Car Lease Calculator: Exact Payment, No Dealer Games

Car Lease Calculator

Estimate lease payment breakdown (depreciation + rent charge + tax), due at signing, total out-of-pocket, and a full monthly schedule with CSV export.

Inputs

If payoff > value, negative equity is rolled into cap cost.

Results

Total monthly payment

—

Base: — • Tax: —

Monthly components

Depreciation: —

Rent charge: —

Rate detail

Money factor: —

APR equivalent: —

Term: —

Due at signing (estimate)

—

Includes 1st month: —

Lease structure

MSRP: — • Selling price: —

Residual: — (—)

Gross cap cost: — • Cap reductions: — • Adjusted cap cost: —

Trade equity (value − payoff): —

Totals & efficiency

Total paid during lease (payments + any upfront tax): —

Total out-of-pocket (includes due at signing + end fee): —

Total cost (net of refundable deposit): —

Total tax (estimate): — • Upfront tax (if chosen): —

Fees: total — • rolled — • upfront —

Mileage allowed (estimate): — • Effective cost per mile: —

Security deposit (often refundable): — • Disposition fee (end): —

Educational estimate. Local tax rules and lender fee handling vary significantly by country/state.

Yearly summary

| Year | Total paid | Depreciation | Rent charge | Tax |

|---|

Monthly schedule (estimated)

| Month | Total payment | Depreciation | Rent charge | Tax | Remaining depreciation | Estimated value line |

|---|

Results appear after you click “Calculate.”

In This Article

What Does a Car Lease Calculator Tell You?

A car lease calculator gives you the exact monthly lease payment before you step into any dealership. It uses the same formula leasing companies use — so you walk in with the real number, not the one a dealer manufactures to maximize their profit.

Here is what you get instantly:

- Your exact monthly lease payment (depreciation + rent charge + tax)

- Due at signing — the full upfront cost, not just the headline number

- Total out-of-pocket over the entire lease term

- A full monthly schedule with depreciation breakdown

- Effective cost per mile based on your mileage allowance

2026 Reality Check: The average monthly lease payment in the U.S. hit approximately $590/month in early 2025, according to Experian’s State of the Automotive Finance Market report — and payments have held elevated heading into 2026. New tariffs on imported vehicles are adding further upward pressure. Knowing your exact number before you negotiate is no longer optional. It’s survival.

Use the calculator above, then read the complete guide below to understand every number it produces — and every game a dealer will play to inflate it.

