Car Insurance Calculator — Real 2026 Rates

Car Insurance Calculator (Estimate)

Estimate annual, 6‑month, and monthly premiums with a transparent breakdown (coverages, deductibles, risk profile, discounts, taxes/fees) plus scenario tables and CSV export. This tool is for education/benchmarking—not an insurer quote.

Inputs

Higher deductibles often lower premiums. [web:290]

This model is designed to be explainable (not “mysterious”) so users can learn how each lever changes the estimate.

Results

Estimated premium

—

6‑month: —

Monthly: —

Taxes & fees

Pre‑tax premium: —

Tax amount: —

Fixed fees: —

Model factors

Base: —

Coverage factor: —

Deductible factor: —

Risk & discounts

Risk factor: —

Discount factor: —

Tip: tweak deductibles + limits to compare.

Step-by-step premium build-up

Scenario: Deductibles (collision = comp)

| Deductible | Annual total | Monthly | Pre-tax |

|---|

Scenario: Coverage mixes

| Scenario | Liability delta (model) | Collision | Comprehensive | Annual total |

|---|

Results appear after you click “Calculate.”

In This Article

The national average for full coverage car insurance in 2026 is $216 per month ($2,575/year) — and rates have surged 57% since 2022. If you haven’t compared your car insurance recently, there’s a real chance you’re overpaying by hundreds of dollars. Use the car insurance calculator above to estimate your real 2026 premium in under two minutes.

In this guide, you’ll learn:

- ✅ How to use this auto insurance calculator step by step

- ✅ Real 2026 average rates by age, record, and vehicle type

- ✅ The 9 factors that directly move your premium up or down

- ✅ 8 proven strategies to lower your car insurance cost today

What Is a Car Insurance Calculator — and Why 2026 Rates Are Different

A car insurance calculator is an estimation tool that combines your driver profile, vehicle details, coverage choices, and location risk to give you a projected annual premium — before you contact any insurer.

But 2026 is not a normal year for auto insurance.

New 2026 tariffs on steel, aluminum, and foreign vehicles are pushing the cost of auto parts higher, which is directly feeding into rising insurance premiums. Insurers are repricing policies faster than at any point in the last decade.

The result: Drivers who last compared rates 12–18 months ago may now be sitting on a 15–25% overcharge. That’s $400–$650 out of pocket — every single year.

