Understanding the Types of Annuities Before You Buy

The types of annuities aren’t interchangeable: fixed locks a rate, variable rides the market, indexed caps gains behind a 0% floor. Here’s which fits.

In This Article

If you’re holding a 401(k) rollover, a maturing CD, or a lump sum and an agent has put an annuity in front of you, the first job is telling the three main types apart before you commit money you may not easily get back. Whether you’re a pre-retiree comparing income options, someone who just received a large sum, or a self-employed saver chasing tax-deferred growth, the choice comes down to how much market risk you want and how much you’re willing to pay for protection.

There are three main types of annuities:

- Fixed annuity — the insurer guarantees a set interest rate for a term. Best for predictability and CD-like savers.

- Variable annuity — your money rides the market through investment sub-accounts. Best for growth-seekers comfortable with risk and higher fees.

- Indexed annuity — returns track a market index but are capped, with your principal protected in down years. Best for a middle ground between the two.

The rest of this guide explains how each one works, what each really costs, how each is taxed, and which fits which situation.

ℹ️ Financial Disclaimer: This article is for general educational purposes only and is not investment, tax, insurance, or legal advice. Annuities are long-term insurance contracts whose fees, surrender charges, crediting rates, and tax treatment vary by product, state, and personal circumstances, and the figures cited reflect the sources and dates shown and can change. Before purchasing, exchanging, or surrendering any annuity, consult a fiduciary financial advisor and a qualified tax professional (a CPA or tax attorney).

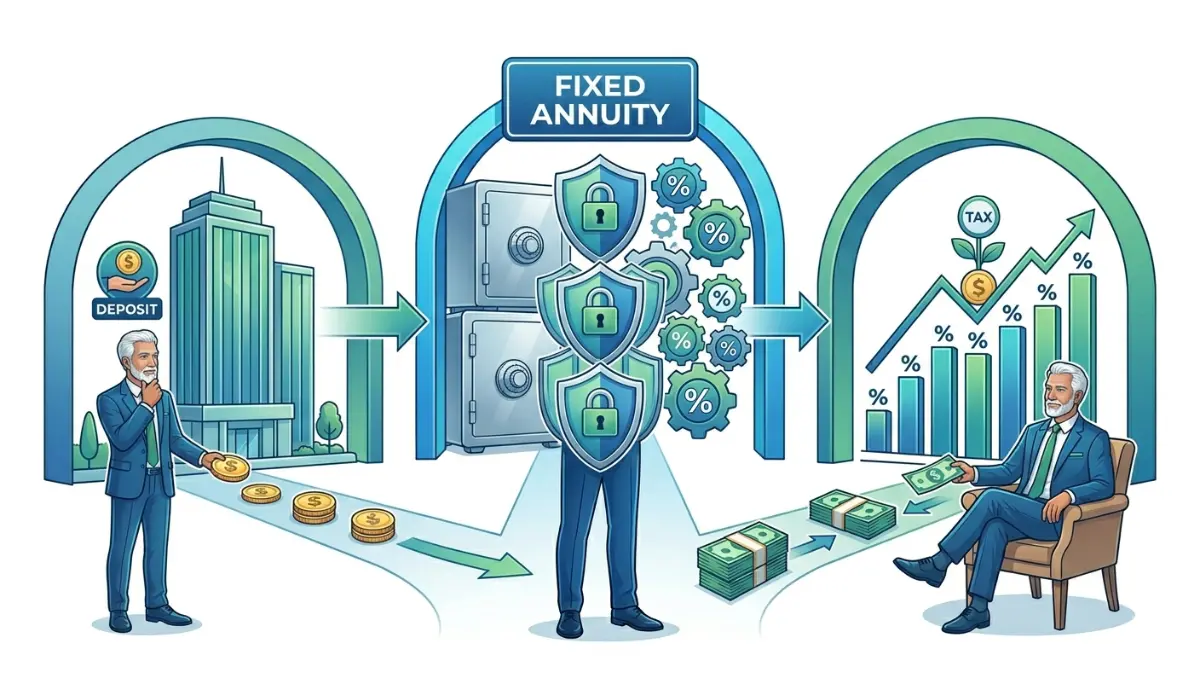

How a fixed annuity works

A fixed annuity is the simplest of the three: you hand an insurance company a premium, and it guarantees a set interest rate for a defined term, commonly 2 to 10 years. The most common version sold today is the multi-year guaranteed annuity (MYGA), often described as the “CD of the annuity world” because the rate is locked and the principal doesn’t move with markets. Growth is tax-deferred, meaning you owe no tax on the interest until you withdraw it, per IRS Publication 575.