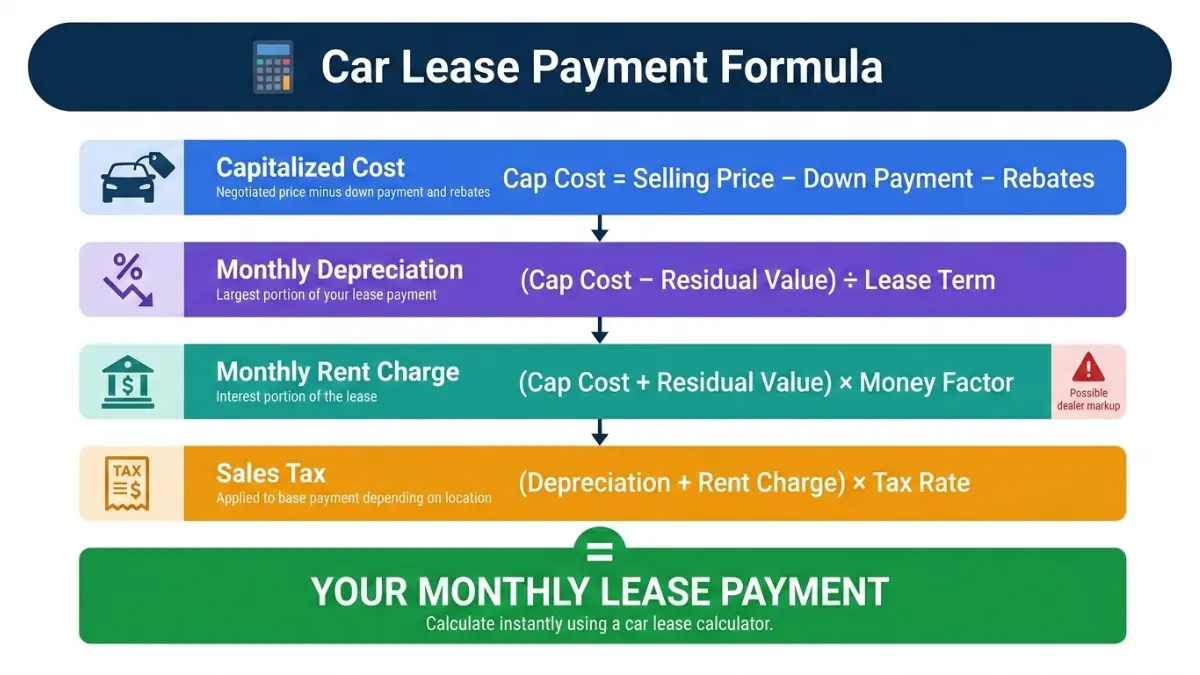

How Does a Car Lease Calculator Work? (The Formula Dealers Hide From You)

Most Americans have no idea how a car lease payment is actually calculated. Dealerships prefer it that way. Here is the complete formula — the same one our car lease calculator runs automatically.

The 3 Numbers That Control Your Monthly Lease Payment

| Component | What It Is | The Dealer Game |

|---|---|---|

| Capitalized Cost (Cap Cost) | The negotiated selling price of the car | Dealers start at MSRP — negotiate this down like you’re buying outright |

| Residual Value | The car’s estimated worth at lease end (set by the bank, not the dealer) | Cannot negotiate — but choosing a high-residual car lowers your payment |

| Money Factor (MF) | The interest rate expressed as a small decimal | Dealers mark this up above the “buy rate” — always ask for the base rate |

Understanding all three is the difference between a great deal and being quietly overcharged for 36 months. The Consumer Financial Protection Bureau confirms that lease terms — including the selling price — are negotiable, and that the residual value is the bank’s estimate of the car’s future worth.

The Step-by-Step Lease Formula (With Real Numbers)

Let’s use a real example: a $42,000 MSRP car, negotiated to $39,500, with a 58% residual and a money factor of 0.00225 on a 36-month lease.

Step 1 — Calculate Monthly Depreciation:

(Capitalized Cost − Residual Value) ÷ Lease Term ($39,500 − $24,360) ÷ 36 = $420.56/month

Step 2 — Calculate Monthly Rent Charge:

(Capitalized Cost + Residual Value) × Money Factor ($39,500 + $24,360) × 0.00225 = $143.69/month

Step 3 — Base Monthly Payment:

$420.56 + $143.69 = $564.25/month

Step 4 — Add Sales Tax (example: 8.25%):

$564.25 × 1.0825 = $611.34/month total

This is the exact number our car lease calculator produces in under 3 seconds. No spreadsheet. No dealership visit required.

Money Factor to APR — The Conversion Dealers Deliberately Obscure

Dealers quote the money factor as a tiny decimal like 0.00225 because it sounds harmless. It isn’t.

The conversion is simple: Money Factor × 2,400 = Equivalent APR

- MF of 0.00225 = 5.4% APR — acceptable for good credit

- MF of 0.00400 = 9.6% APR — expensive

- MF of 0.00125 = 3.0% APR — excellent, seek this

⚠️ Key Takeaway: If a dealer refuses to disclose the money factor — walk out. Under the Federal Trade Commission’s Consumer Leasing Act guidelines, you have the right to full transparency on all lease terms before signing.

A dealer who marks up the money factor by just 0.001 adds approximately $72/month on a $40,000 car — that’s $2,592 in silent profit over 36 months.