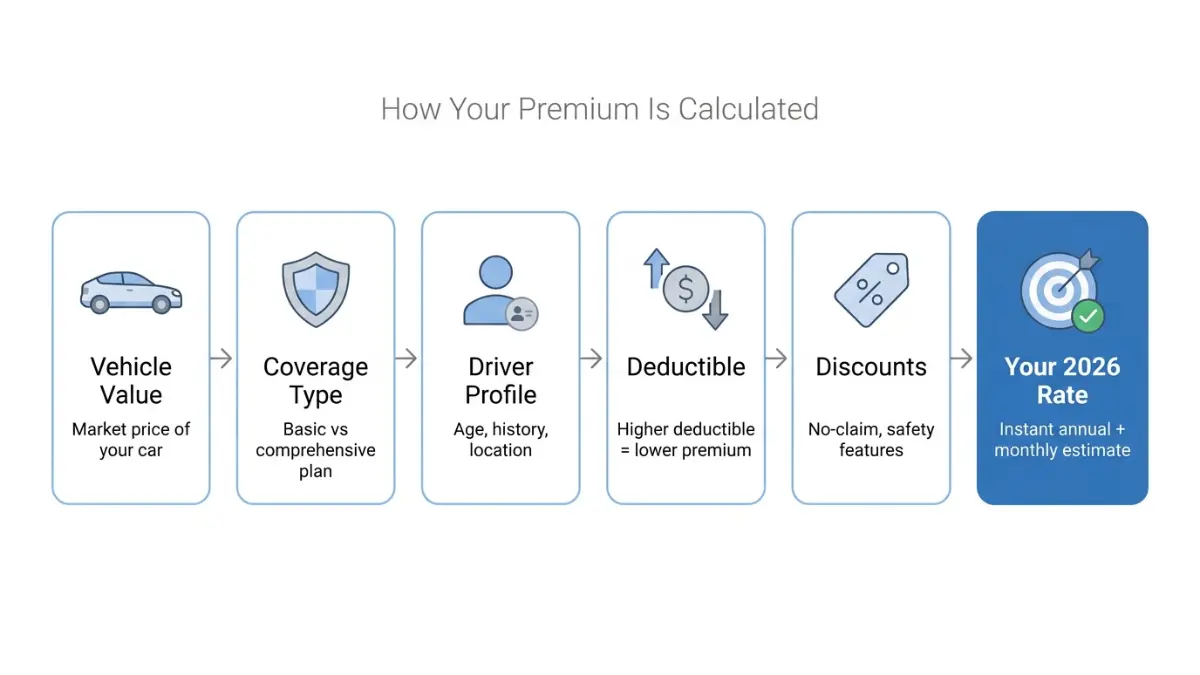

This car insurance cost estimator uses a transparent 6-step premium build-up model (base premium → coverage factors → deductibles → risk profile → discounts → taxes/fees), so you can see exactly which levers control your rate — not just a mysterious black-box number.

What this means for you: Your rate isn’t random. Every input you change in the calculator above has a measurable, calculable effect on your premium.

How to Use This Car Insurance Calculator — 6 Steps to Your Real 2026 Estimate

Most car insurance calculators give you a single number and no explanation. This tool is different — it shows you the full step-by-step premium build-up, so you understand why you’re being quoted what you’re quoted.

Step 1: Choose Your Base Premium Model

Select one of two methods:

- Vehicle Value × Rate — Enter your car’s current market value and a base rate per $1,000 of value (typically 10–15 for standard vehicles)

- Manual Base Premium — Enter a known base annual figure if you already have a quote to compare against

Step 2: Select Your Coverage Levels

Choose from:

| Coverage | What It Covers | Approx. Premium Impact |

|---|---|---|

| Liability (Standard) | Third-party injuries & property damage | Baseline |

| Collision | Your car after an at-fault crash | +20% |

| Comprehensive | Theft, weather, vandalism | +10% |

| UM/UIM | Uninsured/underinsured motorist | +6% |

| PIP / Med Pay | Medical costs regardless of fault | +5% |

Key Fact: As of 2023, more than 1 in 7 U.S. drivers — 15.4% — were uninsured. UM/UIM coverage isn’t optional; it’s essential protection. Learn more about coverage types in our comprehensive car insurance guide.

Step 3: Set Your Driver Profile

Enter your:

- Age band (under 25, 25–34, 35–64, 65+)

- Driving experience (under 3 years, 3–7 years, 8+ years)

- Driving record (clean, minor violations, at-fault accident, DUI)

- Annual mileage (under 5K, 5–10K, 10–15K, 15K+)

- Location risk (low, average, high, very high)

Step 4: Choose Your Deductibles

| Deductible | Effect on Premium | Best For |

|---|---|---|

| $250 | Higher premium | Low emergency savings |

| $500 | Baseline | Most drivers |

| $1,000 | ~12% savings | Stable emergency fund |

| $2,000 | ~22% savings | High net worth / low-mileage |

Rule: Only raise your deductible to an amount you can comfortably cover out of pocket. If your savings calculator shows less than $1,000 in reserves, stick to the $500 deductible.

Step 5: Apply Your Discounts

Check every box that applies:

- Anti-theft device — saves ~5%

- Bundle home + auto — saves up to 8%

- Pay in full — saves ~3% plus avoids installment fees

Step 6: Set a Target Annual Premium (Optional)

Enter a target premium amount. The calculator will identify the optimal deductible combination to get you closest to that number — a feature no competitor offers.

