College Savings Calculator: See If You’re Behind

College Savings Calculator (529)

Plan how much to save each month for college, project year‑by‑year costs (inflation-adjusted), and see whether you’re on track to cover your goal percentage. 529 plans are “qualified tuition programs” designed to encourage saving for education, and qualified withdrawals are tied to qualified education expenses. [web:329][web:330][web:333]

Inputs

Uses monthly compounding for projections (planner-style).

Note: This is a planning calculator. Qualified 529 withdrawals depend on qualified education expenses and your situation. [web:333][web:330]

Results

Goal status

—

Goal coverage: —

Years to start: —

Balance at college start

—

Required at start (goal): —

Projected total costs

Gross: —

Scholarships: —

Net (goal): —

Result after college

—

Required monthly (goal): —

Detailed totals (current inputs)

Total contributions: — • Total withdrawals (simulated): — • Investment earnings (derived): —

Assumptions: return — • edu inflation — • contribution step-up —

Step-by-step math (planner view)

Projected costs by college year

| Year | Gross cost | Scholarship | Net (goal-adjusted) |

|---|

Balances during college (goal-adjusted withdrawals)

| Year | Begin balance | Withdrawal | End balance |

|---|

Sensitivity: Return vs education inflation

| Return | Edu inflation | End balance (current monthly) | Required monthly (goal) |

|---|

Results appear after you click “Calculate.”

In This Article

In 2025–26, a year of public in-state college costs $30,990 in total (tuition, fees, room, and board), according to the College Board’s Trends in College Pricing 2025 report. A private nonprofit university runs $65,470 per year.

By the time your newborn turns 18, that same education could cost $160,000–$240,000 total — assuming just 4% annual tuition inflation.

The hard question isn’t whether college costs are rising. It’s whether your college savings calculator results show you’re on track — or dangerously behind.

Use the calculator above to get your personalized number. Then read this guide to understand exactly what your results mean and what to do next.