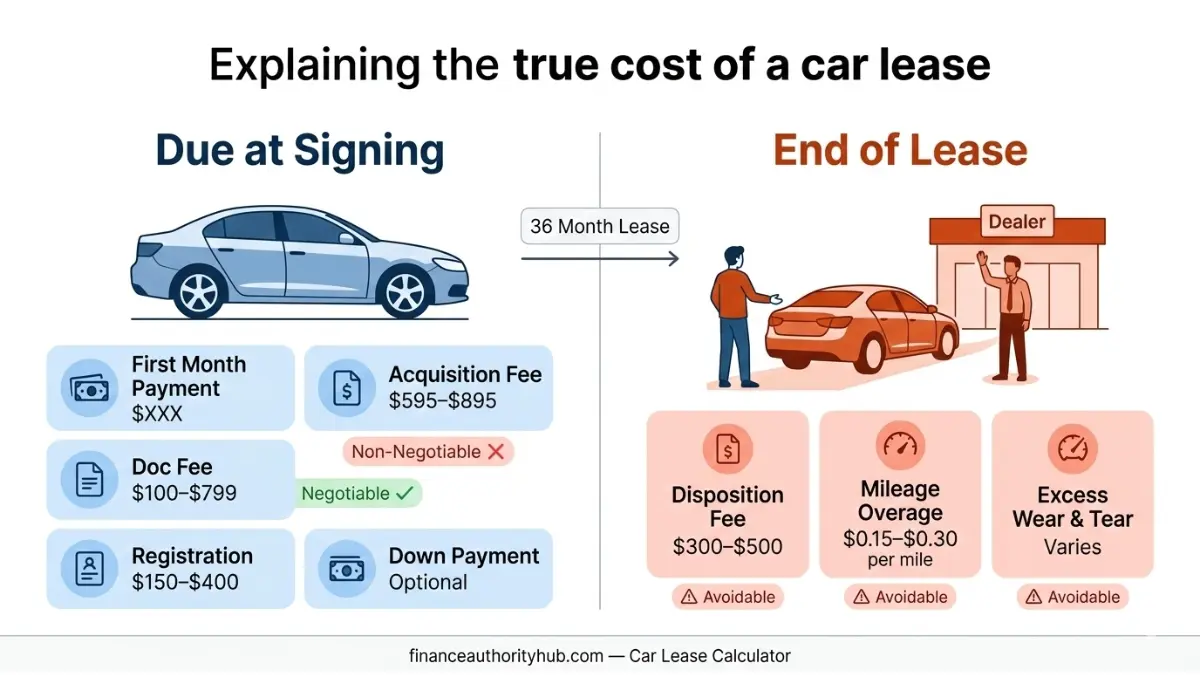

Every Car Lease Fee Explained — The Ones Buried in Fine Print

The monthly payment is only part of what you pay. Here is every fee our auto lease calculator accounts for — and what you need to watch.

Fees Due at Signing (Upfront Costs)

| Fee | Typical Range (USA) | Negotiable? |

|---|---|---|

| Acquisition fee (bank fee) | $595 – $895 | Rarely — set by the lender |

| Documentation fee | $100 – $799 | Sometimes |

| Registration & title | $150 – $400 | No — state-set |

| Down payment (cap cost reduction) | $0 – $3,000+ | Yes — keep it as low as possible |

| First month’s payment | Varies | Built into lease structure |

| Security deposit | $0 – $500 | Often waivable — ask |

Critical Warning on Down Payments: Putting a large down payment on a lease is financially dangerous. If your car is totaled or stolen in month 2, that money is gone. The FTC advises consumers to focus on total cost, not just monthly payment. A larger down payment on a lease builds zero equity and recovers nothing in a total loss scenario. If you need gap coverage, review your options through our Gap Insurance guide.

End-of-Lease Fees (The Surprise Charges)

These are the fees competitors rarely warn you about upfront.

| Fee | Amount | How to Avoid |

|---|---|---|

| Disposition fee | $300 – $500 | Often waived if you lease another car from the same brand |

| Mileage overage | $0.15 – $0.30/mile | Pre-buy extra miles upfront — it’s cheaper mid-lease |

| Excess wear & tear | Varies | Pre-inspection 60–90 days before return |

Mileage Overage Reality: The average American drives approximately 15,000 miles per year. Most standard leases cap at 10,000–12,000 miles. If you drive 15,000 miles over 3 years on a 12,000-mile cap, you owe 9,000 miles × $0.25 = $2,250 at turn-in. Our car lease calculator factors your annual mileage into the cost-per-mile analysis — use it before you accept any mileage tier.

