A CFA’s Honest Look at Selling a Structured Settlement

Selling a structured settlement means accepting 50–80 cents per dollar — and the buyer keeps the rest permanently. A CFA explains the math and when the trade is worth it.

In This Article

Why Selling a Structured Settlement Is a Bigger Decision Than It Looks

The offer will look like rescue money — and it may cost you more than $24,000.

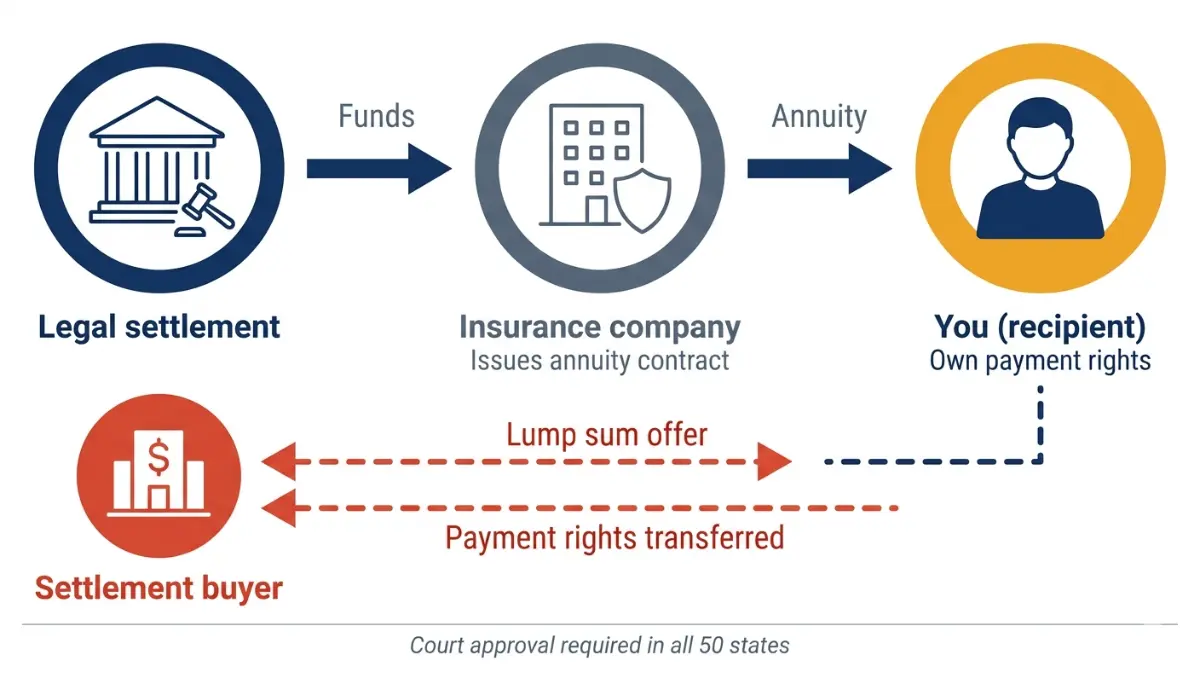

A sell structured settlement transaction is a permanent, court-supervised transfer of your future payment rights to a third-party buyer at a significant discount. The buyer profits from that spread; you receive liquidity now. Before you evaluate any offer, use our salary calculator to establish your actual annual income — the gap driving this decision is often smaller than the pressure makes it feel.

What this article covers — and what it won’t sell you

Finance Authority Hub has no commercial relationship with any structured settlement buyer. Michael R. Thompson, CFA, authored this guide with one purpose: to give you the same analysis a credentialed capital markets professional would deliver to a paying client before anyone signs anything.

The one number most settlement holders never calculate before signing

Most people skip a step that changes everything: calculating the actual monthly dollar gap between income and need. Use our take-home pay calculator to confirm your real net monthly income before treating a lump sum as the only available solution.

What a Structured Settlement Is and What You’re Actually Selling

Knowing exactly what you legally own — and what you don’t — is the difference between a negotiated sale and an exploited one.

