How Factoring Companies Build Your Structured Settlement Offer

Structured settlement factoring requires court approval and a ‘best interest’ finding — see the four inputs that shape your lump-sum offer.

In This Article

Why your structured settlement offer looks lower than you expected

If a buyer quotes you far less than your payments add up to, that gap is not an error — it is the business model.

Structured settlement factoring is the sale of your future settlement payments to a company in exchange for a single lump sum now. The price they offer is assembled from a few inputs you can learn to read for yourself.

Most readers land here holding a quote that feels low. That instinct is worth investigating before anyone signs anything.

What this guide will show you

You will see the four inputs behind every offer, the single figure that drives your true cost, and the court approval that must clear before money changes hands. It also shows where the buyer’s profit hides — and what these buyers actually pay for future payments is rarely what those payments are worth.

Who should read this before signing

Anyone weighing an offer, comparing several buyers, or feeling pressured to decide fast. This is education, not a recommendation to sell — the goal is for you to judge the number with clear eyes.

ℹ️ Disclaimer: This article explains structured settlement factoring — the sale of future settlement payments for a lump sum — for educational purposes only. Discount rates, fees, the IRS valuation rate, and state transfer laws vary by case and change throughout 2026. Before agreeing to sell any payments, consult a licensed financial professional and a qualified attorney who have no financial stake in whether you sell.

What a structured settlement factoring transaction actually is

A structured settlement factoring transaction is the court-approved sale of your right to receive future settlement payments in exchange for a lump sum today.

That distinction matters more than any other on this page. A loan is repaid with interest and you keep your payments; a sale means the payments now belong to the buyer, permanently.

Selling future payments versus borrowing against them

Your original settlement is typically funded by an insurance annuity that pays you on a fixed schedule. When you factor it, you transfer some or all of those payment rights to a third party.

You receive cash once. The buyer collects every payment you sold, for as long as that schedule runs — which is how they recover their money and earn a profit.

Full sale versus partial sale

You do not have to sell everything. A partial sale lets you transfer, say, 48 of 120 monthly payments while keeping the rest, leaving you some future income.

Selling the entire stream maximizes today’s cash but ends the protection a settlement was designed to provide. For many payees a partial sale is the more defensible choice — though the right answer depends entirely on the numbers in front of you.