Real 2026 Car Insurance Rates — Data by Profile

National Average Car Insurance Cost 2026

| Coverage Type | Monthly | Annual |

|---|---|---|

| Full Coverage | $216 | $2,575 |

| Liability Only | $100 | $1,202 |

| Minimum Coverage | $68 | $820 |

Source: MoneyGeek, Bankrate, Insure.com — March 2026 composite

Car Insurance Cost by Age — 2026

A 20-year-old driver pays an average of $395/month for full coverage, compared to $188/month for a 40-year-old. Age is the single largest rating factor for new drivers.

| Age Group | Monthly (Full Coverage) | vs. National Avg |

|---|---|---|

| Under 25 | $395–$537 | +85–149% |

| 25–34 | $220–$260 | +2–20% |

| 35–64 | $188–$216 | Baseline |

| 65+ | $240–$270 | +11–25% |

Car Insurance Cost by Driving Record — 2026

Your driving record is the most controllable factor in your premium. Here’s the real cost of each violation:

| Record Type | Monthly Premium | Annual Cost | vs. Clean Record |

|---|---|---|---|

| Clean | $216 | $2,575 | Baseline |

| 1 Speeding Ticket | $275 | $3,311 | +28% |

| At-Fault Accident | $322 | $3,868 | +50% |

| DUI Conviction | $420+ | $5,000+ | +96% |

After a DUI conviction, drivers pay an average of 96% more for car insurance, and that conviction may stay on their driving record for 10 years or more.

2026 Car Insurance Rates by State — Cheapest vs. Most Expensive

| Cheapest States | Monthly Avg | Most Expensive States | Monthly Avg |

|---|---|---|---|

| Vermont | $104 | Florida | $303 |

| New Hampshire | $138 | Louisiana | $348 |

| Maine | $142 | Maryland | $352 |

| Ohio | $145 | Connecticut | $317 |

| Idaho | $148 | New York | $301 |

⚠️ 2026 Tariff Alert: Rising costs of parts and replacement vehicles due to tariffs, in addition to increased accident severity, extreme weather, rising medical expenses, and legal fees, have all contributed to higher premiums across all states. Even “cheap” states are seeing 10–18% rate increases in 2026.

For drivers comparing the full cost of vehicle ownership, our auto loan calculator can help you factor insurance into your total monthly payment.