A structured settlement is a legal compensation agreement delivering payments over time, typically arising from a personal injury or workers’ compensation claim. Those payments are funded by an annuity contract — but the annuity is owned by the issuing insurance company, not by you. What you hold is the contractual right to receive the payments that contract generates. Understanding how annuities work before engaging any buyer is the fastest way to avoid a preventable loss.

📊 Data Point: The National Structured Settlements Trade Association (NSSTA) estimates that US structured settlement payment obligations exceed $9 billion annually. The secondary market purchasing these payment rights is large, sophisticated, and consistently better-informed than individual sellers. Source: NSSTA, 2026.

How structured settlements are created and funded

A structured settlement originates when a defendant funds a qualified assignment — typically through a life insurance company — that issues an annuity to deliver the agreed periodic payments. The settlement agreement governs your right to receive payments; the annuity governs how they are generated. These are two separate legal instruments. Use our inflation calculator to see how fixed future payment amounts lose real purchasing power over time — a factor buyers price into every offer and sellers routinely underestimate.

Partial sales — why you may not have to sell everything

A partial sale assigns only specific payment dates — say, the next three to five years of payments — without surrendering the full stream. Most buyers do not lead with this option because full transfers generate larger profits. Knowing partial sales are legally available eliminates the false all-or-nothing framing built into most buyer conversations. For a complete breakdown of structured settlement types and payment structures, see the complete guide to structured settlements.

How to Sell a Structured Settlement: The 5-Step Legal Process

Selling a structured settlement involves five legally mandated steps — and it takes a minimum of 45–90 days in most states, not the quick cash that buyer advertising implies.

Step 1 — Request quotes from at least three buyers. Before contacting any buyer, use our loan calculator to determine whether a personal loan at a lower total cost covers the financial need entirely.

Step 2 — Negotiate the transfer agreement. The discount rate is negotiable at this stage and nowhere else. Use our APR calculator to convert any quoted discount rate into an annualized cost figure so you can compare it against borrowing alternatives on equal terms.

Step 3 — Sign the transfer agreement and file the court petition. The buyer files a transfer petition with a state court once you have signed. Do not sign without first having the agreement reviewed by a licensed attorney.

Step 4 — Attend the court hearing. A judge independently reviews whether the transfer serves your best interest — and has authority to reject the petition. The hearing typically occurs 30–60 days after the filing date.

Step 5 — Receive your lump sum. Funding follows the court order, with an additional 5–15 business days for the annuity issuer to process the transfer. Total elapsed time from Step 1 to funded proceeds: 45–90 days minimum.

⚠️ Warning: The mandatory court process exists to protect sellers from decisions made under financial duress. Any buyer claiming completion in fewer than 30 days is misrepresenting legal requirements that apply in every US state.

💡 Expert Note (CFA): In my experience reviewing structured settlement transactions, judges do reject transfer agreements they find economically unreasonable. The court hearing is not an obstacle — it is the most powerful consumer protection available to you in this transaction. Treat it accordingly.

Use our EMI calculator to estimate the monthly payment on a personal loan alternative before initiating Step 1 — if that payment is manageable, the transfer may be unnecessary. For a full overview of your consumer rights in a structured settlement transfer, the CFPB provides specific disclosure guidance that every buyer is legally required to follow.