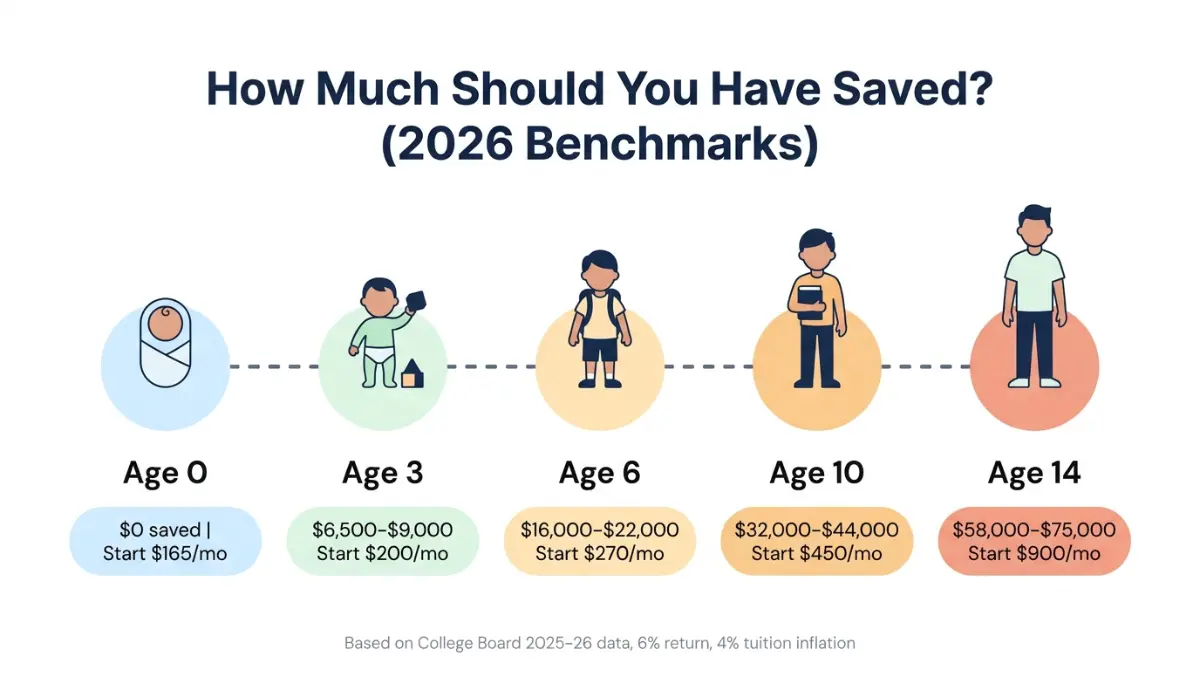

How Much Should You Have Saved in Your College Fund by Age?

Most parents don’t find out they’re behind until it’s too late to fix it cheaply. The earlier you start saving for college, the smaller your required monthly contribution — and the more compound growth does the heavy lifting.

Here’s the 2026 benchmark table every parent needs — and that no major competitor publishes:

College Savings Benchmarks by Child’s Age (2026)

| Child’s Age | Target Balance (Public In-State) | Target Balance (Private) | Required Monthly From Now |

|---|---|---|---|

| Newborn (0) | $0 | $0 | $165–$485/mo |

| Age 3 | $6,500–$9,000 | $16,000–$22,000 | $200–$580/mo |

| Age 6 | $16,000–$22,000 | $38,000–$50,000 | $270–$750/mo |

| Age 10 | $32,000–$44,000 | $76,000–$100,000 | $450–$1,200/mo |

| Age 14 | $58,000–$75,000 | $130,000–$165,000 | $900–$2,400/mo |

Based on 2025–26 College Board data, 4% annual tuition inflation, 6% annual return, targeting 100% coverage of net costs.

If your current balance is below these ranges, you are behind. That’s not a judgment — it’s a number. And numbers can be fixed.

What 2026 College Costs Actually Look Like

According to the College Board Trends in College Pricing 2025, the average full-year undergraduate budget for 2025–26 is:

- Public in-state (4-year): $30,990/year

- Public out-of-state (4-year): $50,920/year

- Private nonprofit (4-year): $65,470/year

Tuition inflation is running at 2.9%–4.0% per year — faster than general inflation. A child born today faces a projected 4-year total of $160,000–$270,000 at enrollment age, depending on school type.

The One-Third Rule for College Savings

Financial planners widely recommend saving one-third of projected college costs — funding the remainder through grants, scholarships, merit aid, and manageable student loans.

- Public university target (1/3 rule): Save $170–$270/month from birth

- Private university target (1/3 rule): Save $485–$700/month from birth

This is why starting a 529 plan or college fund early is not optional — it’s financial math.

How to Use This College Savings Calculator and Read Your Results

Our college savings calculator gives you more than a balance projection. It tells you whether you’re on track, by how much you’re short, and exactly what monthly contribution closes the gap.

Step-by-Step: What to Enter

- Child’s current age — the single biggest variable in your results

- College start age — typically 18; adjust for early or delayed enrollment

- Current savings — enter your actual 529 balance or college fund balance today

- Monthly contribution — your current or planned recurring deposit

- Annual step-up % — the percentage you plan to increase contributions yearly (even 3% annually makes a large difference)

- Expected annual return % — a 6% assumption is standard for a diversified 529 portfolio; conservative planners use 5%

- Education inflation % — use 4–5% to reflect historical tuition growth; this is the most underestimated input

- Scholarships and grants — include any expected financial aid to reduce your net savings target

How to Read Your Results

“On track (goal covered)” means your current savings path covers your target cost percentage by college start. Keep going.

