What a Structured Settlement Cash Advance Really Costs You

A structured settlement cash advance is legal only with a judge’s approval — and a 2026 personal loan near 12% APR often costs far less.

In This Article

A structured settlement cash advance converts future settlement payments into money you can spend today. It is legal, it moves slower than the ads suggest, and it usually costs far more than borrowers expect.

If a flyer promised fast cash for your monthly payments, you deserve a straight answer about what you would actually receive — and what you would surrender.

I have spent 28 years valuing future income streams for clients. The most expensive mistake I see is judging these deals by the cash in hand instead of the total dollars given up.

This guide covers how the advance works, what it costs against 2026 borrowing rates, the court approval that protects you, and the cheaper options worth pricing first. It helps to first understand how structured settlements are built to pay out over time before deciding to unwind one.

ℹ️ Disclaimer: This article explains the lending and payment-transfer activity involved in selling structured settlement payments for cash. Discount rates, offers, and court-approval requirements vary by state, by buyer, and by your individual settlement as of 2026. Before signing any transfer agreement or cash advance, consult a licensed attorney and a tax professional — and obtain independent advice that is not paid for by the company buying your payments.

What a structured settlement cash advance actually is

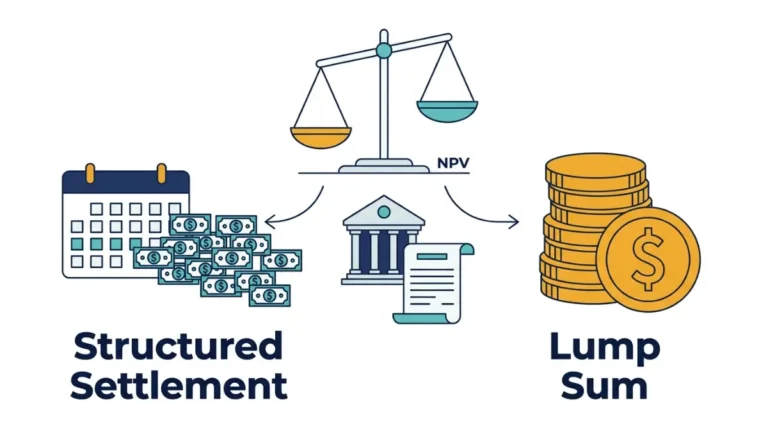

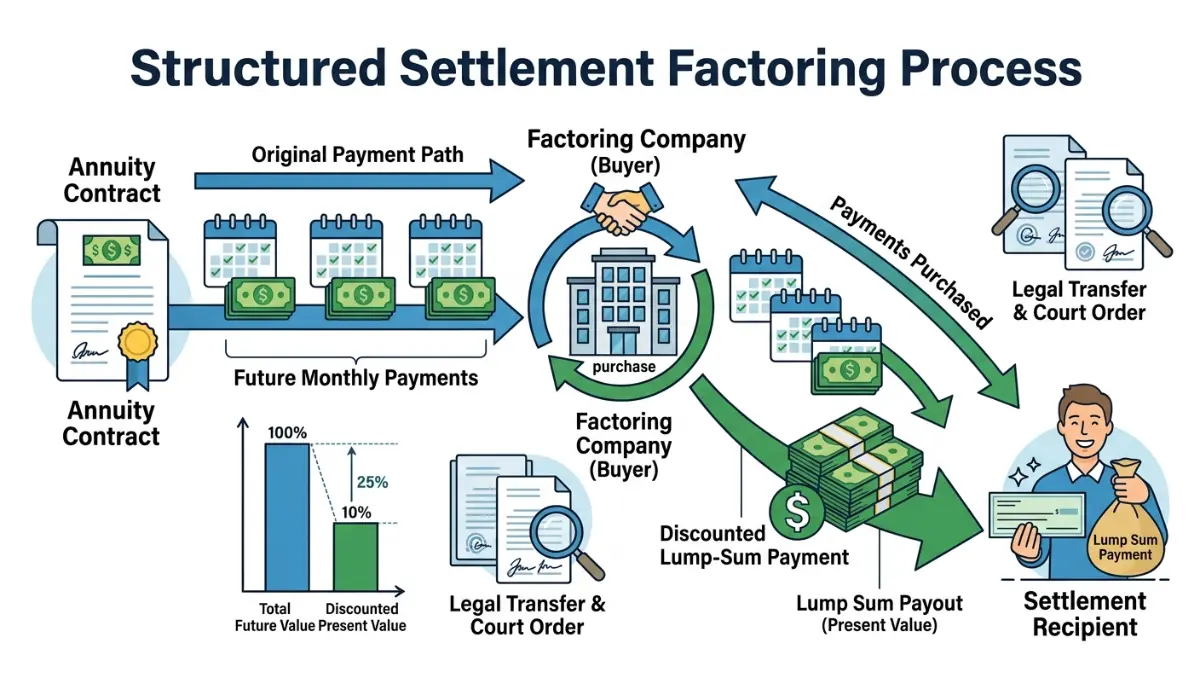

A structured settlement cash advance is the sale of some or all of your future structured settlement payments to a factoring company in exchange for a discounted lump sum now. Despite the name, it is not a loan — you permanently sell payment rights, and a judge must approve the transfer.

How getting cash from a structured settlement works

Your settlement pays you on a schedule, usually funded by an annuity, and a buyer offers cash today in return for the payments you sell.

This buyer-and-seller market is called the secondary market, and companies that purchase your stream often resell it to investors at a profit.

The amount they offer is always less than the face value of the payments. That gap is where their return — and your loss — lives.

Cash advance vs. selling your payments outright

The terms “cash advance,” “buyout,” and “structured settlement loan” usually describe the same thing: a sale. Understanding the mechanics of selling those payments prevents costly confusion at the contract stage.

Some firms also offer a small interim “advance” before a judge approves the full sale. That advance is repaid out of the court-approved transfer, so it is part of the same transaction, not separate financing.

💡 Expert Note (CFA): In my client work, the word “advance” does the heavy lifting — it implies you keep the asset, when you are actually signing away future income for good. That framing costs people thousands.