The Real Cost of Selling: How Discount Rates Work and What You’ll Receive

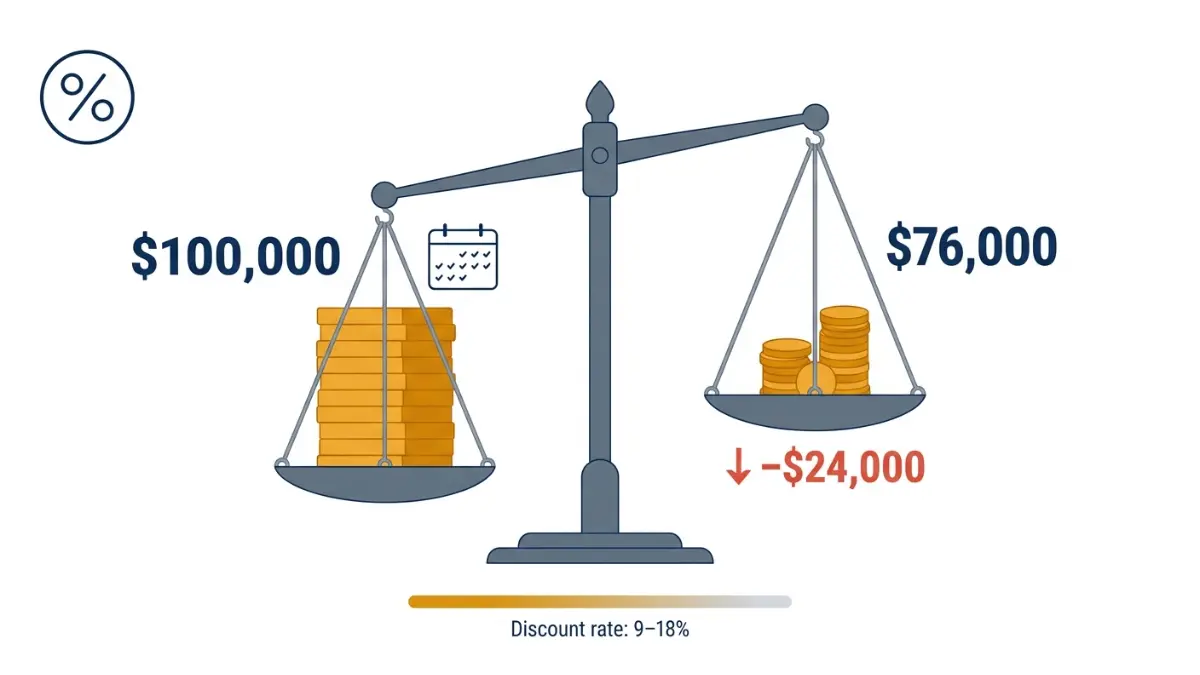

Sellers typically receive between 50–80 cents on the dollar when they sell a structured settlement — the exact figure determined by the discount rate the buyer applies, which ranges from 9–18% in the current 2026 rate environment.

What the discount rate actually means

The discount rate is not a fee. It is the annualized rate of return the buyer earns by purchasing your payment stream. A 12% discount rate means the buyer is pricing your payments at an internal rate of return of 12% — your effective cost of immediate liquidity. Use our percentage calculator to verify any rate figure a buyer presents to you in writing before you respond.

📊 Data Point: FINRA has identified structured settlement factoring as an area where individual sellers face consistent information asymmetry relative to sophisticated institutional buyers. Source: FINRA investor awareness guidance, 2026.