“Shortfall (goal not covered)” means your projected balance at college start falls short. Your calculator shows two critical numbers:

- Required balance at college start — the lump sum needed to fund your goal

- Required monthly contribution — what you need to save each month from today to hit that balance

If the required monthly contribution feels high, don’t panic. Section 5 covers catch-up strategies that actually work.

The Input That Changes Everything

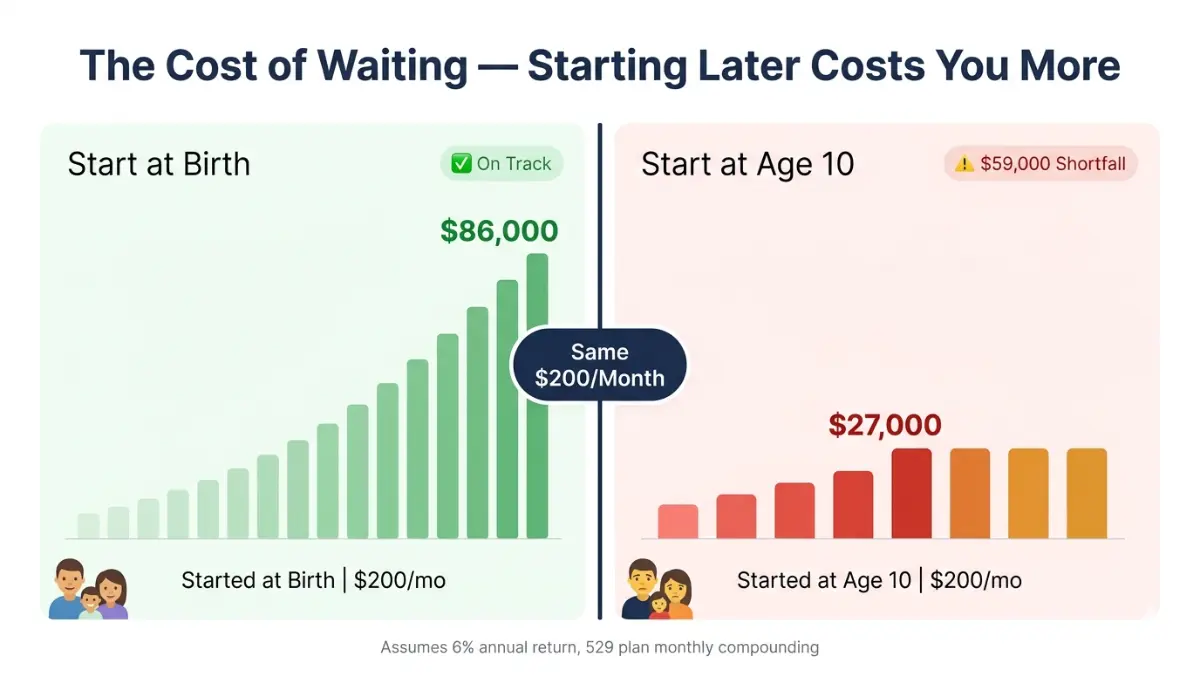

Starting age is the most powerful lever in any college savings calculator. Consider this real comparison:

| Started At | Monthly Contribution | Projected Balance at Age 18 |

|---|---|---|

| Age 0 (birth) | $200/mo | ~$86,000 |

| Age 3 | $200/mo | ~$67,000 |

| Age 6 | $200/mo | ~$49,000 |

| Age 10 | $200/mo | ~$27,000 |

Assumes 6% annual return, no existing savings, 529 plan compounding monthly.

Waiting just 6 years costs you over $37,000 — at the same monthly contribution.

If high-interest debt is eating your monthly cash flow before you can save for college, use our Debt Consolidation Calculator to model a payoff plan that frees up dollars faster.

529 Plans — 2026 Rules, Tax Advantages, and Major New Changes

A 529 plan is the most powerful education savings vehicle available to American families. It offers triple tax advantages that no standard brokerage account can match.

What Is a 529 Plan?