Car Leasing in 2026: Is It Still Worth It?

Why Lease Payments Are Elevated in 2026

Lease payments remain elevated compared to pre-pandemic levels. Vehicle prices, interest rates, and shifting residual values all pushed costs higher over the past three years — and 2026 brings a new pressure: tariffs on imported vehicles that analysts warn could add $2,000–$5,000 to sticker prices on popular models.

Average Monthly Lease Payment by Segment (March 2026):

| Vehicle Segment | Average Monthly Payment | Best Value Pick |

|---|---|---|

| Compact Sedan | $289 – $340/mo | Honda Civic, Toyota Camry |

| Compact SUV | $299 – $420/mo | Honda CR-V, Toyota RAV4 |

| Luxury Sedan | $450 – $650/mo | Genesis G70 (best value) |

| Luxury SUV | $550 – $750/mo | Genesis GV70 (undercuts BMW/Mercedes) |

| Electric Vehicle | $199 – $399/mo | Chevrolet Equinox EV (best 2026 deal) |

The EV Lease Advantage — $7,500 That Goes Directly Into Your Pocket

Leasing an electric vehicle in 2026 is one of the smartest financial decisions you can make. Here is why:

- When you lease an EV, the leasing company — not you — claims the federal $7,500 clean vehicle tax credit

- That $7,500 is passed through as a cap cost reduction, directly lowering your monthly payment

- You get the credit regardless of your income or tax liability — removing the income limits that block many buyers from the credit on purchased EVs

- The Chevrolet Equinox EV, Hyundai Ioniq 6, and Honda Prologue are all structured to maximize this pass-through in 2026

Before you calculate an EV lease, use our Auto Loan Calculator to compare whether financing the same EV outright delivers better long-term value for your situation.