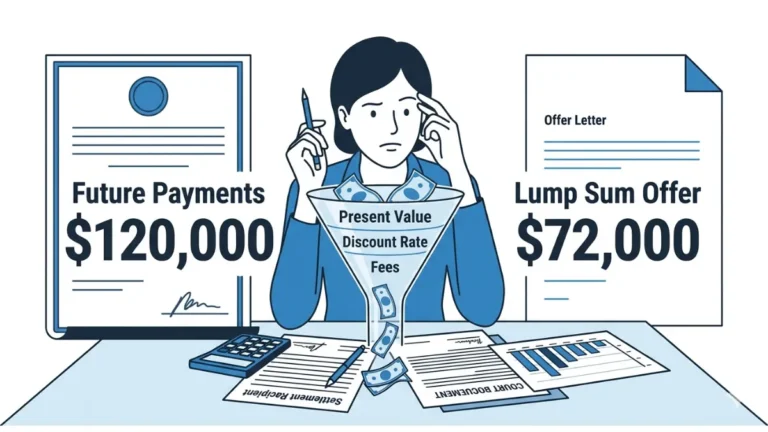

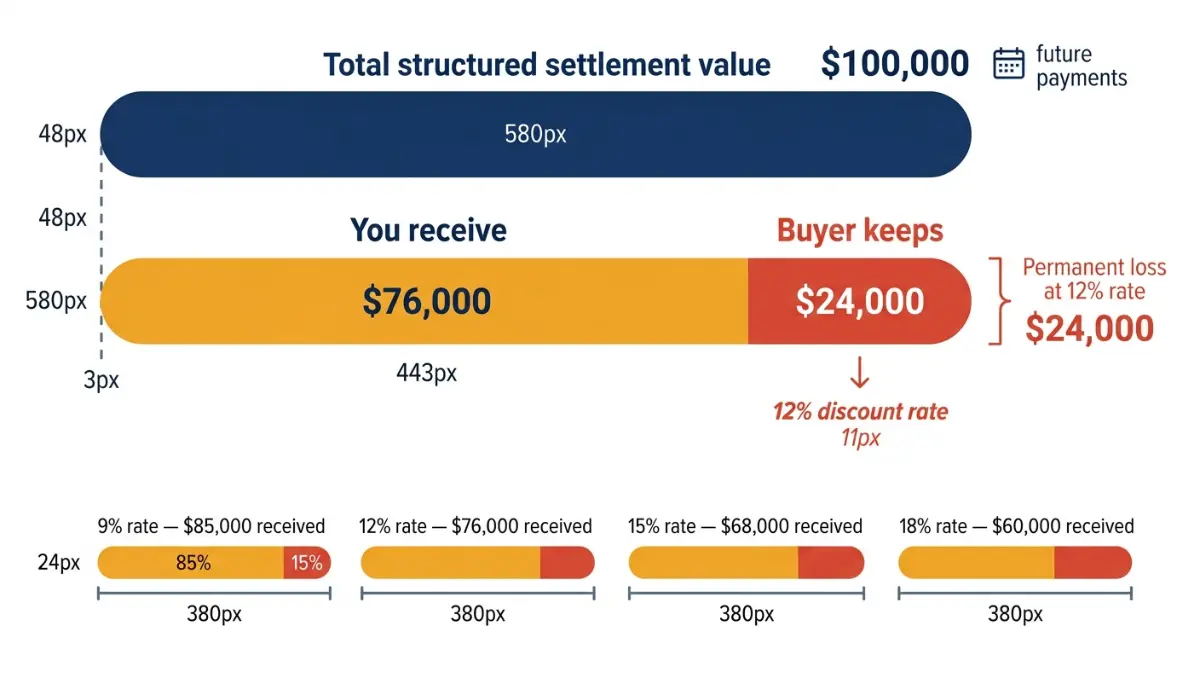

A real calculation: what $100,000 in future payments is worth today

| Discount Rate Applied | Estimated Lump Sum on $100,000 | Dollars Surrendered | Best For |

|---|---|---|---|

| 9% | ~$85,000 | ~$15,000 | Short payment streams; strong negotiating position |

| 12% | ~$76,000 | ~$24,000 | Median market offer; 15-year stream |

| 15% | ~$68,000 | ~$32,000 | Longer streams; weaker credit on issuing insurer |

| 18% | ~$60,000 | ~$40,000 | Long-duration streams; elevated market rates |

Figures are illustrative estimates. Actual values depend on payment schedule, remaining term, and buyer-specific pricing. Source: NSSTA, 2026.

Use our compound interest calculator to model what that same payment stream could grow to if held and conservatively reinvested. Use our investment calculator to compare lump sum deployment scenarios side by side before forming a view on whether selling makes financial sense.

How structured settlement buyers profit from the spread

Buyers collect the full face value of your payments from the annuity issuer over time. The spread between what they pay you and what they collect is their annualized return — 9–18%. Use our ROI calculator to calculate the buyer’s effective return at any quoted rate, then use our break even calculator to find the holding period at which keeping your payments outperforms the lump sum.

ℹ️ Disclaimer: The discount rate table above uses illustrative estimates for educational purposes. Actual transfer values depend on your payment schedule, remaining term, annuity issuer creditworthiness, state law, and individual buyer pricing. The figures above are not a guarantee of any specific offer. Consult a credentialed CFA or CFP before evaluating or accepting any structured settlement transfer agreement.