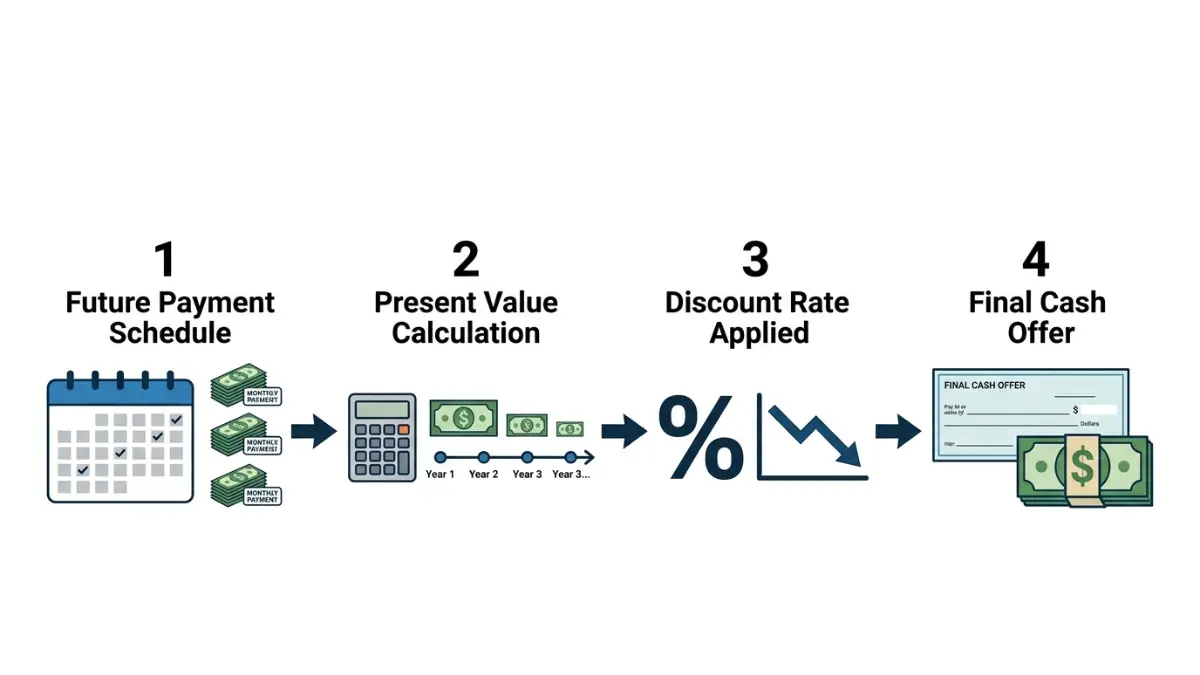

How factoring companies build your offer, step by step

A factoring offer is built from four inputs, applied in this order:

- The payment schedule you want to sell — the dollar amount, frequency, and number of future payments.

- The present value of those payments — what that future money is worth in today’s dollars.

- The discount rate the buyer applies — its profit margin and risk pricing, layered on top of present value.

- The fees and costs — court filing, legal, and processing charges deducted from your total.

The first two are arithmetic. The last two are where the buyer’s money is made.

The four inputs behind every offer

Present value comes first, because a dollar arriving in 2036 is worth less than a dollar today. Buyers begin by calculating what future payments are worth today, then apply their own discount rate well beyond that baseline.

| Offer input | What it represents | Effect on your cash |

|---|---|---|

| Total future payments | The face value you are selling | Starting point only |

| Present value | Future payments in today’s dollars | Lowers the figure |

| Buyer’s discount rate | Profit and risk margin | Lowers it further |

| Fees and costs | Court, legal, processing | Reduces your net |

A worked example using one payment stream

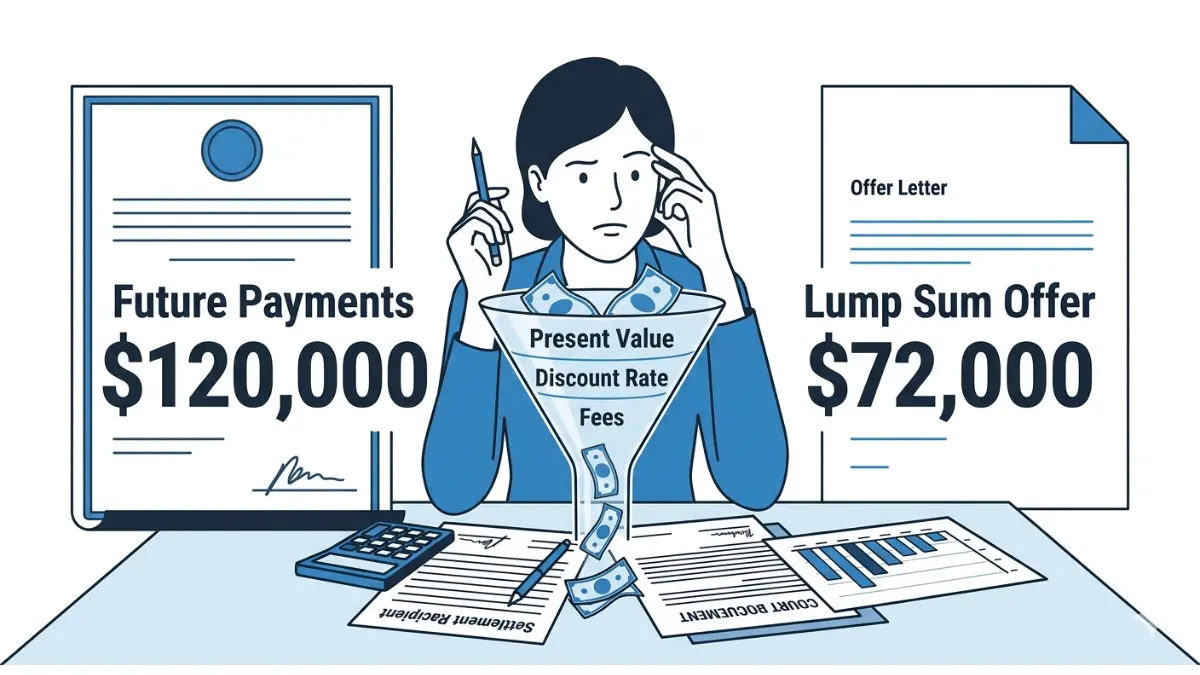

Say you sold $1,000 a month for 120 months — $120,000 in total future payments. Discounted to present value, that stream might be worth roughly $80,000 to $95,000, depending on the rate used.