What rate can you expect? As of June 2026, top MYGA contracts from A-rated insurers generally pay around 5.0% to 5.75%, with the highest rates across the broader market near 6.3% to 6.5%, depending on term and the insurer’s rating (rates from carrier-comparison aggregators; verify the live rate before buying, as these reset weekly and are not guarantees). These yields sit near multi-year highs in part because the Federal Reserve held its policy rate at 3.50%–3.75% at its April 2026 meeting.

📊 Data Point: The Federal Reserve’s federal funds target range was held at 3.50%–3.75% at the April 28–29, 2026 meeting, with the next decision scheduled for June 16–17, 2026 — Source: the Federal Reserve’s record of policy operations.

One honest caveat: a fixed annuity is backed by the insurer’s claims-paying ability, not the FDIC, and state guaranty-association coverage has limits. You can model tax-deferred growth over your time horizon, compare what a similar-term CD would pay, or look at how Treasury bills work as another principal-protected option before deciding.

How a variable annuity works

A variable annuity trades the fixed guarantee for market exposure. Your premium goes into sub-accounts — investment options that work much like mutual funds holding stocks, bonds, or money-market instruments — and the contract’s value rises and falls with their performance. Unlike a fixed annuity, you bear the investment risk, and the value can drop.

Because the value is tied to securities, variable annuities are registered with the SEC and sold with a prospectus, and they’re regulated by both the SEC and FINRA. That structure matters because it determines the disclosures you’re entitled to before signing.

🔍 How It Works: A variable annuity stacks several fees. According to the SEC’s investor bulletin on variable annuities, you typically pay a mortality and expense (M&E) risk charge, plus administrative fees (the SEC’s examples cite roughly 0.15% a year), plus the operating expenses of each underlying fund — and any optional income or death-benefit rider adds more on top.

The appeal is uncapped growth potential and tax-deferred compounding; the trade-off is layered cost and real downside risk. As with all annuities, earnings are eventually taxed as ordinary income when withdrawn, not at capital-gains rates.

✅ Action Step: Before buying a variable annuity, ask a fiduciary financial advisor one specific question — “What is the all-in annual cost of this contract, including M&E, admin, fund expenses, and every rider?” — and read the prospectus fee table line by line.