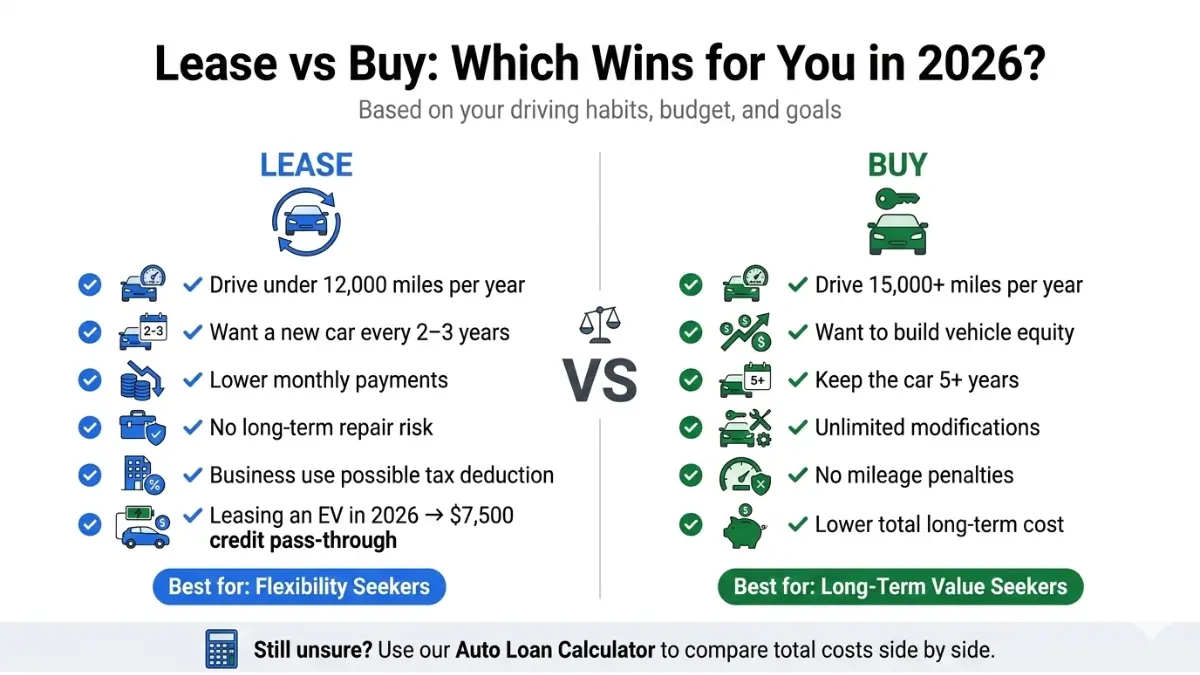

Lease vs. Buy — When Each Option Wins

| Your Situation | Lease ✅ | Buy ✅ |

|---|---|---|

| Drive under 12,000 miles/year | ✅ | |

| Want a new car every 2–3 years | ✅ | |

| Drive 18,000+ miles/year | ✅ | |

| Want to build vehicle equity | ✅ | |

| Business owner (tax deduction potential) | ✅ | |

| Long-term cost minimization | ✅ | |

| Don’t want repair risk | ✅ |

If you are comparing a lease against a home purchase or other major financial commitments, our Home Affordability Calculator and Debt-to-Income Ratio Calculator can help you see the full picture of your monthly obligations before you commit.

7 Dealer Games Our Car Lease Calculator Helps You Crush

This is what no competitor covers. These are the exact tactics dealers use — and how knowing your car lease payment in advance destroys every one of them.

Game #1 — The Inflated Cap Cost

Dealers present the MSRP as the starting negotiation point for a lease. Treat it like a purchase. Negotiate the selling price to invoice or below before you reveal you plan to lease. A $2,000 reduction in cap cost saves you approximately $55/month on a 36-month lease.

Game #2 — The Marked-Up Money Factor

Dealers receive a base “buy rate” from the manufacturer’s finance company — and are permitted to mark it up. A markup of just 0.001 MF adds roughly $864 over 36 months on a $40,000 car. Always ask: “What is the base buy rate money factor for this model this month?” If they won’t answer, use our calculator with the marked-up rate to see exactly how much extra you are paying.

Game #3 — The Buried Acquisition Fee

The acquisition fee ($595–$895) is legitimate but is sometimes rolled into the cap cost without disclosure. Always ask whether it is being capitalized or paid upfront. Capitalizing it adds to your monthly rent charge — meaning you pay interest on a fee.

Game #4 — The Mileage Trap

Standard lease offers are built on 10,000 miles/year. Dealers rarely proactively mention that the average American drives 15,000+ miles/year. Accepting a low-mileage lease and going over is one of the most common and expensive mistakes in leasing. Always calculate your realistic annual mileage before selecting a tier.

Game #5 — The Low Monthly Payment Illusion

A $249/month lease with $5,000 due at signing costs you $13,964 over 36 months. A $319/month lease with $1,000 due at signing costs $12,484. The second deal is cheaper — but the first looks better in the ad. Always calculate total out-of-pocket, not just the monthly payment. Our car lease calculator shows both numbers simultaneously.

Game #6 — The Extended Warranty Upsell

Most car leases run 36 months — which aligns exactly with the manufacturer’s bumper-to-bumper warranty. You are already covered. An extended warranty on a lease is almost always unnecessary. If you encounter financial pressure from add-on products, our Credit Card Payoff Calculator can help you assess the real cost of financing add-ons.

Game #7 — The Disposition Fee Ambush

The $300–$500 disposition fee is due at lease return — and many lessees are blindsided by it. Ask upfront if it is waived when you start a new lease with the same brand. Most manufacturers (Toyota, Honda, BMW) waive it for returning customers. Get this in writing before you sign.

What This Means For You: Run every dealer quote through the car lease calculator above before you respond to any payment offer. When you know the real number, dealer games stop working.

Car Lease Calculator — Expert Answers to the Most Asked Questions

1. What is a car lease calculator?

A car lease calculator is a financial tool that computes your exact monthly lease payment using the standard leasing formula: depreciation fee + rent charge + taxes. It uses inputs including MSRP, selling price, residual value, money factor, lease term, and fees.