The buyer then applies its discount rate and subtracts fees, and the cash you actually receive can fall well below even that present value. The headline “$120,000 in payments” is never the number that matters.

The discount rate is the real price you pay

The discount rate — not the fees — is where most of your money goes.

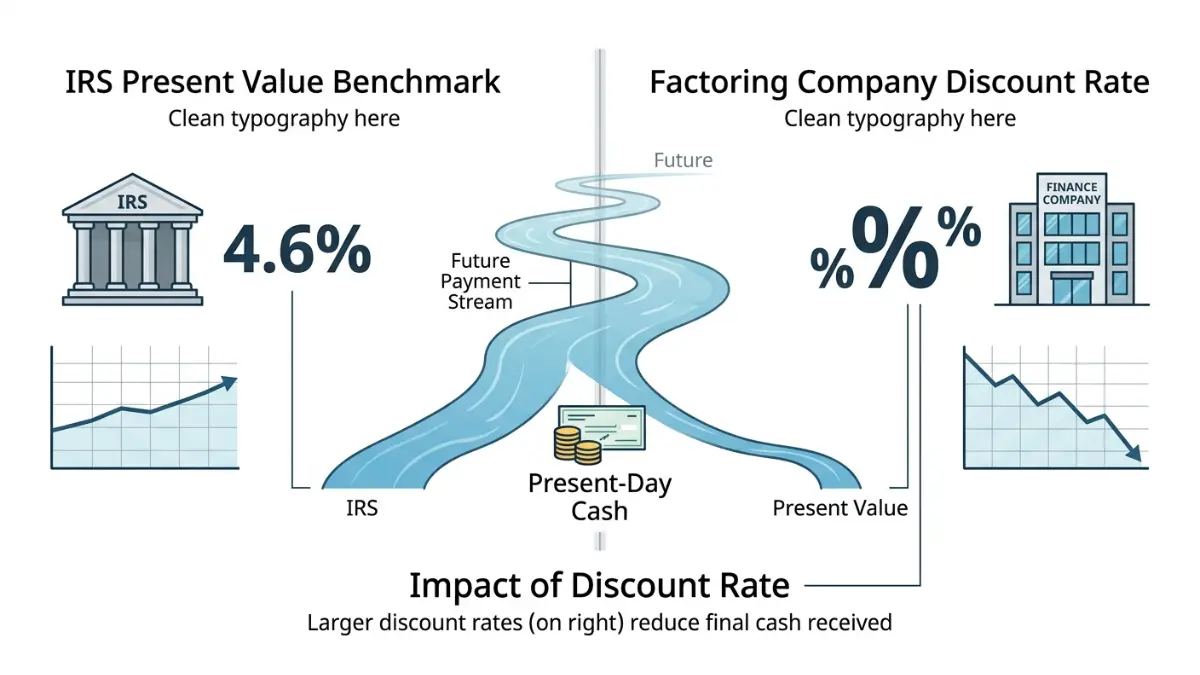

Two different rates get confused here, and buyers rarely correct the confusion. One is a federal benchmark for valuing future payments; the other is what the buyer charges you.

The federal benchmark versus the buyer’s applied rate

The IRS publishes a rate used to value future payment streams. It is the neutral starting point for “what is this future money worth today.”

📊 Data Point: The IRS Section 7520 rate for January 2026 is 4.6%. — Source: Internal Revenue Service, January 2026.

Buyers reference a present-value figure near that benchmark, then apply a discount rate set well above it. You can see the official benchmark at the federal rate used to value future payment streams and check the wider rate climate through the broader interest-rate environment buyers price against.

How to estimate your real cost

Effective annual discount rates on factoring deals frequently reach the low double digits — far above prevailing savings or lending rates. Always compute the rate implied by your own offer rather than trusting the lump-sum dollar figure.

One quick sanity check is to model how a sum grows over time and weigh it against the cash you are offered now. It also helps to see how inflation erodes a fixed payment stream you would be giving up.

⚠️ Warning: A larger lump-sum dollar figure can still carry a worse effective discount rate than a smaller offer. Compare the rate, not the headline cash amount.

