits in another, where ordinary taxes apply.

This guide separates those two buckets using 2026 figures, so you know exactly what to report, what to leave off, and when to pay. It builds on our deeper look at what a structured settlement actually pays out over time.

ℹ️ Disclaimer: This article explains 2026 federal tax rules for structured settlement payments and self-employment income for educational purposes. Whether any settlement payment is tax-free depends on the specific damages and how your settlement agreement is worded under IRC §104(a)(2), and your self-employment tax outcome varies with your business income and your state. Before filing, selling future payments, or setting estimated taxes, consult a licensed tax professional such as a CPA or Enrolled Agent.

Do you pay self-employment tax on a structured settlement?

No. A structured settlement from a personal physical injury is excluded from gross income, so it never enters your self-employment tax base.

The exclusion comes from IRC Section 104(a)(2), which keeps damages for physical injury or sickness out of your income entirely. Because the payments are not income, they cannot be “net earnings from self-employment.”

That distinction matters. Self-employment tax applies only to profit you earn from a trade or business.

Why settlement payments aren’t self-employment income

Self-employment tax funds Social Security and Medicare on money you work for. Your periodic payments compensate you for an injury, not for labor.

The IRS treats injury compensation as a return of something taken from you, not as earnings. This mirrors how personal injury settlements are structured in the first place.

💡 Expert Note (CFA): In my 28 years advising clients, the most expensive error I see is a self-employed recipient adding tax-free settlement payments to their estimated-tax worksheet. One client overpaid by thousands before we separated the two streams correctly.

What “net earnings from self-employment” means

Net earnings from self-employment are your business revenue minus deductible business expenses. Settlement payments appear nowhere in that math.

So a freelancer earning business profit and receiving injury payments owes self-employment tax on the profit alone.

Are structured settlement payments taxable income?

Structured settlement payments for personal physical injury or sickness are not taxable under IRC §104(a)(2); payments tied to other claims can be taxable.

The dividing line is the origin of the claim. Compensation for a physical injury stays tax-free, including medical costs and pain.

Punitive damages, interest on the award, lost-wage replacement, and emotional distress unrelated to a physical injury are generally taxable income. Your settlement agreement’s allocation drives the result.

Physical injury payments stay tax-free

Money paid because your body was harmed is excluded, whether it arrives as one check or a stream. The annuity growth inside a qualifying injury settlement stays tax-free too.

📊 Data Point: Damages received for personal physical injuries or physical sickness are excluded from gross income under IRC §104(a)(2) — Source: Internal Revenue Service, 2026.

What part of a settlement is taxable

Some components never qualify for the exclusion, even inside an injury case:

- Punitive damages are taxable as ordinary income in nearly all cases, reported on Schedule 1.

- Interest that accrued on the award is taxable like any other interest income.

- Lost-wage or back-pay components from an employment claim are taxable and may even face payroll-type taxes.

- Emotional distress with no underlying physical injury is taxable in full.

For a fuller breakdown, see our explainer on how structured settlement payments are taxed, and the IRS guidance on settlement taxability. If you later invest a lump sum, those earnings are taxable, and our capital gains tax calculator can estimate the bite.

How to report income when you’re self-employed and receiving a settlement

First, report only your net business earnings on Schedule SE if they total $400 or more; your tax-free settlement payments stay off the return entirely.

Here is the 2026 sequence for a self-employed recipient:

- Separate the streams — list business revenue and excluded injury payments on separate lines in your records.

- Exclude the §104(a)(2) payments — do not enter them as income on Form 1040.

- Report business profit on Schedule C, then calculate self-employment tax on Schedule SE if net earnings reach $400.

- Set up estimated taxes with Form 1040-ES if you expect to owe $1,000 or more for the year.

- Keep your settlement agreement filed, in case the IRS questions the exclusion.

Do you get a 1099 for settlement payments?

Tax-free injury payments generally produce no Form 1099. Your business clients, however, may issue one for your work.

📊 Data Point: For 2026, the Form 1099-NEC and 1099-MISC reporting threshold for business payments rose from $600 to $2,000 — Source: IRS Publication 15, 2026.

That change touches your self-employment income reporting, not your excluded settlement. The IRS self-employed filing requirements spell out the $400 and estimated-tax rules in detail.

Setting up quarterly estimated taxes

Because no employer withholds for you, the IRS expects quarterly payments on business profit. Map your year first with a take-home pay calculator so each installment is realistic.

⚠️ Warning: Mischaracterizing a mixed settlement — treating taxable lost-wage or punitive portions as tax-free — can trigger back taxes and penalties. Confirm your allocation with a licensed tax professional before you file.

How much self-employment tax will you owe in 2026?