Sell or Hold? A CFA’s Neutral Decision Matrix for 2026

This is the section most structured settlement guides skip — a genuinely neutral analysis of when selling is the rational financial choice and when it is not.

💡 Expert Note (CFA): In 28 years of capital markets advisory work, the most costly mistake I see clients make is selling under time pressure without first exhausting lower-cost alternatives. I have worked with clients who surrendered more than $30,000 in future payment value to retire debt that a balance-transfer card or personal loan would have resolved at a fraction of that cost. That mistake is irreversible. This section is designed to prevent it.

Four financial situations where selling is the rational choice

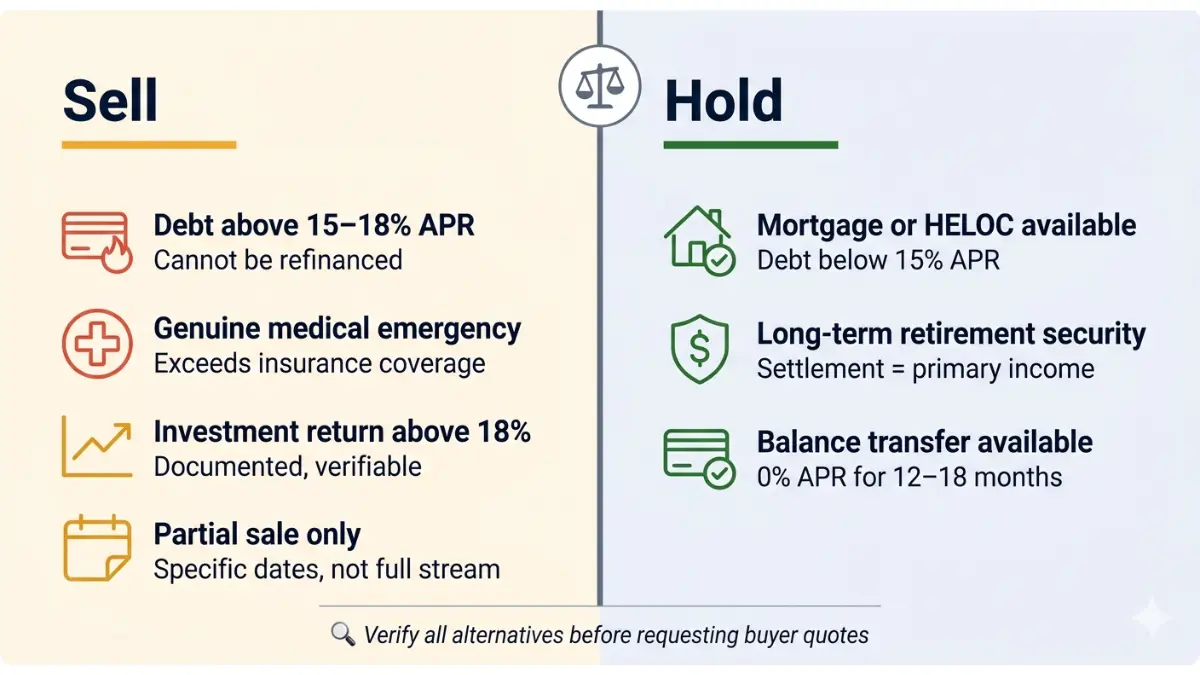

Selling a structured settlement may be the financially sound decision when:

- High-interest debt exceeds 15–18% APR and cannot be refinanced or consolidated — use our debt consolidation calculator first and explore debt consolidation strategies before treating a settlement sale as the default

- A genuine medical emergency creates a cash need that exceeds insurance coverage and all available credit options

- A time-sensitive investment with a documented, verifiable expected return meaningfully exceeds the 9–18% discount rate cost — use our amortization calculator to model any loan-funded alternative first

- A partial sale of a specific payment window addresses a defined shortfall without surrendering the entire stream

Three situations where holding almost always wins

Holding your structured settlement is the stronger financial choice when:

- Your debt carries an APR below 15% and can be addressed through personal loan or credit alternatives — use our credit card payoff calculator to model elimination without a transfer