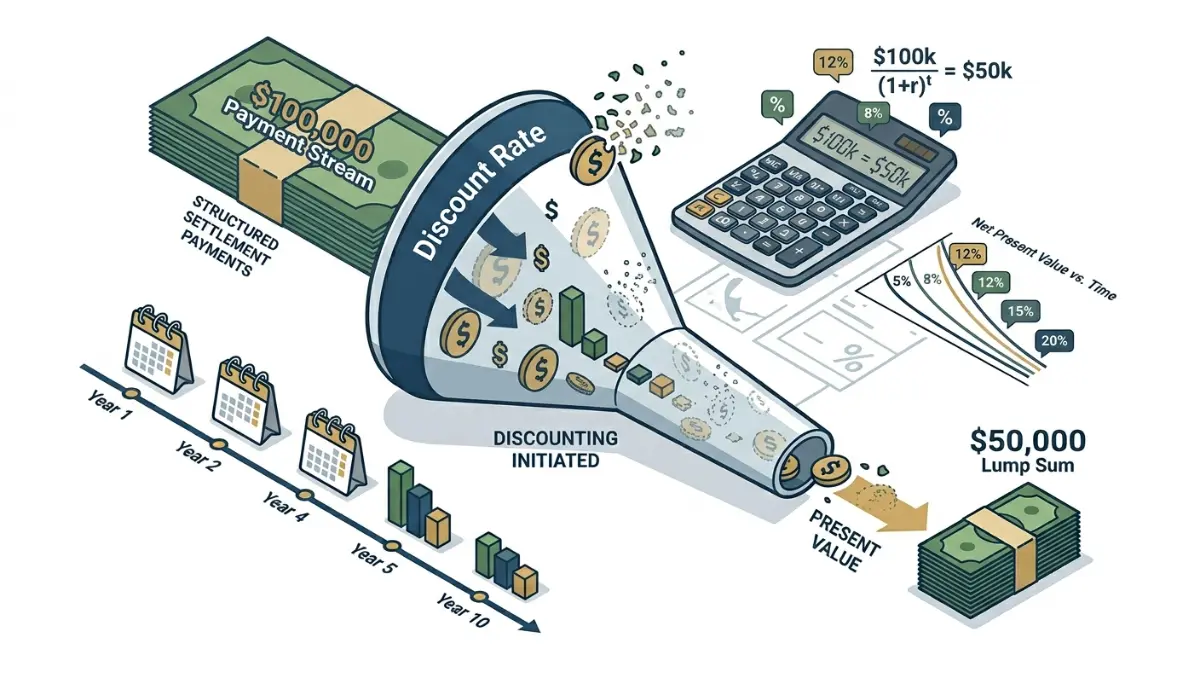

How much you really lose with a cash advance

You receive the present value of your future payments, not their full face value, so the lump sum is always smaller than the total you give up. On a $100,000 stream paid over 10 years, a real offer often lands tens of thousands below that face amount.

The discount rate and what it does to your money

The buyer applies a discount rate that converts your future payments into a smaller sum today. The higher the rate, the less cash you get — and these rates often run well above ordinary borrowing costs.

Seeing what your future payments are actually worth today and how the discount rate is set is the difference between accepting a fair offer and a predatory one.

⚠️ Warning: Judge an offer by the total dollars you surrender, not the lump sum in hand. Two offers with the same cash payout can differ by tens of thousands once the full stream you give up is counted.

What a cash advance costs vs. a regular loan in 2026

The illustrative table below shows why selling is the expensive path for most people.

| Option | You receive now | Total you give up or repay | Reversible? | Best for |

|---|---|---|---|---|

| Cash advance / sale ($100,000 stream, illustrative) | ~$45,000–$58,000 | $100,000 in future payments | No | True last resort |

| Personal loan ($15,000 at ~12% APR, 3 years) | $15,000 | ~$17,900 total | Yes — pay off early | Short-term need, fair credit |

| Partial sale of payments | A smaller lump sum | Only the payments you sell | No, for the sold portion | Keeping some income intact |

Source: borrowing rate from Federal Reserve G.19 Consumer Credit, Q1 2026. Settlement figures are illustrative, not a market quote.

📊 Data Point: As of Q1 2026, the average APR on a 24-month personal loan was roughly 12% and credit-card APR for accounts assessed interest was near 21% — Source: Federal Reserve, Q1 2026. Verify current figures at the Federal Reserve’s G.19 consumer credit release.

A fixed loan costs interest but leaves your settlement intact. To test that gap, model what a fixed loan would actually cost before comparing it to a buyer’s quote.

Is a structured settlement cash advance legal?

Yes — selling structured settlement payments is legal in nearly every state, but only with court approval. Without a qualified court order, IRC Section 5891 imposes a steep 40% excise tax on the buyer’s discount, which is why no legitimate transfer skips the courtroom.

The 40% tax rule and why court approval matters

The 40% excise tax falls on the buyer, not you, and disappears only when a judge approves the deal — which is exactly how the law forces every sale into a courtroom where someone checks that it serves you.

📊 Data Point: A transfer without a qualified court order triggers a 40% federal excise tax on the factoring discount under IRC Section 5891 — Source: IRS. The tax is reported on the IRS form for structured settlement factoring transactions.

The judge must find the transfer is in the best interest of you and your dependents. That standard, set by state Structured Settlement Protection Acts, is the legal backbone of the court approval step every transfer must clear.