For 2026, self-employment tax is 15.3% — 12.4% for Social Security plus 2.9% for Medicare — applied to 92.35% of your net business earnings.

The Social Security portion stops at a wage cap. The Medicare portion has no ceiling.

📊 Data Point: The 2026 Social Security wage base is $184,500, and the self-employment tax rate is 15.3% — Source: IRS Publication 15 and the Social Security Administration, 2026.

Does settlement income count toward the Social Security wage base?

No. The $184,500 cap applies to wages and self-employment earnings only.

Your settlement payments are excluded damages, not earnings, so they never push you toward that cap. They also never trigger the additional Medicare tax of 0.9% that applies above $200,000 (single) or $250,000 (married filing jointly).

A worked 2026 example

Picture a self-employed designer with $80,000 in net business profit who also receives $40,000 a year in injury settlement payments.

Self-employment tax applies to the $80,000 of business profit only. The $40,000 settlement is invisible to the calculation — it does not count toward the $184,500 cap or add a dollar of tax.

| Income stream | Taxable? | In SE tax base? | Counts toward $184,500 cap? |

|---|---|---|---|

| Structured settlement (physical injury) | No | No | No |

| Net self-employment profit | Yes | Yes | Yes |

| Punitive damages / interest | Yes | No | No |

Source: IRS, IRC §104(a)(2) and Schedule SE rules, 2026.

Estimate your own split with an income tax calculator and check the cap interaction using a Social Security calculator. The IRS rules for self-employment tax and the 2026 wage-base figures confirm both numbers.

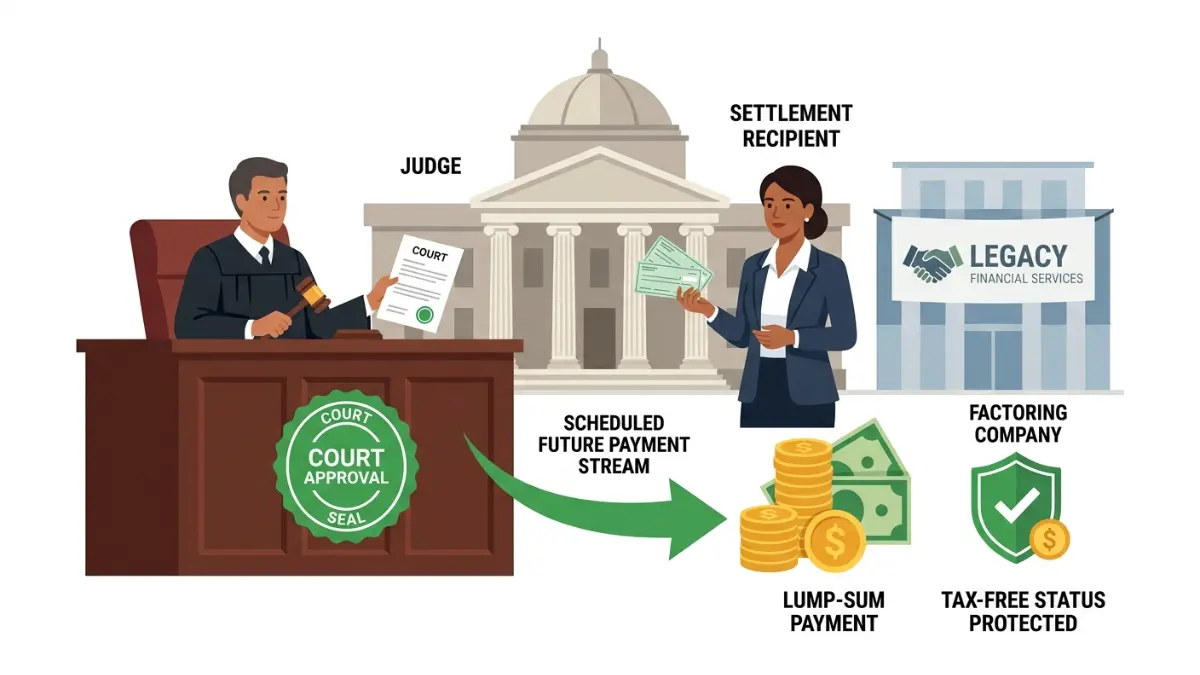

Does selling your structured settlement create a tax bill?

Selling structured settlement payments can trigger a steep federal tax unless a court signs off first.

A factoring company that buys your payments without court approval faces a 40% excise tax under IRC §5891. That tax falls on the buyer, but it shapes every offer you receive.

How court approval protects the tax-free status

Every legitimate sale runs through a judge under your state’s Structured Settlement Protection Act. The judge applies a best-interest test before approving the transfer.

Once a court approves the sale, the lump sum keeps the same tax-free character as the original payments. Skip that step and the deal collapses, or the economics turn against you.