- Your financial need is a housing goal — use our mortgage calculator to assess what a traditional mortgage covers before treating a settlement sale as a down payment source; see how to use home equity in 2026 if you already own property

- Your long-term retirement security depends on the ongoing income stream — use our retirement calculator, 401(k) calculator, and Roth IRA calculator to compare tax-advantaged accumulation alternatives alongside retirement savings benchmarks by age

Alternatives to selling — try these first

Before requesting a single buyer quote, work through this sequence:

- Calculate your debt-to-income ratio with our debt-to-income ratio calculator — lenders use 43% as a qualification ceiling, and knowing your number determines which credit-based alternatives remain available

- Model credit card debt elimination using credit card debt strategies — a 0% APR balance transfer may buy 12–18 months of payment-free debt reduction at no discount to your settlement

- Assess home equity availability with our home equity calculator — a HELOC at 7–9% costs dramatically less than the 12–18% effective rate on a settlement transfer

- Evaluate a mortgage refinance with our refinance calculator — if a cash-out refinance covers the need, your settlement remains fully intact

- Consider a business or investment loan using our business loan calculator — if the financial need is a business opportunity, purpose-specific financing may carry a lower effective cost

✅ Pro Tip — Complete Financial Calculator Toolkit for Settlement Sellers: Before your first buyer conversation, use these tools to model every alternative path your financial situation might support.

Housing: Mortgage Rate Calculator · Home Affordability Calculator · Down Payment Calculator · Closing Cost Calculator · Mortgage Refinance Calculator · Loan to Value Calculator · Rent vs. Buy Calculator

Retirement and savings: Social Security Calculator · CD Calculator · Savings Calculator · Dividend Calculator · Stock Calculator · College Savings Calculator

Auto and transportation: Auto Loan Calculator · Car Lease Calculator · Car Insurance Calculator

Income and employment: Overtime Calculator · Hourly to Salary Calculator · Paycheck Calculator

Education and loans: Student Loan Calculator

Insurance: Life Insurance Calculator

Property and tax: Property Tax Calculator · Sales Tax Calculator · Income Tax Calculator

Credit: Credit Score Calculator

General financial: Currency Converter · Percentage Calculator · Tip Calculator

ℹ️ Disclaimer: The sell/hold framework above reflects general financial analysis principles. Individual outcomes depend on payment schedule, credit profile, state law, and personal tax situation. This framework does not constitute personalized financial advice. Before accepting any offer, request at least three written quotes and have them reviewed by an independent fee-only CFP. The NAPFA directory lists fee-only advisors with no commission interest in your structured settlement decision. Consult a credentialed CFA or CFP before executing any transfer agreement.

Court Approval, State Laws, and Your Consumer Rights as a Seller

Selling a structured settlement without court approval is illegal in all 50 states — a mandatory consumer protection, not a procedural formality.

What the Structured Settlement Protection Act requires in your state

The Structured Settlement Protection Act (SSPA) is a state law, enacted in all 50 US states, requiring that a court approve any transfer of structured settlement payment rights before it is legally binding. A judge must independently determine the transfer serves the seller’s best interest — and has authority to reject the petition. Key state variations: California mandates a 10-day disclosure period; Florida provides a 3-day right of rescission after signing.

📊 Data Point: The CFPB confirms that sellers retain significant legal rights throughout the court approval process, including the right to rescind before a court order is issued. Source: CFPB consumer guidance on structured settlement transfers, 2026.

Tax treatment — what’s protected and what may not be

Original structured settlement payments for personal physical injury are excluded from federal income tax under IRS Section 104(a)(2). The lump sum received in a secondary-market transfer has been subject to IRS scrutiny depending on how the transaction is characterized. Use our capital gains tax calculator if any portion of your proceeds may be characterized as a taxable gain. For the authoritative guidance, see IRS Publication 4345 on the tax treatment of compensatory damages. For a comprehensive overview of structured settlement tax rules, see our guide to structured settlement payment taxation.