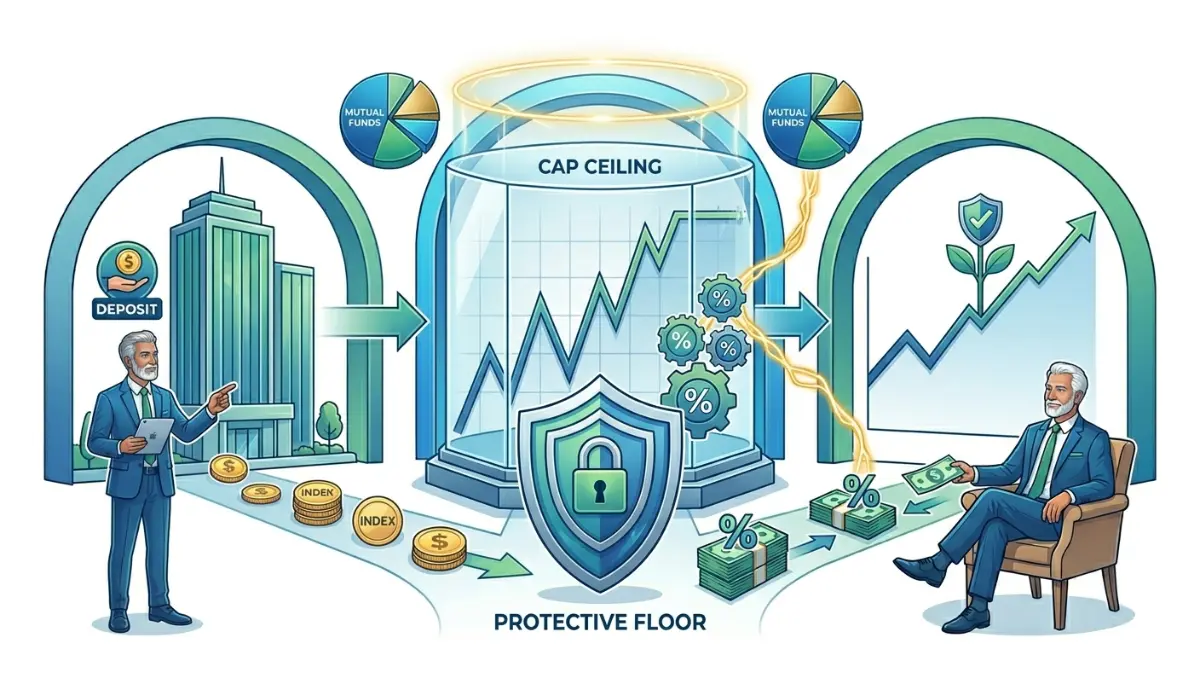

How an indexed annuity works

An indexed annuity sits between fixed and variable: your return is linked to a market index such as the S&P 500, but it’s limited by the contract’s crediting rules, and a floor protects your principal when the index falls. The most common version, the fixed indexed annuity (FIA), is an insurance product regulated by state insurance departments and typically carries a 0% floor — so a down market year credits zero rather than a loss.

🔍 How It Works — caps, participation rates, and spreads. Per the SEC’s bulletin on indexed annuities, three levers limit your credited return. A cap rate sets the maximum (a 7% cap on a 12% index gain credits 7%); a participation rate credits only a share of the gain (a 75% rate on a 10% gain credits 7.5%); and a spread subtracts a set percentage (a 3% spread on a 9% gain credits 6%).

Here is the same 10% index year credited three different ways, using the SEC’s formulas (our calculation):

| Crediting method | Contract term | Index gain | Credited to you |

|---|---|---|---|

| Cap | 7% cap | 10% | 7% |

| Participation rate | 75% participation | 10% | 7.5% |

| Spread | 3% spread | 10% | 7% |

Source: crediting formulas from the SEC’s Updated Investor Bulletin: Indexed Annuities; arithmetic is the editorial team’s own. When a contract combines features — say, a 75% participation rate and a 3% spread — the limits stack, so a 10% index year credits 4.5% (7.5% minus 3%).

💡 Expert Note: FINRA cautions that insurers can reset caps, participation rates, and spreads at each anniversary, and that most indexed annuities exclude index dividends from the calculation — both of which can quietly lower your real return. FINRA’s guide to the risks of indexed annuities details these tradeoffs.

As of mid-2026, competitive FIA caps on S&P 500 annual point-to-point strategies have run roughly 9% to 12%, with uncapped volatility-controlled options offering participation rates near 55% to 75% (aggregator data; confirm current rates before buying). A separate, securities-registered cousin — the registered index-linked annuity (RILA) — uses a buffer instead of a hard floor and can lose value, which is why it’s regulated by the SEC.

✅ Action Step: Ask the agent to put the current cap, participation rate, and spread in writing, along with the contract’s reset history, and have a fiduciary advisor confirm exactly which crediting method applies.

Fixed vs. variable vs. indexed: which fits you?

The clearest way to choose is to line the three types up against the factors that actually affect your money: how the return is generated, what happens to your principal, the main cost, and the kind of saver each suits.

| Annuity type | How returns work | Your principal | Main cost | Best for |

|---|---|---|---|---|

| Fixed (MYGA) | Guaranteed rate for a set term | Protected (insurer-backed) | Usually no explicit annual fee | Predictability; CD-style savers |

| Variable | Market sub-accounts; value floats | Can lose value | M&E + admin + fund + rider fees | Growth-seekers OK with risk and cost |

| Indexed (FIA) | Index-linked, limited by cap/participation/spread | Protected by a 0% floor | Caps/spreads reduce upside (not a stated fee) | A middle ground between the two |

Sources: product mechanics and fees per the SEC’s variable- and indexed-annuity bulletins; tax treatment per IRS Publication 575. Rate specifics appear in the sections above and should be re-verified before purchase.

So which type of annuity is “safest”? It depends on which risk you mean. A fixed or indexed annuity protects your principal from market losses, but a fixed annuity leaves you exposed to inflation risk over a long term, while a variable annuity exposes your principal to market risk in exchange for higher growth potential.

And fixed versus indexed — which is better? If you want a known, locked rate and simplicity, fixed wins; if you’ll trade a guaranteed rate for capped market-linked upside with downside protection, indexed may fit. Neither is right for everyone, and the deciding variables are your time horizon, your need for liquidity, and your tolerance for complexity.