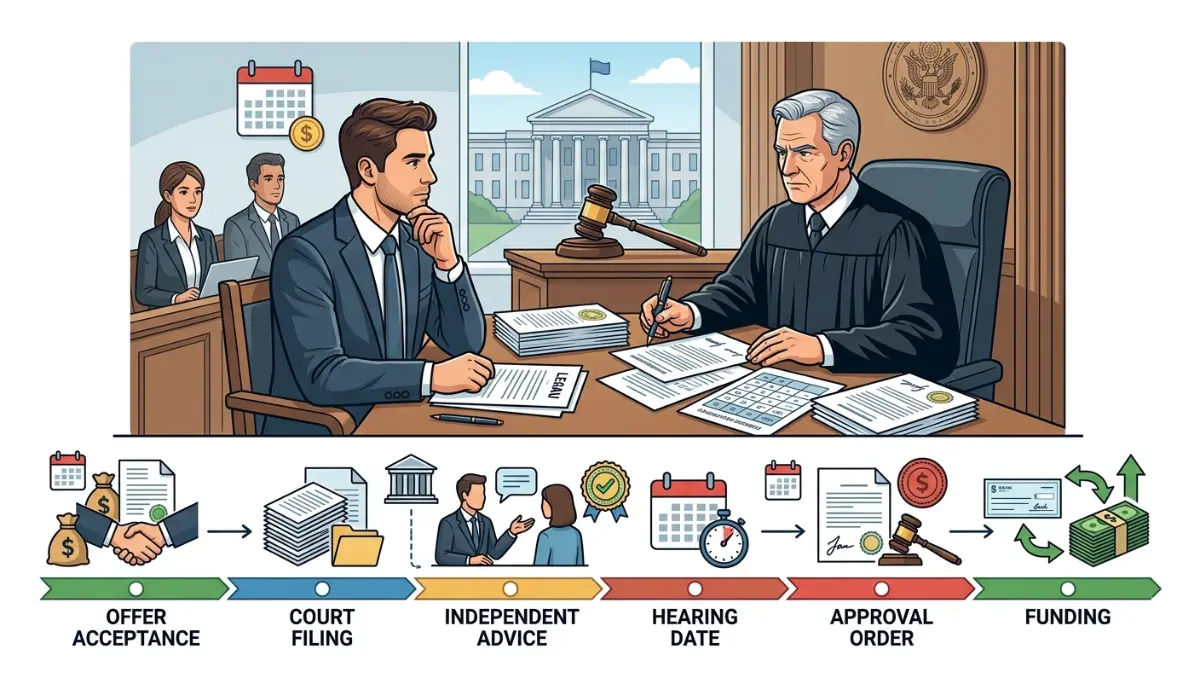

The court-approval process step by step

The process is slower than the marketing implies. Here is the typical sequence.

- You accept a buyer’s written offer that states the lump sum and the discount rate applied.

- The buyer files a transfer petition in your state court and arranges your independent professional advice.

- A hearing is scheduled, usually several weeks out, where a judge reviews your finances and dependents.

- If the judge issues a qualified order, funding usually arrives within 45 to 60 days of approval.

Because the original payments from a physical-injury settlement are generally tax-free, people assume the lump sum is too. The treatment can differ, so review how settlement money is taxed before signing.

The risks and red flags you can’t ignore

Court approval lowers the risk, but it does not erase it — and federal regulators have penalized companies that gamed the process.

Predatory tactics and what regulators have found

The Consumer Financial Protection Bureau warns that sellers can receive far less than their settlement is worth, and that some companies target people with disabilities. Read the CFPB’s guidance on giving up settlement payments for a lump sum before responding to any solicitation.

Regulators have acted on real abuses. In one matter, the CFPB pursued a firm for steering sellers toward “independent” advice from an attorney the company itself paid — see the CFPB’s enforcement record against that buyer.

⚠️ Warning: If the buyer chooses or pays for your “independent” advisor, walk away. Genuinely independent counsel works for you alone, and a paid referral is a documented warning sign of a predatory settlement offer.

How a cash advance can wreck your SSI or Medicaid

A lump sum can disqualify you from means-tested benefits. Programs like SSI and Medicaid use strict income and asset limits, and a sudden payout can push you over them even when your monthly payments did not.

Confirm how a payout interacts with a structured settlement and Medicaid eligibility before you trade steady income for a one-time check.

Smarter alternatives before you sign anything

Selling is rarely the cheapest way to raise money, so price the alternatives first.

When (if ever) a cash advance makes sense

A full sale can be defensible when you have no access to credit, face a genuine emergency, and a judge agrees it serves your interest. Even then, selling only the payments you need usually beats selling the whole stream.

💡 Expert Note (CFA): When clients come to me set on selling, I push for the smallest partial sale that solves the actual problem. Surrendering a $100,000 stream to cover a $12,000 bill is the kind of permanent loss that takes years to recover from.

Cheaper, safer ways to get money now

Several options preserve your future income.

- A fixed personal loan near 12% APR in 2026 costs interest but keeps your settlement intact, unlike a permanent sale.

- A nonprofit credit counselor can review your full picture at little or no cost before you commit to anything irreversible.