How to compare offers and negotiate a better one

Offers are negotiable, and the only way to know if one is fair is to put it beside another.

Request written quotes from at least three buyers before responding to any of them. A single offer gives you no reference point — competition is your leverage.

What to ask every buyer for in writing

Demand an itemized breakdown: total payments sold, the present value used, the effective discount rate, and every fee. If a buyer will not put the effective rate in writing, treat that silence as an answer.

Understanding the true cost of selling your payments and the steps to take after a buyer makes an offer puts you on equal footing at the table.

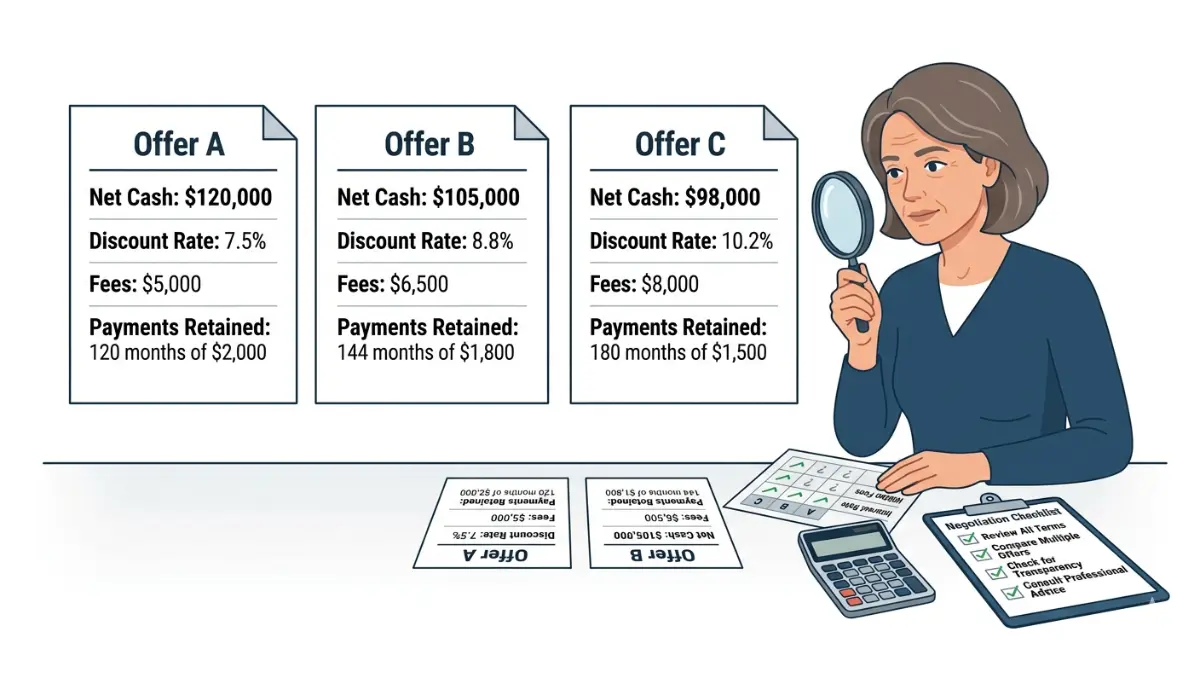

How to compare two offers apples-to-apples

Line the quotes up on the figures that decide value, not the marketing.

| Compare this | Why it matters | Best for spotting |

|---|---|---|

| Net cash to you | The only money you receive | Lowball offers |

| Effective discount rate | Your true annual cost | Hidden expense |

| Total fees | Reduces your net further | Padded charges |

| Payments retained | Income you keep | Over-selling |

Seeing how the major buyers compare and weighing a lump sum against keeping the payments often reveals room to push for better terms.

✅ Pro Tip: Within 48 hours, ask each buyer to email the effective annual discount rate on your specific offer. The number a buyer resists sharing is usually the one that matters most.

Court approval, your legal protections, and red flags

Yes — federal law requires a judge to approve your sale before it becomes final.

This is your strongest protection, and no legitimate buyer can skip it.

Why a judge must approve your sale

A buyer that acquires settlement payments without a court-approved “qualified order” faces a steep federal excise tax — which is why every real transfer goes through a courtroom.

📊 Data Point: Under IRC Section 5891, a buyer acquiring structured settlement payment rights without a qualified court order owes a 40% excise tax on the factoring discount. — Source: Internal Revenue Service, 2026.