ℹ️ Disclaimer: IRS Section 104(a)(2) excludes original personal injury settlement payments from federal income tax. The tax treatment of proceeds from a secondary-market transfer may differ based on transaction characterization and individual circumstances. This content does not constitute tax or legal advice. Consult a CPA or enrolled agent regarding tax implications. Consult a licensed attorney familiar with your state’s SSPA regarding all legal requirements before signing any transfer agreement.

Your Next Step: What a CFA Would Do Before Signing Anything

The decision to sell a structured settlement is one of the few financial moves that cannot be undone once a court order is issued.

The three things to do before you request a single quote

Complete this sequence before contacting any buyer:

- Map your actual monthly budget with our budget calculator — confirm the exact dollar gap between income and financial need

- Run every alternative scenario from the debt, equity, and refinancing options in Section 5 above

- Request three written quotes and have them independently reviewed by a fee-only CFP before negotiating anything

If you decide to sell — what to negotiate and what to document

The discount rate is the single most negotiable element of any transfer offer. A 1% rate reduction on a $200,000 settlement recovers more than $5,000 in lump sum proceeds. Get every figure in writing, with the discount rate stated explicitly as a percentage, before any counter-offer.

💡 Expert Note (CFA): The difference between a 9% and a 15% discount rate on $200,000 in future payments exceeds $50,000 in surrendered value. Never accept a first offer. Never sign without independent review. Use our savings calculator to see what those recovered proceeds could grow to if invested — that comparison is the most powerful negotiating motivation available.

ℹ️ Disclaimer: Structured settlement transfer agreements are legally binding, court-supervised financial contracts. This article provides general financial education and does not constitute personalized financial, legal, or tax advice. Consult a credentialed CFA or CFP for financial guidance, a licensed attorney for all legal and court requirements, and a CPA for tax implications specific to your situation before executing any transfer agreement.

Structured Settlement FAQs: Questions Answered by a CFA

1. How much do you lose when you sell a structured settlement?

Sellers who sell a structured settlement typically receive 50–80 cents on the dollar, depending on the discount rate applied — usually 9–18% in 2026 — and the duration of remaining payments. A $100,000 settlement discounted at 12% yields approximately $76,000 today, meaning roughly $24,000 is surrendered permanently. Source: NSSTA, 2026. Consult a credentialed CFP or CFA before accepting any offer.

2. What is the discount rate for structured settlements?

The discount rate is the annualized rate of return a buyer applies when pricing your future payment stream. In 2026, rates typically range from 9–18%, with longer-duration streams commanding higher rates due to the buyer’s extended capital commitment. The rate is not fixed by law and is negotiable if you hold competing written offers simultaneously. Source: NSSTA, 2026.

3. How long does it take to sell a structured settlement?

Selling a structured settlement takes a minimum of 45–90 days in most US states, driven by mandatory court approval under individual state Structured Settlement Protection Acts. Some states impose additional waiting periods — California requires 10 days from initial disclosure; Florida mandates a 3-day rescission window. Buyer advertising claiming faster timelines misrepresents statutory legal requirements. Source: NSSTA, 2026.

4. Is selling a structured settlement a good idea?

Selling a structured settlement is the rational choice in four specific circumstances: debt carrying an APR above 15–18% that cannot be refinanced, a genuine medical emergency exceeding all available credit, a time-sensitive investment with a verifiable return above the discount rate cost, or a partial sale addressing a defined shortfall. In all other circumstances, alternatives should be exhausted first. Consult a credentialed CFP before deciding.

5. What are the tax implications of selling a structured settlement?

Original structured settlement payments for personal physical injury are excluded from federal income tax under IRS Section 104(a)(2). The lump sum received in a secondary-market transfer may be characterized differently by the IRS depending on transaction structure. Consult a CPA or enrolled agent before completing any transfer. Source: IRS Publication 4345.

6. Can you sell part of your structured settlement?

Yes — a partial structured settlement sale assigns only specific payment dates, such as the next three years of payments, without surrendering the full stream. This option is legally available in all states that permit transfers under their SSPAs. Most buyers do not volunteer this option because full transfers generate larger profits. Consult a licensed attorney to structure a partial transfer agreement correctly.