A 529 plan (officially a “qualified tuition program” under IRS Topic No. 313) is a state-sponsored, tax-advantaged savings account designed specifically for education expenses.

Core benefits:

- Tax-free growth — your investment earnings compound without federal tax

- Tax-free withdrawals — for qualified education expenses including tuition, room, board, and books

- State tax deductions — over 34 states offer a deduction or credit for contributions to their own state’s plan

- No income limits — anyone can open or contribute to a 529, regardless of earnings

- High contribution ceilings — most states allow $300,000–$550,000 lifetime per beneficiary

- Flexible use — any accredited college, university, vocational school, or eligible K-12 institution in the U.S.

🚨 Major 2026 Rule Changes You Must Know

The One Big Beautiful Bill Act, signed July 4, 2025, and SECURE 2.0 Act (effective 2024) brought the most significant 529 changes in years. Most competitor articles have not updated for these.

1. K-12 Annual Withdrawal Limit Doubled Starting January 1, 2026, you can withdraw up to $20,000/year (up from $10,000) from a 529 for K-12 tuition. This makes 529 plans significantly more useful for families with children in private elementary and secondary schools.

2. New Qualified Expense Categories (2026) Under the One Big Beautiful Bill Act, the following are now qualified 529 expenses:

- Curriculum materials (textbooks, workbooks, digital tools)

- Tutoring by a licensed educator

- AP exam fees and dual enrollment costs

- Educational therapies for students with disabilities

3. 529-to-Roth IRA Rollover (SECURE 2.0) This is the single most important update for families worried about oversaving. Under SECURE 2.0, you can now roll unused 529 funds into the beneficiary’s Roth IRA — tax-free and penalty-free — under these conditions:

- The 529 account must have been open for 15+ years

- Funds must have been in the account for at least 5 years

- Annual rollover limit: $7,500 in 2026 (subject to Roth IRA contribution limits)

- Lifetime cap: $35,000 per beneficiary

- The Roth IRA must be in the beneficiary’s name, not the account owner’s

To plan how that Roth IRA nest egg grows over time, use our Roth IRA Calculator.

4. 529-to-ABLE Account Rollovers Now Permanent Tax-free rollovers from 529 plans to ABLE accounts for beneficiaries with disabilities are now permanent law — no longer set to expire.

Expert Insight — Laura M. Bennett, CFP: “The 2026 K-12 expansion and the SECURE 2.0 Roth IRA rollover provision together eliminate the two biggest fears families had about 529 plans: inflexibility and oversaving. There has never been a better year to open or increase your 529 contributions.”

529 vs. Coverdell ESA vs. UTMA: Quick Comparison

| Feature | 529 Plan | Coverdell ESA | UTMA Account |

|---|---|---|---|

| Annual contribution limit | No federal cap | $2,000/year | Unlimited |

| Tax-free growth | ✅ Yes | ✅ Yes | ❌ No |

| Tax-free withdrawals | ✅ Education only | ✅ Broader K-12 | ❌ No |

| Income restrictions | ❌ None | ✅ Phase-out applies | ❌ None |

| K-12 withdrawal limit | ✅ $20,000/yr (2026) | ✅ Broad | ✅ Any purpose |

| Control after child turns 18 | ✅ Parent retains | ✅ Parent retains | ❌ Transfers to child |

| Roth IRA rollover option | ✅ Up to $35,000 | ❌ No | ❌ No |

For most American families, the 529 plan wins on every axis that matters — especially with the 2026 expansions now in place.

Which 529 Plan Should You Choose?

You are not required to use your home state’s 529 plan. You can invest in any state’s plan — and in many cases, an out-of-state plan offers better investment options or lower fees.

How to Choose the Right 529 Plan

Step 1: Check your state’s tax deduction first. If your state offers a deduction for contributions to your own state’s plan, compare the tax benefit against the investment options and fees. For high earners in states with income taxes, the deduction can be worth $500–$2,000+ annually.