- Consolidating high-rate balances may free up monthly cash; compare consolidating what you owe against the cost of selling.

- A written plan often shows you need less than feared; build a budget around the amount you actually need first.

✅ Pro Tip: Within 48 hours, get one personal-loan quote and one nonprofit credit-counseling appointment. Having both in hand before you talk to any buyer changes the entire negotiation.

Weighing steady payments against a lump sum is the decision that should come before you ever request an offer.

Structured settlement cash advance: frequently asked questions

1. What is a structured settlement cash advance?

A structured settlement cash advance is the sale of your future settlement payments to a factoring company for a discounted lump sum today. It is not a loan — you permanently transfer payment rights, you receive less than face value, and a court must approve the transfer before any money changes hands.

2. Is selling structured settlement payments legal?

Yes, selling structured settlement payments is legal in nearly every state, but only with court approval. A judge must rule the transfer serves your best interest, and skipping that step triggers a 40% federal excise tax on the buyer under IRC Section 5891, so legitimate sales always go through court.

3. How much money will I lose if I sell my payments?

When you sell structured settlement payments, you receive their present value, not face value, so losses are steep. A $100,000 stream might yield only $45,000 to $58,000 depending on the discount rate applied. The longer the payout period, the larger the gap between what you get and what you surrender.

4. Do I need a judge to approve a structured settlement cash advance?

Yes, a judge must approve every structured settlement cash advance through a qualified court order. The court reviews your finances, your dependents, and the deal’s terms to confirm it serves your best interest. Without that order, the buyer faces a 40% excise tax, so no legitimate transfer avoids the hearing.

5. How long does the court approval process take?

A structured settlement cash advance is not fast. After you accept an offer, the buyer files a court petition, arranges your independent advice, and waits for a hearing date that is often weeks away. Once a judge issues a qualified order, funding typically arrives within 45 to 60 days.

6. What is the difference between a cash advance and selling my payments outright?

For most companies, a structured settlement cash advance and selling your payments outright are the same court-approved sale. Some firms add a small interim “advance” before approval, but that money is repaid from the final transfer, so it is part of one transaction rather than separate, reversible financing.

7. Will selling my settlement affect my SSI or Medicaid?

A structured settlement cash advance can disqualify you from SSI and Medicaid. These programs use strict income and asset limits, and a large lump sum can push you over them, while your original monthly payments may not have counted the same way. Confirm the impact with a benefits specialist first.

8. Can I sell only part of my structured settlement?

Yes, a partial structured settlement cash advance lets you sell only some payments while keeping the rest. This usually beats a full sale because you raise the cash you need without surrendering all your future income. The same court-approval and best-interest rules apply to the portion you transfer.

9. Are structured settlement buyers a scam?

Most structured settlement cash advance buyers operate legally under court supervision, but predatory conduct exists. Federal regulators have penalized firms for steering sellers to advisors the company secretly paid. Treat unsolicited offers, rushed signings, and company-chosen “independent” advice as warning signs that the deal may not serve you.

10. What are cheaper alternatives to a structured settlement cash advance?

Before a structured settlement cash advance, price a fixed personal loan, a partial sale, debt consolidation, or nonprofit credit counseling. A 2026 personal loan near 12% APR keeps your settlement intact, while a partial sale surrenders only some payments. These options usually cost far less than selling your entire future income stream.

11. Do I pay taxes on the lump sum from selling my payments?

The original payments in a structured settlement cash advance are often tax-free, but the lump sum’s treatment can differ from those scheduled payments. The 40% excise tax under IRC Section 5891 falls on the buyer, not you, yet your own tax outcome depends on your situation, so confirm it before signing.

The bottom line before you sign

A structured settlement cash advance is legal, court-supervised, and almost always expensive. You trade a known stream of future payments for a lump sum that reflects only their discounted value today.

The math rarely favors the seller, and most people who feel cornered into selling have a cheaper option they have not yet priced.

Before you contact a single buyer, get one personal-loan quote, speak with a nonprofit credit counselor, and ask whether a partial sale would solve the problem. If you still choose to sell, bring an independent attorney and tax professional you selected yourself.

Your settlement was designed to protect your future income. Treat any offer to cash it out early with the scrutiny that protection deserves.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.