⚠️ Warning: Treat any buyer who rushes you past court approval as a red flag. Our guide to the process of selling future payments walks through the protections you keep by doing it correctly.

A CFA’s take: planning when you have two income streams

Two income streams give you planning room that single-income filers do not have.

Your tax-free settlement covers baseline needs while your business income can fund tax-advantaged accounts. That sequencing is where real money is made or lost.

The mistake I see self-employed clients make

The recurring error is letting tax-free cash flow blur the discipline around business taxes. Clients relax on estimated payments because total cash looks healthy, then face an underpayment penalty in April.

💡 Expert Note (CFA): I tell self-employed clients to ring-fence the settlement mentally and run the business as if it were their only income for tax purposes. That single habit prevents the most common and costly filing surprises I encounter.

Smart planning moves for 2026

Business profit, not settlement money, is what funds your retirement shelters. Model the long arc with a retirement calculator before choosing a vehicle.

A self-employed earner can route profit into a Roth or solo plan; a Roth IRA calculator shows the tax-free growth potential. Remember the deduction worth half of your self-employment tax, and steady your uneven cash flow with a budget calculator built for irregular income.

Structured settlement and self-employed taxes: FAQ

1. Do you pay self-employment tax on a structured settlement?

No. A structured settlement from a personal physical injury is excluded from gross income under IRC §104(a)(2), so it is not net earnings from self-employment. The 15.3% self-employment tax applies only to your business profit, never to your tax-free settlement payments.

2. Are structured settlement payments considered earned income?

No. Earned income comes from working — wages or self-employment profit. Structured settlement payments for physical injury are excluded damages, not earned income, so they do not count toward self-employment tax, the Social Security wage base, or work-based credits.

3. Are structured settlement payments taxable?

Structured settlement payments for personal physical injury or sickness are not taxable under IRC §104(a)(2). Payments for punitive damages, lost wages, or emotional distress without a physical injury are taxable. How your settlement agreement allocates each category determines the final tax outcome you face.

4. Do I get a 1099 for structured settlement payments?

Usually not. Tax-free structured settlement payments for physical injury generally generate no Form 1099. For 2026, the 1099-NEC reporting threshold for business payments rose to $2,000, but that affects your self-employment income, not your excluded settlement payments.

5. Do I report structured settlement payments on my tax return?

Tax-free structured settlement payments for physical injury are not reported as income on Form 1040. You still report and pay self-employment tax on your business profit using Schedule SE. Keep your settlement agreement on file in case the IRS asks.

6. How much is self-employment tax in 2026?

For 2026, self-employment tax is 15.3% — 12.4% for Social Security plus 2.9% for Medicare — applied to 92.35% of your net business earnings. Your structured settlement payments are excluded entirely, so they never raise your self-employment tax bill for the year.

7. Do settlement payments count toward the Social Security wage base?

No. The 2026 Social Security wage base of $184,500 applies to wages and self-employment earnings only. Your structured settlement payments are excluded damages, not earnings, so they never count toward that cap or change your self-employment tax.

8. Is selling my structured settlement taxable?

Selling structured settlement payments can trigger a 40% federal excise tax on the buyer under IRC §5891 unless a court approves the transfer under your state’s protection act. A court-approved sale keeps the original tax-free status on the lump sum you receive.

9. What part of a settlement is taxable?

In a structured settlement, punitive damages, interest, lost-wage replacement, and emotional distress unrelated to a physical injury are taxable as ordinary income. Compensation for the physical injury itself, including medical costs and pain, stays tax-free under IRC §104(a)(2).

10. Do I owe state tax on a structured settlement if self-employed?

Most states follow federal rules, so a structured settlement for physical injury that is tax-free federally is also free of state income tax. Your self-employment income stays taxable wherever your business operates, though a handful of states levy no income tax at all.

11. Do I need to make quarterly estimated tax payments?

If you expect to owe $1,000 or more on your self-employment income, the IRS generally requires quarterly estimated payments using Form 1040-ES. Your tax-free structured settlement payments do not create this requirement on their own under the 2026 rules.

The bottom line on settlements and self-employment tax

Your structured settlement for a physical injury is tax-free under IRC §104(a)(2), and it stays outside your self-employment tax no matter how much your business earns.

The only stream the 15.3% self-employment tax touches is your business profit, capped for Social Security at the 2026 wage base of $184,500. Punitive damages, interest, and non-physical components are the exceptions that can be taxable.

Separate the two buckets, report only the business side on Schedule SE, and confirm any mixed-settlement allocation with a CPA or Enrolled Agent before you file. Then download our self-employed tax checklist to keep every 2026 deadline in front of you.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.