Step 2: Compare investment options and fees. Look for plans with low expense ratios (under 0.20%) and age-based portfolios that automatically shift from aggressive equity to conservative fixed-income as your child approaches college age.

Step 3: Don’t overpay in fees. A 1% higher expense ratio over 18 years can cost you $15,000–$25,000 in lost returns on a $300/month contribution.

For families in states without a state income tax deduction (notably California and others), an out-of-state plan is often the smarter move. The College Savings Plans Network maintains a state-by-state directory of all 529 plan options.

Use our Investment Calculator to compare the long-term impact of different expense ratios on your 529 portfolio.

Starting Late? Catch-Up Strategies That Actually Work in 2026

If your child is 10 and you have less than $15,000 saved, you are not alone — and you still have options. Here is what actually works.

5 Proven Catch-Up Moves

1. Annual Contribution Step-Up Increase your monthly 529 contribution by 3–5% every year as your income grows. Even starting at $200/month and increasing 5% annually turns into significantly more than a flat $200/month over 8 years.

2. One-Time Lump Sum Injections Direct tax refunds, bonuses, or inheritance dollars straight into your 529. Grandparents can contribute a lump sum of up to $95,000 per beneficiary in 2026 ($190,000 for couples) using the 5-year gift tax election — front-loading 5 years of the $19,000 annual exclusion without triggering gift tax.

3. Redirect Freed Debt Payments Every dollar you eliminate from high-interest debt becomes a dollar available for college savings. Use our Debt-to-Income Ratio Calculator to identify how much cash flow you can redirect once debt is cleared.

4. Lower Your Coverage Goal Strategically You do not need to save 100% of projected college costs. Aim to cover 50–70% through savings, then supplement with:

- FAFSA-based federal grants and subsidized loans

- Merit scholarships (no need-based requirement)

- Work-study programs

- Modest student borrowing (target under $27,000 total)

For a full FAFSA and financial aid strategy, read our guide on FAFSA 2026 new SAI rules and Financial Aid 2026.

5. Use Age-Based Portfolio Allocations If you have 10+ years until college, an aggressive equity-heavy portfolio in your 529 provides maximum growth runway. Shift to conservative allocations (bonds, stable value) in the final 3–5 years.

The Real Cost of Waiting: A Side-by-Side Look

| Started Saving At | Monthly Savings | Total Contributions | Projected Balance at 18 |

|---|---|---|---|

| Age 0 | $300/mo | $64,800 | ~$110,000 |

| Age 5 | $300/mo | $46,800 | ~$69,000 |

| Age 10 | $300/mo | $28,800 | ~$37,000 |

| Age 14 | $300/mo | $14,400 | ~$17,500 |

Assumes 6% annual return, 529 plan monthly compounding. No existing savings.

Waiting from birth to age 10 costs you $73,000 in projected balance — despite saving the same $300/month.

The only way to make up for lost time is higher monthly contributions. Use the calculator above to find your exact catch-up number.

What Happens If My Child Doesn’t Go to College?

This is the most common fear parents have about 529 plans — and it’s largely solved by 2026 rule changes.

Your options if the 529 goes unused:

- Change the beneficiary to a sibling, cousin, or even yourself for graduate school

- Roll up to $35,000 into the beneficiary’s Roth IRA over multiple years (2026 annual limit: $7,500)

- Use for K-12 education — up to $20,000/year under 2026 rules

- Use for vocational or trade school — any accredited program qualifies

- Withdraw the funds — only the earnings portion is taxed plus a 10% penalty (penalty is waived if your child receives a full scholarship)

The 10% penalty only applies to earnings, not contributions. If you contributed $30,000 and earned $8,000, only the $8,000 earnings face the penalty — and the principal comes back to you penalty-free. Given the 2026 Roth IRA rollover option, the risk of “wasting” 529 savings is lower than ever.