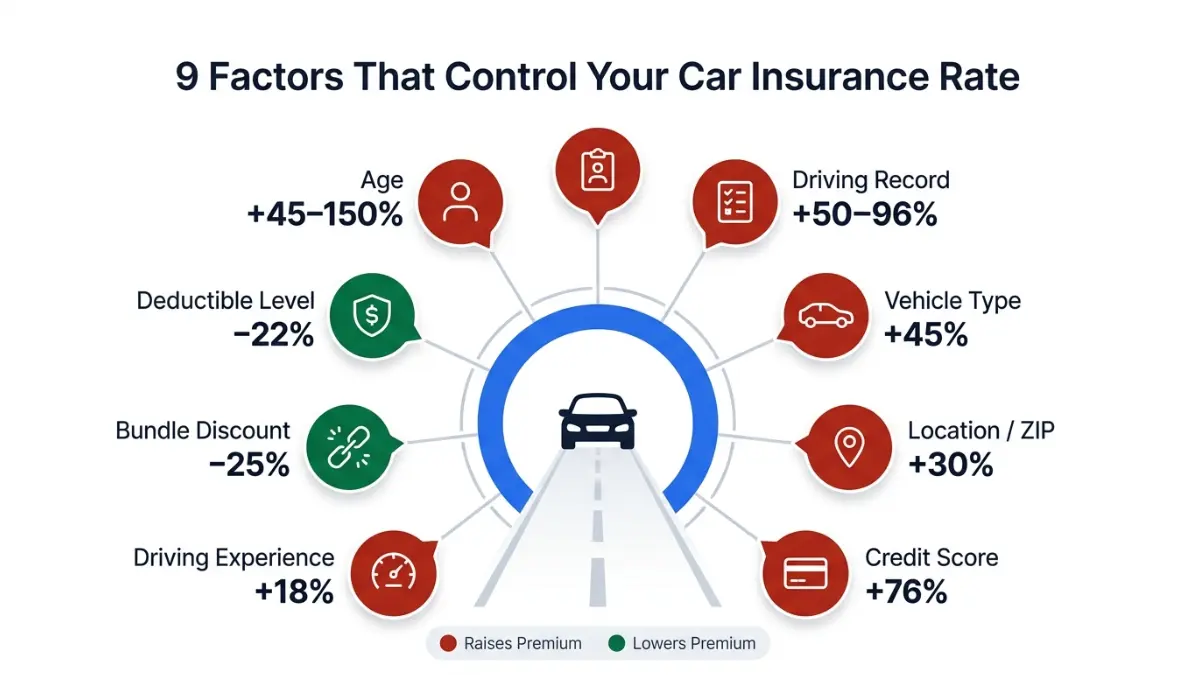

9 Factors That Determine Your Car Insurance Premium (With % Impact)

According to the Insurance Information Institute, insurers use a complex set of rating factors to calculate auto insurance premiums. Here’s exactly what each factor does to your rate:

| # | Factor | Premium Impact |

|---|---|---|

| 1 | Age (under 25) | +45–150% |

| 2 | DUI conviction | +96% |

| 3 | At-fault accident | +50% |

| 4 | Vehicle type (sports car) | +45% |

| 5 | Location (very high risk) | +30% |

| 6 | Poor credit score | +76% |

| 7 | High annual mileage (15K+) | +18% |

| 8 | No anti-theft / discounts | +5–8% |

| 9 | Paying monthly vs. annual | +3–5% |

Credit Score & Car Insurance — A Costly Blind Spot

Drivers with poor credit pay nearly 76% more for full coverage car insurance compared to those with good credit. Most drivers don’t realize their credit score is being used against them at renewal time.

Important exception: California, Hawaii, Massachusetts, and Michigan prohibit insurers from using credit scores in rate calculations. If you live in one of these states, your credit won’t affect your auto insurance premium. Check your credit score calculator to see where you stand.

Vehicle Type — The Hidden Rate Multiplier

| Vehicle Type | Premium vs. Sedan Baseline |

|---|---|

| Sedan (standard) | Baseline |

| SUV / MPV | +5% |

| Electric Vehicle | +15% |

| Luxury | +25% |

| Sports / Performance | +45% |

EVs deserve special attention in 2026. Higher repair costs and specialized parts make EVs 15% more expensive to insure than comparable sedans — a gap that’s widening as tariffs raise parts prices further. If you’re financing a vehicle, use our car lease calculator to model the full cost of ownership including insurance.

8 Proven Ways to Lower Your Car Insurance in 2026

The average American is leaving $400–$900/year on the table by not actively managing their car insurance. Here’s how to stop that.

1. Compare Quotes From at Least 5 Insurers

Each insurer has unique underwriting formulas, risk factors, and discount options, which means rates for the same driver and vehicle can vary 40–50% between companies. This is the single highest-ROI action you can take.

Action step: Set a calendar reminder every 12 months — at minimum before each renewal — to run fresh quotes.

2. Raise Your Deductible Strategically

Moving from a $500 to a $1,000 deductible typically saves 12% on your annual premium. On a $2,575 average policy, that’s $309/year. Keep the deductible amount in a dedicated emergency fund — use our savings calculator to plan this buffer.

3. Bundle Home + Auto Insurance

Bundling your home and auto policies with the same insurer saves an average of 8–25%. Getting homeowners insurance from the same provider as your car insurance can save you as much as 25%. For homeowners evaluating their full picture, our home affordability calculator and our homeowners insurance guide are essential resources.

4. Drop Collision/Comprehensive on Older Vehicles

If a car is worth less than $1,000, or less than 10 times the insurance premium, purchasing collision and comprehensive coverage may not be cost effective. This is the classic “when to drop full coverage” rule — and most drivers ignore it far too long.

5. Use Telematics / Usage-Based Insurance

Telematics programs track driving habits (speed, hard braking, mileage) via an app or OBD device. Safe drivers can earn 10–30% premium reductions. If you work from home and drive under 5,000 miles/year, this can be a major win.

6. Maintain a 5-Year Clean Record

By maintaining a clean driving record for at least five years with no collisions, at-fault accidents, or violations, drivers can save up to 10% on their auto insurance policy.

7. Pay Your Premium in Full

Paying annually instead of monthly eliminates installment fees and often unlocks a 3–5% pay-in-full discount. On a $2,575 policy, that’s $77–$128 saved with zero effort. If cash flow is a concern, use our budget calculator to plan for the lump payment.