7. What companies buy structured settlements?

The largest structured settlement buyers include JG Wentworth, Peachtree Financial Solutions, Novation Settlement Solutions, and CBC Settlement Funding. Finance Authority Hub does not endorse any specific buyer. Request written quotes from at least three companies and have all offers independently reviewed by a fee-only CFP or CFA before negotiating or signing any transfer agreement.

8. How does court approval work for selling a structured settlement?

The buyer files a transfer petition with a state court after you sign the transfer agreement. A judge reviews whether the structured settlement transfer is in your best interest — and can reject it. The hearing typically occurs 30–60 days after filing. Source: CFPB consumer guidance. Consult a licensed attorney before signing any transfer agreement.

9. What is the difference between a structured settlement and an annuity?

A structured settlement is a legal compensation agreement delivering periodic payments arising from a legal claim. It is funded by an annuity contract — but the annuity is owned by the issuing insurance company, not the payment recipient. The settlement holder owns the contractual right to receive payments, not the annuity itself — a legally significant distinction in any transfer transaction.

10. Can you sell a workers’ comp structured settlement?

Workers’ compensation structured settlements face significantly different rules than tort settlements. Most US states restrict or outright prohibit the transfer of workers’ comp payment rights. The SSPAs that permit structured settlement transfers typically apply to personal injury tort settlements only. Consult a licensed attorney before engaging any buyer regarding workers’ compensation payment rights in your state.

11. What happens to a structured settlement when you die?

The outcome depends on the terms of the original settlement agreement and the funding annuity contract. Some structured settlements include a guarantee period under which remaining payments transfer to a named beneficiary. Others terminate at the recipient’s death. Review both documents with an estate attorney and use our life insurance calculator to evaluate whether additional estate protection is warranted.

12. How do structured settlement buyers make money?

Structured settlement buyers purchase your future payment rights at a discount — typically 9–18% annualized — then collect the full face value of those payments from the annuity issuer over time. The spread between what they pay you and what they ultimately collect is their return on investment. This is a legal, regulated secondary-market transaction governed by individual state SSPAs and court oversight.

13. Is there a penalty for selling a structured settlement?

There is no IRS penalty for selling a structured settlement through a court-approved transfer under current law. The economic cost is the discount rate itself — 9–18% — which represents the true price of immediate liquidity, not a legal penalty. Court filing fees and administrative costs typically add $500–$2,000 to the transaction. Source: NSSTA, 2026. Consult a licensed attorney regarding court costs specific to your state.

14. What is my structured settlement worth?

The present value of your structured settlement depends on total remaining payments, the payment schedule, and the discount rate a buyer applies. As a working estimate: $100,000 in future payments discounted at 12% over 15 years equals approximately $76,000 today. Always obtain three written quotes before accepting any valuation. Consult a credentialed CFA for an independent present value analysis before negotiations begin.

15. Can you negotiate the discount rate on a structured settlement?

Yes — the discount rate in a structured settlement sale is negotiable. Holding written quotes from at least three buyers creates competitive pressure that consistently lowers offered rates. A 1% rate reduction on a $100,000 settlement recovers approximately $2,000–$5,000 in proceeds. Always negotiate before signing. Never accept a first offer as final. Consult a CFP or CFA before any counter-offer. Source: NSSTA, 2026.

16. What is the Structured Settlement Protection Act?

The Structured Settlement Protection Act (SSPA) is a state law enacted in all 50 US states requiring that a court approve any transfer of structured settlement payment rights before it becomes legally binding. A judge must determine the transfer is in the seller’s best interest. Source: CFPB consumer guidance. Consult a licensed attorney for your state’s specific SSPA requirements.

17. How do I get out of a structured settlement?

Exiting a structured settlement means selling some or all of your payment rights through a court-approved factoring transaction. The process requires a signed transfer agreement, a court petition, a judicial hearing, and a court order — a minimum of 45–90 days in most states. Any offer claiming a faster or court-free exit is a serious red flag requiring immediate verification by a licensed attorney before further engagement.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.