Frequently Asked Questions About College Savings

Q1: How much should I save per month for my child’s college?

Financial planners recommend $170–$485/month from birth, depending on whether you’re targeting a public or private university under the one-third coverage rule. Use the college savings calculator above to get your personalized monthly target based on your child’s current age and existing savings.

Q2: What is a 529 plan and how does it work?

A 529 plan is a tax-advantaged education savings account authorized under Section 529 of the IRS tax code. Contributions grow tax-free, and withdrawals for qualified education expenses — tuition, fees, room, board, books, and more — are completely tax-free at the federal level.

Q3: How much does college cost in 2025–26?

According to the College Board Trends in College Pricing 2025, the average full-year budget (tuition + fees + housing + food) is:

Public in-state: $30,990/year

Public out-of-state: $50,920/year

Private nonprofit: $65,470/year

Q4: Is $10,000 a good start for a college fund?

Yes — especially if your child is young. At a 6% annual return with $10,000 today and $200/month added, you’d have approximately $107,000 by age 18 (starting from birth). Without additional contributions, $10,000 alone would grow to roughly $28,500. Every additional monthly contribution multiplies that outcome.

Q5: What happens to a 529 plan if my child doesn’t go to college?

Under 2026 rules, you can: change the beneficiary to another family member; roll up to $35,000 into the beneficiary’s Roth IRA under SECURE 2.0 rules; use funds for K-12 expenses up to $20,000/year; or withdraw the money (earnings taxed + 10% penalty, though the penalty is waived for scholarship amounts).

Q6: Can grandparents contribute to a 529 plan?

Yes. In 2026, grandparents can contribute up to $19,000 per year per beneficiary without triggering federal gift tax. They can also superfund a 529 with up to $95,000 (or $190,000 for couples) using the 5-year gift tax election. Starting with the 2024–25 FAFSA cycle, grandparent-owned 529 distributions no longer hurt financial aid eligibility.

Q7: Are 529 contributions tax deductible?

529 contributions are not federally tax deductible. However, over 34 states offer a state income tax deduction or credit for contributions to their own state’s 529 plan. To maximize your benefit, check your state’s rules before selecting a plan.

Q8: How much can I contribute to a 529 plan in 2026?

There is no annual federal contribution limit. Most states cap lifetime contributions at $300,000–$550,000 per beneficiary. However, contributions exceeding $19,000 per year per individual donor (or $38,000 for married couples) may require filing a federal gift tax return.

Q9: Can I use a 529 for K-12 tuition?

Yes. Starting January 1, 2026, the annual K-12 withdrawal limit increased to $20,000 per student (up from $10,000), thanks to the One Big Beautiful Bill Act signed on July 4, 2025. This now covers tuition at private elementary, middle, and high schools.

Q10: What is the average 529 plan balance in the U.S.?

The national average 529 account balance was approximately $30,295 as of mid-2024, according to the College Savings Plans Network. However, financial experts recommend a balance of $37,000–$245,000 by the time your child starts college, depending on school type and your coverage target.

Q11: How does education inflation affect my savings goal?

Education inflation runs at approximately 3–5% annually — roughly double the general consumer price index. If you calculate your savings goal using today’s college prices without inflation adjustment, you will significantly underfund your college savings account. Always use an education inflation rate of at least 4% in any college fund calculator.

Related Planning Tools: Use our Compound Interest Calculator to see exactly how your 529 grows year by year. If you’re also planning for retirement simultaneously, our Retirement Calculator and 401(k) Calculator help you balance both goals without sacrificing either.

📌 Disclaimer: This article is for educational and informational purposes only and does not constitute financial, tax, investment, or legal advice. 529 plan rules vary by state and are subject to change. College cost projections are estimates based on historical data and assumed inflation rates — actual future costs may differ. Consult a licensed financial advisor, CPA, or tax professional before making education savings decisions specific to your situation.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.