8. Audit Every Available Discount

Most insurers offer 15–20 discounts. The average driver claims only 2–3. Check your eligibility for:

- ✅ Safe driver discount

- ✅ Good student discount (under 25 with B+ average)

- ✅ Low mileage / work-from-home discount

- ✅ Anti-theft / vehicle safety features

- ✅ Military / professional association discount

- ✅ Paperless billing discount

- ✅ Defensive driving course completion

Pro tip: For a broader view of how insurance fits into your overall financial plan, see our guide to affordable car insurance options in 2026 and our car insurance cost-cutting strategies.

The Federal Trade Commission’s consumer auto resources also provide government-verified guidance on understanding your policy terms before signing.

Frequently Asked Questions — Car Insurance Calculator 2026

1. How accurate is a car insurance calculator?

A car insurance estimator provides a planning-level estimate — typically within 15–25% of a real quote. It won’t replace an actual underwritten quote, but it gives you a calibrated baseline so you can spot when a live quote seems too high or too low.

2. What is the average car insurance cost per month in 2026?

The national average cost of full coverage car insurance in 2026 is $216 per month ($2,575 annually), up 11.3% from the prior year. Minimum coverage averages $100/month.

3. How do I calculate my car insurance premium?

Insurers multiply a base rate by these core factors:

– Your vehicle value and type

– Coverage level selected

– Driver age, record, and experience

– Location ZIP code risk

– Credit score (most states)

– Chosen deductibles

4. What’s the difference between liability and full coverage?

Liability only pays for damage you cause to others — it does not cover your own vehicle. Full coverage adds collision (your car in an accident) and comprehensive (theft, weather, vandalism). If your car is financed or leased, full coverage is typically required by the lender.

5. Does a car insurance calculator give me a real quote?

No. A car insurance cost calculator is an estimation tool, not an insurer quote. Real quotes require your VIN, driver’s license, and underwriter verification. Use the calculator to benchmark — then get 3–5 actual quotes to compare.

6. How much does a DUI raise car insurance rates?

A DUI conviction raises average premiums by 96% — nearly doubling your annual cost. That conviction can stay on your driving record for 10 years or more, meaning the financial impact extends for a decade.

7. Is $200/month for car insurance too much in 2026?

It depends on your state. The nationwide average for full coverage is $181/month by some measures, meaning $200 is near-average nationally. In Vermont it’s above average; in Florida or New York, it’s a bargain.

8. What deductible should I choose for car insurance?

Choose the highest deductible you can comfortably pay out of pocket in an emergency. If you have a solid emergency fund (3–6 months of expenses), a $1,000 deductible saves you ~12% annually. Use our debt-to-income ratio calculator to check your financial resilience before raising your deductible.

9. Can I lower my car insurance if I work from home?

Yes. Driving under 5,000 miles/year often qualifies you for a low-mileage discount of 5–15%. Notify your insurer of your new commuting situation — many won’t proactively offer this reduction without being asked.

10. Which states have the cheapest car insurance in 2026?

The five cheapest states for full coverage are:

Vermont — ~$104/month

New Hampshire — ~$138/month

Maine — ~$142/month

Ohio — ~$145/month

Idaho — ~$148/month

11. Does bundling home and auto insurance actually save money?

Yes — in most cases significantly. AARP members who switch to The Hartford, for example, can save an average of $577 on their car insurance through bundling and membership discounts. Always verify the bundled price beats standalone policies from specialists before committing.

⚠️ Disclaimer: This car insurance calculator is for educational and benchmarking purposes only. All results are estimates based on general rating factors and 2026 national average data — they are not actual insurer quotes. Rates vary by insurer, state regulations, credit history, and individual underwriting criteria. Always obtain quotes directly from licensed insurance providers before making coverage decisions. FinanceAuthorityHub.com is not an insurance company, insurance broker, or licensed insurance agent. This article does not constitute financial or insurance advice.

Sources: Insurance Information Institute — Auto Insurance Facts & Statistics | FTC Consumer Auto Resources | Bankrate March 2026 Rate Analysis | MoneyGeek 2026 Data | Insure.com 2026 National Averages

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.