2. How accurate is an online car lease calculator?

Our calculator uses the same formula lenders apply. Results are highly accurate for most U.S. leases. Minor variances may occur due to state-specific tax treatment or lender-specific fee structures. Always verify final numbers with your lease contract.

3. What is a good money factor for a car lease in 2026?

A money factor of 0.00200 or below (equivalent to 4.8% APR or lower) is considered competitive for well-qualified buyers in 2026. Anything above 0.00300 (7.2% APR) warrants negotiation or an alternative offer.

4. What is residual value in a car lease?

Residual value is the bank’s estimate of what the car will be worth at lease end, expressed as a percentage of MSRP. A higher residual value means lower monthly payments because you are financing less depreciation.

5. How do I lower my monthly car lease payment?

– Negotiate the capitalized cost (selling price) down aggressively

– Choose a car with a high residual value (50–60%+ of MSRP)

– Qualify for a lower money factor by improving your credit score — check where you stand with our Credit Score Calculator

– Apply all manufacturer rebates and incentives as cap cost reductions

6. Is leasing a car worth it in 2026?

For drivers who value lower monthly payments, new cars every 3 years, and no long-term ownership commitment — yes. The EV $7,500 credit pass-through makes EV leasing particularly compelling. For high-mileage drivers or those building long-term equity, purchasing typically wins.

7. What fees are paid upfront when leasing a car?

Typical upfront fees include the first month’s payment, acquisition fee, documentation fee, registration fees, and any voluntary down payment (cap cost reduction). Total due-at-signing typically ranges from $1,500 to $4,000+ depending on vehicle and negotiated terms.

8. Can I negotiate a car lease?

Yes — multiple elements are negotiable. The selling price (cap cost) is the most important. The money factor is sometimes negotiable. Fees like the doc fee can often be reduced. The residual value is set by the bank and cannot be negotiated.

9. What happens if I go over mileage on my car lease?

You owe a per-mile overage charge at turn-in, typically $0.15–$0.30 per mile depending on the manufacturer. The only way to avoid this retroactively is to purchase the car at lease end. Prevention: pre-purchase additional miles upfront — they cost significantly less than end-of-lease overage rates.

10. What is the difference between money factor and APR?

The money factor is the lease interest rate expressed as a decimal (e.g., 0.00225). APR is the same rate expressed as a percentage (5.4%). Multiply any money factor by 2,400 to get the APR equivalent. For broader APR comparisons across financial products, see our APR vs. Interest Rate guide.

Generally, no. A down payment on a lease reduces your monthly payment but disappears if the car is stolen or totaled. The FTC explicitly advises that consumers focus on total cost rather than minimizing the monthly payment through large upfront sums on leases. Put that money in a high-yield savings account instead.

Expert Summary

Laura M. Bennett, CFP® — Senior Financial Advisor, financeauthorityhub.com

“The single most effective thing a car shopper can do before visiting a dealership is calculate their own lease payment. When you know the real number — depreciation, rent charge, fees, and total out-of-pocket — every dealer tactic becomes transparent immediately. Our car lease calculator gives you that number in seconds. Use it every time, without exception.”

📋 Disclaimer: This article is for educational and informational purposes only. It does not constitute financial, legal, or tax advice. Lease payment calculations are estimates based on standard industry formulas and may vary depending on your lender, state tax laws, local fees, and individual credit profile. Always review your actual lease contract and consult a qualified financial advisor before signing any lease agreement. The federal EV tax credit details referenced are based on current IRS guidance and are subject to legislative change.

🔗 Related Tools & Guides from financeauthorityhub.com:

- Auto Loan Calculator — Compare leasing vs. financing side by side

- Debt-to-Income Ratio Calculator — Know your borrowing power before you negotiate

- Amortization Calculator — Model any financing schedule in detail

- Automobile Insurance Rates 2026 — Factor your full monthly car cost

- Comprehensive Car Insurance Guide — Required on all leased vehicles

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.