A judge must also find the sale is in your best interest before granting the court approval your sale must clear. It is worth reviewing what federal regulators tell consumers to weigh first before your hearing.

Red flags and where to get independent advice

Watch for buyers who rush you, steer you toward “their” advisor, or dodge the effective-rate question. Regulators have penalized exactly these tactics — see a case where regulators penalized a buyer for steering consumers and the broader warning signs of a predatory buyer.

💡 Expert Note (CFA): In my work with payees, the costliest mistake I see is treating the court hearing as a formality. Bring an independent advisor’s written present-value estimate to that hearing — judges weigh it, and buyers know it.

Structured settlement factoring: frequently asked questions

1. How do factoring companies calculate my offer?

A structured settlement factoring offer starts with your payment schedule’s present value. The buyer then applies a discount rate for profit and risk and subtracts court, legal, and processing fees. The cash you receive is what remains after all four adjustments — never your payments’ face value.

2. What discount rate is typical when selling a structured settlement?

Effective rates in structured settlement factoring frequently reach the low double digits, well above ordinary savings or loan rates. There is no single fixed rate, so always request the effective annual rate on your specific offer in writing and compute it yourself before comparing any deals.

3. Can I sell only part of my structured settlement payments?

Yes. A partial structured settlement factoring sale lets you transfer a set number of payments — for example, 48 of 120 months — while keeping the rest. This preserves some future income and often produces a more balanced outcome than selling your entire payment stream at once.

4. Do I have to go to court to sell my structured settlement?

Yes. Every structured settlement factoring transfer requires a judge’s approval through a qualified court order. The judge must find the sale is in your best interest, and federal law penalizes buyers who try to bypass this step, so no legitimate company will ever skip the hearing.

5. How long does a structured settlement sale take?

A typical structured settlement factoring transfer takes roughly 45 to 90 days, driven mainly by your state’s court scheduling and required notice periods. Buyers advertising near-instant cash usually offer a small advance against a deal that still must clear court approval before it fully funds.

6. Will I pay taxes when I sell my structured settlement payments?

Generally, the lump sum from a structured settlement factoring sale of tax-free personal-injury payments is also received tax-free, and the 40% federal excise tax falls on the buyer, not you, when a qualified court order is obtained. Tax treatment can still vary by individual case.

7. What is the IRS Section 7520 rate and why does it matter?

The IRS Section 7520 rate — 4.6% for January 2026 — is the federal benchmark for valuing future payment streams. In structured settlement factoring it sets a neutral present-value baseline; the buyer’s applied discount rate sits well above it, and that gap is largely where their profit comes from.

8. Can I negotiate a structured settlement factoring offer?

Yes. Structured settlement factoring offers are negotiable, especially when you hold written quotes from multiple buyers. Competition is your leverage: ask each company to improve its effective discount rate or cut its fees, and be ready to walk away from any buyer that refuses to itemize.

9. What is a “best interest” hearing?

It is the court step in a structured settlement factoring transfer where a judge decides whether selling your payments genuinely serves your interest. The judge reviews your finances, the offer terms, and your stated reasons, and can reject deals that look exploitative or unnecessary for the payee.

10. How do I compare offers from multiple factoring companies?

Compare structured settlement factoring offers on four figures: net cash to you, the effective annual discount rate, total fees, and how many payments you keep. Ignore the headline payment total — a larger advertised figure can still carry a worse effective rate than a smaller, cleaner offer.

11. What are the biggest risks of selling my structured settlement?

The main risks of structured settlement factoring are accepting a high effective discount rate, losing future income you may later need, and pressure tactics from aggressive buyers. Selling the entire stream can leave you without the long-term security the settlement was originally designed to provide.

Before you sign: your next three steps

You now understand your offer better than most buyers expect you to.

Turn that into action. First, request itemized written quotes from at least three companies so you have something real to compare.

Second, calculate the effective discount rate on each offer and judge the deal on that number, not the headline cash. Third, take the strongest offer to an independent, fee-only advisor and an attorney before your court hearing.

A structured settlement was built to protect your future income. Selling it can be the right move in a genuine emergency — but only at a fair rate, with eyes open, and after the math has been checked by someone with no stake in your decision.

The buyer has done this thousands of times. Now you can walk in prepared.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.