✅ Action Step: Match the type to your time horizon and liquidity needs with a fiduciary advisor, and ask one specific question — “How would surrender charges and any market value adjustment apply if I need this money in year three?”

What annuities really cost — fees, surrender charges, and taxes

The headline rate is rarely the full story; annuity fees and tax rules decide what you actually keep. Fixed MYGAs usually carry no explicit annual fee, variable annuities layer M&E, administrative, fund, and rider charges, and indexed annuities limit your upside through caps and spreads rather than a stated fee.

🔍 How It Works — surrender charges. Most annuities lock your money for a surrender period of about 6 to 10 years. The SEC’s example describes a surrender charge starting at 7% in the first year and declining roughly one percentage point each year, while letting you withdraw about 10% of the contract value penalty-free annually; some fixed and indexed contracts also apply a market value adjustment to early withdrawals.

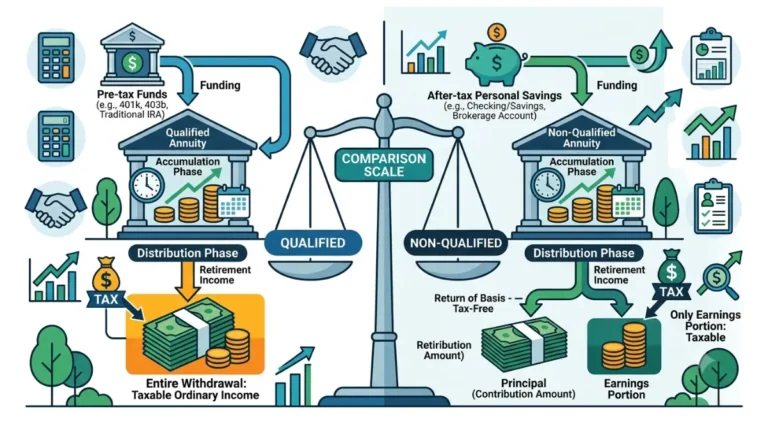

On taxes, the core rule from IRS Publication 575 is that growth is tax-deferred and withdrawn earnings are taxed as ordinary income, not at the lower long-term capital gains rates. How much of a withdrawal is taxable depends on whether the annuity is qualified or non-qualified.

A non-qualified annuity (bought with after-tax dollars) is taxed last-in, first-out: your earnings come out first and are fully taxable, then your original principal comes out tax-free. A qualified annuity (held inside a pre-tax account like a traditional 401(k)) has 100% of withdrawals taxed as ordinary income, whereas a Roth IRA’s tax-free withdrawals follow different rules entirely.

For illustration, mechanics per IRS Publication 575: if a $100,000 after-tax premium grows to $200,000 and you annuitize, the exclusion ratio treats about half of each payment as a tax-free return of principal and half as taxable income until your principal is recovered.

⚠️ Costly Mistake: Withdrawing before age 59½ generally triggers a 10% additional federal tax — but only on the taxable (earnings) portion, per IRS Publication 575 — on top of any surrender charge. Stacking an early surrender charge, a market value adjustment, and the 10% penalty can erase a meaningful slice of your money. See IRS Publication 575 for the exceptions.

✅ Action Step: Before withdrawing or annuitizing, confirm your specific tax outcome with a CPA, and ask the carrier for your contract’s exact surrender schedule and whether a market value adjustment applies.

Common annuity mistakes to avoid

Annuities aren’t inherently good or bad, but a few avoidable errors cause most of the regret — and most are about cost and access, not the product itself.

The most common mistake is buying before understanding the full cost, especially on variable contracts where rider fees can stack on top of M&E and fund expenses. The second is ignoring the surrender period and tying up money you may need within 6 to 10 years.

Can you lose money in an annuity? In a variable annuity, yes — if your sub-accounts fall, so does your value. A fixed indexed annuity’s 0% floor protects principal from market losses, and a fixed annuity’s rate is guaranteed by the insurer, though all of these rest on the insurer’s claims-paying ability and state guaranty limits rather than FDIC insurance.

⚠️ Costly Mistake: Treating an indexed annuity’s headline cap as a permanent rate. FINRA notes insurers can reset caps and participation rates lower after the first year, so a 10% cap today can be materially lower at the next anniversary.

✅ Action Step: Use a simple test before signing — if the agent can’t clearly explain the fees, the surrender schedule, and how your rate is credited in plain language, treat that as a stop sign and get an independent fiduciary advisor’s read first.

Frequently asked questions about types of annuities

1. What are the three main types of annuities?

The three main types of annuities are fixed, variable, and indexed. A fixed annuity pays a guaranteed rate set by the insurer; a variable annuity invests in market sub-accounts whose value can rise or fall; and an indexed annuity links returns to a market index, capped on the upside but protected by a floor on the downside.

2. Which type of annuity is safest?

It depends on which risk concerns you. Fixed and indexed annuities protect your principal from market losses, while a variable annuity puts principal at market risk. But a fixed annuity carries inflation risk over long terms, and all annuity guarantees rest on the insurer’s claims-paying ability. Discuss the tradeoff with a fiduciary advisor.

3. How does a fixed annuity work?

A fixed annuity, usually sold as a MYGA, guarantees a set interest rate for a term of roughly 2 to 10 years, with tax-deferred growth. As of June 2026, top contracts from A-rated insurers paid around 5.0% to 5.75%. Rates change weekly, so confirm the current figure and consult a financial professional before buying.

4. Are variable annuities a good investment?

A variable annuity offers uncapped, market-linked growth and tax deferral, but it carries real downside risk and layered fees — a mortality and expense charge, administrative fees, fund expenses, and any rider costs. Whether it fits depends on your risk tolerance and the all-in annual cost. Review the prospectus fee table with a fiduciary advisor first.

5. How does an indexed annuity work?

An indexed annuity credits interest tied to a market index, limited by a cap, a participation rate, and/or a spread, with a 0% floor protecting principal in down years. For example, a 7% cap credits 7% even if the index gains 12%. The SEC notes insurers can reset these rates, so confirm terms with a financial professional.

6. What are the fees on an annuity?

Fixed MYGAs usually have no explicit annual fee. Variable annuities carry a mortality and expense (M&E) risk charge, administrative fees (about 0.15% a year per SEC examples), underlying fund expenses, and optional rider fees. Indexed annuities limit upside through caps and spreads rather than a stated fee. Ask for the all-in cost and consult a fiduciary advisor.

7. How are annuities taxed?

Annuity growth is tax-deferred, and withdrawn earnings are taxed as ordinary income, not at capital-gains rates, per IRS Publication 575. Non-qualified annuities are taxed earnings-first (last-in, first-out); qualified annuities have 100% of withdrawals taxed. Withdrawals before age 59½ generally add a 10% federal tax on the taxable portion. Confirm your situation with a CPA.

8. What is a surrender charge on an annuity?

A surrender charge is a fee for withdrawing more than the penalty-free amount during the surrender period, typically 6 to 10 years. The SEC describes a schedule starting near 7% in year one and declining about one point a year, with roughly 10% of the contract value available penalty-free annually. Ask your carrier for the exact schedule before buying.

9. Can you lose money in an annuity?

Yes, in a variable annuity, where falling sub-accounts reduce your value. A fixed indexed annuity’s 0% floor protects principal from market losses, and a fixed annuity’s rate is insurer-guaranteed. All annuity guarantees depend on the insurer’s claims-paying ability and state guaranty limits, not FDIC insurance. Review the contract’s risk terms with a fiduciary advisor.

10. Fixed vs. indexed annuity — which is better?

If you want a known, locked rate and simplicity, a fixed annuity wins. If you’ll trade a guaranteed rate for capped market-linked upside with downside protection, an indexed annuity may fit. The deciding factors are your time horizon, liquidity needs, and tolerance for complexity. Neither suits everyone, so confirm the fit with a fiduciary advisor.

11. What is the difference between a fixed indexed annuity and a RILA?

A fixed indexed annuity (FIA) has a 0% floor, so a down market credits zero rather than a loss, and it’s regulated by state insurance departments. A registered index-linked annuity (RILA) uses a buffer instead of a hard floor and can lose value, which is why it’s an SEC-registered security. Discuss which structure fits with a financial professional.

Choosing the right type of annuity

The decision really reduces to one tradeoff: a fixed annuity buys predictability, a variable annuity buys market upside at the cost of fees and risk, and an indexed annuity buys a capped middle ground with principal protection. None is universally best — the right fit follows your time horizon, your need for access to the money, and how much complexity you’re willing to manage.

Before you sign anything, map where an annuity sits in your wider plan. You can see how an annuity fits your retirement income plan and check it against typical retirement savings benchmarks by age, then confirm the specific product with a fiduciary advisor and a CPA before committing.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.